JBI - Janus International: Steady Margin Overshadows Top Line Moderation

2023-06-21 18:27:30 ET

Summary

- Janus International Group has experienced margin stability in Q1 2023 due to its R3-Self-storage business and the adoption of Nok? remote access products.

- Despite facing challenges such as project delays in the housing sector and high labor costs, Janus plans to improve operating margins and reduce debt in 2023.

- The stock is currently undervalued, and investors are advised to hold it for steady medium-term returns.

Janus Focuses On The Margin Side

Janus International Group ( JBI ) manufactures and supplies roll-up and swing doors, hallway systems, relocatable storage units, and facility and door automation technologies for self-storage, commercial, and industrial buildings. Recently, it has added R3-Self-storage, which added to its capacity significantly via conversions and expansions. On top of that, Nok? remote access products' installed unit growth and the eCommerce market proliferation have been the most remarkable drivers of its margin stability in Q1. I think the Noke platform has enabled the company to integrate hardware and software efficiently for its customers.

However, JBI experienced an extended construction time in Q1 due to project delays in the housing sector. It also experienced high labor costs associated with scaling up and additional investments in Nok?. So, it plans to adjust its design, eliminating the lag in the cost recovery, resulting in improved operating margins in Q1. It also substantially improved cash flow generation, reducing debt in 2023. The stock appears to be relatively undervalued. I suggest investors "hold" it for steady medium-term returns.

Current Drivers And End Markets

Janus achieved robust growth in Q1 2023 compared to a year earlier based on a solid performance in the restoration, rebuilding, and replacement (or R3) business. The company sells through three channels: New construction self-storage, R3-Self-storage (or R3), and Commercial & Other. Recently, it added significant new capacity via conversions and expansions. Under the current industry environment, I think the demand for R3 offerings will be higher than greenfield new construction sites due to the excess availability of idle brick-and-mortar retail capacity. Its R3 business becomes essential because it optimizes unit mix and idle land. It also enables higher rental rates and competes with modern self-storage facilities efficiently.

At the start of 2023, JBI garnered a significant share of the interior building market through REITs (real estate investment trusts) and non-institutional operators. REITs comprised ~30% of the overall self-storage market. The eCommerce growth provides Janus with exciting opportunities in the self-storage, commercial, and industrial sectors.

Investors may note that Janus acquired Noke in 2018 to access control technologies, software, and solutions in the self-storage sector. It bolstered its platform by integrating hardware and software through backward integration. From Q4 to Q1, Noke's total installed units increased by 92%. Much of the growth can be attributed to the accelerating adoption of the Noke range of smart-entry key solutions.

Margin Stability

{kind=link}

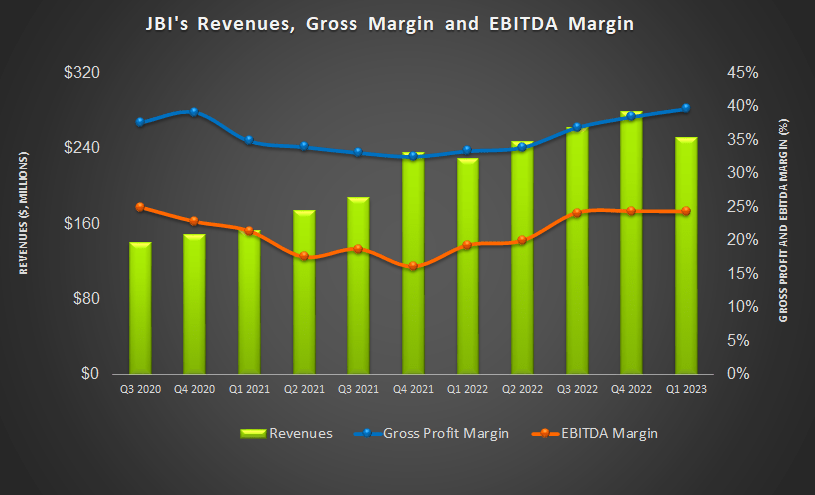

Despite 10% lower revenues in Q1 2023 over a quarter earlier, JBI's gross profit margin expanded by 120 basis points in Q1. Its adjusted EBITDA margin remained nearly unchanged at ~24% during this period. In 2022, the company undertook several commercial and cost-containment initiatives.

These actions offset the raw material, labor, and logistics cost hikes in Q1 2023. Also, its costs related to steel coil decreased due to favorable supplier agreements signed in 2022. I think the company's operating margin will remain resilient and may improve as volume rises in the medium term.

Strategies And Challenges

However, JBI also experienced an extended construction time in Q1 due to project delays in the housing sector. The company expects to gain from increased commercial sector actions and market share gains, particularly in hotels, warehouses, pharmacies, and schools. The other challenge for the company lies in higher labor costs associated with scaling up and additional investments in Nok?. So, the company plans to adjust its input costs by design, eliminating the lag in the cost recovery.

