JACK - Jack In The Box: Management Execution Is Promising But Valuation Is A Concern

2023-05-02 09:44:32 ET

Summary

- Jack in the Box's stock has surged over 50% since July 2022, outpacing the S&P 500 and industry peers.

- Improving cost trends, such as stabilizing average hourly earnings and moderating food inflation, are benefiting margins.

- Management’s store growth strategy is beginning to take shape, driving the company toward management’s goal of 4% net store growth beyond 2025.

- The acquisition of Del Taco offers opportunities for geographic expansion and refranchising, which should increase shareholder value.

- Given the recent stock performance and downside risk, the stock is a hold at current levels. However, the stock is likely a buy on a 10%-15%pullback.

Summary

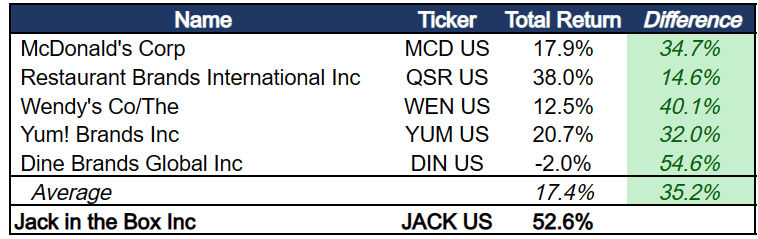

In July 2022, we wrote about our bullish outlook on Jack in the Box ( JACK ), and since then the stock has surged over 50%. The stock’s performance has significantly outpaced the S&P 500's 7.4% return and its industry peer average return of 35%.

{kind=link}

This remarkable performance is attributable to a combination of favorable macroeconomic conditions and the management's successful execution of its business strategy. Given these developments, we wanted to provide an update, reassessing the stock's short and long-term potential and evaluating the factors that could contribute to its continued growth.

Cost Trends are Improving

One of the primary challenges faced by the restaurant industry over the past two years has been rising food costs and labor inflation. These factors have put significant pressure on profitability and operational efficiency.

However, recent data suggest a reversal of these trends.

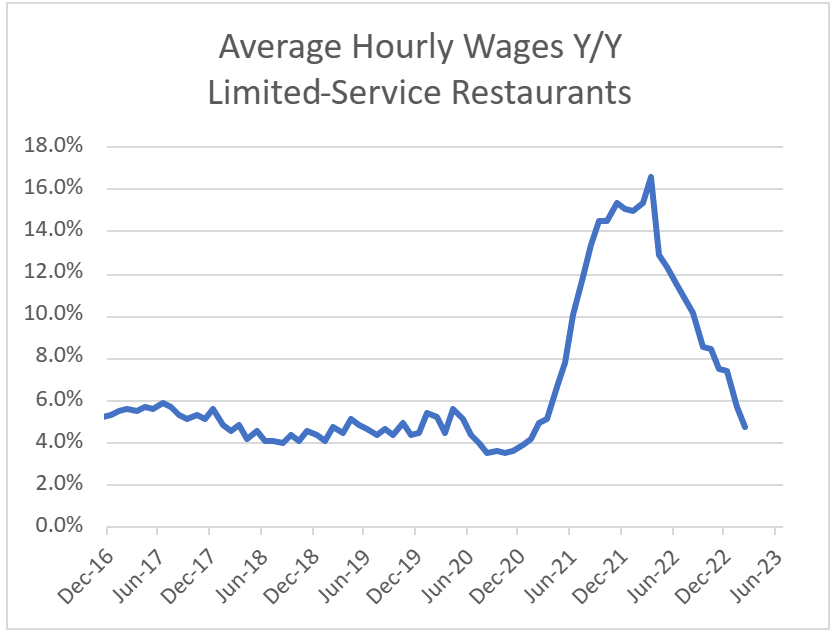

U.S. average hourly earnings for limited-service restaurants has seen its growth rate stabilize to historical levels of 4% to 5%. This development has positive implications for Jack in the Box since payroll represents 20% of JACK’s expenses. An improvement in labor trends leads to higher company-owned restaurant profitability. Additionally, lower wage growth indicates an easing of labor conditions, which enhances operational efficiency and potentially encourages franchisees to open new stores.

