JAPSY - Japan Airlines Aims For Double-Digit Profit Growth

2023-08-15 17:16:24 ET

Summary

- Japan Airlines saw a significant increase in capacity and revenue, driven by international passenger demand.

- Domestic passenger service revenues increased, but were offset by a decline in cargo business.

- Japan Airlines forecasted higher revenues for the year, with growth expected in the international operations and a higher consolidated net profit.

As part of our expanding airline coverage, I'm now adding Japan Airlines (JAPSY). Asian airlines have been one of the last airlines to see a significant improvement in the demand profile. In this report, I will analyze the most recent quarterly results and discuss the outlook for Japan Airlines.

{kind=link}

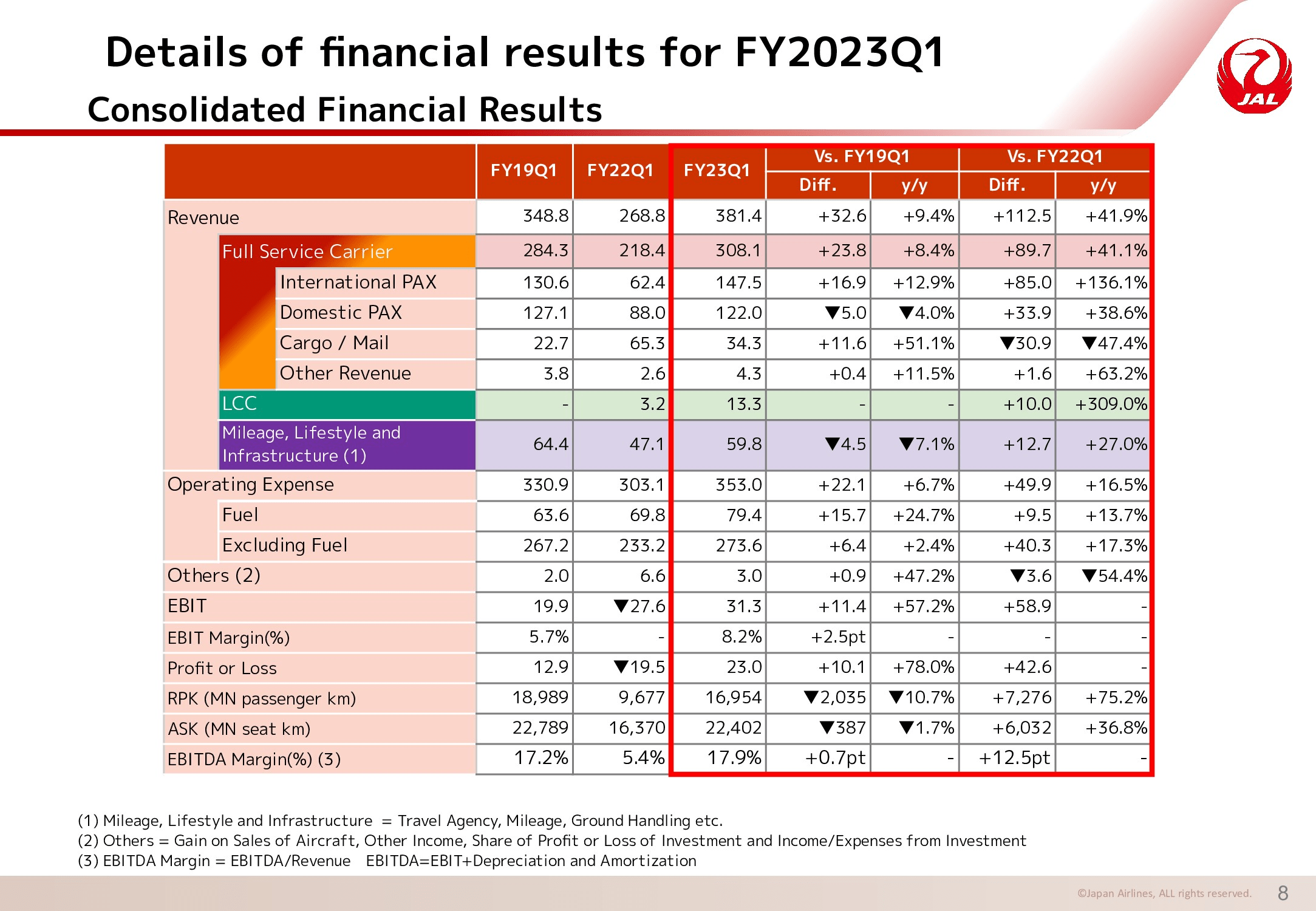

Overall, Japan Airlines increased its capacity by nearly 37% and saw its revenue increase by 42%. The changes in the LCC revenues are big, but they're not quite interesting to look at to assess a recovery trajectory as Zipair, which is part of the LCC operations of Japan Airlines, and was founded in 2020, and Spring Japan, which has a fleet of just six Boeing 737s. Spring Japan doubled capacity but its passenger revenue increased only 45% pointing at a 57% reduction in yield. Zipair increased capacity by 75% and saw revenue per passenger increase 24.1% and an increase of passenger load factors to nearly 78% for a 467.2% increase in passenger revenues.

