JBL - Jabil Lowers 2024 Revenue Outlook: We Reiterate Buy

2023-11-29 07:45:47 ET

Summary

- Jabil lowers its fiscal 2024 revenue outlook, citing softer demand and inventory corrections as reasons for downward revision.

- Despite lower revenue outlook, Jabil expects to maintain operating margin within previously provided guidance range, which matters the most.

- Jabil's long-term growth prospects remain intact, we reiterate our Buy rating.

What Happened?

On November 28, 2023, Jabil ( JBL ) updated its fiscal 2024 outlook, which was below market expectations. The company cited softer demand and inventory corrections as the main reasons for the downward revision.

Below are the key points from the announcement:

- FY 2024 Q1 Revenue Guidance Update : Jabil expects Q1 revenue to fall within the $8.3 billion - $8.4 billion range instead of $8.4 billion – $9.0 billion.

- FY 2024 Q2 Revenue Guidance Update : The revenue is forecasted to range from $7.0 billion to $7.6 billion, as the company anticipates the inventory rebalancing to continue until then.

- FY 2024 Full Year Revenue Guidance Update : The company forecasts a revenue of approximately $31 billion, which is 7% lower than the previous guidance.

- FY 2024 Operating Margin Update : The company maintains its previous guidance of core operating margin between 5.3% and 5.5%, with EPS exceeding $9.00 for FY 2024.

The market reacted negatively to the FY 2024 outlook update, sending the stock price down by almost 10% during afterhours. In this article, we want to look at the situation and re-examine Jabil’s valuation based on the updated guidance and explain why we still believe that the company is a good investment opportunity.

Our previous article from a month ago provides a more detailed analysis and valuation of Jabil’s business.