{kind=link}

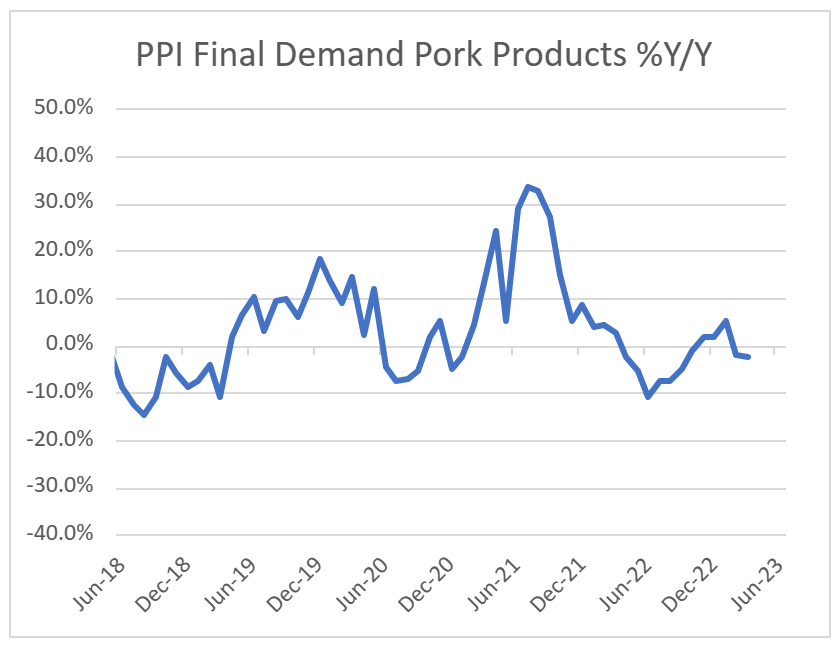

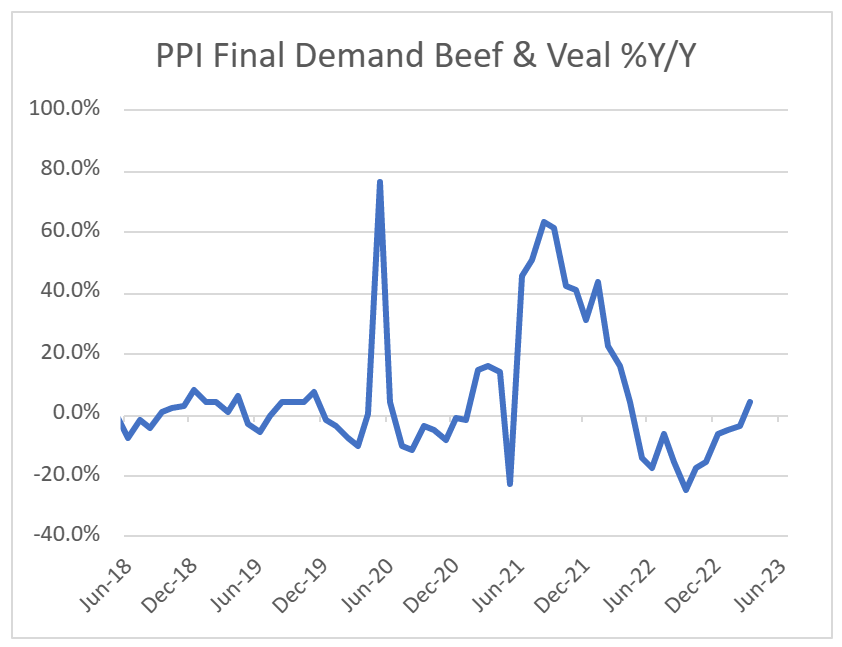

Moreover, food inflation has shown signs of moderation, with the year-over-year changes in the Producer Price Index ("PPI") for pork and beef exhibiting substantial improvements.

