JHG - Janus Henderson: Downside Concerns Eased Buy Rating Reinstated

2023-11-02 17:34:08 ET

Summary

- Janus Henderson reported a solid 3Q23 result, with key operational trends ahead of expectations.

- The announced $150m buyback program is modest, but reduces downside risk relating to the potential for aggressive M&A activity.

- Improved product investment performance in Equities and stability in the investment management fee margin ease concerns regarding future earnings headwinds.

- With a dividend yield above 6%, a solid balance sheet, and an undemanding valuation, JHG warrants a Buy rating.

Introduction

In early August, with the stock then trading at around $27.15 per share, I downgraded Janus Henderson Group ( JHG ) to Hold based on concerns arising from disappointing outcomes on net flows, investment fee margin softness, and organization instability. By late October, with equity markets performing poorly, JHG had drifted down towards $22. The company released 3Q23 results on November 1, 2023 that were well-received by the market, with the stock rallying by almost 5% on the day. In this note I’ll highlight and discuss key positives and negatives that caught my eye in reading through the 3Q23 materials and review my JHG rating.

3Q23 Positives

Key positives reported in the 3Q23 materials are summarized and discussed below:

- JHG announced a $150m buyback. Since CEO Ali Dibadj set out his strategy for the group, I’ve been concerned that JHG would chew through its excess capital with acquisitions designed to diversify the group’s investment product suite (refer to my February 2023 note for discussion on this topic). Whilst $150m is not a huge buyback in the scheme of things (being ~3.7% of JHG’s market capitalization), it does slightly mitigate acquisition risk downside. M&A remains on the cards however, so the buyback announcement has not eliminated acquisition risk concerns.

- The cost-out program is going well. Run-rate cost efficiencies of $50m pa will be achieved by the end of FY23E. This outcome is better than the original target saving range of $40m to $45m pa set out in FY22. As a result of the progress on cost-out, management guidance for FY23E non-compensation expense growth (on FY22) has been lowered from mid-to-high single digits (%), to mid-single digits (%).

- The announced delisting from the Australian Stock Exchange strikes me as a sensible move, with very little downside and modest benefits in terms of lower costs and organizational simplicity.

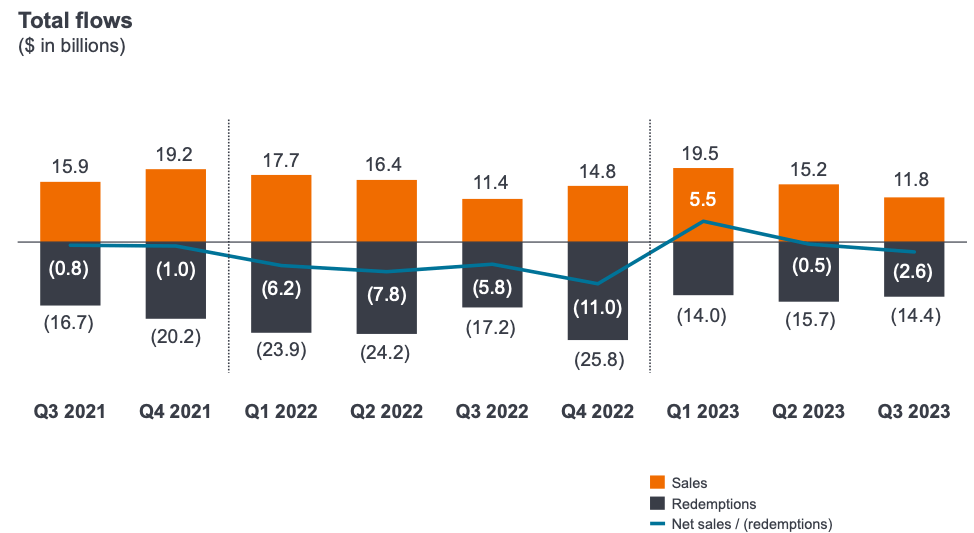

- At 2Q23, the CFO guided to net outflows of -$3.5bn to -$5.0bn in 3Q23E. Actual net flows for 3Q23 came in materially better than management’s expectation, at -$2.6bn. That being said, I realise it’s a bit of a stretch to classify a net outflow of AUM as a positive. On a financial year-to-date basis, JHG’s net flows through to the end of 3Q23 are still in positive territory, thanks to a strong 1Q23.

{kind=link}

Source: JHG 3Q23 Presentation, slide 5.

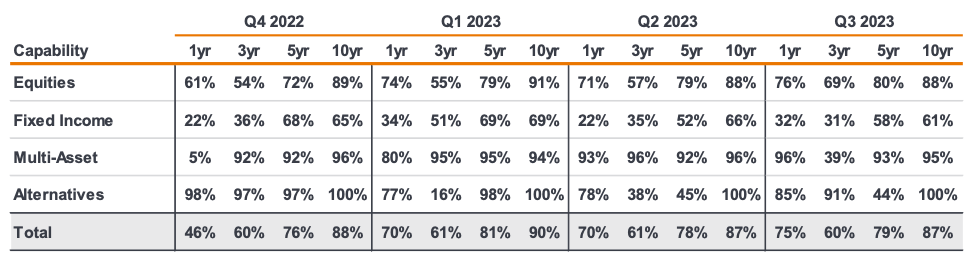

- Peer-relative investment product performance for Equities improved further in 3Q23. Peer-relative Equities performance numbers are now better than they have been for several years. Equities is a key product segment for JHG (being 61% of group AUM) and strong peer-relative rankings should be supportive of sales into the retail channel in particular. On a benchmark-relative basis, the Equities performance numbers are solid, and the 1-year outcome of 83% of AUM beating benchmark is the strongest outcome I have observed since I began tracking JHG in late FY18.

{kind=link}

Source: JHG 3Q23 Presentation, slide 21.

- In 2Q23, the net management fee margin declined sharply to 48.5bp of AUM (1Q23 49.8bp), driven by JHG winning a large institutional mandate in 1Q23 that came on to the books at a low fee rate. In the 2Q23 management speech, CFO Roger Thompson guided to stability in the margin for 3Q23E. Management’s guidance proved to be reliable, with the 3Q23 net management fee margin coming in at 48.7bp, very slightly up on 2Q23.

3Q23 Negatives

Key negatives reported in the 3Q23 materials are summarized and discussed below:

- Peer-relative Fixed Income performance remains weak. There was an improvement at the 1-year measure, but with only 32% of Fixed Income AUM in the top two Morningstar quartiles for 3Q23, this is nothing to get excited about. At the 3-years measure, a disappointing 31% of Fixed Income AUM was in the top two Morningstar quartiles for 3Q23. Fixed income is the group’s second largest AUM bucket, making up 21% of JHG AUM as of 3Q23. It is important that Fixed Income performance improves from here given that higher fixed income yields are now attracting investor attention to this asset class.

For further details see:

Janus Henderson: Downside Concerns Eased, Buy Rating Reinstated