BNL - January's 5 Dividend Growth Stocks With 4.93%+ Yields

2024-01-18 10:56:39 ET

Summary

- Dividends can play an important part in an investor's portfolio for generating regular cash flows that can be reinvested or used on expenses for living.

- Companies that can grow their dividends consistently can be a great way to build one's passive income over time, compounding growth further for those investors who can reinvest.

- We look at names that have not only been able to grow their dividends more regularly but also sport some high yields as well.

Written by Nick Ackerman.

For some background on this monthly publication, here is my view on dividend growth stocks :

Dividend growth stocks aren't always the most exciting investments out there. They often aren't grabbing the headlines, and they aren't the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn't generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there - I've owned a few that I'm not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position "paid off." It is all returned back into your pocket from that point forward.

All of this being said, it is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. As with any initial screening, this is just an initial dive - more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I'll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn't mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn't an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 420 stocks at this time from the 414 listed last month. I'll link the screen here , though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn't hurt.

I will share the top 25 that showed up as of 01/04/2024.

{kind=link}

DHT Holdings ( DHT ) ranks the highest this month, but that company pays an inconsistent dividend. Banco Latinamericano de Comercio Exterior S.A. ( BLX ) also showed up this month, but that company also doesn't raise consistently. In fact, they had paid a flat dividend for several years heading into Covid. During Covid, they cut and have only simply held the dividend steady since.

We had previously included The Western Union Company ( WU ) when looking at this screening. However, as mentioned in last month's screening article, the company hasn't delivered an increase in its dividend for several years now. Additionally, the performance of the company doesn't bode well for that to change anytime soon.

With all that said, it is the start of a new year, but we have some familiar names to touch on today. We have three REITs to look at, and I believe that REITs look set to perform well over the coming years as rates go down. The names this month that we are going to take a quick look at are NewLake Capital Partners (NLCP), Innovative Industrial Properties ( IIPR ), BCE Inc ( BCE ), Broadstone Net Lease ( BNL ) and The Williams Companies ( WMB ).

NewLake Capital Partners 10.01% Yield ((NLCP))

NLCP first showed up in our September 2023 article and has once again shown up on this list. Another name that frequently shows up for this screening is IIPR. This is the first month we are going to touch on some quick updates for both, as IIPR also made the list this month. Of course, for those familiar, these are both industrial REITs, but more specifically, they own warehouses that are related to the cannabis industry.

Not only are REITs under pressure due to higher costs on their borrowings, which is a huge source of where growth has been able to come out of these structures over the zero-rate environment period, but their underlying business is also facing higher costs. Given the industry that NLCP and IIPR operate in, these tenants aren't necessarily the highest quality in terms of their credit. With higher borrowing costs and less interest in speculating further on equity positions, their tenants have faced pressure in the last couple of years as opposed to when things were flying high in 2020/2021.

The most exciting news for NLCP since our prior update is that they more recently raised their dividend once again. This REIT was similar to IIPR, which had been raising more frequently than annually, but going through the higher interest rate environment, they slowed that pace down. I don't blame either of the companies either, as the environment was and even still is quite uncertain. The latest raise also wasn't anything to boast too loudly about, but it was good for another penny per quarter or an increase of 2.56%.

{kind=link}

Earnings estimates for NLCP come in at FFO estimates of $1.84 for fiscal 2024, which is above the $1.77 estimates for fiscal 2023. It is worth noting this was a drop from the expectations of FFO of $1.80 in our prior update. Though they currently have $1.33 FFO in the bag for 2023 already, meaning FFO is expected to come in basically in line with where it was in the first three quarters.

At a payout ratio of 87% for next year's earnings estimates, we are somewhat on the higher end, even for a REIT. That further reinforces why the management team was and is likely to continue being cautious in terms of raising their payout going forward. However, at a yield that is coming in at around 10%, you are getting a juicy yield upfront. If one wants to see more growth, they may turn to reinvesting a portion of this back into more shares.

NLCP currently trades over the counter, which often leads to a lack of liquidity due to relatively lower trading volume. That said, they have made comments in the past that uplisting to a major exchange could be an "impactful catalyst" to seeing a higher valuation of their shares.