Over the long term, Janus will look to bank on growing Nok? adoption for its self-storage customers, increased efficiencies, and value-accretive M&As. In this context, investors may note that it acquired DBCI and ACT in 2021. ACT provides low-voltage security systems integrators in the self-storage and multi-family industries. DBCI manufactures and services self-storage, commercial, residential, and repair markets.

FY2023 Outlook

In my opinion, growth across existing sales channels and increased adoption of Nok? Remote Access products have helped Janus stabilize its margin. With commercial actions and volume-related organic growth, JBI estimates it can achieve 4% to 6% organic revenue growth in FY2023. Its Q1 EBITDA margin of 24.3% can expand further, helping it achieve the long-term target range of 25% to 27%. It also plans to earn an adjusted net income to free cash flow conversion range of 75% to 100% in FY2023.

Recently, it raised its adjusted EBITDA estimates for FY2023. At the midpoint, EBITDA can increase by 17% in FY2023 compared to FY2022. Over the next several years, it plans to deliver an adjusted EBITDA margin of 25% to 27%.

Q1 Performance Analysis

{kind=link}

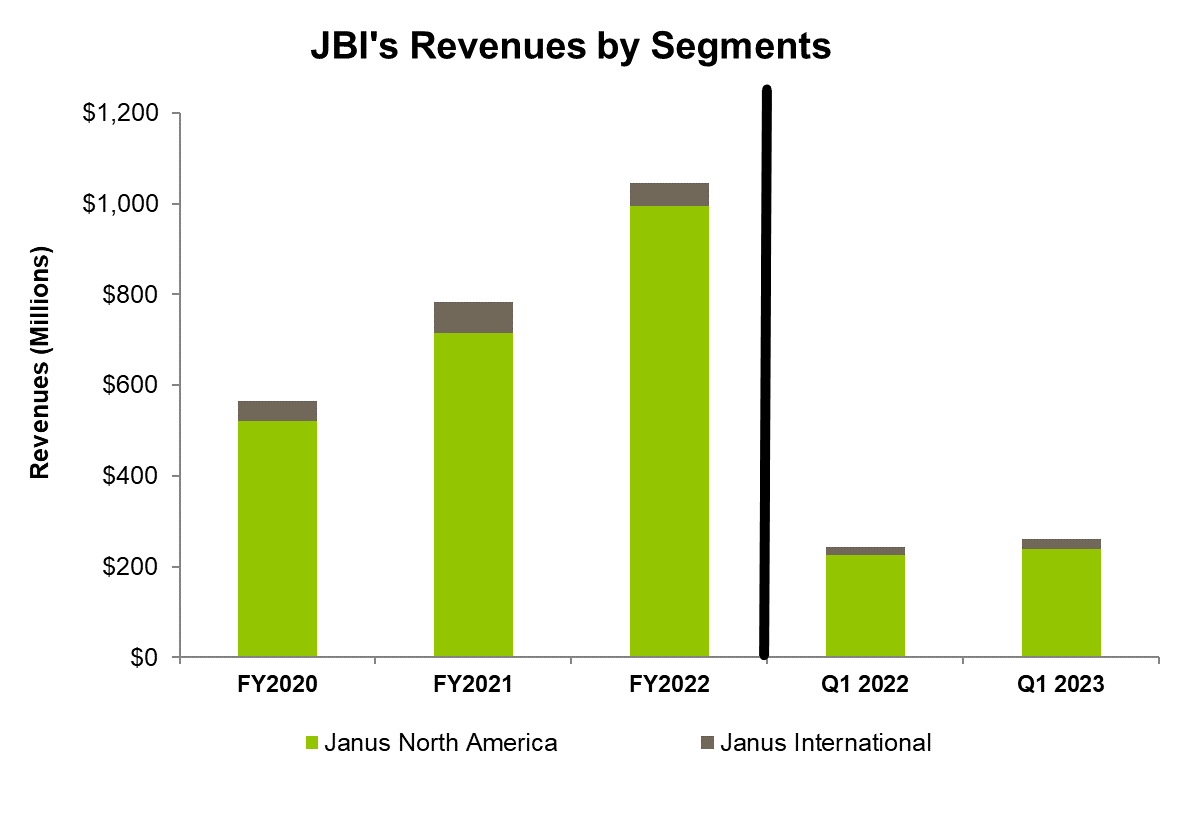

In Q1 2023, JBI's revenues increased by 10% compared to a year ago. Year-over-year, R3 was up 26.9% versus a moderate 2%-3% growth in the construction and commercial sectors. Geography-wise, JBI's North America region increased more sharply (by 20.5%) year-over-year in Q1 2023 than the International segment, which increased by 10.6% during this period. However, quarter-over-quarter revenues decreased by ~10% due to delays in the housing sector projects.

