JAGGF - Jaguar Mining: Valuation Beginning To Improve

2023-05-28 09:25:04 ET

Summary

- Jaguar Mining released its Q1 results earlier this month, reporting higher production at lower costs despite a tough quarter operationally.

- However, although the headline results may have appeared impressive, a beat was inevitable in Q1 2023, with it lapping one of its weakest quarters in years during Q1 2022.

- From a positive standpoint, Jaguar continues to enjoy exploration success and while its organic growth story is in its infancy, it could offer a way to claw back lost margins.

- At a valuation of ~$120 million, Jaguar is the most reasonably valued it's been in years, and I see the stock as a Speculative Buy from a swing-trading standpoint below US$1.44.

The Q1 Earnings Season for the Gold Miners Index (GDX) is finally over and we saw mixed results across the board. Overall, the royalty/streaming companies put up solid results, given that they didn't have to deal with inflationary pressures, but the producers had a mix of beats and misses, with a clear trend of higher operating costs year-over-year. This resulted from higher fuel prices, labor, and costs on most consumables, even if we appear to be seeing some easing vs. Q3/Q4 2022 levels. Fortunately, Jaguar Mining (JAGGF) bucked this trend, which might seem positive on the surface, but it was because of being up against easy year-over-year comparisons. Let's take a closer look at the Q1 results and recent developments below:

All figures are in United States Dollars unless otherwise noted.

