JACK - Jack in the Box: The Bad News Is Priced In

2023-11-27 07:00:00 ET

Summary

- Jack in the Box has experienced inflationary pressures, resulting in a significant multiple compression and negative annualized returns.

- Despite a mixed fourth quarter, JACK stock price increased, indicating that the bear-case scenario has been priced in.

- The recent passage of AB1228 in California and wage inflation pose challenges, but the market has already accounted for these factors in the stock's discounted valuation.

Summary

We've previously written on Jack in the Box ( JACK ), recommending a buy at levels near where the stock is current trading and then a hold rating when the stock rose to the high 90s. The stock has once again fallen to a level where it is too cheap to ignore, so we are moving our rating back to a buy.

Jack in the Box has struggled with inflationary pressures over the past couple of years, but has performed well over the long-term. Over the last 5-year and 10-year periods, EPS has compounded at a 9.7% and a 12.7% annual rate, respectively. While these EPS growth rates are impressive and look set to continue, concern about inflationary pressures has resulted in significant multiple compression. Since 2021, JACK's P/E multiple has drifted from the high-teens to low double digits, resulting in 5 and 10-year annualized total returns are -2.9% and 4.7%, respectively.

While inflationary pressures are subsiding, they still resulted in Jack in the Box reporting a mixed fourth quarter. However, the stock still managed to finish up almost 2% the following day. We believe the increase in the stock price reflects the fact that the bear-case scenario for the stock has largely been priced in at this point. We see limited downside from current levels on JACK, perhaps into the upper 50s. If management can execute on their growth plans and inflationary pressures abate, we think the stock could easily double over the next couple of years.

Fiscal Fourth Quarter Review

Jack in the Box's fourth quarter and fiscal 2023 earnings report revealed a mix of challenges and strategic wins. JACK reported EPS of $1.09 per share, missing estimates by $0.05 and marking a 22% year-over-year decrease.

FY 2023 EPS of $6.03 was slightly above the midpoint of guidance, growing 3.3% year over year (from $5.84 last year).

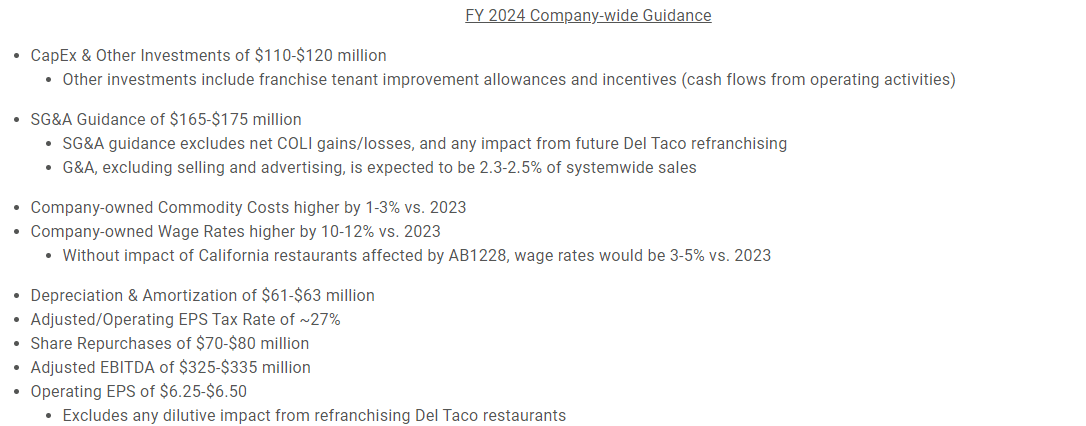

Fiscal year 2024 guidance was set at $6.25 to $6.50, slightly below the street estimate of $6.60. That implies 6% growth at the midpoint.

This guidance notably omits potential gains from the continued franchising of company-owned Del Taco ((DT)) units, a factor we believe contributed to the miss in guidance expectations.

Jack in the Box FQ4 2023 Press Release

{kind=link}

Despite these underwhelming figures, the Jack in the Box segment displayed resilience with comparable sales up 3.9% and a significant improvement in restaurant-level margins to 20.7%.

The segment concluded the year with an 11.2% increase in operating income.

However, these robust results were overshadowed by weaker performances at Del Taco. DT's comparable sales declined by 1.5% due to challenging year-over-year comparisons. DT's restaurant-level margins also dropped by 110 basis points to 14.8%.

On the positive side, refranchising efforts are progressing well, with 45 more restaurants transitioned, bringing the total to over 125 since the program began. This shift has increased the share of DT franchised restaurants from 50% at the time of acquisition to 75% today.

We would point out that as the business shifts to more franchise revenue and earnings, the quality of the business improves. And so, the valuation should begin to re-rate higher.

Management's strategic execution remains strong but is now shifting focus towards also improving the performance of DT restaurants. A notable management change was the promotion of Tom Rose to president of DT, who had previously achieved success in turning around Jack in the Box markets. This leadership change, combined with the ongoing refranchising narrative, sets the stage for DT's improvement in 2024 and beyond.

