BNL - January's 5 Dividend Growth Stocks With 6.16%+ Yields

Summary

- New year, new investment opportunities.

- This month's dividend growth screener article presents ideas worth exploring further.

- We have a new diversified REIT name making the list for January 2023.

Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on January 4th, 2023.

Dividend growth stocks aren't always the most exciting investments out there. They often aren't grabbing the headlines; they aren't the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn't generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield-traps out there - I've owned a few that I'm not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position "paid off." It is all return back into your pocket from that point forward.

Inflation remains on the downtrend, but that doesn't mean it isn't still very high. The Fed is remaining fairly aggressive too, as they expect further interest rate hikes into the new year. Albeit at a much slower pace than what we saw previously. The 50 basis point hike in December seems to confirm a slower pace going forward. That could leave stocks and fixed-income investments pressured once again.

YCharts

Although I'm generally more optimistic and expect that we could see some mild returns in 2023 after a down year, at the same time, I don't necessarily need returns in the short term. Investing in dividend growth stocks over the long run tends to work itself out in the longer term.

All of this being said, it is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. These are September's 5 dividend growth stocks that might be worthwhile for a deeper exploration. As with any initial screening, this is just an initial dive - more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I'll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors but earnings payout ratios, debt and free cash flow are amongst these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn't mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn't an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 561 stocks at this time—from December's 540 listings. I'll link the screen here , though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn't hurt.

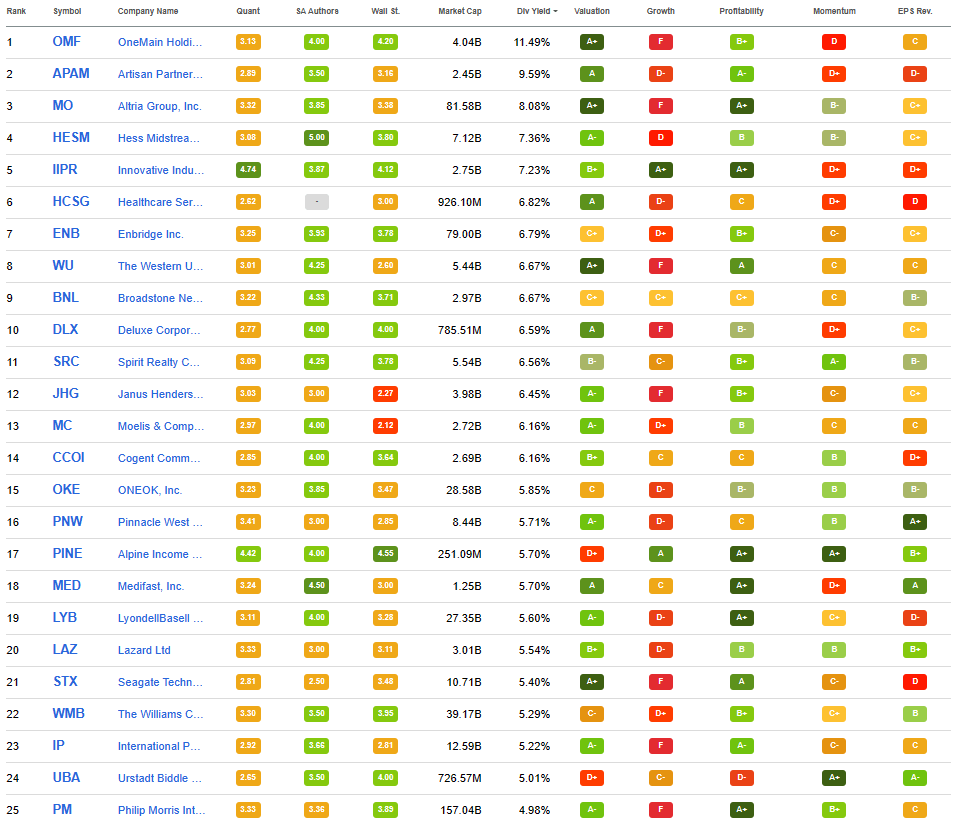

I will share the top 25 that showed up as of 01/04/2023.

