STT - Japanification Of The U.S. Banking System And Zombie Banks

2023-04-16 09:30:00 ET

Summary

- The Fed saves the system, but there are side-effects.

- The Japanification of parts of the U.S. banking industry and the creation of zombie banks.

- I prefer the large U.S. banks.

- There will be asymmetric risk-reward opportunities in the regional and mid-size banking space.

- However, investors must do their homework in a very granular manner.

The recent banking turmoil has profoundly impacted the U.S. banking industry. There will be winners and losers, which is also likely to accelerate further consolidation in the banking industry. The U.S. has far too many banks currently but the consolidation trend has been clear for many years.

{kind=link}

Confluence Of Factors Pressuring Banks

The catalyst for the recent banking turmoil is the rapidly rising interest rates in 2022. This has the following key implications:

- The U.S. banks have $620 billion of unrealized losses on their books as of 31/12/2022 which for some banks presents an outsized percentage of their tangible equity (some over 100% of their equity). In other words, these banks are effectively insolvent.

- Deposits costs have gone up materially as customers are increasingly switching to money market funds and other investments.

- Deposits flight are most pronounced from banks perceived to be weak and/or with a high percentage of FDIC uninsured deposits.

- Commercial Real Estate ("CRE") credit risks already exasperated by high-interest rates, are further pressured by tightened lending conditions.

- The high-profile collapse of Silicon Valley Bank (SIVB) and Signature Bank ( SBNY ) have dented confidence in the banking industry.

- Flight to quality of deposits to the large U.S. banks who are seen as too-big-to-fail ("TBTF").

- The upcoming regulatory agenda is expected to focus on the regional and mid-size banks. Regulators have a tendency to "fight the last war".

The Thesis: What Does It All Mean For Investors?

The regional and smaller banks are likely to be under pressure on multiple fronts for a prolonged period, including:

- High cost of deposits.

- Losses on long-duration investment securities.

- Vicious and self-reinforcing cycle from a need to preserve capital and liquidity, tightening of lending standards, exposure to high-risk areas in a recession (especially CRE), and higher cost structure.

- Regulatory scrutiny and additional regulatory costs.

- Loss of investors' confidence.

In short, that vicious and self-perpetuating cycle is likely to give rise to the Japanification of parts of the U.S. banking industry and the birth of a large number of zombie banks. This does not bode well for the U.S. economy either as these banks are very important sources of credit.

The dichotomy in returns (year-to-date) between some of the TBTF banks such as Citigroup ( C ), Morgan Stanley ( MS ), JPMorgan ( JPM ), Bank of America ( BAC ), Wells Fargo ( WFC ) and Goldman Sachs ( GS ) and the regional banks ETF (Invesco KBW Regional Banking ETF ( KBWR )) is already telling the story.

The usual valuation metrics of price to tangible book and/or PE ratios for the regional banks should be taken with a large grain of salt in the current environment.

The Opportunities

Every crisis also presents opportunities and there will be winners and losers.

The large U.S. banks such as JPMorgan and Citigroup are direct beneficiaries of the flight to quality and a much more diversified business model. JPM delivered stellar earnings in Q1'2023 printing 23% RoTCE even as he continued to build up provisions. Citi is my conviction buy as a turnaround story that is gaining strength from quarter to quarter. Its crown jewel Treasury and Trade Solutions ("TTS") is on track to deliver close to ~$15 billion of revenue in 2023 coupled with a return on equity in the 30%s.

There will also likely be opportunities in the regional and community banks going forward. Delivering alpha, however, requires detailed analysis (balance sheet, capital, deposits trajectory, credit risks, the impact of unrealized losses, and identifying acquisition targets, etc.). This is a stock picker market in the banking industry currently, and buying ETFs is unlikely to work in this environment.

Cannot Regulate Out Incompetence

The current banking turmoil was triggered from idiosyncratic risk issues in several banks. It was essentially all about the mismanagement of asset and liability matching which is banking 101 really. There is ongoing debate whether the 2018 relaxation of regulatory rules for the smaller banks (<$250 billion) have contributed to the debacle. Although, there is very little doubt that this is a colossal failure of risk management (by some banks) as well as the famous failure of regulatory oversight. As the old adage goes, one cannot regulate out incompetence.

