JAPAF - Japan Tobacco: We Are Still Neutral

Summary

- The company delivered a good set of numbers in 2022, with a positive acceleration in Q4.

- However, the 2023 guidance disappointed our expectations with an estimated decrease both in sales and adj. operating profit.

- Dividend is set at 75% payout, with no expected catalysts, so our neutral rating valuation is left unchanged.

In our Japan Tobacco ([[JAPAY]], JAPAF ) latest publication called Ploom X Expansion Is Underway , we were more optimistic about the company's 2022 outlook. In detail, we were impressed by the latest development and we reported 1) the new collaboration agreement with Altria to expand Ploom X products in the US with a specific JV participated at 25%, 2) still related to the Reduced-Risk Products evolution, Ploom X rollout in London and 3) a dividend revision from 150 to 188 yen. As a reminder, our initiation of coverage was an analysis titled Not Our Cup Of Tea , including our negative consideration versus the company's Russian impact . Yesterday, after market hours, Japan Tobacco released its 2022 accounts, and after having carefully reviewed the release, here are our key takeaways:

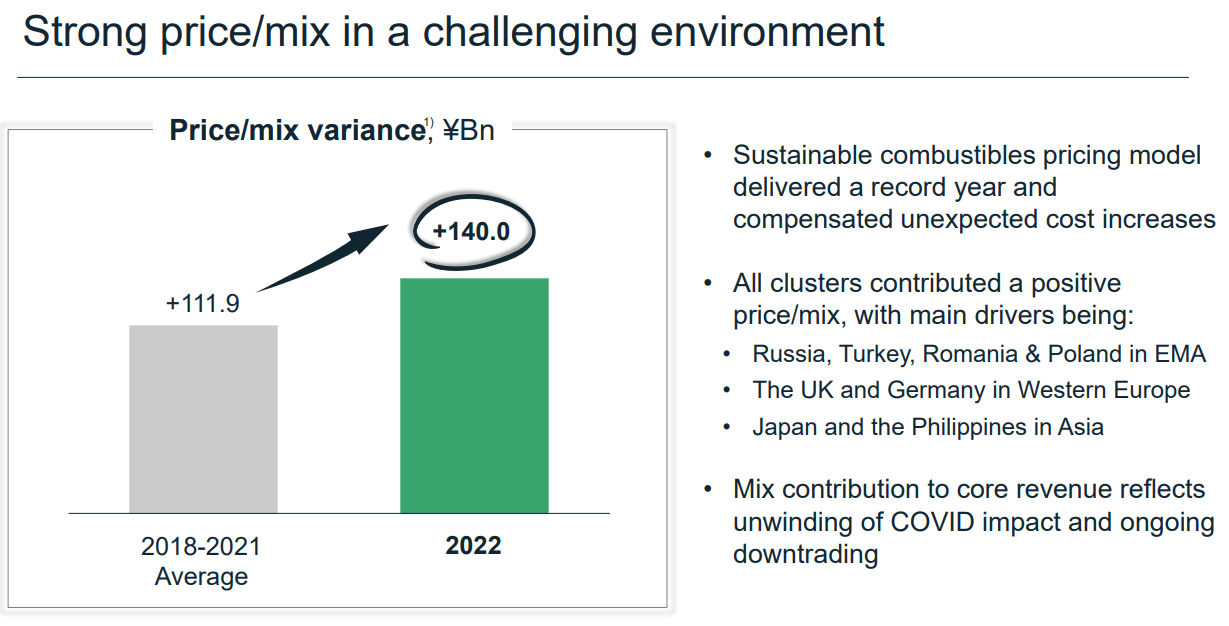

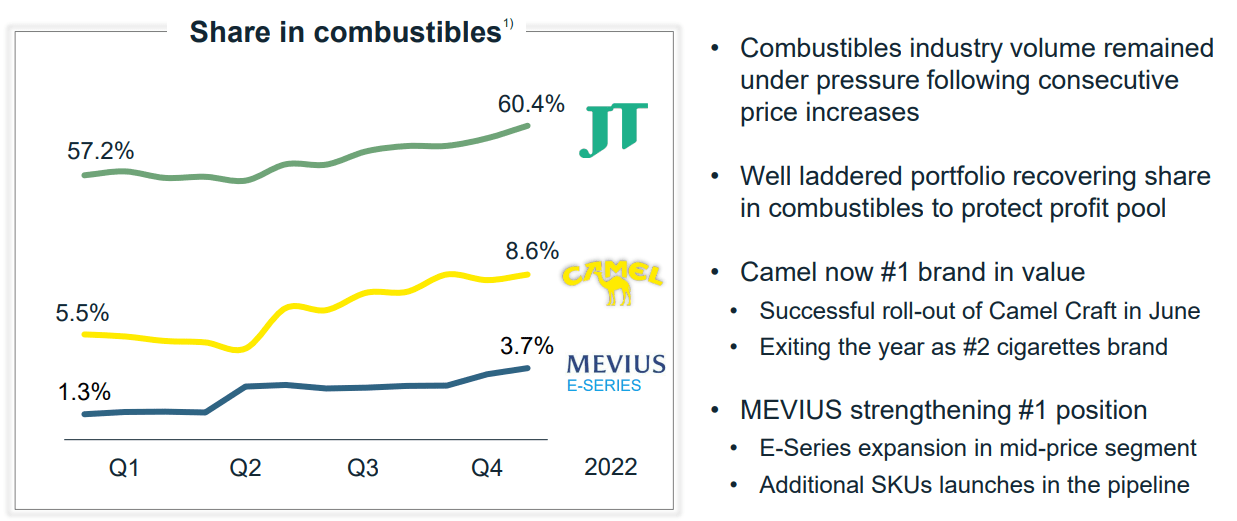

- On a yearly basis, JP's top-line sales increased by 14.3% from Yen 2,324.8 billion to Yen 2,657.8 billion. At the quarter level, we note a revenue acceleration with a plus 16.2?. As already mentioned for Nissan , there were turnover support thanks to the positive FX evolution. In detail, combustible tobacco volume was almost flat with a minus 0.7% versus the previous year's end, but the company gained market share in its key markets (Fig 1) and more importantly, recorded a solid increase in the price mix evolution (Fig 2);

