JAGGF - Jaguar Mining: Margins Continue To Remain Under Pressure

Summary

- Jaguar Mining released its Q2 results last month, reporting quarterly production of ~22,000 ounces, translating to a 9% increase year-over-year.

- This translated to a 5% increase in revenue year-over-year due to a higher average realized gold price, and a slight increase in ounces sold.

- However, costs continue to trend higher at a rapid pace, up more than 50% since 2020 levels despite lower sustaining capital in the period (Q2 2022 vs. Q2 2020).

- While Jaguar is cheap at a sub $150 million market cap, I continue to see much better opportunities elsewhere, especially given its ability to deliver into guidance last year with a large miss on deck this year from a cost standpoint.

Just over six weeks ago, I wrote on Jaguar Mining ( JAGGF ), noting that while I saw the stock as uninvestable, the stock's pullback below US$2.07 offered a very attractive opportunity from a swing-trading standpoint. The stock promptly rallied 30% in less than 30 trading days but has now pulled back towards its lows following a mediocre Q2 report. While production was revised slightly higher at Turmalina, which led to a 9% increase in production and higher revenue, costs soared, with operating cash flow sinking to just $9.4 million due to weaker margins. Let's take a closer look at the quarter below:

All figures are in United States Dollars unless otherwise noted.

{kind=link}

JAGGF Daily Chart (TC2000.com)

