FIS - Jack Henry & Associates: Hard To Make Bank With The Stock At This Price

2023-03-04 10:00:00 ET

Summary

- Jack Henry & Associates is a high-quality business in the Core Banking business.

- The company checks my quality boxes and looks to be well led.

- Right now the market prices too much into the stock to see significant upside in the shares.

Jack Henry & Associates (JKHY) has been a compounding machine over the last decade, growing at a 15% CAGR, outperforming the SPY by 3%, leaving its competitor Fidelity National Information Services (FIS) left behind, but underperforming Fiserv (FISV). The company operates in the boring part of the exciting Fintech industry called Core Banking. According to HCLTech , Core Banking is defined as:

a back-end system that processes banking transactions across the various branches of a bank. The system essentially includes deposit, loan and credit processing. Among the integral core banking services are floating new accounts, servicing loans, calculating interests, processing deposits and withdrawals, and customer relationship management activities.

Let's see if the outperformance story is behind us or just getting started.

Peer group performance (Koyfin)

{kind=link}

Jack Henry has three pillars embedded in its culture: Employees, Customers and Shareholders. With Employees as the first pillar, culture and satisfied employees are an important objective for Jack Henry. Below are the results of the Q3 FY 22 internal employee experience monitoring. We can see that Employees show high satisfaction and are on board with the company's values. This is underlined by the Glassdoor ratings , which are good with 3.9 stars, 74% recommendation to a friend and an 84% CEO approval rating. This is significantly better than the direct competitor Fiserv's results in its Glassdoor rating , showing a grim picture of the company culture. Customer satisfaction also came in strong at 4.73/5. This is very important if you operate in an old and slow-moving industry like banking.

Q3 FY 22 Employee Experience Monitor (Jack Henry Investor Presentation)