25 Top Dividend Stocks (Seeking Alpha)

{kind=link}

OneMain Holdings ( OMF ) makes its way on the list again, as it frequently does. However, since we last covered it just in November, we will skip past the overview of that name this month. This also includes Enbridge ( ENB ) and The Western Union Company ( WU ).

Additionally, Healthcare Services Group ( HCSG ) and Janus Henderson Group ( JHG ) made their way to last month's article.

We will also skip over Artisan Partners Asset Management ( APAM ) as they pay a variable dividend. We will also leave Deluxe Corporation ( DLX ) out - despite having an interesting name - due to paying a flat dividend for years. I want to highlight dividend growers with dividends that can generally trend higher over time. Similarly, Spirit Realty Capital ( SRC ) will also be excluded. Although SRC raised its dividend last year, it might make this list at some point in the future. It isn't that these names aren't worthwhile, but they just don't quite fit with the article on dividend growers I'm trying to highlight.

That leaves us with giving Altria Group, Inc. ( MO ), Hess Midstream LP ( HESM ), Innovative Industrial Properties, Inc. ( IIPR ), Broadstone Net Lease, Inc. ( BNL ), and Moelis & Company ( MC ).

MO, HESM, IIPR and MC are all names we've covered before, so we can take a quick look to see how they've been doing since. BNL is a new name, and it was one I considered leaving off. However, they've raised a few times since launching and initiating their dividend in 2020.

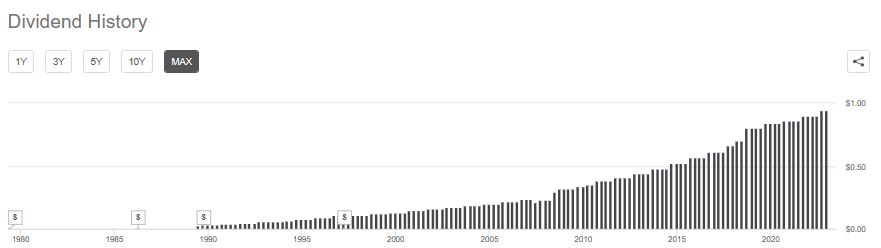

Altria Group - 8.26% Yield

MO needs little introduction as they have 53 years of dividend increases under their belt. Despite the widely known and serious health conditions that smoking can cause and the continued anti-smoking campaigns, this oldie but goldie keeps puffing out the cash to shareholders.

MO Dividend History (Seeking Alpha)

{kind=link}

Albeit, the share price has certainly taken a hit.

YCharts

They've taken initiatives in smokeless tobacco products and in cannabis. None of those investments have really paid off, which seems to be what is hitting the stock price. Juul in 2022 was certainly a big setback, but it also led to them ending their non-compete agreement. Longer-term, that might be a good thing as they can develop their own product or invest elsewhere.

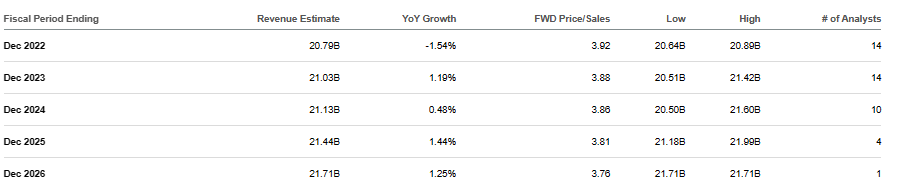

I believe that new growth avenues are something that MO needs, as revenue growth going forward is expected to be anemic or even decline. EPS estimates are a bit better because they certainly have pricing power.

MO Earnings Estimates (Seeking Alpha)

{kind=link}

However, that won't last forever and isn't a viable long-term growth strategy, in my opinion. They target being smoke-free by 2030 , so we need to see products that will replace cigarette sales start gaining traction.

Hess Midstream - 7.59% Yield

What's better than an annual distribution increase? That's right, a quarterly boost! HESM has hit the ground running with these regular increases. We last covered this name in October, and they announced another quarterly raise later in the month after touching on it.

HESM Dividend History (Seeking Alpha)

{kind=link}

As energy prices have decreased, HESM shares have been under pressure. After such a strong run in the energy space, it wouldn't be completely unrealistic to expect energy to be a middle-performing sector this year. With a recession, there could be even more cause for concern.