Q2 Production & Sales

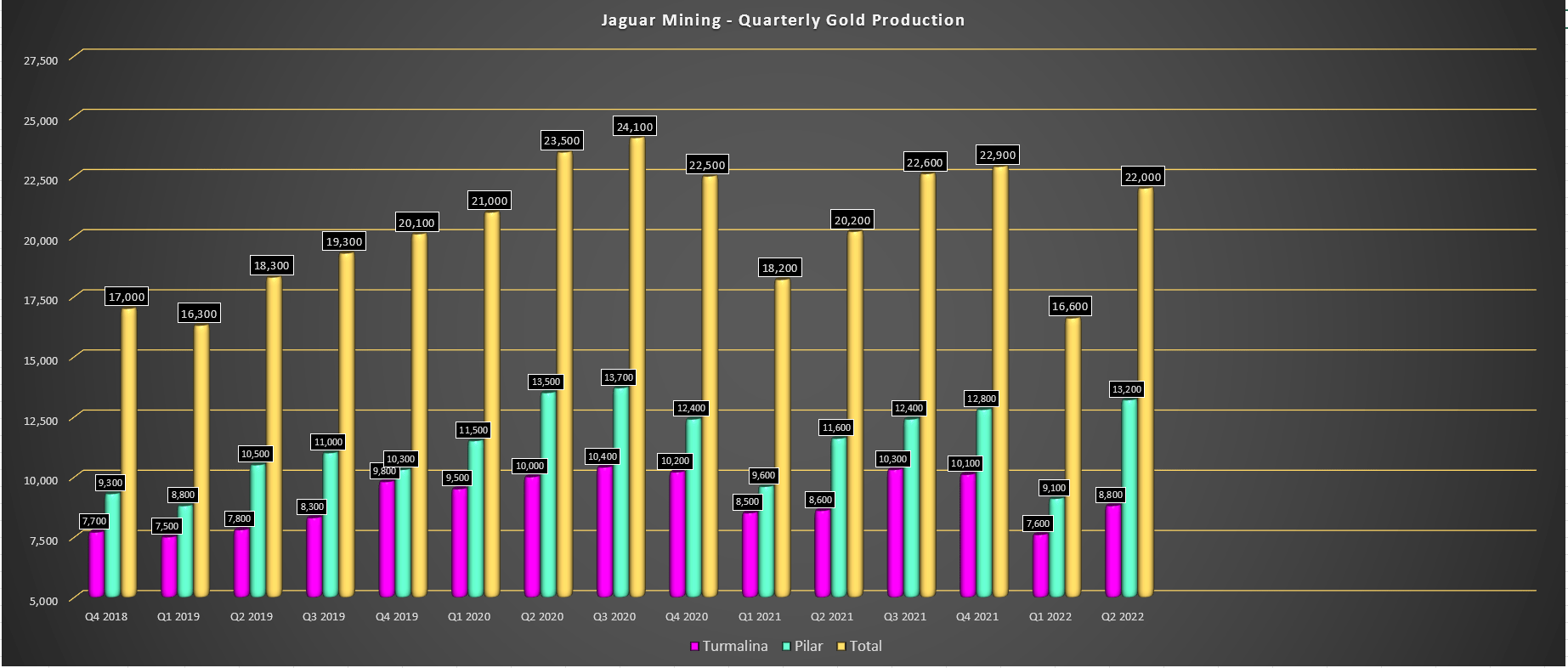

Jaguar Mining released its Q2 results last month, reporting quarterly production of ~22,000 ounces, a 5% increase from its initial pre-released July results after 1,000 ounces were found within the electrowinning tank walls at Turmalina. This led to a 9% increase in output year-over-year, with Jaguar finishing H1 with roughly 39,000 ounces produced. Given its updated guidance of 45,000 ounces in H2, (implying full-year output of ~83,600 ounces), Jaguar is tracking below the bottom end of its initial guidance of 86,000 to 94,000 ounces. This is quite disappointing, and while the company had difficulties due to a severe rainy season. However, even after the tough Q1, it noted that it would deliver into the low end of guidance, which no longer looks to be the case.

{kind=link}

Jaguar Mining - Quarterly Production (Company Filings, Author's Chart)