{kind=link}

{kind=link}

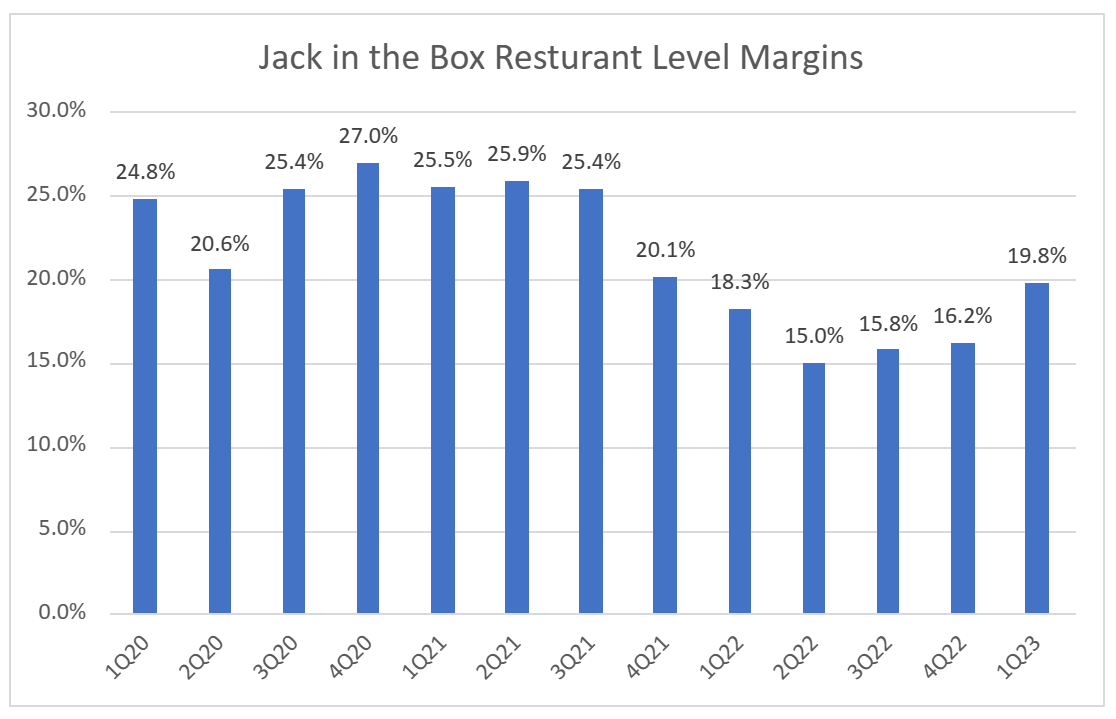

Consequently, operating margins have improved in recent quarters. While still below the mid-20 percent levels prior to the pandemic, the improvement has been welcomed by investors.

Company Reports, Author's Calculations

{kind=link}

Currently, for conservatism, we are modeling for company owned restaurant margins to stay in the 18% range for the next couple of years. If we assume margins return back towards pre-covid levels of approximately 24% in the couple of years, this would increase our 2025 EPS estimate 21% from $8.26 to $10 and our EBITDA estimate 14% from $378 to $431 million.