{kind=link}

Q1 Production & Sales

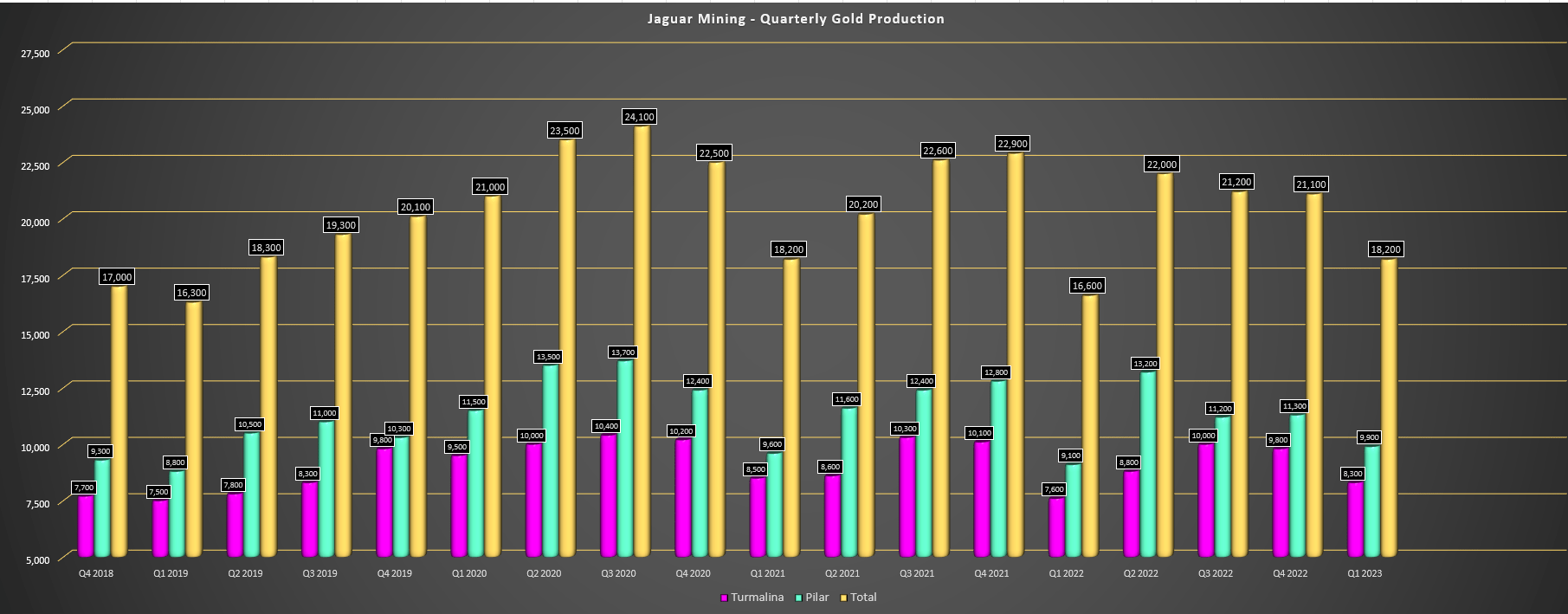

Jaguar Mining released its Q1 results earlier this month, reporting quarterly production of ~18,200 ounces of gold, a 9% increase from the year-ago period. Meanwhile, gold sales increased 15% to ~19,000 ounces, translating to revenue of $35.8 million (+17% year-over-year). However, while these headline results might have appeared impressive to investors, it's important to note that the company was up against easy year-over-year comps, lapping its weakest quarter of production in over three years (Q1 2022: ~16,600 ounces). In fact, production was actually materially lower on a three-year basis (Q1 2023 vs. Q1 2020) with increased tonnes processed offset by much lower grades.

Head grades at Turmalina and Pilar were 4.37 and 3.98 grams per tonne of gold, respectively, in Q1 2020, with grades of 2.84 and 3.54 grams per tonne of gold, respectively in Q1 2023.

Jaguar Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

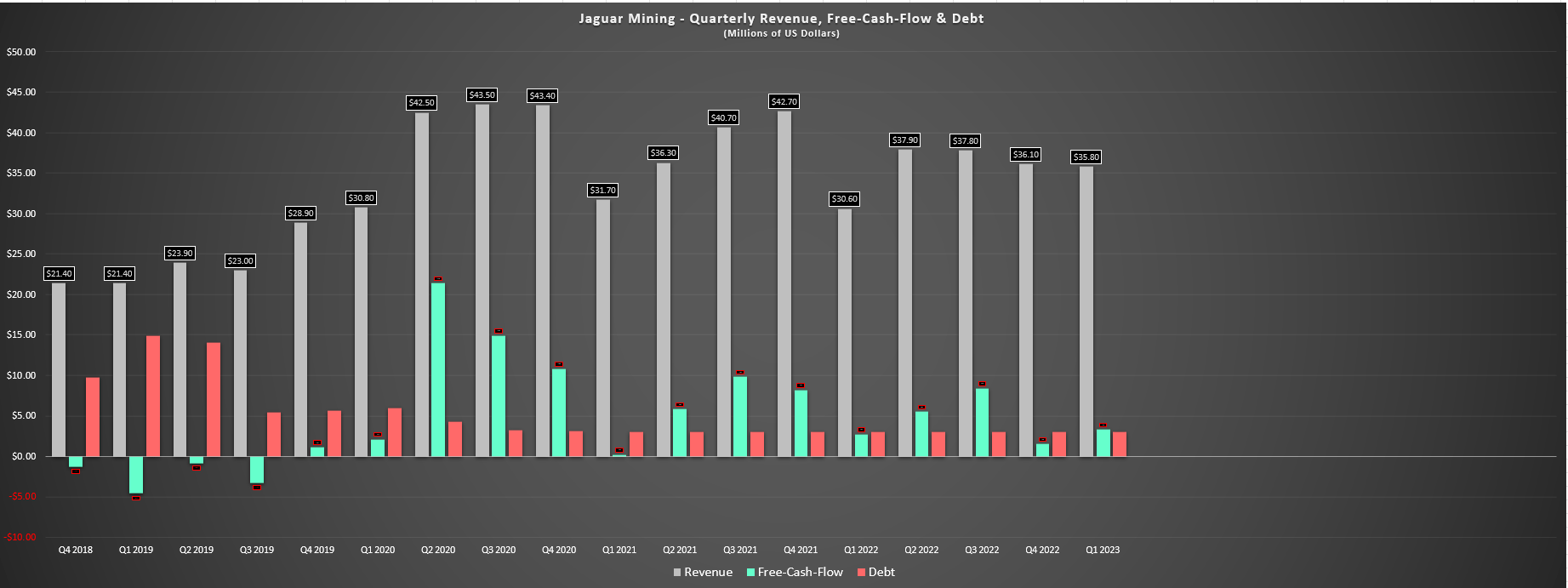

Given the higher production and 4% higher ounces sold vs. produced in the period (~19,000 ounces sold vs. ~18,200 ounces produced) combined with a higher gold price ($1,886/oz vs. $1,855/oz), revenue increased materially to $35.8 million vs. $30.6 million in the year-ago period. However, like its production results, Jaguar was up against relatively easy comps here as well and revenue remains well below peak levels of $40.0+ million enjoyed even with similar realized gold prices. Plus, while production and revenue were up year-over-year, the company is tracking well behind its annual guidance for the second consecutive year, with ~18,200 ounces representing just 21.1% of its FY2023 guidance midpoint.