Innovative Industrial Properties 7.51% Yield ((IIPR))

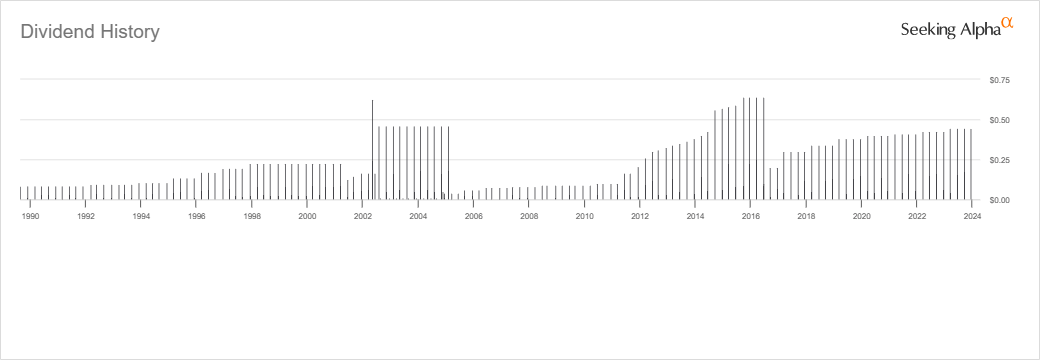

We last touched on IIPR in our October 2023 article, but it is a regular name to make this list with its attractive and once again growing yield - but growing for the right reason now. They recently raised their dividend after holding it steady for the five previous quarters. Similar to NLCP, it was a small raise. In this case, it was a two-cent raise, but given it went from $1.80 to $1.82 quarterly, it worked out to a 1.1% raise.

IIPR Dividend History (Innovative Industrial Properties)

They had originally been able to raise every quarter in the early few years of their life, then it switched to a semi-annual raise, and now it might appear that it will be irregular raises as they can. There is certainly nothing wrong with that, as they can retain cash to grow their business rather than resorting to raising debt.

Given the $8.20 in expected earnings this year, the FFO payout ratio for the latest dividend annualized would come to around 88.8%. That puts it in line with where NLCP's payout is. It also means there might not be too much cash sloshing around for growth after the dividend is paid.

The yield here might not be as hot as NLCP, but it does still come in at a high yield of around 7.5%. This also follows along with the REIT's AFFO history and forecasts going forward. There was rapid growth as they were getting started, but the direction is more sideways now.

{kind=link}

As we mentioned above, the industry here has faced pressure. IIPR was able to participate in that more speculative market, but NLCP showed up pretty late to the public market. IIPR most definitely was one of those names that participated in the wild markets of 2020/2021. Cash was cheap, and there was plenty of it going around.

YCharts

I think that both IIPR and NLCP are worthwhile candidates for a more speculative portfolio. I continue to hold IIPR myself.

BCE Inc. 7.07% Yield ((BCE))

BCE is a Canadian telecom company, and similar to its U.S. peers AT&T ( T ) and Verizon ( VZ ), it offers investors a steady and high yield. Coming in at just over 7%, BCE is definitely delivering on the yield front, but not only that, they've been able to raise their dividend consistently for many years . However, being that they pay in CAD, U.S. investors might see a 'variable' dividend due to the fluctuations of currency values when it converts from CAD to USD.

{kind=link}

On the other hand, similar to its U.S. counterparts, growth in this industry is coming in at a crawl and has even gone backward on occasion. Growth in earnings is expected to come in 2024 and 2025, but that has been moving sideways, more or less, for several years now.

BCE Earnings History and Forward Estimates (Portfolio Insight)

{kind=link}

This sideways movement is quite similar to its share price, which is what has occurred over the last decade. In fact, over the last decade, it looks like shares have been down about 4%.

Free cash flow in their latest quarter did come up to $754 million, which was a 17.4% increase. Shares outstanding of 914 million against their latest $0.9675 means they paid out $884.3 million. In the first nine months, FCF came in at $1.855 billion, so that doesn't bode well for the $2.653 billion that would be paid in dividends during a three-quarter period. That said, the Q1 2023 FCF came in at an abnormally low $85 million, which was down by over 88% from the Q1 2022 $716 million.