Strong Gross Openings, But Still Work to Achieve Long-Term Targets

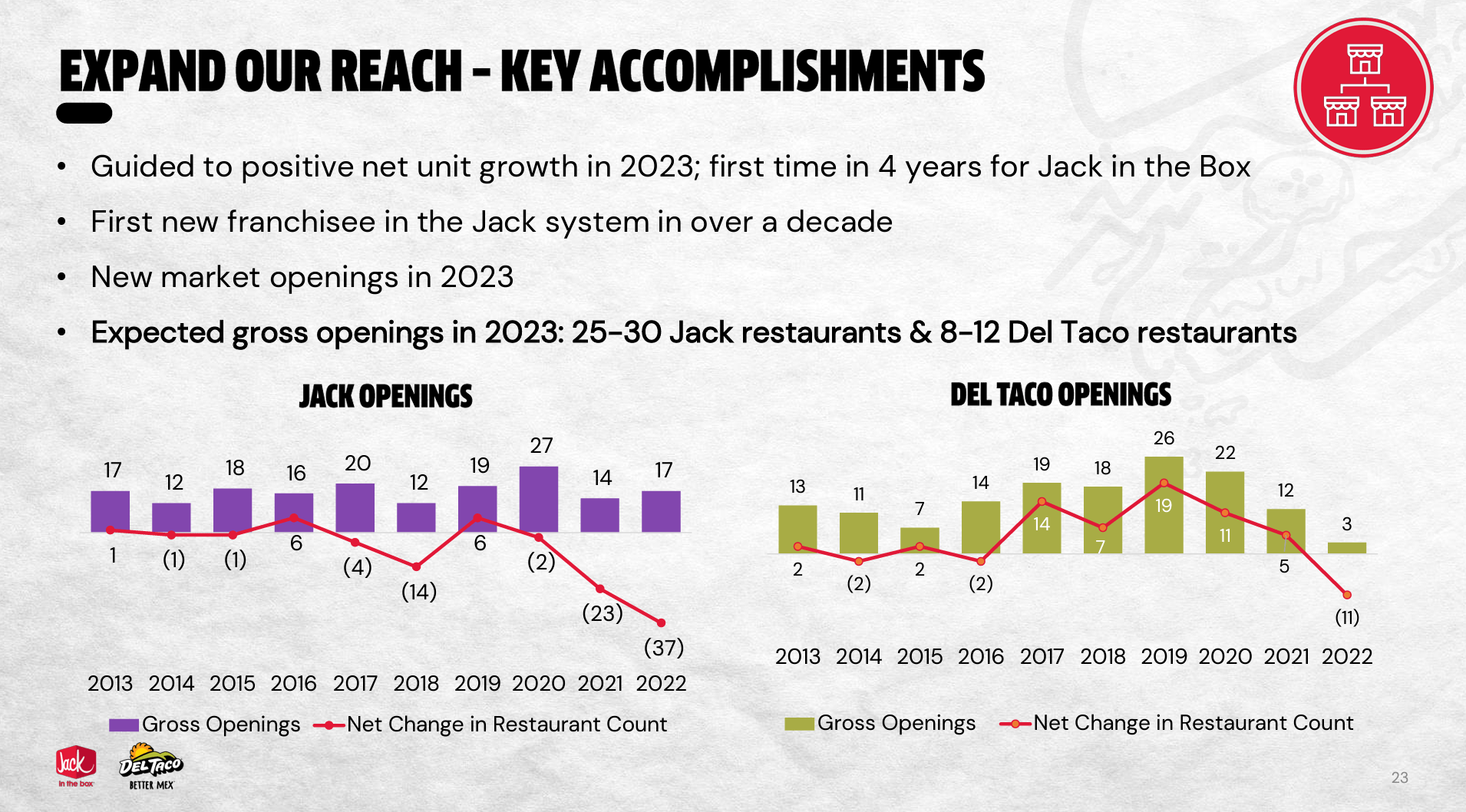

The strategy around new store growth implemented by Jack in the Box's management has begun to yield positive results.

JACK’s management has been working towards its goal of 1% to 3% net store growth through 2025 and for 4% net store growth beyond 2025. The driving force behind achieving this goal is the company’s new store development program that has proven to be successful since it was launched in 2021. The program has garnered commitments for over 300 new restaurants, with 25 new stores already opened under these agreements.

JACK’s management team has guided gross door growth of 25 to 30 stores this year, which is already off to a solid start with six opened in the first quarter of 2023. This is a significant improvement from prior quarters. If JACK can sustain this trend, then Jack in the Box system is on track to grow at the low end of its net store growth goal of 1% to 3% this year.

JACK 2023 ICR Conference Presentation

{kind=link}

Adding Value Via the Del Taco Acquisition

The acquisition of Del Taco has proven to be an opportunistic investment. Jack in the Box paid $585mm for Del Taco, which equates to a 9x EBITDA multiple. Since closing on the deal, Del Taco’s business fundamentals have been good considering how challenging of an operating environment it has been. Profitability has held up surprisingly well, which can be attributed to the low price points Mexican QSRs typically offer, leaving room for significant price increases to offset cost inflation.