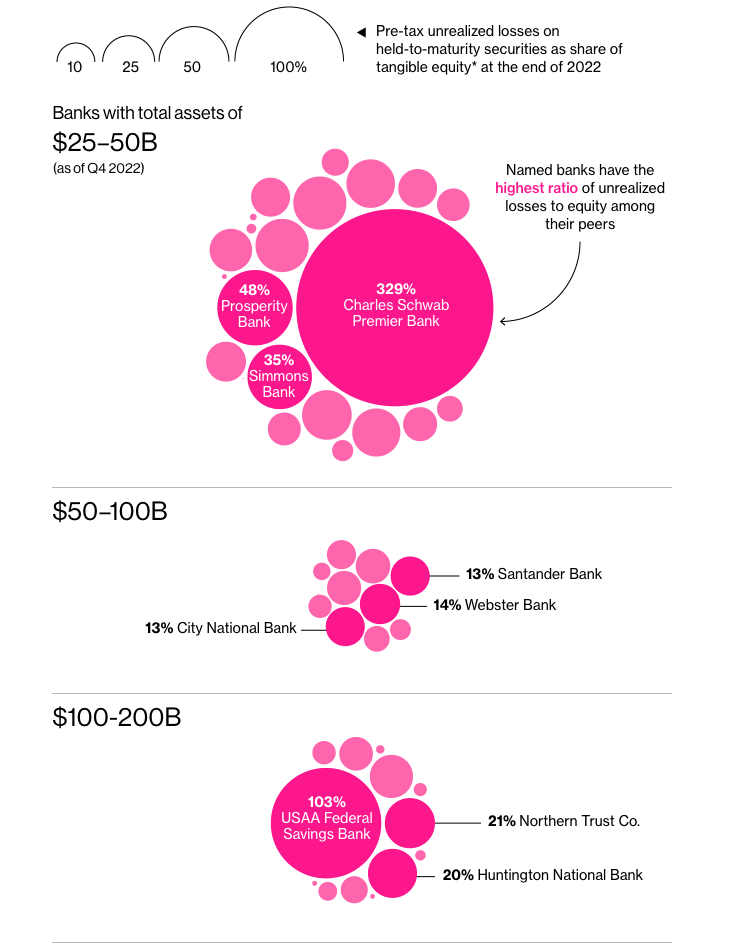

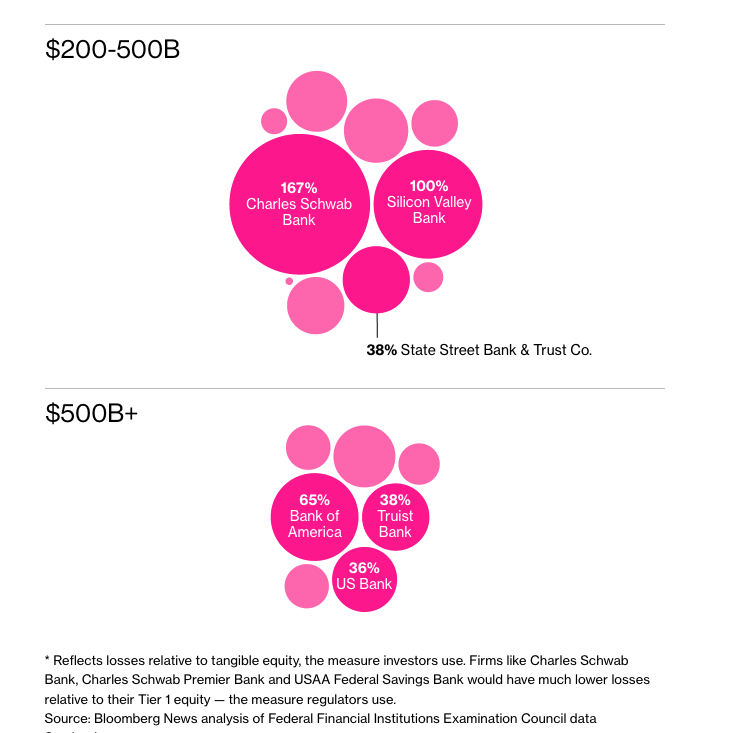

The culprit was of course the recency bias in respect of the lower for longer interest rates since the Global Financial Crisis. Many banks reached out for yield on long-duration "safe" assets such as the U.S. treasuries. With the rapidly rising rates in 2022, the unrealized losses accumulated quickly to an alarming level. The below Bloomberg chart shows the unrealized losses on Held-To-Maturity ("HTM") securities as a percentage of tangible equity for impacted banks (categorized by size):

{kind=link}

{kind=link}

US Bank ( USB ), Truist Bank ( TFC ), State Street Bank & Trust Co ( STT ), First Republic Bank ( FRB ), Charles Schwab Bank ( SCHW ), USAA Federal Savings Bank ( USISX ) , Charles Schwab Premier Bank ( CSB ), Prosperity Bank ( PB ) and Simmons Bank ( SFNC ) appear to be particularly impacted.

An important point to note is that the above only reflects HTM securities and is only part of the story. There are also Available For Sale ("AFS") securities with current material unrealized losses. However, unlike HTM, these are mark-to-market on the balance sheet but are not reflected in the profit and loss statement, but rather in the Accumulated Other Comprehensive Income ("AOCI") on the equity side of the balance sheet. Importantly, however, the capital ratios of banks (except for the largest U.S. banks) exclude the impact of AOCI for regulatory purposes. As such, the capital ratios of some banks are overstated in my view.

Commercial Real Estate Credit Risks

The pressures on the regional and mid-size banks are not just limited to the liability side (i.e., deposits cost and flight). The CRE market is also facing significant challenges due to multiple factors including the end of cheap money era, refinancing at much higher interest rates, tightened lending conditions and the working-from-home phenomenon.

