JAPAF - Japan Tobacco Overvalued

2023-05-03 22:11:24 ET

Summary

- Ongoing RRP volume growth supported by a Ploom X device price reduction.

- The Ploom X international expansion is underway.

- On a reverse P/E estimate, Japan Tobacco's valuation looks full. BAT is yielding higher. Therefore, we confirm our neutral view.

Yesterday, Japan Tobacco ([[JAPAF]], [[JAPAY]]) released its quarterly update and today we are taking the time to deep-dive into its key figures. Last time, we positively emphasized the latest company's update, and as a reminder, we should recall the agreement with Altria for the US expansion, 2) ' the Ploom X Intake ' in the EU/UK with a rollout in more than ten markets expected for the current fiscal year, and 3) the dividend upgrade to 188 yen from 150 yen.

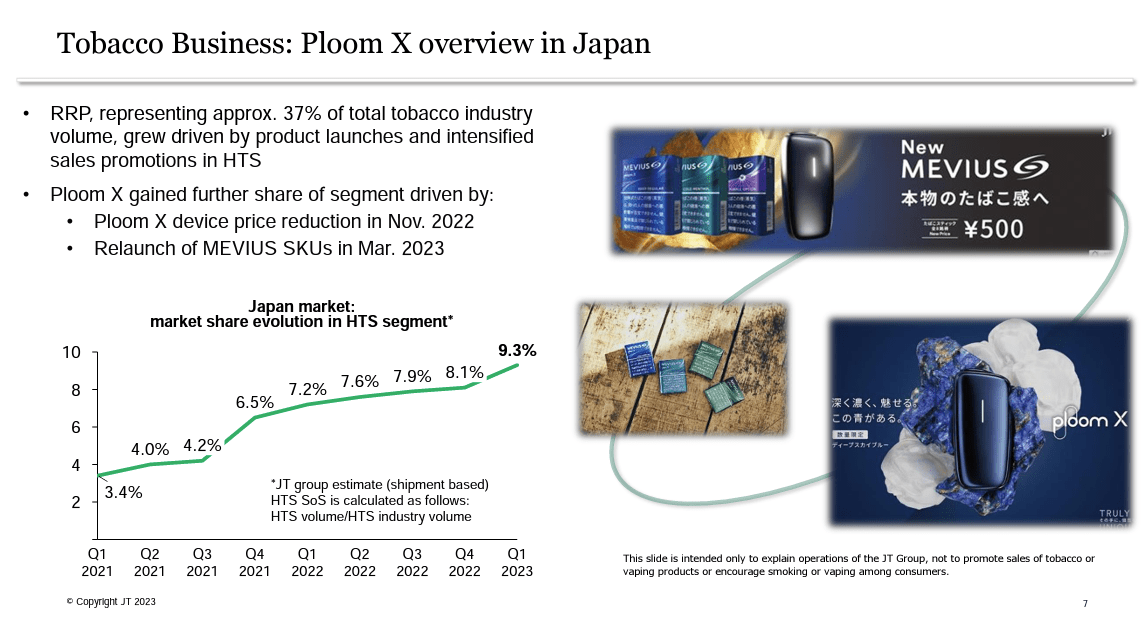

Starting with point 1), the Japanese market is notable for heated tobacco devices and RRP products represent almost 37% of the country's tobacco industry. In its home market, Japan Tobacco is slowly increasing its market share now at 9.3%. This was supported by volume growth as well as by a Ploom X device price reduction which started in November 2022. In numbers, sustained RRP volume growth and market share gains resulted in a total volume increase of approximately 1.3%. Looking at the Japanese volume, RPP grew by an additional 3.0%. Related to Altria, there were no major updates. Here at the Lab, we positively view Japan Tobacco's equity stake at 25% with Altria, but for now, we are not providing any material upside in our forecasted estimates. Many investors believed that Altria would introduce its own product or acquire an e-cig player with an approved device already present in the market. However, we believe that this JV is a winning deal for both companies. Altria will leverage a successful existing product with a partner that already has the internal know-how, while Japan Tobacco will be back to growth in a key market such as the US.