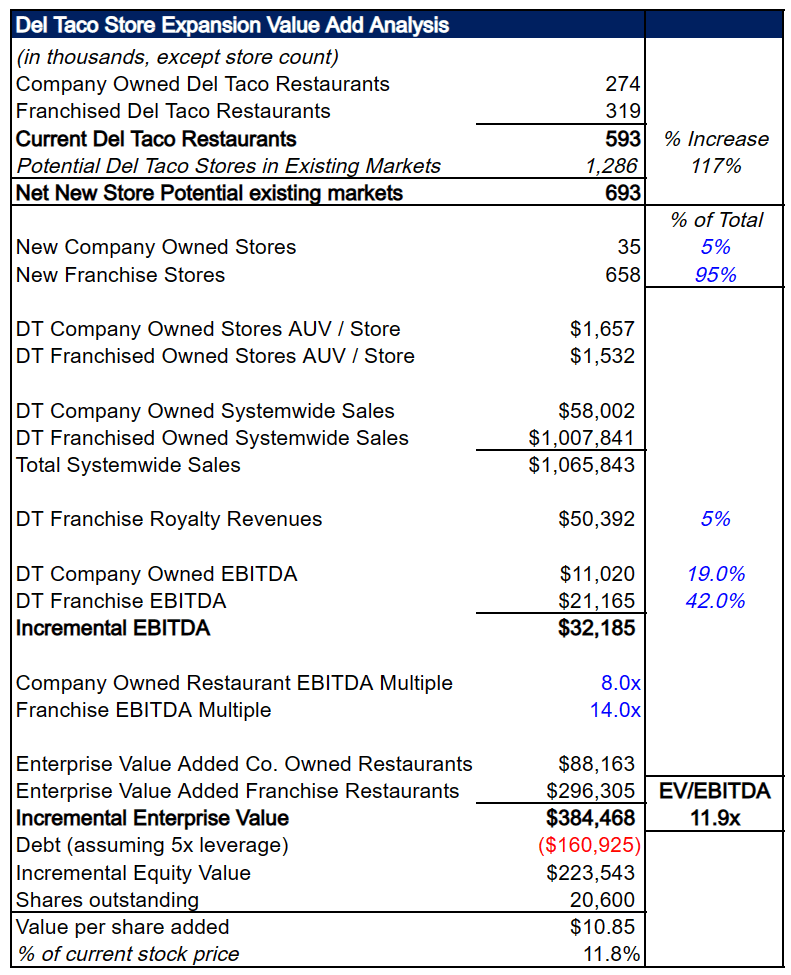

Beyond the attractive business fundamentals, there is an opportunity to increase shareholder value by over 10% through geographically expanding the Del Taco brand. Del Taco currently only has 593 stores, which remain largely concentrated in the western and southwestern United States.

Jack in the Box’s management team believes that in existing markets, Del Taco has expansion potential of 1,286 stores. That would represent a 117% increase in the system’s store count from current levels. Using current store economics, our analysis estimates that If Del Taco were to open these stores on a leverage neutral basis, it is worth an incremental 11.8% ($10.85) of equity value for shareholders.

