JBL - Jabil: Rating Downgrade As Share Price Has Rallied Very Strongly

2023-10-03 04:59:44 ET

Summary

- Jabil's 4Q23 results were strong, with sales exceeding estimates and gross margins increasing.

- Management's long-term guidance, including revenue forecasts and margin expectations, drove positive sentiment and stock performance.

- I revised my rating from buy to hold as the potential upside seems to be already priced in.

Investment action

I recommended a buy rating for Jabil ( JBL ) when I wrote about it the last time because of the company's ongoing transition into more promising and expanding markets like electric vehicles, healthcare, cloud computing, and renewable energy. Based on my current outlook and analysis of JBL, I recommend a hold rating. I believe the market has already priced in the bulk of potential upside, given the strong share price rally over the past few months. While I am still positive about the business, I think the risk or reward no longer fits my criteria.

Review

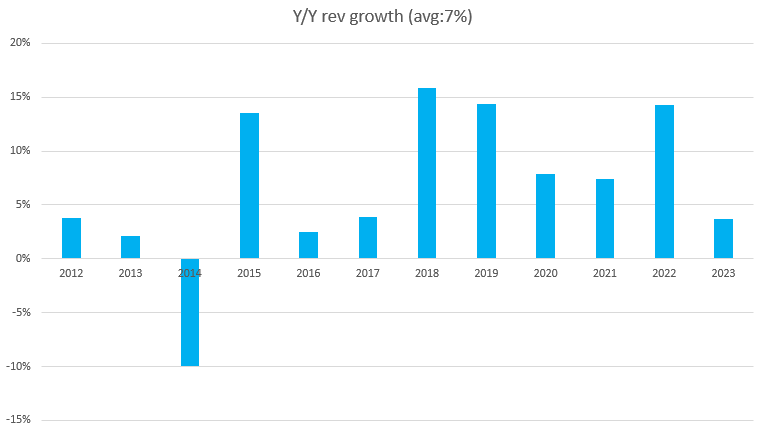

As expected, JBL 4Q23 results were strong, coming in line with guidance. A total of $8.46 billion was reported in sales, which is higher than both the consensus estimate of $8.51 billion and management's own forecast of $8.2 to $8.8 billion. With a more favorable product mix, gross margins increased to ~9.1%, resulting in 5.6% in EBIT margin. The EBIT margin is slightly higher than the 5.3% predicted by consensus and the 5.5% upper bound of management's target range. The overall result was an earnings per share of $2.45, which was above the $2.32 predicted by consensus and the $2.14 to $2.50 range set by management.

I believe that management's long-term guidance was the bigger highlight of the results that drove the stock, despite the fact that the results themselves were impressive. In light of JBL's announcement that it would sell its mobility business to BYD , the long-term guide provides investors with something solid on which to build their anticipation. Amid macroeconomic uncertainty in some end markets, management has been providing cautious revenue guidance, but they have expressed optimism about improving margins in the future, which will drive greater earnings power in the long run. Revenue was forecast between $33 and $34 billion, which is below the consensus estimate of $36 billion, but I don't consider this to be a major concern because the "miss" is attributable to the absence of the Mobility business. The key takeaway is that the company expects its EBIT margin to be between 5.3% and 5.5%, resulting in an EBIT of $1.81 billion and EPS of $9.30 to $9.70, both of which are significantly higher than the consensus estimate (even at the low end of the range). Just by looking at this, I think it is quite indicative of the margin profile of JBL, excluding the mobility business.

As such, I believe the stock sentiment is now very positive, as there are no lingering uncertainties. More importantly, management has stayed true to its robust capital allocation plan; the Mobility sale proceeds will be used to expand the existing $2.5 billion share repurchase program. Moreover, with this new long-term guidance, I believe it sets the expectation right for investors in that JBL now has a clear path to earnings per share in excess of the $10.65 projected for FY25. Remember that the FY25 outlook embeds low-single-digit revenue growth and margins expanding to more than 5.6%, but JBL has been growing at high-single digits for the past decade (as such, growing low-single digits is very much possible), and margins are already guided to be as high as 5.5% in FY24.

{kind=link}

I am confident in JBL's ability to reach the FY25 goal, in large part because of the secular uptrends I've previously mentioned. JBL's increased focus on EVs, renewables, healthcare, and the datacenter, among other secularly growing markets, should help the company increase revenue and margins, in my opinion. These industries tend to have a higher average profit margin because of their longer product cycles, which means more opportunities for JBL to value add. Management also anticipates that AI (another rapidly expanding industry) will account for 20-25% of its cloud business in FY2024. Considering the higher value added and greater demand, I anticipate higher margins from this division.

Valuation

Author's work

I believe JBL can achieve its FY25 EPS target of at least $10.65 given the margin outlook and secular uptrends supporting growth. My assumption is that growth will see a minor dip in FY24 (-3%) as the Mobility business has been sold off. Growth should normalized back to 5% in FY25 as it starts to show growth on a like-for-like basis. Margins should improve as the lower-margin Mobility business has been sold off, and that the “new” JBL has a much better margin profile. As such, I reiterate my view that the business should continue to trade at a premium relative to historical levels. Putting these assumptions together, I have a target price of $138 (9% upside).

Albeit having upside, I recognize that the stock has done very well over the past few months, surging past my price target of $103 previously. At the current share price of $126, I believe the market has priced in the bulk of potential upside already. Therefore, I am revising my rating from buy to hold.

Risks & Final thoughts

Jabil's top five customers account for more than 40% of the company's total revenue. Therefore, the company's revenue and earnings could be negatively affected by factors such as customer consolidation, reduced purchase commitments, or the loss of key customer relationships.

In conclusion, my recommendation for JBL has evolved from a buy rating to a hold rating based on the recent strong share price rally and the market's anticipation of JBL's future prospects. JBL's 4Q23 results were impressive, particularly with a favorable product mix and promising long-term guidance. The sale of the Mobility business provides a clear path to improved earnings and a solid capital allocation plan.

While I am confident in JBL's ability to reach its FY25 EPS target, thanks to its focus on secularly growing markets like EVs, renewables, healthcare, and AI, the current share price of $126 already reflects much of this potential. Therefore, I believe the risk-reward balance no longer aligns with my criteria, prompting the revision of my rating to hold. In sum, JBL's transformation and future outlook remain positive, but the market's optimism has already been priced in.

For further details see:

Jabil: Rating Downgrade As Share Price Has Rallied Very Strongly