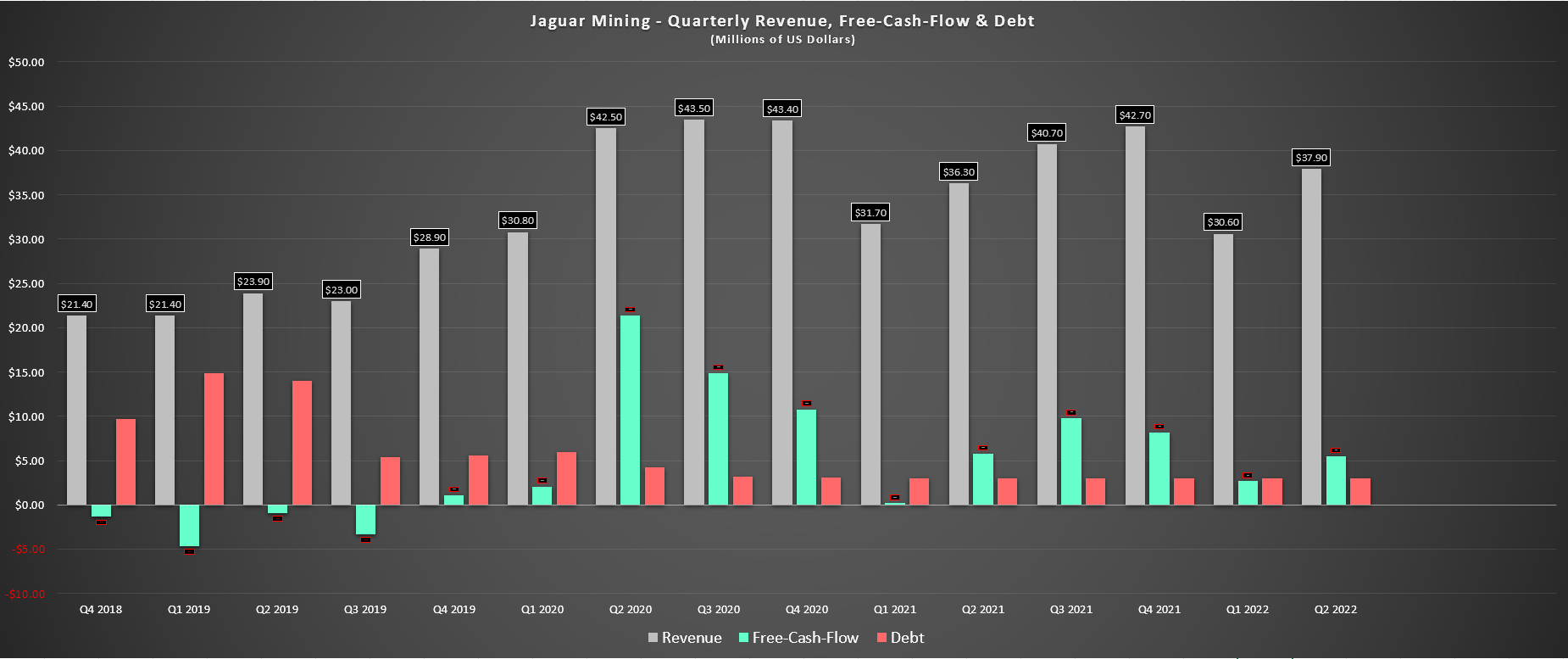

Moving to sales, Jaguar reported revenue of $37.9 million, up 5% year-over-year due to slightly higher sales volumes and a higher average realized gold price ($1,852/oz vs. $1,795/oz). However, with the gold price currently clinging to the $1,700/oz level, it's clear that it's going to be a much weaker second half for the company, with H2 revenue likely to come in at $80 million or less, down from $83.4 million in the year-ago period (H2 2021). Combined with the weaker profitability metrics, this doesn't bode well for free cash flow, which will likely continue to trend lower.

As discussed by the company, costs have been pressured by increased prices for consumables and labor. Judging by commentary from most companies, this should continue into H2 2022. Unfortunately, with Jaguar not benefiting from economies of scale and operating in a country (Brazil) with above-average inflation readings, I see it having a more difficult time controlling costs, which is what we see below, with AISC margins slipping to just ~26% in Q2. Let's take a closer look:

{kind=link}

Jaguar - Quarterly Revenue & Free Cash Flow (Company Filings, Author's Chart)