Its adjusted EBITDA increased by 37% during this period, representing an adjusted EBITDA margin growth of 480 basis points. Increased productivity initiatives and commercial actions mitigated higher costs in an inflationary environment, mainly labor and logistics.

Cash Flows And Debt

In Q1 2023, JBI's cash flow from operations (or CFO) more than doubled compared to a year ago. Although revenues increased moderately over the past year, improving working capital led to an improvement in CFO. Free cash flow (or FCF) also doubled in the past year.

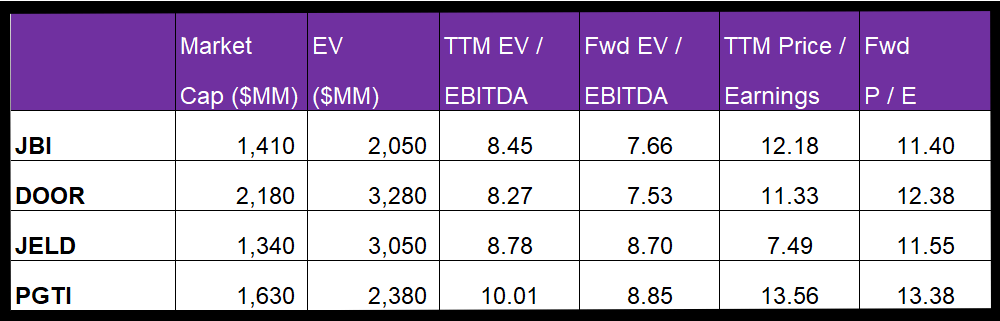

The company's debt-to-equity (1.6x) is higher than its competitors' (DOOR, JELD, and PGTI) average. During Q1, it repaid $50 million of its first-lien term loan facility. Recently, Moody's upgraded the company's credit rating following its debt reduction initiatives. It has $150 million in liquidity as of March 31.

Analyst Rating And Relative Valuation

{kind=link}

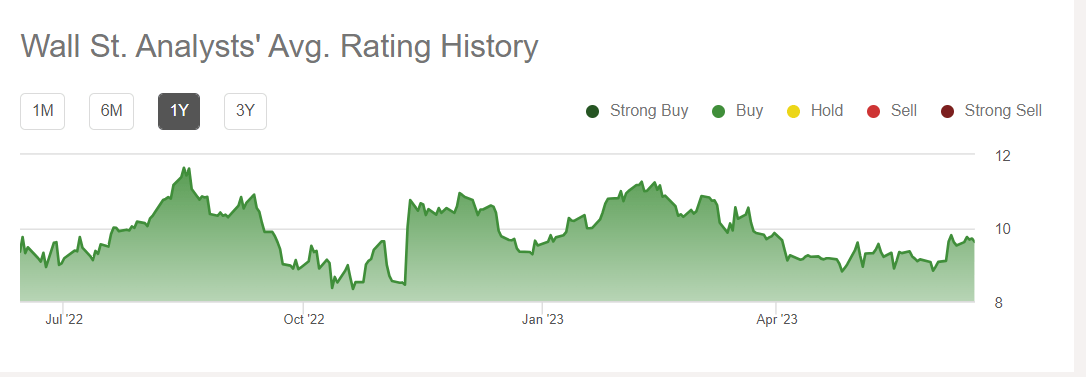

According to data provided by Seeking Alpha, four sell-side analysts rated JBI a "buy" in the past three months (including "Strong Buy"), while two rated it a "hold." None rated it a "sell." The consensus target price is $14.3, suggesting a 48% upside at the current price.

{kind=link}

JBI's forward EV/EBITDA multiple contraction versus its current EV/EBITDA is marginally steeper than its peers. This typically results in a higher EV/EBITDA versus its peers' multiple because its EBITDA is expected to rise more sharply than its peers. The company's EV/EBITDA multiple (8.5x) is lower than its peers' (DOOR, JELD, and PGTI) average (9.0x).

Its average EV/EBITDA for the past nine quarters is 13.8x, much higher than the current multiple. So, the stock appears to be undervalued versus its peers. If it trades at the average multiple that its competitors trade, I figure the stock has a 31% upside potential.

