JBI - Janus International: Good Growth Prospects And Reasonable Valuation Make It A Buy

2023-06-29 11:03:36 ET

Summary

- Janus International Group is expected to see strong demand for self-storage capacity additions, particularly in the R3 segment, which includes the conversion and expansion of old and existing facilities.

- The company's margins are expected to benefit from volume leverage in the upcoming quarters, ongoing cost reduction initiatives, and price increases. These factors should help the company offset inflationary pressures from labor and logistics.

- The company's stock looks attractive at its current valuation, and its strong market position and ongoing demand for additional self-storage capacity are expected to positively impact its revenue in the upcoming quarters.

Investment Thesis

Janus International Group ( JBI ) is expected to continue experiencing strong demand for self-storage capacity additions, particularly in the R3 segment (Restore, Rebuild, and Replace), which includes the conversion and expansion of old and existing facilities. This, combined with a solid backlog and long-term secular growth trends such as an aging self-storage stock, high occupancy rates, and the rise of E-commerce, is likely to benefit the company's revenue in the long run.

In terms of margins, Janus International Group is expected to benefit from volume leverage in the upcoming quarters. Additionally, ongoing cost reduction initiatives and price increases should help the company offset inflationary pressures from labor and logistics, leading to margin expansion in 2023 and beyond. The stock looks attractive at its current valuation which coupled with its near and long-term prospects make it a good buy.

Revenue Analysis and Outlook

Janus is a provider of end-to-end customer solutions for self-storage which includes products (e.g. Roll up doors, commercial sheet doors), system and components, wireless solutions (Noke), and value-added services.

JBI Product and Services Offering (Investor Presentation)

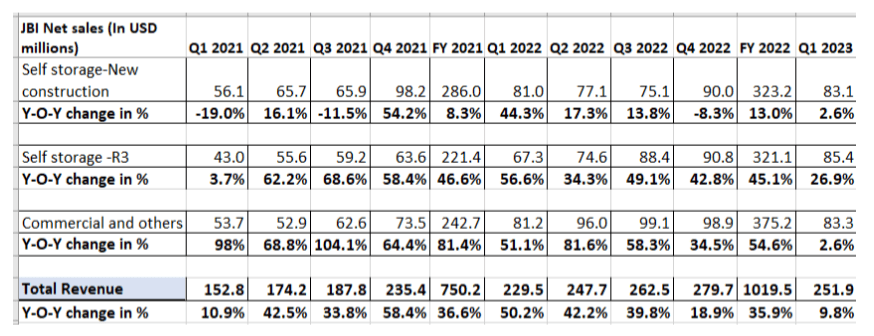

JBI has posted strong growth over the last couple of years, thanks to high occupancy and strong revenue growth of the company's primary customers including self-storage REITs and other institutional clients, which drove capital investments. The company also benefited from price increases, market share gains, and M&A. After seeing a Y/Y revenue growth of 36.6% in FY21 and 35.3% in FY22, the company's revenue growth has returned to a more normalized level in the first quarter of 2023. During Q123, the company's revenue increased by 9.8% year-over-year, reaching $251.9 million. The growth was primarily driven by the strength of the R3 segment, which experienced a 26.9% year-over-year growth, amounting to $85.4 million. This growth was supported by the addition of new capacity through expansion and conversion efforts. On the other hand, the New Construction and Commercial and others segments saw modest growth of 2.6% each compared to the same period last year, due to difficult comparisons

JBI Historical Revenues (Company Data, GS Analytics Research)

{kind=link}

The growth outlook of the company remains positive. While I am not expecting the growth to be as strong as what we have seen in FY21 and FY22, the company can easily meet or beat management's long-term target of 4-6% annual organic growth in the coming years, thanks to solid end market demand. There is a potential for further upside if management engages in bolt-ons and M&A. The self-storage industry is experiencing high demand nationwide, resulting in occupancy rates exceeding 90% , surpassing the historical level of 85%. This high occupancy rate is driving the demand for new construction in the self-storage sector across North America, which should provide long-term benefits to the company's New Construction segment.