Still, it would seem, on that front, that the U.S. counterparts are safer in terms of their FCF payout. At some point, it would seem inevitable that something has to give: the dividend or the earnings. The yield is very nice here, but this does seem a bit concerning.

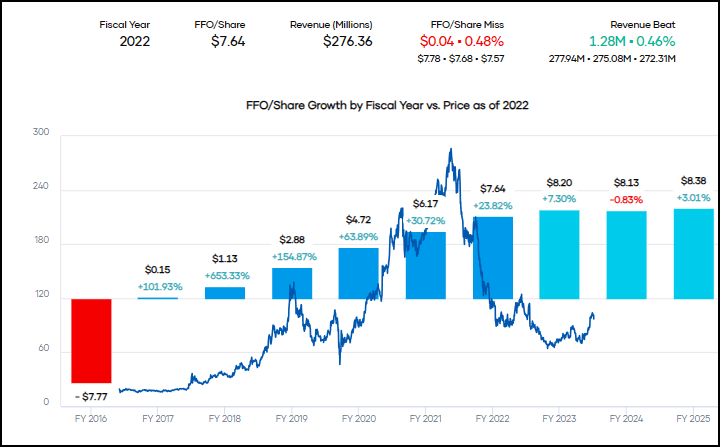

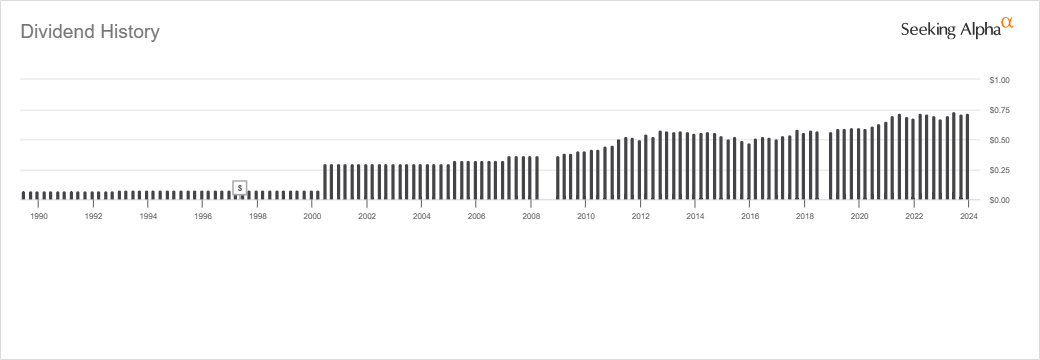

Broadstone Net Lease 6.7% Yield ((BNL))

BNL last made our monthly article in October 2023, but we first touched on it in January 2023. After seeing it was an interesting, diversified REIT and after a good reminder of it coming up last time, we recently did a full coverage of that name. After that, it still remained interesting and something that I believe is probably worth pursuing for an investor looking for another REIT to add to their income portfolio. Shares did inch up a bit since that update, but the overall REIT space was really on fire coming out of the October lows, and the Fed pivot further fueled this.

BNL Performance Since Last Coverage (Seeking Alpha)

For what it is worth, I'm also not alone in believing that BNL looks like a promising prospect worthy of some capital being thrown at it. Across the board, SA Analysts, Wall Street and even the usually short-term driven Quant rating scale all give it a 'Buy.' rating. Wall Street analysts have an average price target of $19.17, which would indicate a nearly 14% upside.

BNL Rating Summary (Seeking Alpha)

This is still a fairly new REIT to the public market, though, and the raises for the dividend haven't been anything wild but enough to make it interesting. Given the 6.7% high dividend yield, some slower dividend growth isn't the worst thing.

{kind=link}

So the yield is nice upfront, and the bit of growth is also a bonus, but the downside here is that FFO growth expectations just aren't there. Over the coming years, FFO is essentially expected to be flat. Fiscal 2023 and 2024 are both showing estimates for $1.55, with $1.57 for fiscal 2025.

Of course, anything can happen between now and then, but at some point, just like BCE, something has to give. Either the dividend growth has to pause, or earnings need to start heading north to continue to support a growing dividend sustainably. The payout ratio here is 73.5%, so we do have some cushion here before it would be overly concerning.