Jaguar Mining - Quarterly Revenue, Free Cash Flow & Debt (Company Filings, Author's Chart)

{kind=link}

Finally, from a free cash flow standpoint, Jaguar Mining reported $3.3 million in free cash flow, a decent result if the company calculated free cash flow like most producers. However, free cash flow is defined by Jaguar as operating cash flow minus sustaining capital (but not non-sustaining capital) and with adding back asset retirement obligation, making the numbers look more attractive than they were. So, if we use the generic free cash flow generation, which is operating cash flow minus sustaining and non-sustaining capital, free cash flow was barely positive in the period despite a near $1,900/oz gold price, with free cash flow of just ~$1.3 million (after adding back asset retirement obligations). This was roughly flat year-over-year, and hardly anything to write home about.

Costs & Margins

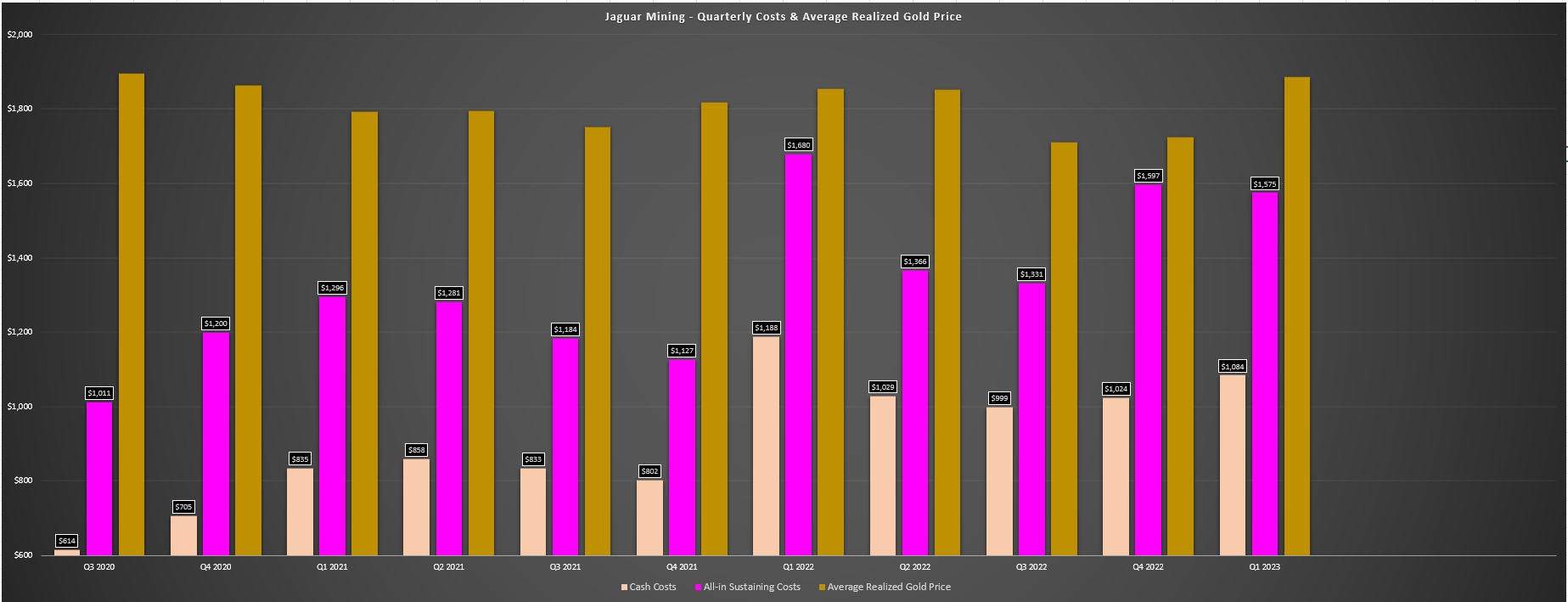

Moving over to costs and margins, Jaguar reported cash costs of $1,084/oz in Q1 2023, an improvement from $1,188/oz in the year-ago period. Meanwhile, all-in sustaining costs [AISC] came in at $1,575/oz, which while at industry-lagging levels were better than the year-ago period ($1,680/oz). This decline in AISC was despite higher sustaining capital spend due to increased primary development and higher G&A costs, but benefited from lapping easy comparisons and higher sales volume relative to ounces produced. Plus, while costs were lower, they are well above the annual guidance range of $1,275/oz to $1,375/oz, and all-in cost margins were barely positive at $134/oz. From an AISC margin standpoint, margins improved to $311/oz vs. $175/oz, a material increase but well below the industry average of ~$570/oz in Q1.