However, that's where midstream companies can be a consideration. With their mostly fixed-fee contracts, their cash flows are fairly predictable. That means the payouts to investors can be fairly predictable too. That being said, a higher energy pricing environment will still be where they shine best.

An important distinction is that HESM is a midstream C-Corp for tax purposes, which means a 1099 and no K-1. Some investors find the additional paperwork of a K-1 off-putting. Although, I think investors should make investment decisions on fundamentals and not because of a tax form.

Since our last update, they have also posted their quarterly earnings . Most notable is that they raised their full-year 2022 guidance for net income and adjusted EBTIDA. They also reiterated the target of 5% distribution growth through at least 2024.

Innovative Industrial Properties - 7.33% Yield

Being a real estate investment trust ("REIT") in 2022 was not a good thing. Being a speculative marijuana REIT operating was even worse. I personally hold shares of IIPR, and I held right through 2022. So I felt the meteoric rise and now the downfall of holding this investment.

YCharts

At the same time, they've remained committed to growing their dividend to shareholders. The latest increase was a much slower pace, but an increase nonetheless. The dividend history below is from the website .

IIPR Dividend History (IIPR Website)

Being more conservative with an increase during economic uncertainty seems to be a prudent move. Their tenants are newer, given the newness of the cannabis industry in the U.S. becoming more mainstream. However, these are basically startups with weak financials. That means they are at risk of being unable to pay rent during an economic slowdown. It's basically that simple, and that is part of why the share price of IIPR has come screaming lower.

There will also be more competition in the field they operate in as things become even more mainstream. That said, analysts still expect growth, which should translate into a growing dividend for IIPR investors.

For now, I'm content with continuing to sit on this investment. I bought it several years ago, so I'm still above water as my cost basis is around $92.

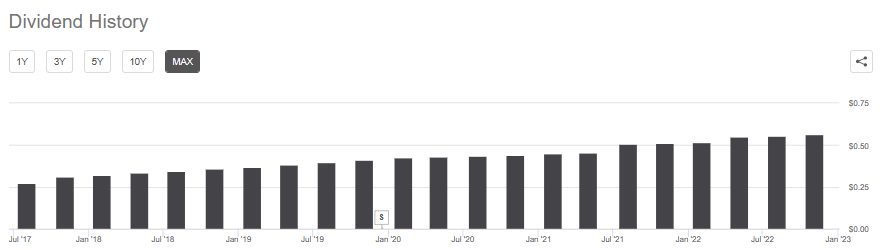

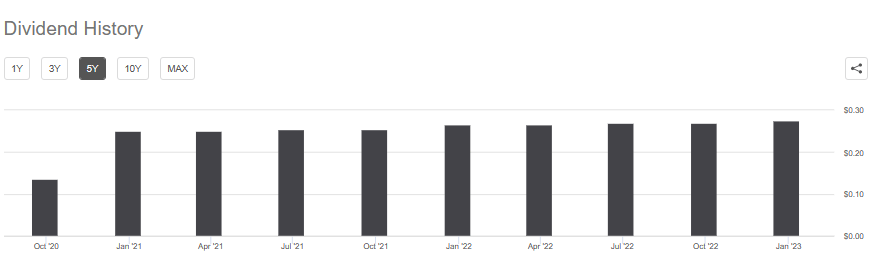

Broadstone Net Lease - 6.79% Yield

This is the only new name on the list this month and is particularly interesting. Most people that have read my articles know that as an income investor, I tend to lean toward REIT investments.

They were founded in 2007, but it didn't go public until 2020

Broadstone Net Lease, Inc. (NYSE: BNL ) is a REIT that acquires, owns, and manages primarily single-tenant commercial real estate properties that are net leased on a long-term basis. Since the company’s formation in 2007, BNL’s investment strategy has been grounded in strong fundamental credit analysis and prudent real estate underwriting. The continued growth and consistent performance of our portfolio has delivered predictable cash flow and returns to investors through multiple real estate cycles.

Being a diversified REIT means it grabs my attention. They operate in several indentures, even touching office properties, which I'm not particularly fond of.