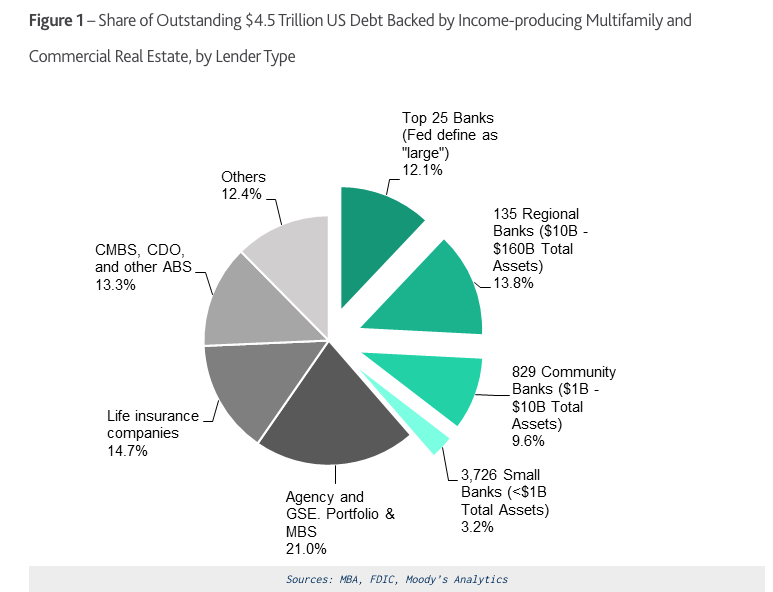

The banks, especially the small, midsize and regional, are an important source of funding for the CRE market. The following chart from Moody's provides a breakdown of current funding to the CRE market:

{kind=link}

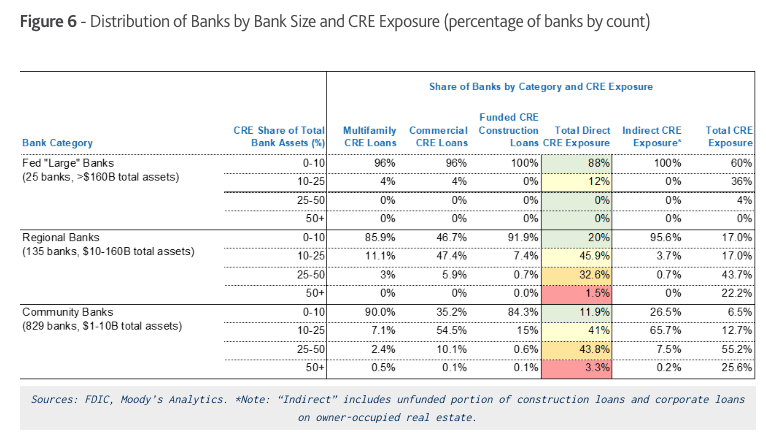

However, it is also important to consider specific banks' exposures to CRE of total assets:

{kind=link}

As you can see from the chart, over 34% of Regional banks and 47% of community banks, have a direct CRE exposure greater than 25% of their total assets. These banks are clearly vulnerable on the asset side as well.

Mr. Market is hugely concerned about the vicious cycle between falling asset values, tightened lending standards, deposits flight, higher cost of debt and large exposure to this asset class.

Paper Losses or Zombie Banks?

Some punters argue that the unrealized losses are just paper losses as long as there isn't a bank run. I argue that this, by and large, misses the point completely. Those banks with large unrealized loss on long-duration securities yielding ~1.5% are funding these, for many years to come, with deposits at a cost of 4% to 4.5%.

The Fed's new Bank Term Funding Program ("BTFP") facility is merely a stopgap measure to thwart systemic risks and bank runs and expires after one-year term. This buys banks some time to address any liquidity and/or capital holes.

Combined with pressures on assets side (CRE exposures), high cost of funds and expected regulatory costs - the focus for some banks would be on survival rather than shareholders' returns. I have very little doubt that lending conditions have tightened already which will exacerbate that vicious cycle of both asset and liability headwinds especially if a recession ensues.

Final Thoughts

The Fed has "saved" the system but the side effects include a Japanification of parts of the U.S. banking industry and creation of zombie banks. In time, weak banks will fail or otherwise be acquired. The valuation may seem cheap currently but I advise investors to proceed with caution and do their homework to a very granular level. I am planning to write a number of long and short articles on regional and mid-size banks, so if of interest, do "follow me".

At this juncture, I favor the large TBTF U.S. banks and especially Citigroup and JPM. The valuations are attractive. For example, Citi is trading at only 0.6x tangible book value and is directly benefiting from the collapse of Credit Suisse as well as the recent banking turmoil.

There will also be asymmetric risk/reward opportunities in the regional and mid-size banks and I fully intend to take advantage of these.

For further details see:

Japanification Of The U.S. Banking System And Zombie Banks