Jaguar Mining - Quarterly Costs & Average Realized Gold Price (Company Filings, Author's Chart)

{kind=link}

Looking at the trend in costs above, Jaguar has continued to struggle from a margin standpoint, which isn't surprising given the above-average inflation in Brazil, the stronger Brazilian Real in Q1, and the impact of inflationary pressures on producers sector-wide. And given this severe margin compression with limited free cash flow generation, it's encouraging that the company suspended its dividend to focus on growth and exploration vs. continuing to pay dividends out of what would be a weakening cash position. And given the exploration success enjoyed to date, I believe the market will eventually reward the company for this decision, even if Jaguar continues to be a massive underperformer since 2020, down ~80% from its highs.

From a positive standpoint, commentary sector-wide during Q1 Conference calls suggest we are seeing some easing of inflationary pressures, and while the Brazilian Real started the year on a tear vs. the US Dollar ( UUP ), we've seen some mean reversion since. This should help Jaguar to deliver close to its FY2023 guidance mid-point of $1,325/oz, but I'm not that optimistic about the company's ability to beat this cost figure for the year. So, from a delivery on guidance standpoint, Jaguar continues to disappoint, with FY2022 being an enormous disappointment with ~81,000 ounces produced vs. a guidance midpoint of 90,000 ounces.

