VOO - Jabil: On Fire Year-To-Date (+13%) And Still A Fantastic Value

Summary

- At pixel time, the stock of Jabil is up 13.6% this year, yet still trades with a forward P/E of only 9.3x.

- Florida-based JBL will likely be a prime beneficiary of the global trend to diversify and off-shore electronic manufacturing operations away from China.

- Free cash flow is growing as the company shifts to higher margin opportunities. As a result, earnings and FCF are growing faster than revenue.

- Jabil has a history of topping consensus EPS estimates, and did so again in its Q1 FY23. It's likely to do the same for Q2 and full-year 2023.

For whatever reason, and despite the company's consistent excellent financial and operational performance, my Seeking Alpha articles on Jabil ( JBL ) get some of the fewest page views of all the companies I cover on a consistent basis. I actually view the lack of public interest as a (bullish) contrary indicator and as such was not at all surprised to see the stock come bolting out of the starting gate this year to a 13%-plus rally, far outperforming the S&P 500 and Nasdaq-100 as represented by the ( VOO ) and ( QQQ ) ETFs (see below). Yet despite the rise in the share price, JBL still trades with a forward P/E of only 9.4x while generating strong free cash flow that's used to buy back the undervalued shares and significantly reduced the fully diluted outstanding share count.

JBL is a buy.

Investment Thesis

JBL operates two segments: Electronics Manufacturing Services ("EMS") and Diversified Manufacturing Services ("DMS"). Over the past couple of years, the company has been moving into fast-growing and higher-margin businesses such as Health Care & Packaging, Auto & Transportation (i.e. EVs), 5G Wireless & Cloud, and Industrials & Semi-cap. The company should continue to benefit from the general move to diversify geographic manufacturing and off-shore operations away from China, as well as a strong free cash flow profile that enables the company to buy back stock and significantly reduce the outstanding share count.

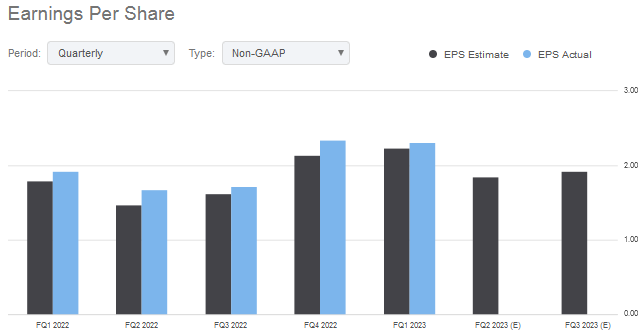

Earnings

Jabil has a solid track record of consistently beating analysts' consensus EPS estimates:

{kind=link}

Seeking Alpha

Part of that is likely due to management's relatively conservative projections, and part of that is likely due to the underlying strength of the company's operations. Regardless, I would much rather have a management team that under-promises and over-performs as compared to the alternative.

JBL released its Q1 FY23 earnings report two days after my last Seeking Alpha article on the company (the stock is +8% in the five weeks since that BUY rated piece was published). As I suggested in that article, JBL once again came through with very strong results:

- Revenue of $9.63 billion (+12.5% Y/Y) beat estimates by $310 million .

- Non-GAAP EPS of $2.31 was a $0.07 beat.

- EMS Segment revenue grew 18% yoy.

- Consolidated core-margin was 4.8%.

- Auto & Transportation (think EVs) revenue grew 42% yoy.

As I have mentioned in my previous articles on JBL, expanding margin and share buybacks means that the company is growing operating income and EPS faster than revenue. That was true again in the Q1 results, with operating income growing 15% yoy and EPS growing 20% yoy.

During the quarter, JBL bought back $161 million worth of stock. On a year-over-year basis, the diluted average outstanding share count fell by 9.7 million shares (6.6%).

Going Forward

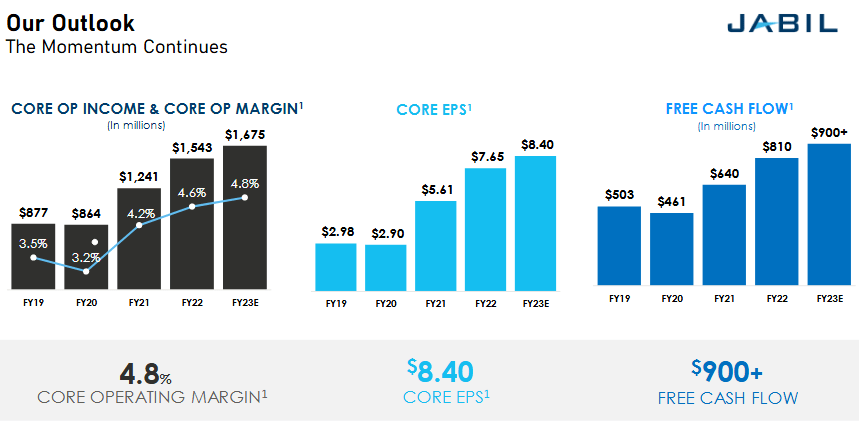

JBL gave the following guidance for full-year FY23:

{kind=link}

Jabil

CEO Mark Mondello said:

I remain confident in our plan moving forward, which is supported by both strong secular tailwinds and continued refinement of our more traditional businesses. As a result, we are raising our core EPS for the year to $8.40, a twenty-five cent increase from our outlook at the beginning of the fiscal year."