{kind=link}

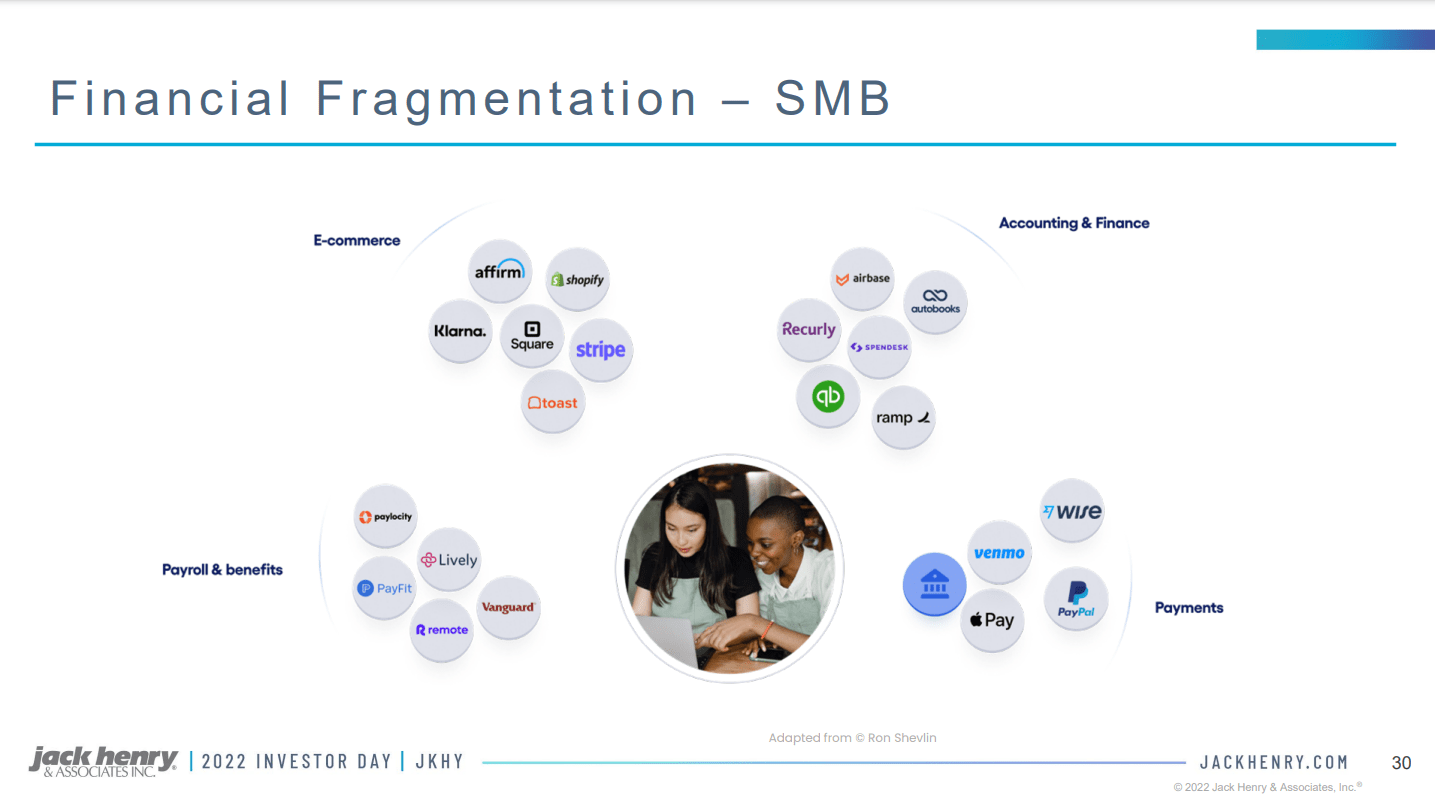

The financial landscape is changing

The saying 'There's an app for that' nowadays applies to most of our daily lives, including our finances. Customers must use various apps from dozens of other providers to buy from varying vendors and perform varying services. This fragmentation creates an opportunity for financial services companies like Jack Henry to help develop interfaces for their banking customers.

{kind=link}

Jack Henry is redefining its strategy by unbundling its products from a large on-premise solution to customizable cloud applications from which customers can choose.

Unbundling services to move to the cloud (Jack Henry Investor Presentation)

{kind=link}

Margins and Efficiencies

Financial Services companies are known to be very asset-light and profitable businesses. Jack Henry is no different, although we don't see improvement in the numbers over the last decade. The company has done a remarkable job keeping the gross margins steady at 41% and has lowered SG&A margins from 13% to 11%. These are minor improvements but nothing extraordinary.

{kind=link}

Another essential metric and a KPI Jack Henry displays in its quarterly reports and investor presentations is returns on capital. There are many ways to look at this. Still, Jack Henry uses Return on invested Capital (ROIC defined as Net income/average invested capital) and Return on average shareholder's equity (basically Return on equity), so let's have a look. We can see that the numbers generally trend upwards over the long term and have consistently stayed at decent levels. We always want to see ROIC at least 2% above the cost of capital (we can generally use 10% as a default value) and Jack Henry achieves this. The median of 15.81% is also strong.

{kind=link}

Capital Allocation

Jack Henry is a cash-flowing business, generating just under $500 million in Free cash flows in each of the last three years. This leaves a lot of capital to allocate, so let's see how they do it. The company is paying out a modest dividend of around 1%, buying back shares and doing occasional acquisitions. The company also doesn't issue much debt and has a clean balance sheet at just 0.5% net debt/EBITDA. The buybacks reduced outstanding shares by 18% over the last decade, with $1.51 billion (or 12.34% of the current market cap) spent on buybacks and headwinds of $148 million in stock-based compensation. This indicates that Jack Henry has effectively done value accretive buybacks for its shareholders. Capital Allocation looks excellent.

{kind=link}

Valuation

At this point, we have established that Jack Henry is a high-quality business, but we also need to find out if JKHY stock trades at a fair price. First, we should determine what kind of growth we can expect from Jack Henry. The company provided a slide to visualize how they project a typical year. We arrive at a high single-digit revenue growth expectation with several low single-digit incremental growth drivers. This is above the company's recent performance (3 and 5 years), which saw revenues, net income and cash from operations grow between 6-7% annually. Let's give them the benefit of the doubt and assume that 8.5% is a reasonable assumption for the company's revenue growth.

Revenue growth in a typical year (Jack Henry Investor Presentation)

{kind=link}

Let's do an inverse DCF analysis to see if the current price is fair. Based on its free cash flows, the company looks to be fairly valued, maybe slightly over its fair value at expectations of 8-9% growth. I assumed 1.8% of buybacks annually due to its 10-year track record. This could be an aggressive assumption.