Recent Developments

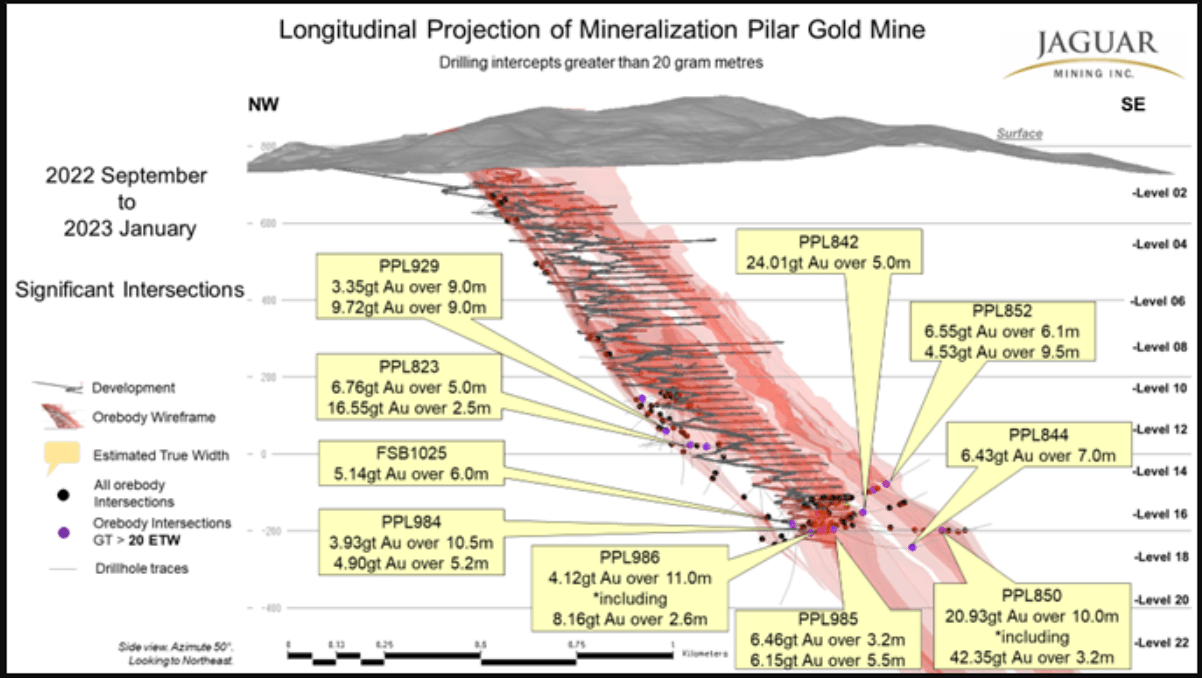

Moving over to recent developments, there is a silver lining, and that is Jaguar's exploration success. As shown below, the company continues to hit solid intercepts at its larger Pilar Mine, with highlight intercepts that include 3.2 meters at 42.35 grams per tonne of gold, 5.0 meters at 24.01 grams per tonne of gold, and 9.0 meters at 9.72 grams per tonne of gold near existing infrastructure. These strong results at grades above the average reserve grade suggest the potential to continue replacing mining depletion at similar or better grades, which should allow Turmalina to maintain its ~50,000-ounce production profile longer-term. Meanwhile, at the Catita Target, which lies southwest of Corrego Brandao (shallow oxide target), Jaguar reported two decent sulfide intercepts here, which included:

- 2.5 meters at 3.6 grams per tonne of gold.

- 5.9 meters at 9.51 grams per tonne of gold.

Pilar Mine Long Section & Recent Drill Highlights (Company Website)

{kind=link}

Corrego Brandao and Catita may represent relatively small resources today, but they are in close proximity to the Caete Plant, a plant that has excess capacity with the potential to process upwards of 2,000 tonnes per day (~1,100 tonnes per day being processed currently). Hence, near-surface oxide ounces from Corrego Brandao would represent low-hanging fruit to take advantage of excess processing capacity. So, while these grades aren't earth-shattering by any means and are lower-grade than the feed being sent through the plant at the Caete Plant currently, this could add incremental ounces at a reasonable cost post-2025, with what should be relatively modest upfront capital expenditures.