Low-cost operations results are not really an indication of recovery but more about future growth for Japan Airlines to compete with other Asian low-cost carriers. More reflective of recovery is the full service carrier which consists of the domestic operations, international operations and the cargo operations. Domestic cargo revenues are up less than a percent on 7.4% higher capacity while international cargo revenues are down 53.7% on an 18% higher capacity. Cargo capacity is down 47.4% year-over-year, but still up 51.1% compared to pre-pandemic. Cargo revenues are, however, expected to remain under significant pressure as more capacity is added internationally which will ease the supply side of cargo operations while from demand side there's some softness due to inflation and consumer spending habits.

Just like we saw for ANA Holdings, for Japan Airlines we observed that the increase in domestic passenger service revenues was almost fully offset by a decline in the cargo business. Domestic revenues increased by 33.9 billion yen, but the cargo revenues declined by 30.9 billion yen. Overall the domestic passenger service saw revenues increase by 39% but is still down 4% compared to pre-pandemic on a 6.4% year-over-year capacity increase and 3.4% lower capacity. So, we're seeing that the domestic business is a challenging one. It's not the business where we see double-digit yield expansion. It is a segment where capacity needs to be deployed prudently.

International passenger revenues increased by 136% on a 65.7% increase in capacity. So, we're seeing the long-haul demand being filled and I would expect that to continue in Q2 but I would expect off-peak yields in the second half of the financial year.

Overall, Japan Airlines saw its EBIT increase from a 27.6 billion yen loss to a 31.3 billion yen profit and that is despite a 14.9 billion yen negative hedge results along with higher staff, maintenance and service costs.