Company Reports, Author's Calculations

{kind=link}

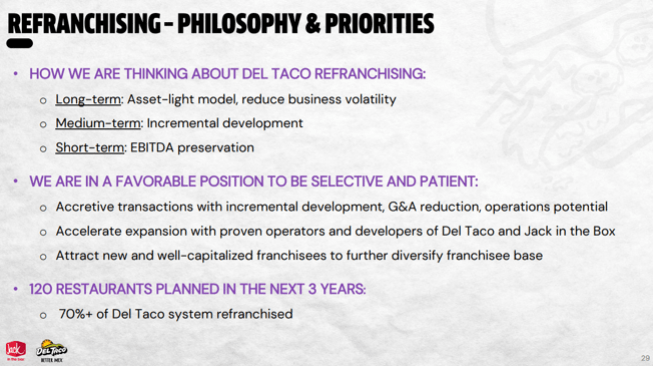

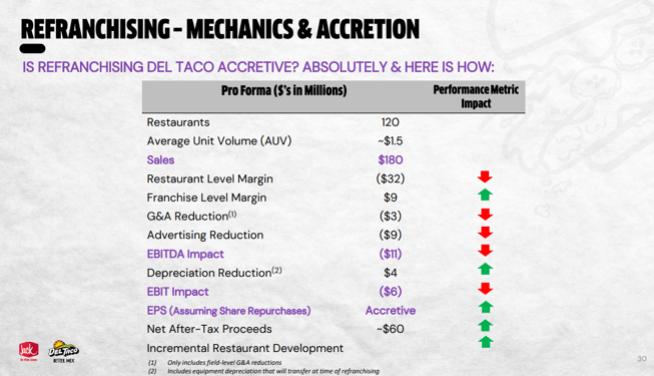

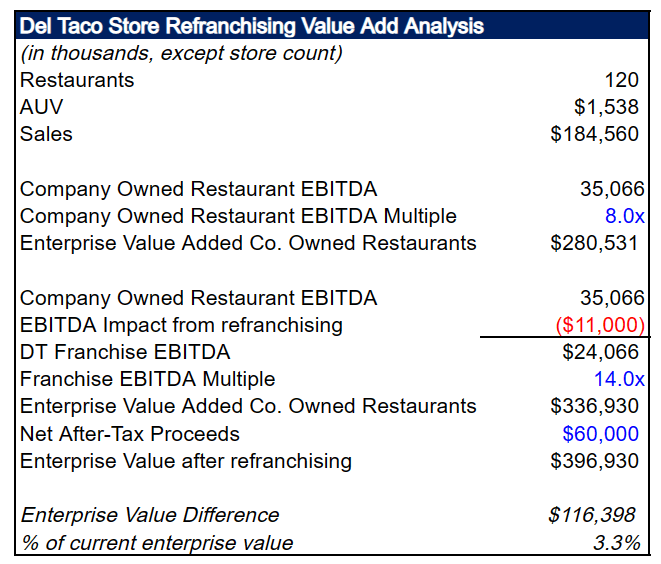

Perhaps what is a more interesting opportunity is the ability to refranchise Del Taco’s 274 company-operated stores. Doing so would unlock over $100 million of liquidity for JACK’s management to reinvest in growing the business. Additionally, profits generated from franchised restaurants are valued significantly higher than company owned profits because of their capital light nature. This conversion should fetch JACK a higher overall EBITDA multiple as the company becomes more capital light and will become more insulated from operating challenges such as input cost inflation.

Management has outlined a plan to refranchise approximately 120 Del Taco stores over the next three years. Doing so would provide $60 million in after-tax proceeds and shift the Del Taco system to a significantly more capital light model. We estimate a 3% benefit to JACK’s enterprise value (approximately $116 million).

JACK 2023 ICR Conference Presentation JACK 2023 ICR Conference Presentation Company Reports, Author's Calculations

{kind=link}

{kind=link}

{kind=link}

The acquisition of Del Taco has not only proven to be a strategic and opportunistic investment for Jack in the Box, but also presents several avenues for enhancing shareholder value in both the short and long term.

Jack in the Box Trades 30% Cheaper Than its Peers

Despite outperforming its industry peers by an average of 35% since July of 2022, Jack in the Box continues to trade at an attractive discount relative to its competitors. Historically, prior to the franchisee relationship challenges, the company's stock traded at a 15% to 20% discount. This discounted valuation provides an additional upside opportunity for shareholders.

{kind=link}

Note that EBITDA and EPS growth, EBIT margins, and ROICs are in line with or above peer company Wendy’s (WEN), yet JACK trades at a 20% discount on an EV/EBITDA multiple basis.