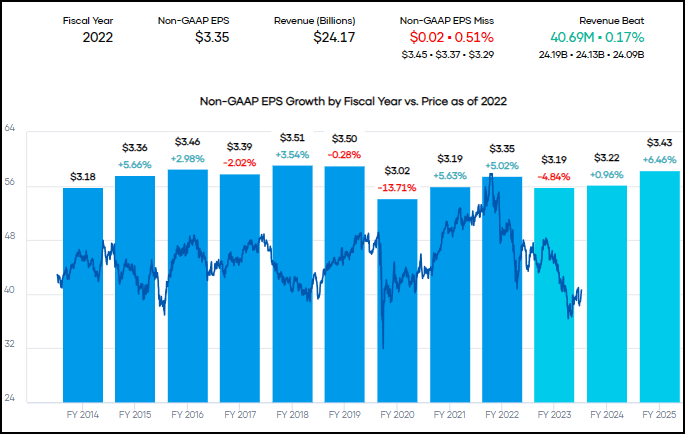

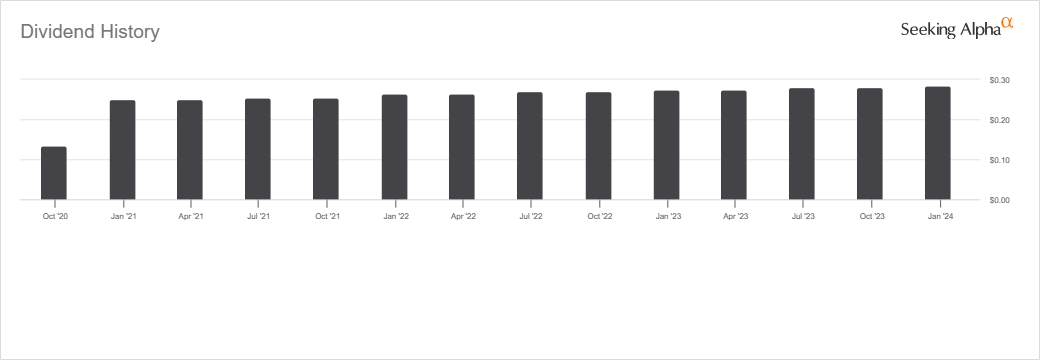

The Williams Companies 4.93% Yield ((WMB))

WMB also makes another appearance in our monthly article, with the prior and only other time we touched on it being in our May 2023 piece. The dividend history for WMB has been quite volatile, much like the energy sector that it belongs to. WMB operates as a gas pipeline company with gathering & processing operations as well.

{kind=link}

As a C-corp, there is no K-1 but instead a 1099. That being said, this is one of those companies that can still have a bit of return of capital in its distribution . ROC distributions can be beneficial for those holding in a taxable account because it can be a way to defer tax obligations potentially until the shares are sold. This is because ROC reduces an investor's cost basis rather than being taxable in the year received.

While it has been volatile, it's been much more steady since the last oil collapse, even being able to maneuver successfully through Covid. The 4.93% yield that this dividend payer comes with also makes it a solid income play.

{kind=link}

Less than 5% for an energy operation is likely to cause some reluctance from income investors since several energy pipeline peers can pay more - particularly those in the MLP space. That said, the dividend coverage here also remains incredibly strong, albeit even if it did come down a touch from the prior quarter-over-quarter period. The more important year-over-year comparison did show a bit of growth.

{kind=link}

Whether dividend coverage is 2.26x, as shown for the quarter, or 2.38x, it is still quite strong coverage with basically no worry for a cut. It would have to see a dramatic downfall in the economy before coverage became so weak that the dividend would be threatened, in my opinion. They are also forecasting full 2023 guidance of dividend coverage at 2.25x, which is only the last quarter of the year missing. We'll see if they hit that target toward the end of February when they announce their full-year results.

That is all positive, and on top of being an investment-grade rated organization with no outsized near-term debt being due, it is in an even stronger, more financially sound position.

For further details see:

January's 5 Dividend Growth Stocks With 4.93%+ Yields