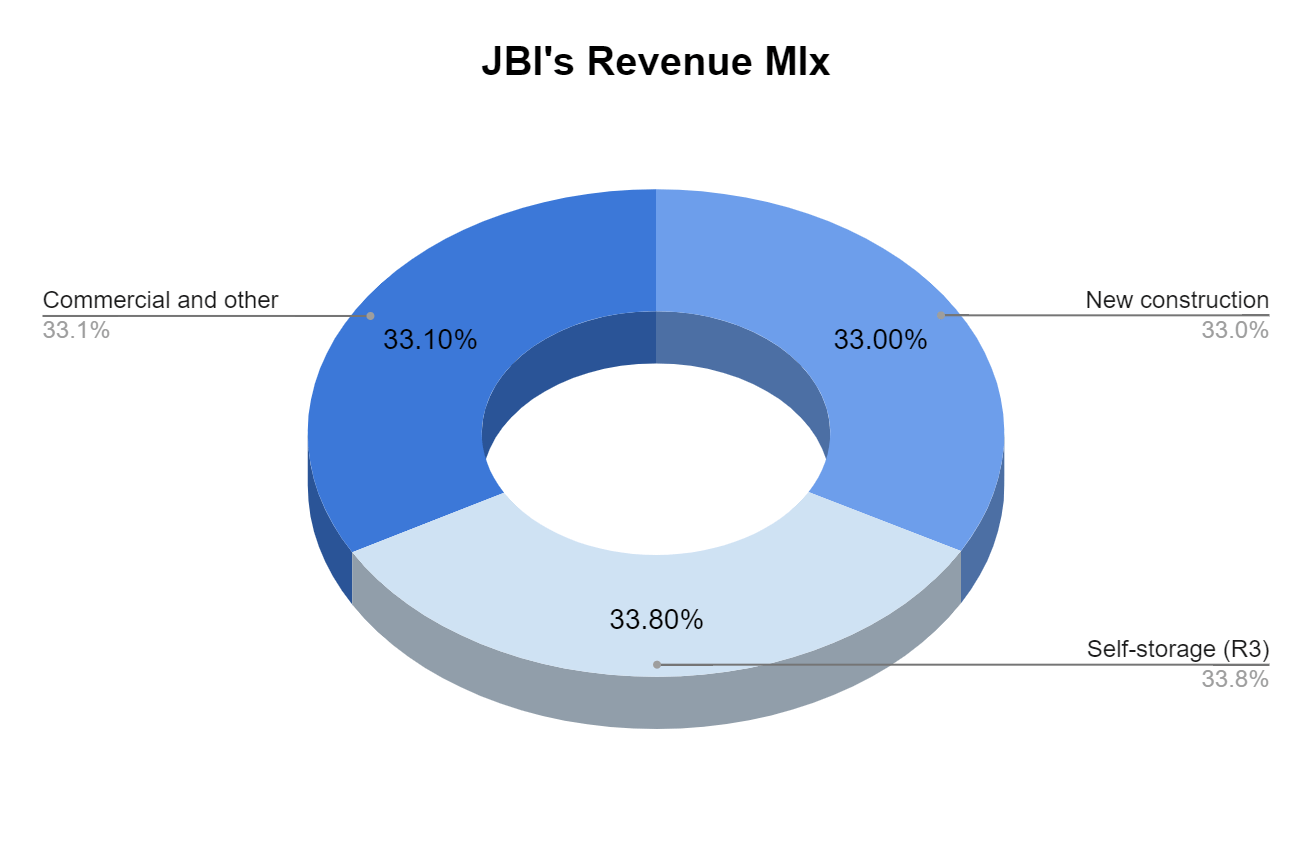

The R3 segment is expected to benefit from the aging of existing facilities in North America. Management anticipates that approximately 60% of the current self-storage facilities are over 20 years old, creating a potential need for replacement and refurbishment. This presents an opportunity for the company to generate additional revenue in this segment. Further, the R3 offering such as conversion and expansion are also benefiting from the availability of brick-and-mortar retail capacity, which is attractive to JBI customers and they can convert and expand there rather than opening new greenfield capacity

{kind=link}

JBI Revenue Mix (Company data, GS Analytics Research)

The company also has a good opportunity to gain a share in the commercial business. JBI's commercial and other segment, which primarily focuses on commercial metal doors used across various industries such as hotels, warehouses, pharmacies, schools, etc., currently holds a relatively small market share in a significantly larger addressable market and management is focusing on gaining share. Additionally, the increasing prevalence of e-commerce and the growing demand for warehousing and distribution centers, driven by the e-commerce sector, position the company favorably for future growth. These factors are expected to contribute to the company's revenue growth in the coming years.

Furthermore, the company is also well-positioned to grow inorganically. It has benefitted from the acquisition of DBCI and ACT in recent years. The company also has brought down its leverage meaningfully in recent quarters. The company ended the last quarter with a net leverage ratio of 2.4x, down from 4.3x in Q1 2022, and within the target range of 2x-3x. These strong financials provide further support for potential bolt-on acquisitions and contribute to the company's revenue growth in the upcoming years.

Margin Analysis and Outlook

On the margin front, the company has benefited from volume leverage as well as price increases in recent quarters. In the first quarter of 2023, the company's adjusted EBITDA margin expanded by 480 basis points year-over-year to reach 24.3%. This margin growth can be attributed to the implementation of productivity initiatives and commercial actions (price increases) during the quarter. These measures were successful in offsetting the higher costs, particularly in labor and logistics.

JBI Adjusted EBITDA Margin (Company data, GS Analytics Research)

Looking ahead, the anticipated volume growth in the upcoming quarters is expected to result in volume leverage, thereby benefiting margins. This, combined with the ongoing cost reduction initiatives and price increases should help the company offset the negative impact of higher costs, particularly in labor and logistics. As a result, margin expansion is expected in the coming quarters.

Furthermore, the company remains focused on innovation and the adoption of the Noke Smart Entry System, which aims to reduce facility labor and operating costs for the company’s clients. This is a high-margin offering and should improve the company's product mix. Additionally, the company has made improvements in its contract structuring to better address cost and pricing variability, ensuring appropriate margins relative to the services and solutions provided.

Overall, I believe that the company's emphasis on cost reduction initiatives, expansion of the Noke Entry system, and price increases should help drive its margin. The company’s long-term EBITDA margin target is between 25% to 27% which I believe is achievable.

Valuation and Conclusion

The company's stock is currently trading at a forward price-to-earnings (P/E) ratio of 11.61x. This looks cheap when we consider the company’s double-digit EPS growth potential over the coming years as well as its long-term growth potential.

{kind=link}

JBI Consensus EPS Estimates and P/E (Company Data, GS Analytics Research)

The company's strong market position and ongoing demand for additional self-storage capacity are expected to positively impact its revenue in the upcoming quarters. Furthermore, the company's margins are anticipated to benefit from volume leverage and continued cost-reduction initiatives, aligning with its long-term goal of achieving an EBITDA margin within the range of 25%-27%.

Given the company’s reasonable valuation and good near as well as long-term prospects, I have a buy rating on the stock.

For further details see:

Janus International: Good Growth Prospects And Reasonable Valuation Make It A Buy