As of September 30, 2022, BNL’s diversified portfolio consisted of 790 individual net leased commercial properties with 783 properties located in 44 U.S. states and seven properties located in four Canadian provinces across the industrial, healthcare, restaurant, retail, and office property types.

Fortunately, office space is the minority of their property types . The highest exposure by a significant margin is the industrial space.

BNL Property Type (BNL Presentation)

Raising their dividend five times since 2020 is also catching my attention.

BNL Dividend History (Seeking Alpha)

{kind=link}

They have a dividend that is well covered, as they reported a Q3 AFFO of $0.35. They guided for 2022 full-year AFFO of between $1.38 and $1.40. The current annualized dividend works out to $1.10, which means a payout ratio of only 79%. With growing AFFO and room for error, the dividend here feels quite safe and should continue to grow. That's why it made the list, despite having a relatively shorter history.

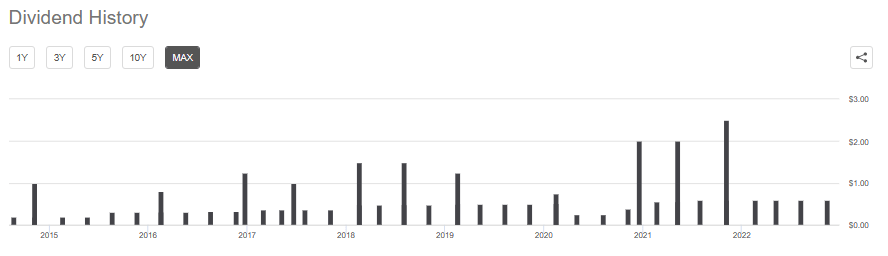

Moelis & Company - 6.16% Yield

Another area of the market that took a hit in 2022 was investment banking. There wasn't a lot of activity, so MC suffered. The outlook isn't necessarily that rosy, either. Most economists believe that a recession could be a real possibility in 2023 with the Fed raising rates.

MC's dividend history might first appear erratic.

MC Dividend History (Seeking Alpha)

{kind=link}

However, this is due to special dividends being paid during good times. The regular dividend has grown since 2020, even if it is harder to see. In 2020, they cut their regular due to the COVID crash. It went from $0.51 to $0.2550 from Q1 to Q2. They also have frozen the dividend at $0.60 since Q3 2021.

That means there are now six quarters in a row of the same dividend being received. In the latest earnings call , there were remarks about the dividend specifically.

Mike Brown

And just to change gears to the capital return, you guys always return about a hundred percent of capital to shareholders. Clearly, it's a more challenging environment here. So some of the inbound questions we've gotten from investors is about the regular dividend here. So your EPS was 37 cents this quarter and your regular dividend is $0.60. And your cash levels certainly seem adequate and your, your free cash flow is typically higher than what your EPS would indicate. But just given the fact that we are still in a quite a turbulent period here, as you mentioned any comment there about the regular dividend here is it still safe here at $0.60?

Ken Moelis

Yeah. So, remember your $0.37 includes a one-time change in the comp ratio to bring it up. The way we think about it is we're supposed to bring our accrual up to what our best guess of the year is. So we did it all in the quarter.

Joe Simon

And full-year earnings are approximately maybe a little higher than the year-to-date dividend. So -- and then we also have the non-cash charge of equity.

Ken Moelis

Look, if anything we've had conversations, and I'll say this, but it's up to the board to do it about increasing the regular dividend. We just felt like in this market it felt kind of strange to do that. So we do want to return a 100% of capital, and we think we've got more excess capital that we could return. We just haven't done it, because it would seem strange to increase the dividend in the wake of what's going on.

Of course, the usual caveat of "it's up to the Board" was mentioned. However, they didn't specifically say the dividend was safe; instead, the CEO and founder hinted that it was likely safe. He also felt they could raise, but they didn't do so simply because of the current environment. I think that's at least a little bit reassuring that the current dividend remains safe. That would be despite a decline in EPS for 2022. Analysts also expect a slight decline in EPS in 2023.

For further details see:

January's 5 Dividend Growth Stocks With 6.16%+ Yields