Impact of AB1228

The recent passage of AB1228 in California, which raised the minimum wage for fast-food workers to $20 per hour , introduces new dynamics for JACK. Being heavily exposed to the California market, the company anticipates a company-wide wage inflation rate of 10-12% for 2024, significantly higher than the 3-5% it would have faced without AB1228.

Management expects to raise prices as much as they can to preserve margins, but the company will most likely not be able to completely offset higher wages costs. Our analysis indicates that the increase in the minimum wage in California has reduced Jack in the Box's EPS growth by $0.50 to $0.60, or 8-10%.

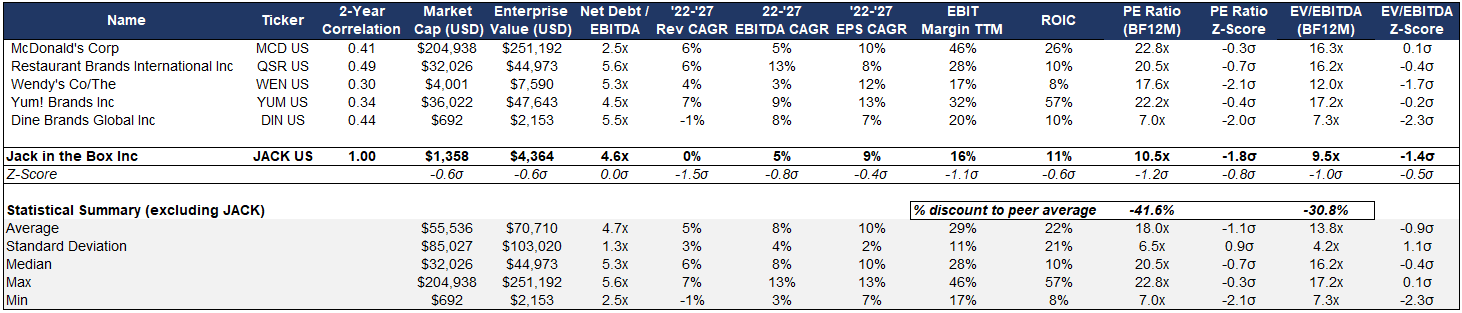

As JACK continues its refranchising efforts at Del Taco, the company overall will become less sensitive to the impacts of AB1228 and wage inflation in general. While the significant exposure to California remains a potential overhang for the stock, we believe the market has more than accounted for these factors, as evidenced by the stock's current 15% discount to historical multiples and 30-40% discount to peers.

Valuation

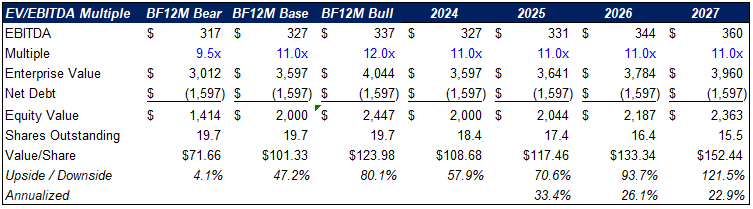

In terms of valuation, JACK is currently trading at just 9.5x our EBITDA estimate of $326.5 million for 2024 and 10.6x our EPS estimate of $6.48. These multiples are significantly below both the company's long-term median P/E and EV/EVITDA multiples of 17x and 11x, respectively.

While the lower quality Del Taco assets were a bit valuation dilutive, the company's path toward franchising the business and growing its store base should be valuation accretive.

Peers such as Wendy's trade at 12x forward EBITDA and 17.6x EPS. Restaurant Brands International ( QSR ) trades at 16.2x forward EBITDA and 20.5x forward earnings. McDonald's ( MCD ) trades even richer at 16.3x EBITDA and like JACK EPS is expected to grow 6% in 2024.

Author's Spreadsheet, Company Reports, Sell-Side Estimates

{kind=link}

We think 11x EBITDA and 16x earnings are fair valuation multiples for JACK once wage inflation headwinds abate. If growth accelerates, multiples could be even higher.

Interestingly, JACK's stock price rose 1.8% the day after the earnings release, suggesting that investors may be recognizing the stock's undervaluation despite a largely underwhelming earnings report. We see the current valuation as an opportunity, and project an upside of 40-55% over the next 12 months. That implies potential annualized returns of 20%+ over the next 3-5 years.

Author's Spreadsheet, Company Reports Author's Spreadsheet, Company Reports

{kind=link}

{kind=link}

Conclusion

JACK's stock dropped by a surprising 30% from its July 31st high, presenting a compelling opportunity to buy at a discount to intrinsic value. The post-earnings reaction indicates the market has priced in much of the negative news, while key positives such as Del Taco's successful refranchising and a strong pipeline of development deals are being overlooked.

We are buyers in the $60s, believing the stock deserves a valuation closer to that of Wendy's, which would place it near $110.

For further details see:

Jack in the Box: The Bad News Is Priced In