JACK - Jack in the Box: Stock Faces Multiple Headwinds

Summary

- Wage and commodity inflation continue to press JACK's margins.

- Del Taco deal levered up the company at the wrong time.

- Expansion outside its core markets has proven a failed strategy in the past.

Jack in the Box ( JACK ) is facing both food commodity and labor inflation headwinds, while its lower-income customer base faces a difficult inflationary and economic environment. Meanwhile, its CEO is pushing expansion beyond JACK's core markets, which has proven trouble for the company in the past. A high valuation and heavy debt load only add to JACK's issues.

Company Profile

JACK operates fast-food restaurant chains under its namesake brand, Jack in the Box, as well as Del Taco.

The Jack in the Box concept is a hamburger chain with nearly 2,200 locations across 21 states. However, about 70% of its restaurants are located in the states of California and Texas.

Approximately, 93% of its Jack in the Box locations are franchised. The company generally gets a royalty of 5.0% of gross sales, but it can be as high as 15%. Marketing payments are also 5%.

Del Taco, meanwhile, is the #2 Mexican fast-food chain in the U.S. by number of locations, with nearly 600. Over 60% of its locations are in California.

Half of its restaurants are franchised. Royalty and marketing payments are typically set at 5.0% and 4.0% of gross sales, respectively.

Opportunities

In the past, JACK successfully transformed its business model through the re-franchising of its namesake brand. Not only does refranchising bring in cash, it is also a higher-margin, more steady business that can generally get a higher multiple from the market.

The company is currently using that same playbook with Del Taco, where about half the locations are company owned. This will help reduce its heavy debt load, while also putting the concept more in line with the profile of Jack in the Box.

CEO Darin Harris is also looking to expand the brands into new markets. Harris has a history of restaurant development in previous roles at Arby's and Captain D's and is looking to develop new markets outside of California and Texas. 2023 will see the company have positive net unit growth for the first time since 2019. If successful, this would help diversify the company geographically and show that the company has the ability to more aggressively grow its number of units.

In addition, the company is also looking to improve Jack in the Box restaurant-level margins. The company is looking to use equipment, technology, and training to help drive down costs. Some of these things can be as simple as a cheese pump to reduce waste. Meanwhile, it will look to roll out a new POS system in 2024.

Speaking at the 2023 ICR conference in January, Harris said:

"In order to get to modernization or to what I would like to get to, which is innovation, we have to tart with the heartbeat of the system, which is the POS investment. And that will lead to our ability to do things like digital menu boards or AI, machine learning models to recommend upsell or predict demand, and some of the automation things we're doing with robotics.

"But we have to start with the central heartbeat of our organization, which is our POS systems. So it all required initial investment. We won't do all of these tomorrow. We'll keep these future investments responsible. But thanks to the leadership and infrastructure, it's now a possibility for Jack in the Box to invest into our future through technology investments."

Downside Risks

Inflation is one of the biggest risks that JACK faces. The company is facing both wage and commodity cost inflation headwinds.

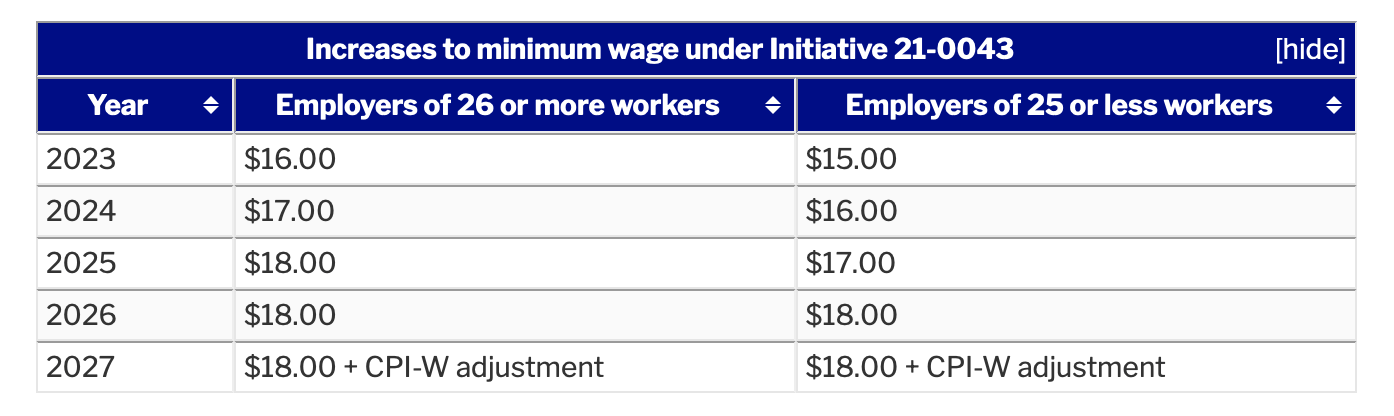

California has seen minimum wages soar over the last several years, jumping to $15.50 in January of this year. Some cities and counties in California have even higher. Meanwhile, the state has a ballot initiative next year to raise wages to $17 in 2024 and to $18 in 2025.