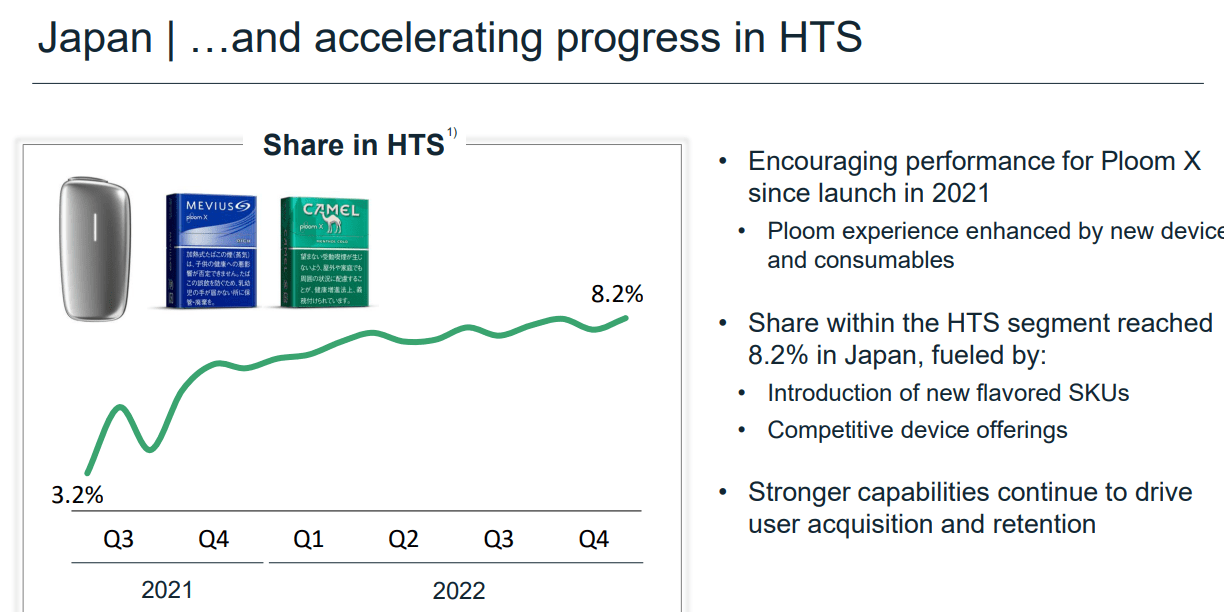

- On a negative note, the company delivered solid Ploom X growth in Japan. Looking at the release , this was " driven by a significantly improved consumer experience, sustained investments, and enhanced capabilities"; however, if we are looking at the 2021 FY results presentation, JP was guiding an RRP market share of 11.8% (Fig 3). While the company reached a Reduced-Risk Products penetration of 8.2% (well-below management guidance) (Fig 4). Regarding its main competitors, British American Tobacco (BTI) with glo finished 2022 with the same 7.5% share, while Philip Morris International (PM) thanks to IQOS and ILUMA's new launch increase its market penetration from 22.8% to 24.5%; all in all, considering the fact that this is JT home market, we negatively view this outcome;

- Going down to the company's P&L, JT adj. EBIT profit at constant currency reported an increase of 9.0% to Yen 665.7 billion. This was mainly driven by pharmaceutical and tobacco businesses and partially offset by decremental results in the processed food sector margin. Important to note is also the negative evolution of JT's FCF which decreased by Yen 99.1 billion to Yen 382.9 billion. This was due to higher working capital requirements from raw material inflationary pressure, more income tax, and more marketing cost in its home market (and we believe in the Ploom X international rollout).

{kind=link}

(Fig 1)

Combustible market share evolution

{kind=link}

(Fig 2)

Japan Reduced-Risk Products previous target

{kind=link}

(Fig 3)

Japan Reduced-Risk Products evolution

{kind=link}

(Fig 4)

Conclusion and Valuation

The dividend guidance was left unchanged at Yen 188 per share, confirming a dividend payout ratio of 75% (in line with management indication). What negatively surprised our team was the latest 2023 forecasts (Fig 5). In detail, the company expects revenue and adj. EBIT profit to decrease by 1% and 6.4% respectively. We believe this is due to higher marketing expenses both for the Japanese market to retain market share and also for the Ploom X rollout in more than 10 markets for 2023 (Fig 6). There are no positive catalysts to price in for the forecast period, and while we believe that JT's current yield is safe at 7.12%, we reiterate our neutral valuation based on a 10x P/E estimate with an EPS of Yen 227.26. Our 12-month target price is Yen 2,720.00 and $10 per share on the ADR.

For further details see:

Japan Tobacco: We Are Still Neutral