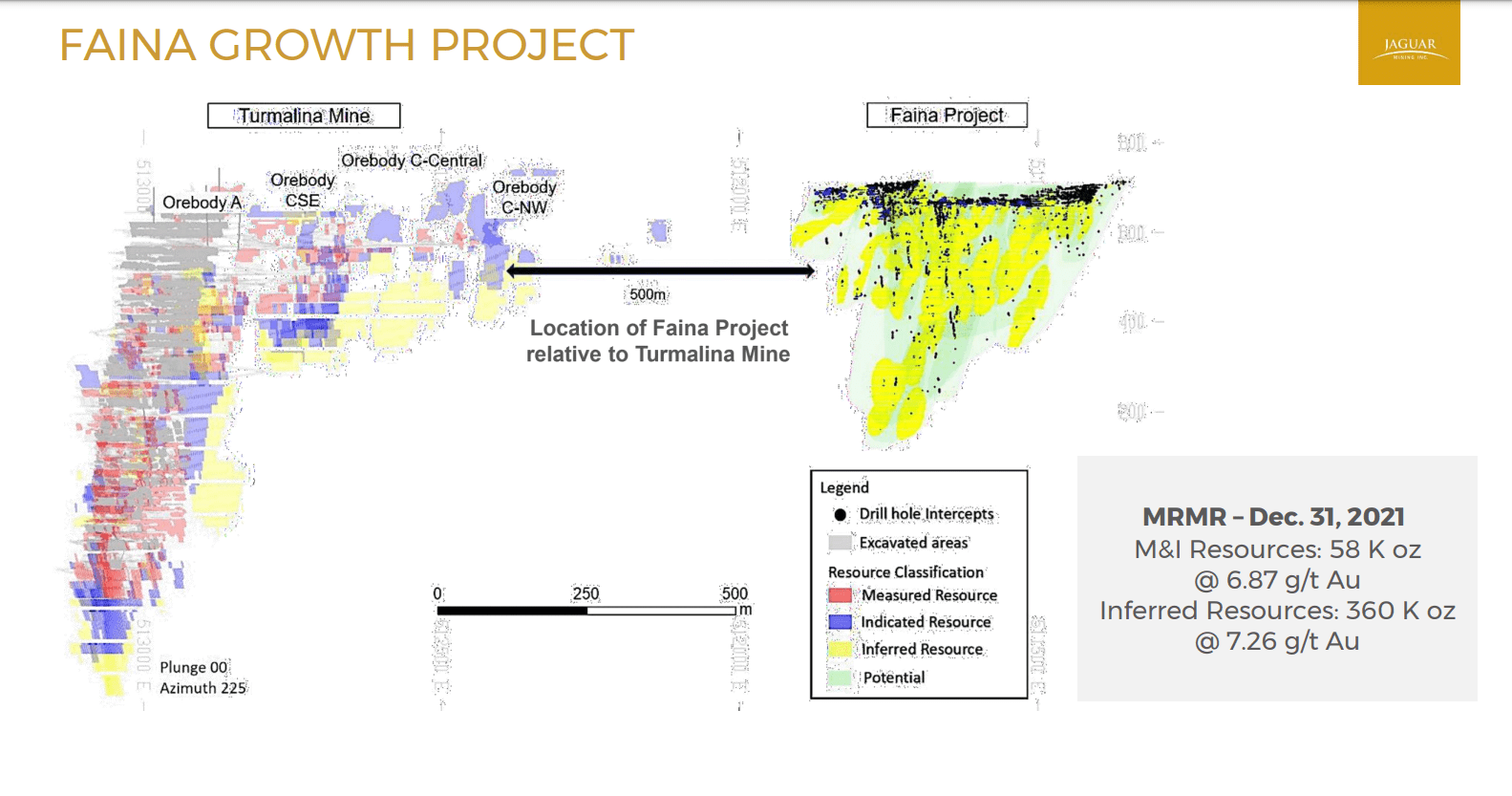

Moving over to the company's smaller Turmalina Mine, the company is currently progressing underground ramp development from Orebody C at Turmalina to the Faina deposit, which lies barely 500 meters away and has shown promising drill results. The goal is to reach the Faina Zone later this year and continue working towards the orebody next year, with Faina having a measured & indicated resource of ~233,000 ounces at 5.08 grams per tonne of gold. That said, and while this could provide incremental production growth, recoveries are likely to be sub-par in the interim until a better solution is reached from a processing standpoint. This is because Faina ore is semi-refractory and recoveries won't likely exceed 60% using the current CIL process at the Turmalina Plant.

{kind=link}

That said, longer-term processing options are available with modifications to the plant which could boost recoveries at this higher-grade asset. Jaguar noted that there's the potential for recoveries to be improved to ~85% with a combination of gravity concentration followed by flotation of gravity tails. Roasting and Acid POX were also studied, with recoveries of ~80.6% and ~83.5%, respectively. Jaguar noted that options to improve recoveries would be the construction of a pressure oxidation circuit on site or the construction of a flotation circuit only, and the sale of concentrates. We should get more information on potential processing solutions in the next eighteen months and what the cost might be to add these circuits to improve recoveries longer-term at Faina.

Valuation

Based on ~75 million fully diluted shares and a share price of US$1.58, Jaguar Mining trades at a market cap of US$120 million, a significant departure from its ~$500 million market cap just over two years ago when I noted to avoid the stock. The good news is that this much lower valuation has finally baked some margin of safety into the stock, with Jaguar now trading at just ~2.6x cash flow, even assuming a conservative cash flow estimate of $45 million for FY2023. That said, Jaguar remains a high-cost miner that is more susceptible to corrections in the gold price because of its razor-thin margins. And while it is an organic growth story, this growth won't show up immediately, and while Faina can increase production, a solution from a metallurgical standpoint will be required to recover more of these ounces.

Using what I believe to be a fair multiple of 4.5x cash flow for Jaguar Mining, given that it's a high-cost junior producer in a Tier-2 ranked jurisdiction and FY2023 cash flow estimates of $45 million, I see a fair value for the stock of $202 million. If we divide this by ~75 million fully diluted shares at year-end, this translates to a fair value of US$2.70. And while this represents a meaningful upside from current levels, I am looking for a minimum 50% discount to fair value to justify starting new positions in micro-cap names. So, while I see Jaguar Mining as the most attractively priced it's been since 2020 and a Speculative Buy at US$1.43, I continue to see more attractive bets elsewhere, especially on a risk-adjusted basis.

Summary

Jaguar's Q1 results were once again disappointing and, while the company has maintained its FY2023 guidance of 84,000 to 88,000 ounces at $1,275/oz to $1,375/oz AISC, I'm not overly confident in its ability to meet or beat the midpoint of 86,000 ounces at sub $1,325/oz AISC. And with several smaller producers looking to grow production meaningfully at more attractive margins over the next couple of years, it's hard to justify owning a micro-cap producer like Jaguar with all-in costs near $1,750/oz. That said, and for those that don't mind stepping out on the risk curve, Jaguar is a high-risk, high-reward bet that could easily gain 50% if it can turn things around. So, while I remain on the sidelines, I see the stock as a Speculative Buy at US$1.43.

For further details see:

Jaguar Mining: Valuation Beginning To Improve