Costs & Margins

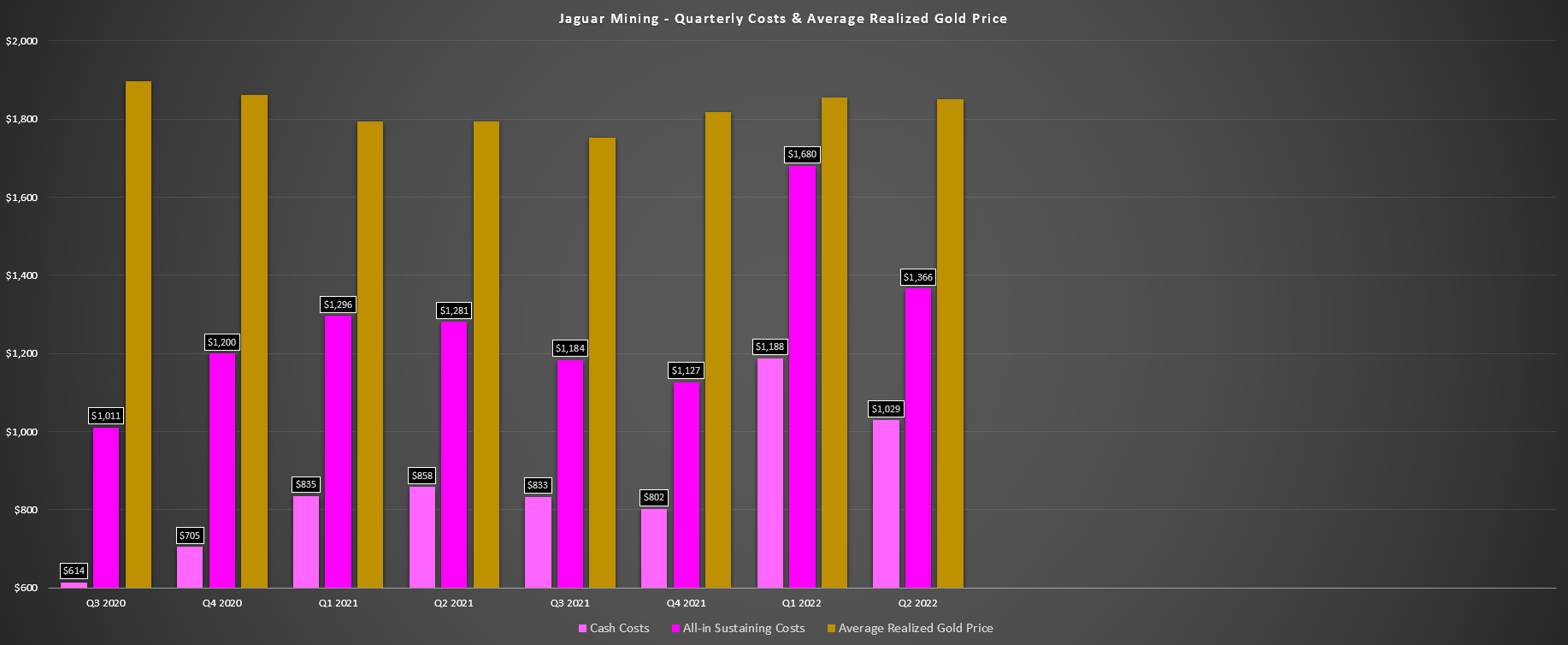

In my June update on Jaguar, I noted that I would be amazed if it delivered into its cost guidance ($1,150/oz - $1,250/oz), even with the company pointing out that it should be able to deliver into this guidance range, but at the high end , in its May update. In the most recent release, the company did not address that it's on track to once again significantly miss its annual guidance, with the only note being that it's expecting to produce 45,000 ounces at all-in sustaining costs of plus or minus $1,325/oz in H2 2022. Even if it hits the low end of that range ($1,259/oz), costs will come in above $1,325/oz for the year, based on H1 2022 costs of $1,506/oz, a $75/oz miss on the guidance range, not "near the top end of guidance."

{kind=link}

Jaguar Mining - Quarterly Costs & Average Realized Gold Price (Company Filings, Author's Chart)

The company's continued lack of conservatism when it comes to guidance makes it difficult to trust its future projections and is one reason I have continued to avoid the stock, in addition to its worsening margin profile. Looking at costs in Q2, they increased 7% year-over-year, which might not appear that bad compared to what we see sector-wide. However, it's important to note that Jaguar was up against very easy year-over-year comps, given that costs were up 45% in the year-ago period ($1,281/oz vs. $882/oz). So, on a two-year basis, all-in-sustaining costs have soared 55%, and this was despite lower sustaining capital spending ($4.6 million vs. $6.0 million).