Jack Henry Inverse DCF ( Author's Model)

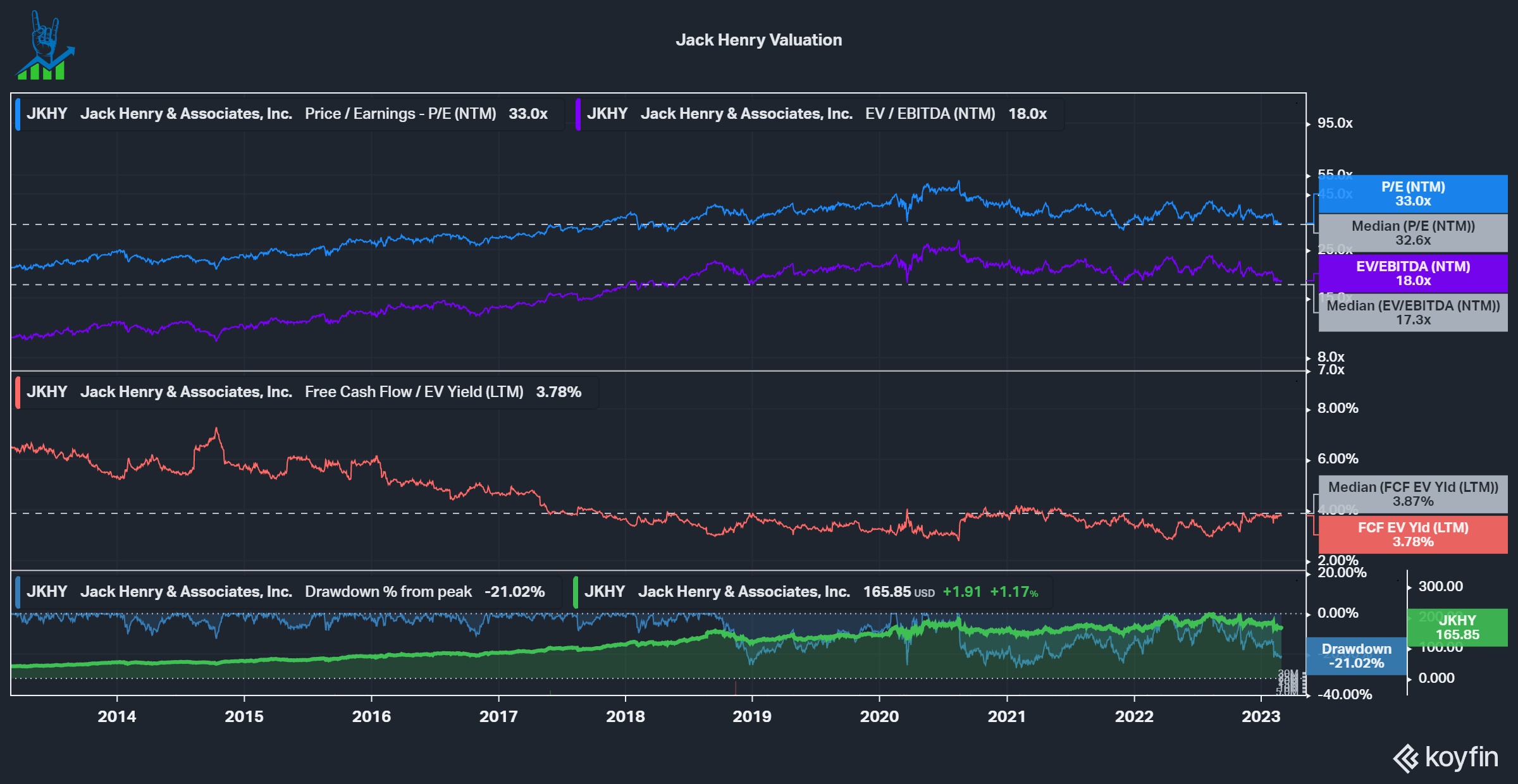

Another way to value Jack Henry is by looking at historical multiples. The story looks a lot different here. Over the past decade, the multiples have raced up and peaked in bubble territory around 30 times EV/EBITDA. Multiples came down a lot but are still elevated and high, considering their expected growth rate.

{kind=link}

Conclusion

Like many other high-quality companies, Jack Henry is also currently, at best, trading at fair value and, at worst overpriced in my opinion. I do not see much upside in this stock right now, so I'd put Jack Henry on my watchlist.

For further details see:

Jack Henry & Associates: Hard To Make Bank With The Stock At This Price