{kind=link}

Commodity costs have also been soaring. JACK saw commodity inflation of 14.4% for its fiscal year ending in October. The company sees commodity costs rising 9-11% for its fiscal year '23.

Inflation has greatly impacted restaurant-level margins, as in FQ4 they were 16.2% at Jack in the Box, down from 20.1% a year ago. In response to inflation, JACK has been aggressively increasing price. Given its lower-wage customer base, this can eventually hurt transaction volume as well, given the weakening consumer environment.

While JACK's expansion plans represent an opportunity, they are also a risk. The company has a long history of having difficulties moving into new markets. Long ago it had to shutter its East Coast and Midwest locations due to poor sales, and more recently it even struggled in parts of Texas such as San Antonio. Harris plans to get to 4% annual unit growth by 2025, but told investors at an investment conference that management "underestimated how thin the pipeline is."

{kind=link}

Finally, the company carries a fair amount of leverage. Based on its trailing EBITDA, its leverage is about 5.7x. However, if you want to include its operating lease obligations, it's over 10x.

Last Quarter

JACK saw revenue soar 45% to $402.8 million due to the Del Taco acquisition. Adjusted EBITDA rose 5% to $77.9 million. Adjusted EPS fell from $1.73 to $1.33, coming in slightly below estimates of $1.36.

Same-store sales at its namesake restaurant climbed 4.0%, with company-owned stores jumping 11.4%. Del Taco comparable sales rose 5.2%, with company-owned stores up 4.1%.

Restaurant-level margins (RLMs) were 16.2% at Jack in the Box, down from 20.1% a year ago. Del Taco RLM were 15.9%.

Wage inflation rose 11.3%, while commodity costs soared 14.9%.

Looking ahead, JACK forecast adjusted 2023 EPS of $5.25-5.65. That was well below the $6.59 consensus. The guidance excludes any dilutive impact from refranchising Del Taco restaurants.

It sees SSS of low single digits for both brands. The company forecast commodity costs increasing 9-11% and company-owned wages being up 3-6%. Jack in the Box RLMs are projected to be between 18-20%, while Del Taco RLMs are forecast to be between 14-16%.

On the call, Harris said:

"The inflationary environment from 2022 and into 2023 remains challenging. Just like our peers, we are not able to fully overcome the last 2 years of inflation on food, paper, labor and electricity with just price alone. But make no mistake, our core business is strong, and we are executing on our strategy despite the headwinds. The investments we are making in digital technology transformation, reimages and new restaurants are critical for us to accomplish our long-term goals, compete and grow.

"As we shift towards becoming a growth-oriented company, we understand there have been an abundance of moving parts within the business and the operating model since new management began the process of transforming the business. The overhaul of our strategy plus an acquisition along the way has likely made it difficult to model the business precisely and consistently, and we understand that."

Valuation

Including operating leases in the EV equation, JACK trades at 15x the FY23 EBITDA consensus of $312.6 million and 14x the FY24 EBITDA consensus of $332.5 million.

From a P/E perspective, it trades at 14x FY23 EPS estimate of $5.37. Meanwhile, it's valued at about a 12.5x FY24 EPS estimate of $6.36.

Conclusion

JACK's stock has held up very well over the past year, but I think the stock has plenty of downside ahead. The restaurant operator continues to face inflation pressures from both the food side and wage side, and it has already taken a lot of price over the past year. However, the company is generally more exposed to lower-end consumers in California and Texas, which puts it at risk.

The fast-food chain has historically struggled during a weakening economy, when larger rival McDonald's ( MCD ) tends to become more promotional. We haven't seen that yet, but if the U.S. does head into a recession, it's a possibility that the burger price wars could be reignited.

The March 2022 acquisition of Del Taco, meanwhile, levered up the company at the wrong time. Given the current environment and past expansion failures, the expansion strategy also feels ill-timed.

Given its high valuation, robust debt, and inflationary headwinds, I'd avoid the stock.

For further details see:

Jack in the Box: Stock Faces Multiple Headwinds