{kind=link}

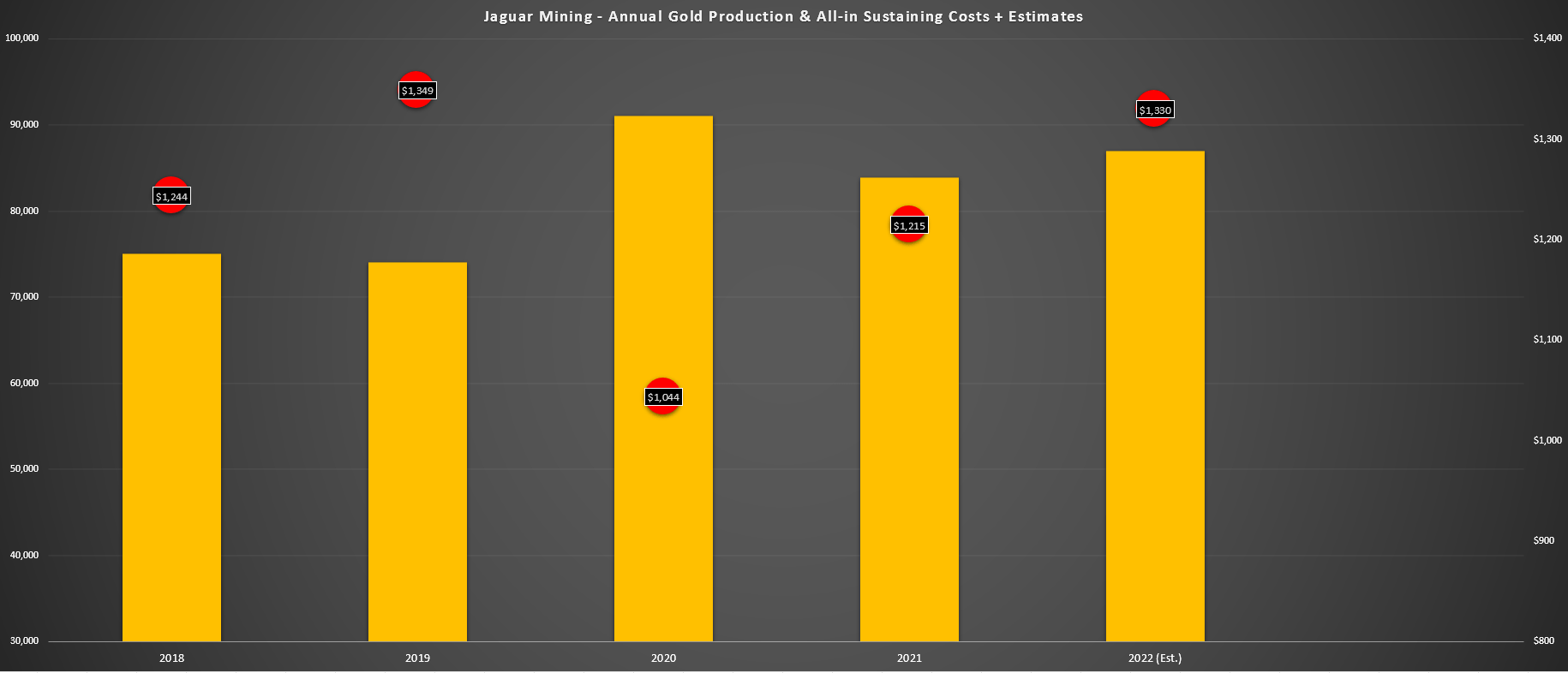

Jaguar Mining - Annual Gold Production & AISC (Company Filings, Author's Chart)

Some investors continue to anchor themselves to 2020, believing that Jaguar has a shot at heading back above US$5.00 or even to its highs near US$8.00 based on some message boards. However, as the chart above shows, Jaguar has an entirely different margin profile than when it headed above US$8.00 per share in Q1 2021. As we can see, it produced more gold (~90,000 ounces), and its AISC for the year came in at $1,044/oz. Based on current cost trends, I expect Jaguar's costs to come in at $1,330/oz or higher in FY2022.

So, even with the benefit of a higher gold price, AISC margins have plunged from $663/oz (FY2020) to $480/oz or less (FY2022), and that's with the benefit of a higher gold price in H1 2022. If we assume a gold price of $1,750/oz and sticky inflationary pressures in labor due to Brazil's high inflation rates, we could see all-in sustaining costs come in at $1,300/oz in FY2023, leading to just $450/oz margins with a $1,750/oz average realized gold price. To summarize, there's no reason to believe that Jaguar should return to US$5.00 per share, let alone US$8.00 per share, and while growth is on deck later this decade, it's too little and too late to make a difference medium-term.