As you can see, core operating margin is expected to grow another 20 basis points in FY23, core EPS is expected to grow 9.8% yoy, and FCF is expected to grow to $900 million (+11.1% yoy). When looking at these numbers - as good as they are - remember, JBL management typically under-promises and over delivers.

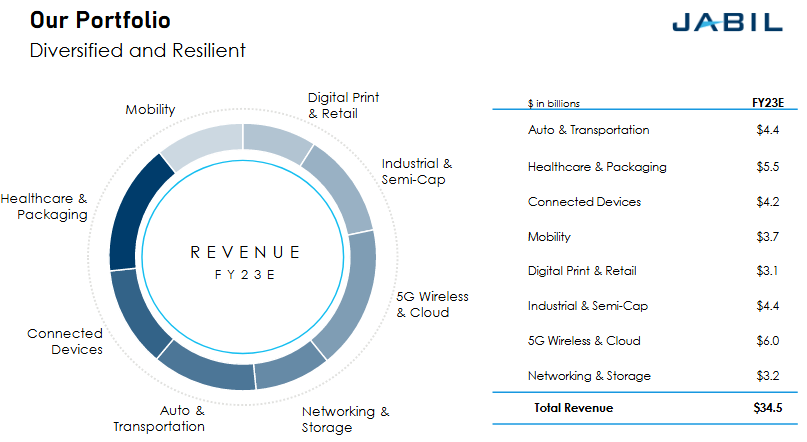

As the slide below demonstrates (taken from the company's Q1 presentation ), I emphasize that a primary strength of JBL going forward is the work the company has done over the last several years to build a well-diversified portfolio:

{kind=link}

Jabil

I say that because after watching the company for a few years now, it seems whenever one particular piece of the business has relatively weak quarter, there's another stronger sub-segment that more than makes up for it - with the overall result being growing revenue, growing earnings, and growing free cash flow.

Jabil continues to innovate. Just today (Jan. 18) the company released news that its optical design center in Jena, Germany:

... is currently demonstrating a prototype of a next-generation 3D camera with the ability to seamlessly operate in both indoor and outdoor environments up to a range of 20 meters. Jabil, ams OSRAM and Artilux combined their proprietary technologies in 3D sensing architecture design, semiconductor lasers and germanium-silicon ("GESI") sensor arrays based on a scalable complementary metal-oxide-semiconductor technology platform, respectively, to demonstrate a 3D camera that operates in the short-wavelength infrared ("SWIR" at 1130 nanometers.

Meantime, and due to JBL's large and global geographic footprint, the falling US Dollar is likely to continue to be a strong tailwind going forward. I believe the US dollar peaked last September and will likely fall back below 100 as inflation pressures continues to ease:

MarketWatch

Valuation

As mentioned earlier, JBL currently trades with a TTM P/E of 11.4x and a forward P/E of only 9.4x. As the graphic below shows, Jabil is trading at a relatively deep-discount to its peers Flex ( FLEX ) and Plexus ( PLXS ):

| TTM P/E |

| Forward P/E |

| JBL |

| 11.4x |

| 9.4x |

| FLEX |

| 13.1x |

| 10.4x |

| PLXS |

| 22.9x |

| 18.6x |

NOTE: TTM P/Ex from Yahoo Finance, Forward P/Es from Seeking Alpha

But FLEX's most recent quarter saw net income drop 20% yoy . And while Plexus is arguably worth a premium given its most recent quarter demonstrated revenue growth of 32.9% - but a 2x premium? After all, in FY22, Plexus grew GAAP EPS by only 2.1% while JBL grew GAAP earnings from $4.58/share to $6.90/share in FY22 (50.7%).

Summary and Conclusion

Many investors - especially in the technology sector - are apparently not impressed by a business that delivers core operating margin in the neighborhood of 5%. "Too low" they say. However, what they're missing with JBL is that expanding margin and strong free cash flow, combined with its share buyback plan, enables JBL to grow earnings per share at a significantly higher rate than revenue. Meantime, and despite the recent run-up in the stock price, JBL is still arguably under-valued. And that's why I reiterate my buy rating on JBL.

I'll end with a five-year stock chart comparison of JBL vs. the broad market as represented by the VOO and QQQ ETFs:

For further details see:

Jabil: On Fire Year-To-Date (+13%) And Still A Fantastic Value