Why Jabil's Margin Performance Matters More Than Its Revenue Guidance

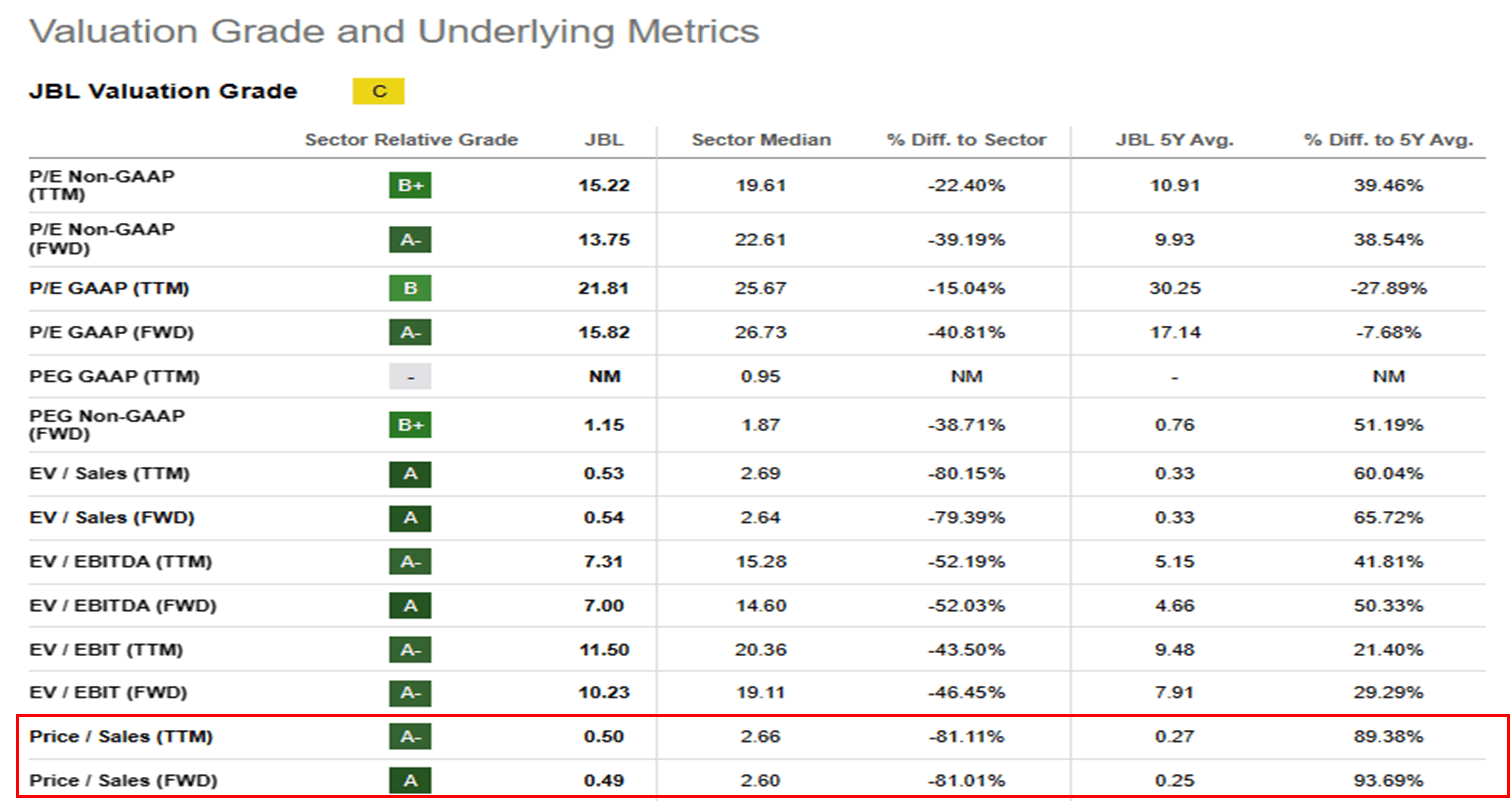

We want to explain why Jabil’s revenue guidance update does not change our positive view on the company, and why we focus on its margin performance as the key driver of its valuation. The valuation of EMS (Electronics Manufacturing Services) companies like Jabil is not driven by their sales multiples, so a lower revenue guidance does really not affect Jabil’s worth significantly. Jabil already has a very low sales multiple of 0.49 (see below) which implies that the market doesn't really value its revenue highly. Therefore, Jabil’s revenue update has a limited impact on its valuation, as the market is more concerned about its profitability and earnings potential.

A similar situation occurred during FY2023 Q4 earnings release, when Jabil’s revenue fell short of the estimates by $50M. However, the stock soared 15% the next day, due to the EPS beat and improved margins outlook.

Jabil Valuation Metrics (Seeking Alpha)

{kind=link}

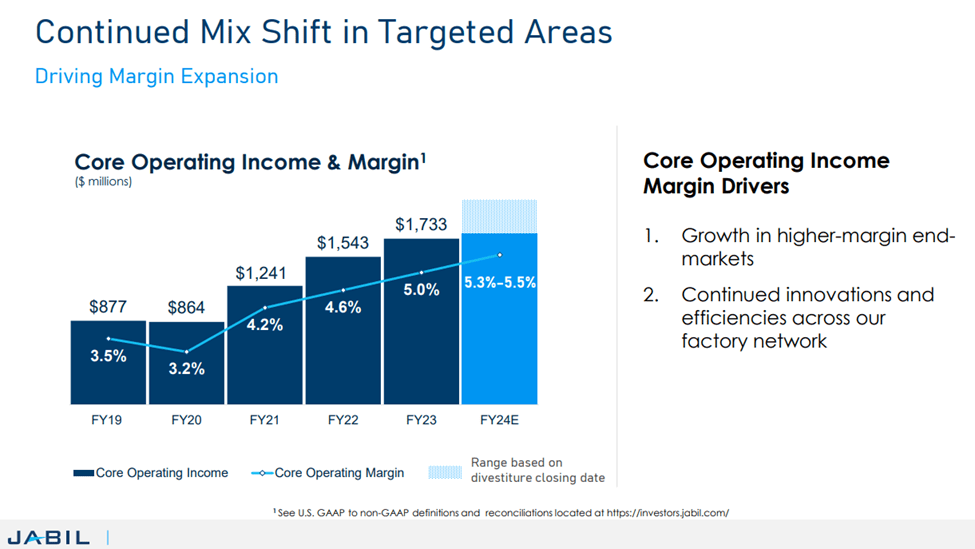

The key valuation multiple for Jabil is the P/E which reflects it profitability and operating margin. Jabil has been improving its core operating margin over the past few years, from 3.5% in FY2019 to 5.0% in FY 2023 (see below)

The good news about this updated outlook is that the company still expects to maintain its core operating margin within the previously provided guidance range of 5.4% for FY 2024, despite the lower revenue outlook. We believe that this is the most important metric to evaluate Jabil’s performance.