Risk Factors

{kind=link}

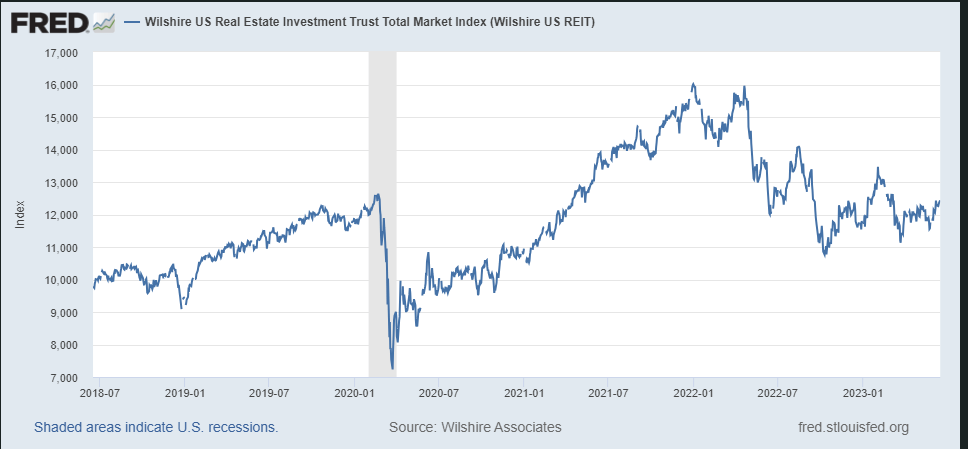

JBI's business critically depends on the housing market, REIT market growth, unemployment, and broader economic growth. While inflation and rising interest rates have been the story over the past year, the economy appears to be stabilizing in recent months. The Wilshire US REIT index increased by 6% in 2023 after falling by 26% in 2022. The new privately-owned housing units in the US are returning to the pre-pandemic level. From April 2022 until January 2023, it dipped by 25%. Since then, it has shown signs of consolidation and increased by 4.6% until April.

The US interest rate has increased from below 1% in April 2022 to more than 5% until June 2023. Higher interest rates adversely affected office occupancy. Higher debt costs are throttling commercial real estate transaction volume. As a confluence of all these factors, JBI's revenues decreased in Q1 from a quarter ago. I do not think the situation will improve soon, although some other indicators, like US unemployment, have remained low, which can mitigate the negative impact.

What's The Take On JBI?

{kind=link}

JBI considers the R3-Self-storage market the most robust growth driver in the current environment. It added significant new capacity via conversions and expansions over the past year. Its control technologies, software, and solutions in the self-storage sector have recently accelerated. On top of that, the eCommerce market proliferation has also provided opportunities in the self-storage, commercial, and industrial sectors.

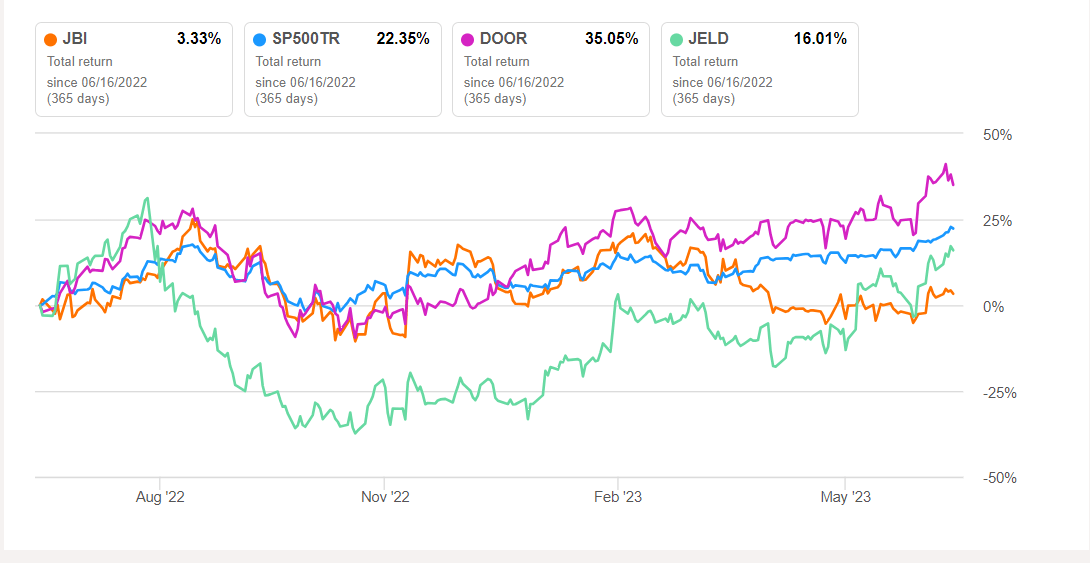

But JBI's growth decelerated due to the excess capacity in brick-and-mortar greenfield construction. So, the stock underperformed the SPDR S&P 500 ETF ( SPY ) in the past year. Despite the challenges, it appears to be on course to achieve its revenue and EBITDA margin in FY2023. It repaid some debt in Q1, followed by a credit rating upgrade. Given the low relative valuation, investors would do well to "hold" it for now in my view.

For further details see:

Janus International: Steady Margin Overshadows Top Line Moderation