Valuation & Technical Picture

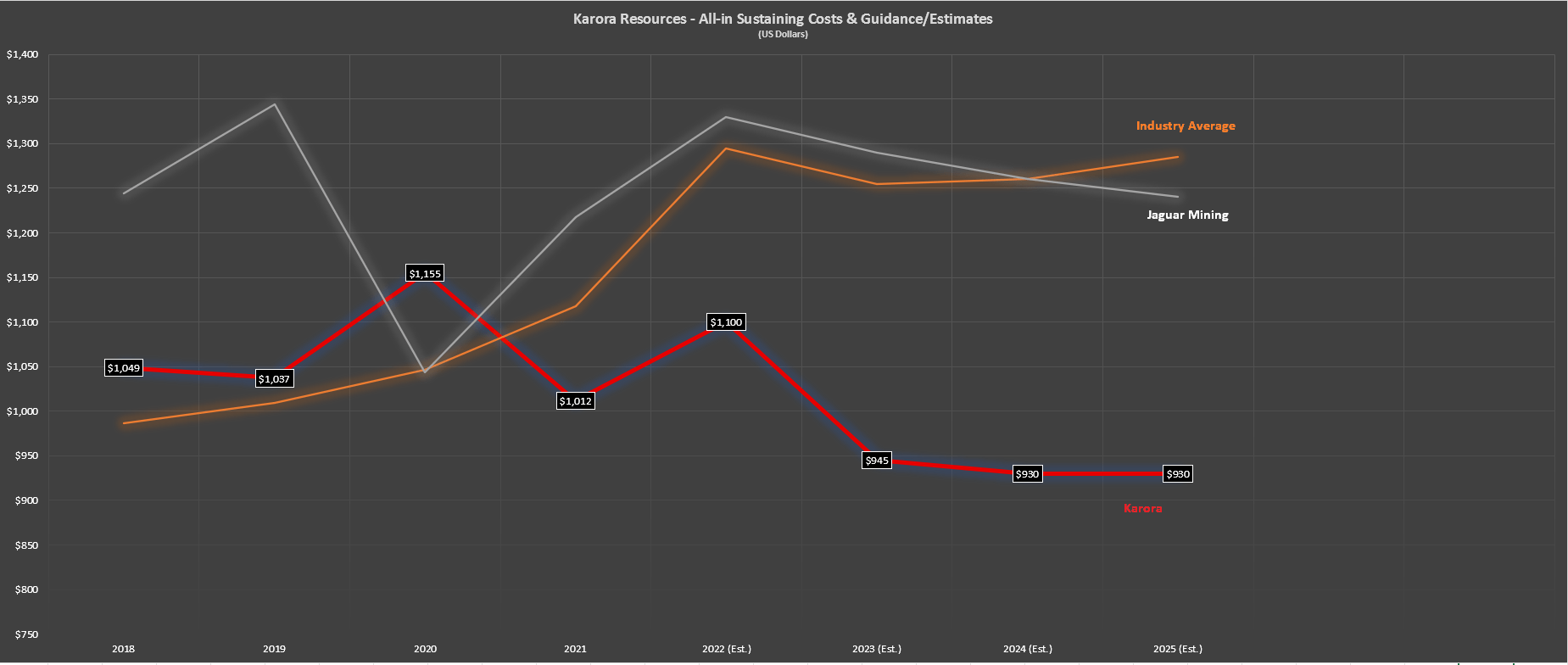

Based on ~71 million shares and a share price of US$2.20, Jaguar trades at a market cap of $156 million, a very reasonable valuation for a junior producer. That said, while Jaguar is becoming more reasonably valued, other names are also becoming even more attractively valued. One example is Karora ( OTCQX:KRRGF ), that's expected to have double the production profile of Jaguar in H2 2023 (180,000 ounces vs. 90,000 ounces) at much lower costs in a safer jurisdiction (Australia vs. Brazil). The chart below shows Jaguar's cost trend vs. Karora and the industry average, indicating that Karora is seeing margin compression yet is still very attractively valued (2.2x FY2023 cash flow estimates).

{kind=link}

Karora vs. Jaguar Cost Trends (Company Filings, Author's Chart & Estimates)

So, from a relative value standpoint, I think it's hard to justify owning Jaguar here when there are many more attractive opportunities. This is especially true if the gold price continues to weaken, which would give Jaguar negative all-in cost margins at a sub $1,700/oz gold price vs. Karora, which would still enjoy 30%+ all-in cost margins based on estimated FY2023 all-in costs of $1,100/oz. The other risk is that Brazilian elections are on deck. With a continued shift to the left in South America (Colombia, Peru), I have avoided most South American producers.

Summary

Jaguar Mining had a satisfactory H1, given the challenges from an operational standpoint. Still, the margin profile leaves much to be desired, and the company is on track for another significant guidance miss. This makes it difficult to put much faith in the company's future projections, with guidance having the possibility to come in more than $75/oz above the top end of its initial guidance, even with it reiterating the potential to deliver into guidance in May. In a violent bear market for the sector, I think it makes sense to bet on the best producers with the lowest risk of missing estimates, which means those consistently under-promising and over-delivering, not those missing guidance by a mile.

So, while Jaguar is undoubtedly valued attractively at a sub $150 million market cap and pays an attractive dividend, I think investors can do much better elsewhere in the sector from a risk-adjusted standpoint. Among large-cap producers, I prefer Agnico Eagle Mines ( AEM ), which offers growth, a 4.0% dividend yield, and owns some of the best mines globally in the safest jurisdictions. Among small-caps, I see Karora as a far more attractive bet than Jaguar, trading at a valuation reserved for some developers despite strong organic growth. That said, if JAGGF were to dip below US$1.80 before year-end, I would consider the stock from a swing-trading standpoint.

For further details see:

Jaguar Mining: Margins Continue To Remain Under Pressure