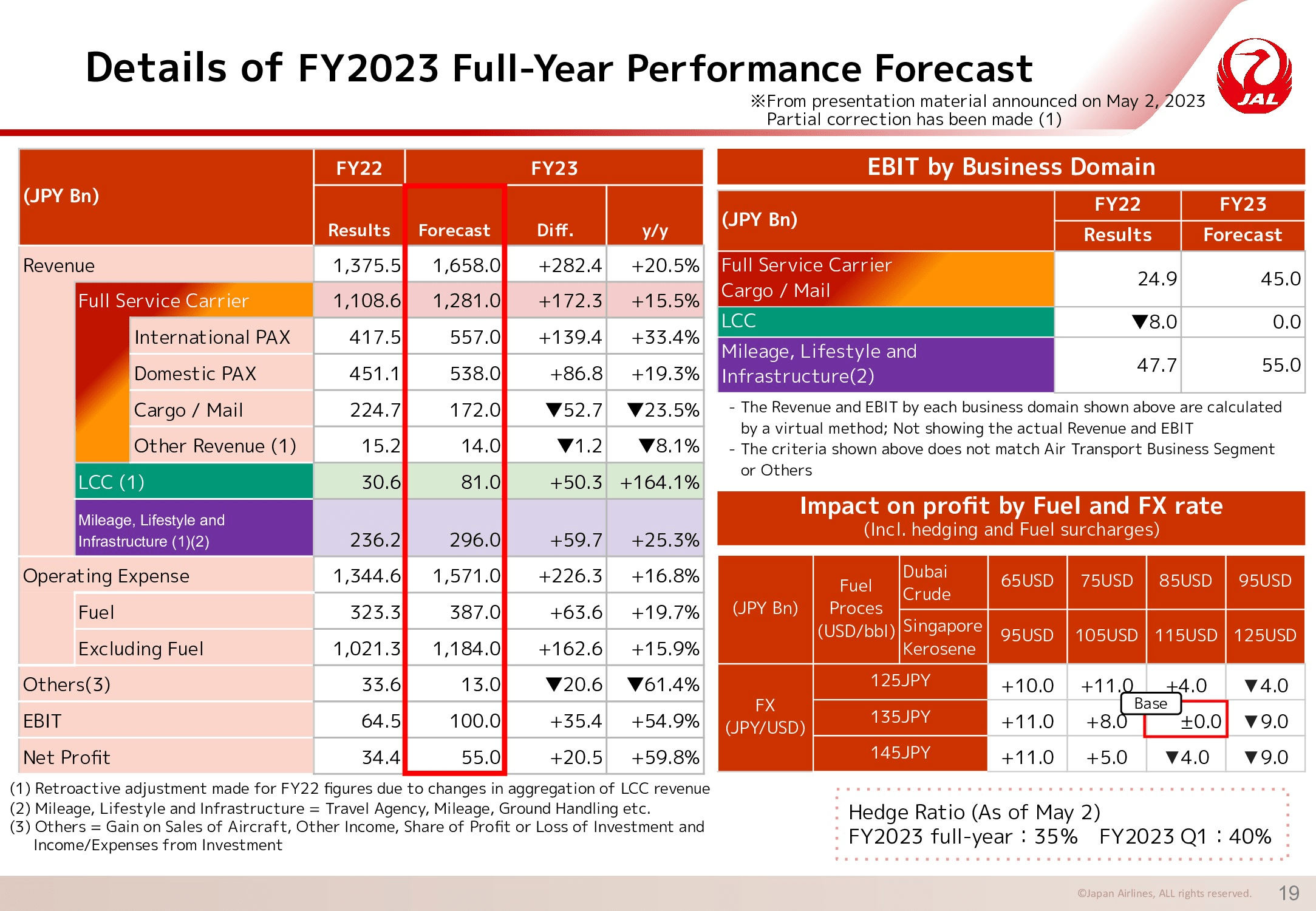

Japan Airlines Forecasts A Strong Year

{kind=link}

Japan Airlines forecasts 20.5% higher revenues this year. The low-cost segment will continue to show high growth but that will merely turn the business from loss-making to break-even while cargo revenues are expected to fall 23.5% offset by 19% growth in domestic revenues. Most of the growth will be in the international operations with revenue increasing by 139.4 billion yen or 33.4% higher revenues which should help the full-service carrier increase results by 80% and realize a 60% higher consolidated net profit.

For Q2, international demand is expected to recover to 67% of pre-pandemic levels which is above the 62% forecast earlier and for Q1 the recovery was 4 percentage points higher than expected. The domestic market will be 94% recovered in Q2 which is in line with earlier expectations.

Conclusion: Japan Airlines Is A Hold

While Japan Airlines will see a significant increase in profits in 2023, its historical EV/EBITDA of 5.3x does not weigh favorably against the 6.35x projected for 2023 against a higher EBIT than forecast by Japan Airlines. As a result, while I do like Japan Airlines better than ANA Holdings due to its cargo revenue decline not offsetting the domestic growth. I don’t see an extremely compelling buy case for the stock and any upside would really only be driven by positive momentum rather than long-term fundamentally driven upside.

For further details see:

Japan Airlines Aims For Double-Digit Profit Growth