Company Reports, Bloomberg, Author's Calculations

{kind=link}

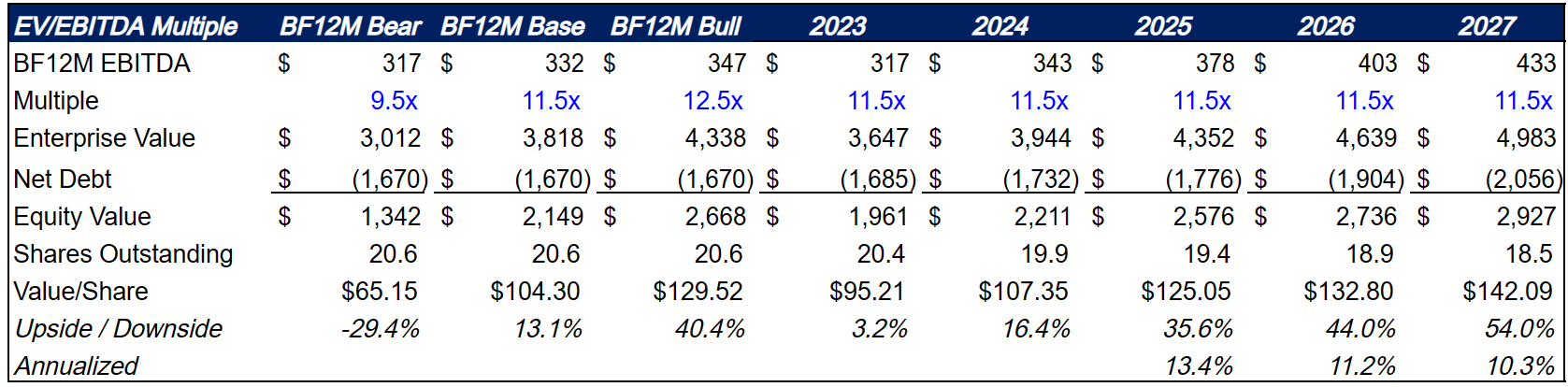

As Jack in the Box continues to demonstrate improved results and growth opportunities, we believe the potential for the stock to return to its historical 15% to 20% discount is possible. This would translate to a valuation of approximately 12.5x EBITDA multiple and 17x EPS multiple. Under this scenario, the stock price could increase by 20% to 30% in 12-24 months, a still healthy amount of upside assuming management executes.

Company Reports, Author's Calculations Company Reports, Author's Calculations

Valuation and Return Forecast

Applying historical multiples to Jack in the Box's EPS and EBITDA suggests potential upside of approximately 10% and 13%, respectively, over the next 12 months. However, the stock could face downside risk of 30% to 35% if the company encounters further macroeconomic challenges or management execution issues.

Longer-term, the prospects for Jack in the Box remain promising due to store growth for both Del Taco and Jack in the Box, refranchising opportunities, and an improving commodity environment, which should drive further EPS and EBITDA growth.

Over the next 3 to 5 years, we see the potential for the company to generate 10% to 15% annualized returns, slightly outperforming the S&P 500's long-term return average of 10%. This long-term return potential, combined with the company's growth initiatives, make Jack in the Box an attractive investment option for those willing to take a longer-term view.

Company Reports, Author's Calculations Company Reports, Author's Calculations

{kind=link}

{kind=link}

Conclusion

Jack in the Box's stock has performed remarkably well over the past 10 months. However, in the short-term, it is difficult to envision the stock rising more than 10 to 15%. Despite the business’s recent performance, downside risks remain due to continued inflation and wage costs pressures.

We expect Jack in the Box to be impacted by a recession, but the company should perform well relative to other consumer discretionary and food service companies. As we wrote about in our previous article, prior recessions have had a large impact on Jack in the Box's business performance because of the role lower-income consumers have played as customers. However, it is important to note that since the pandemic, Jack in the Box has attracted higher end customers, largely driven by its digital push. Generally, we believe the stock should fare well in a recession, as QSRs are typically the most affordable option for budget-conscious consumers seeking to dine out.

The medium to long-term outlook for Jack in the Box is still enticing. However, given the stock's recent run and the asymmetric risk of the downside in the near term (six to 12 months), the stock is a hold at its current levels. Should the stock pull back again by 10-15%, and the company's outlook unchanged, we would consider it an opportune time to buy.

For further details see:

Jack In The Box: Management Execution Is Promising But Valuation Is A Concern