{kind=link}

Source: Japan Tobacco Q1 results presentation

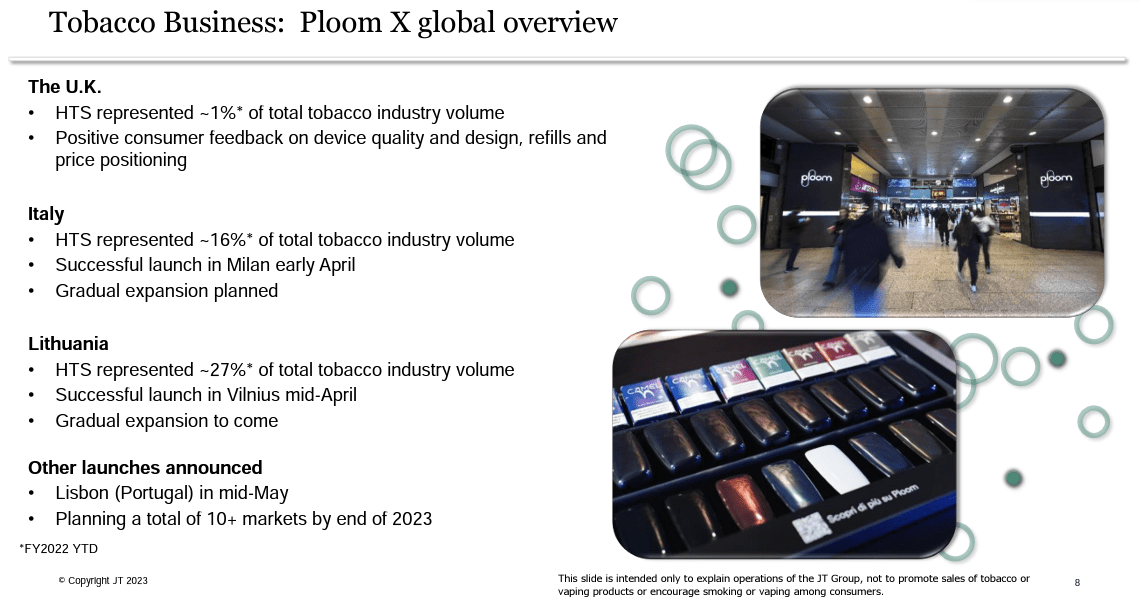

Concerning our second intake, in line with our latest estimates, Japan Tobacco is expanding in new markets to increase heated tobacco presence and establish potential future earnings growth. In April, the company successfully started to sell Ploom X in Lithuania and Italy. This was supported by a positive rollout in London and then in the UK. In May, Japan Tobacco also plans to expand its presence in Portugal. Looking at JT's press release, the CEO confirmed that they " are making good progress for additional international launches ". On JT's international presence, we should recall that the company has still valuing options to sell its Russian tobacco business entity. As reported at this moment, Japan Tobacco " is unable to reasonably estimate the outlook and the impact on its financial results ". Related to Russia, volumes are going down, but revenue and operating profit were up thanks to higher excise-tax which led to price increases. As a reminder, 20% of the company's total EBIT is coming from Russia and JY hold a leading market share in combustible cigarette (higher than 35%). In 2022, we analyzed JT's Russian exposure providing two updates called: ' Not Our Cup Of Tea ' and ' It Just Gets Worse '.

{kind=link}

Lastly, the management confirmed its dividend payment set at 188 yen per share. At today's price, the company is yielding 6.33%.

Japan Tobacco dividend per share

Q1 update and valuation

The company delivered revenue of JPY 665.3 billion which was up by 14.4%; however, adjusted for FX, this increase was only by 6.2%. Similar performance was recorded at the adjusted EBIT profit level with a ratio up by 5.1% to JPY 204.7 billion. Last time, we were incorporating higher marketing expenses to retain home market share as well as for the Ploom X international expansion. The CEO was the first one to emphasize that the FX rate needs to be carefully monitored. Despite that, we positively view these latest results, the CEO also explained how the " group delivered solid results in Q1, building on the positive momentum across its businesses. Robust pricing in the tobacco business continued to drive the strong performance of the Group ". Therefore, the company left its guidance unchanged and a forecast earning revision could be announced in Q2. At the moment, JT's stock price is already trading higher than our current estimates. Our target price was derived using an EPS of Yen 227.26 with a 10x P/E (in line with JT's historical valuation). We valued the tobacco company at Yen 2,720.00 (in ADR $10 per share). As a reminder, JT was guiding 2023 revenue and adjusted core operating profit to decrease by 1% and 6.4% respectively. On a reverse P/E basis, we believe that the current valuation looks full, and we also believe that the British American Tobacco yield discrepancy (7.6%) is currently not justified. Therefore, we reiterated our view on ' We Are Still Neutral '.

{kind=link}

For further details see:

Japan Tobacco Overvalued