FY 2023 Q4 Earnings Presentation (Jabil)

{kind=link}

Valuation Update

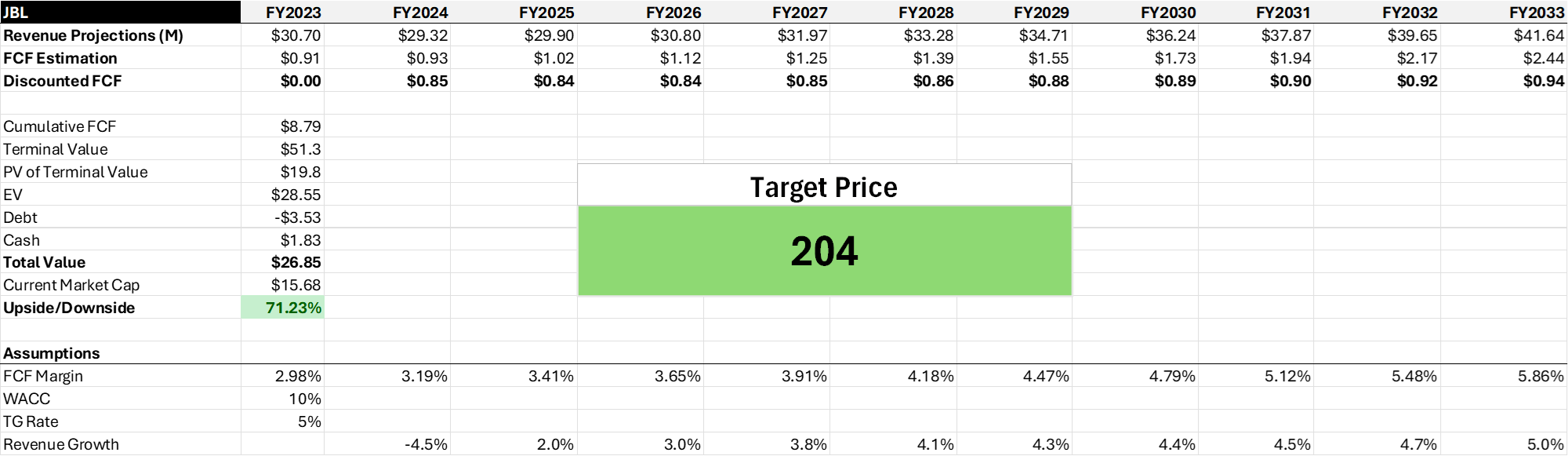

Our previous price target for Jabil was set at $220, reflecting Jabil's FY24 positive growth and margin guidance. Considering the adjusted revenue outlook, we have updated our previous DCF model with the lowered FY24 revenue target (-4.5%) and also decreased FY25 and FY26 revenue estimates by 0.5% accordingly.

Assumptions: We use a 10% WACC to discount the future cash flows. We base our analysis on $30.7 billion as the FY 2023 revenue baseline, which excludes the divested Mobility business. We also exclude the Mobility business’s revenues and free cash flows ((FCF)) for FY 2024. We assume a gradual revenue increase up to 5% by FY 2033 and a 7% annual FCF margin increase, consistent with the margin expansion momentum. Moreover, we apply a 5% revenue CAGR as the terminal growth rate after the 10-year period.

{kind=link}

As a result, we are lowering Jabil’s price target from $229 to $204 and reiterate our Buy rating.

Conclusion

We believe that Jabil's long-term growth prospects remain intact, as the company has the ability to grow its margins and earnings in the future, despite the short-term headwinds.

Jabil's diversified portfolio, resilient business model, and technological expertise position it well for future growth and margin expansion. We remain bullish on Jabil's potential, and reiterate our Buy rating with a price target of $204.

For further details see:

Jabil Lowers 2024 Revenue Outlook: We Reiterate Buy