JARLF - Jardine Matheson: A Cheap Way To Play Asian Growth

2023-10-19 16:34:47 ET

Summary

- Asia-focused conglomerate Jardine Matheson has seen earnings recover past pre-COVID marks, albeit in a somewhat lumpy fashion.

- Despite that, the share price has done nothing but languish recently, leaving the stock on a depressed multiple of earnings and NAV.

- Expectations are much too low here given its earnings growth profile.

Old-fashioned conglomerates may have fallen out of favor in some developed markets, but Asia still has its fair share of them. One of the better-known ones is Jardine Matheson ( JMHLY )( JARLF )("Jardines"), which has a current market capitalization of around $12 billion.

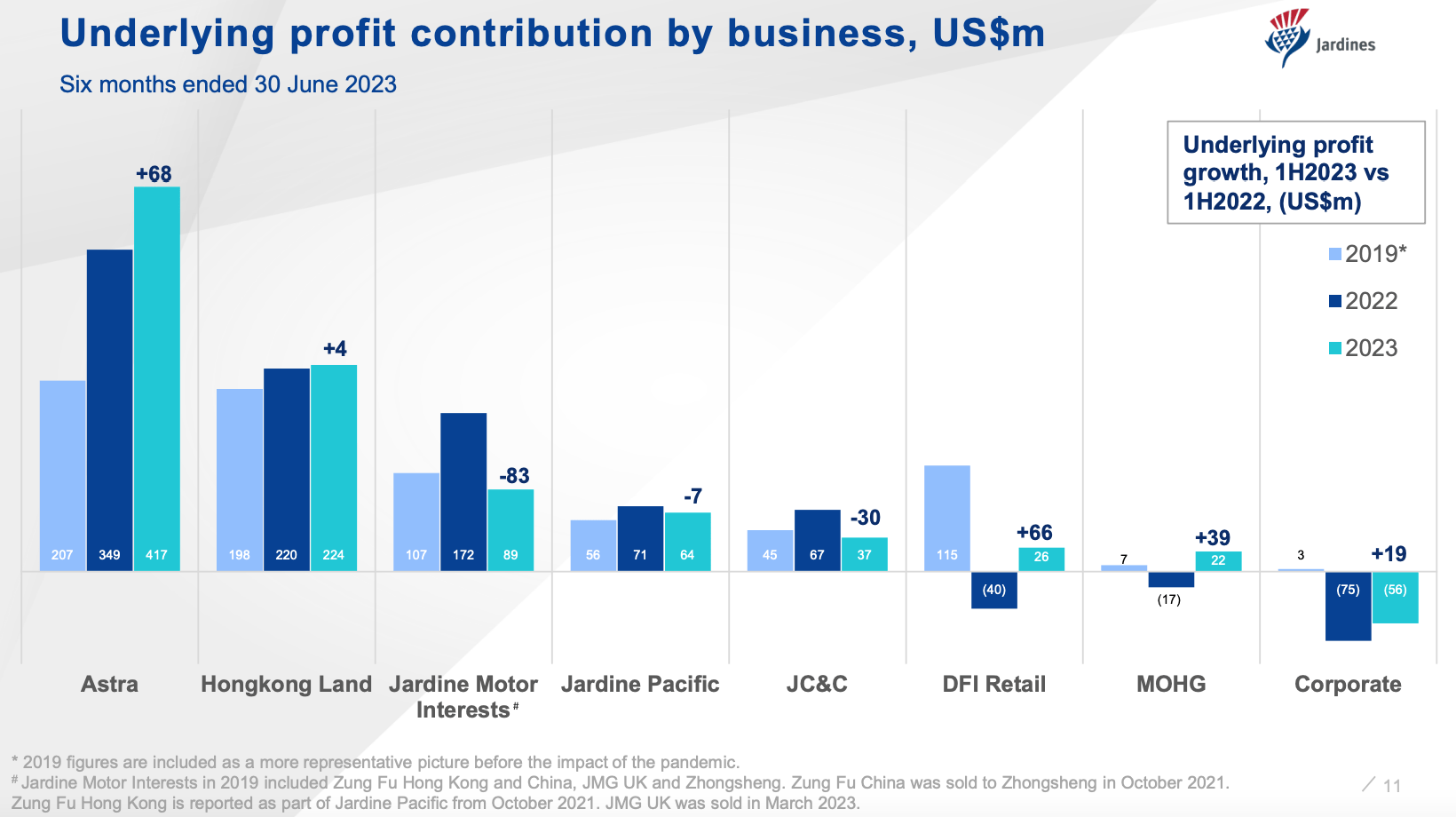

Jardines has its fingers in a lot of pies. By contribution to 1H 2023 operating profit, its main segments are Astra (~50%) and Hongkong Land (27%)("HKL")(Fig 1). Astra is itself an incredibly diverse group of operations: car and motorbike sales, consumer finance, heavy equipment and mining are some of its main lines. It is essentially a conglomerate within a conglomerate. I have covered HKL before – it is a real estate developer and landlord: most of its income comes from rental properties, and it owns some of the highest quality real estate in Hong Kong and Singapore. Jardines owns the majority of HKL.

{kind=link}

Source: Jardine Matheson 1H 2023 Results Presentation

Elsewhere, the company also controls the 5-star Mandarin Oriental hotel chain (~3% of H1 underlying profit) as well as DFI Retail Group (~3%). DFI operates numerous retail brands across Asia, including drug stores (e.g. Mannings, Guardian), grocery stores (e.g. Wellcome) and restaurants (e.g. Maxim's).

Profit Has Recovered...

The above might make Jardines appear very complex. In a sense that is true, but mainly because it is very diverse. In other ways, it is actually quite a focused business. For example, geographically it offers focused exposure to South East Asia and Greater China. The combination of these points makes it an interesting way to play regional economic growth.

{kind=link}

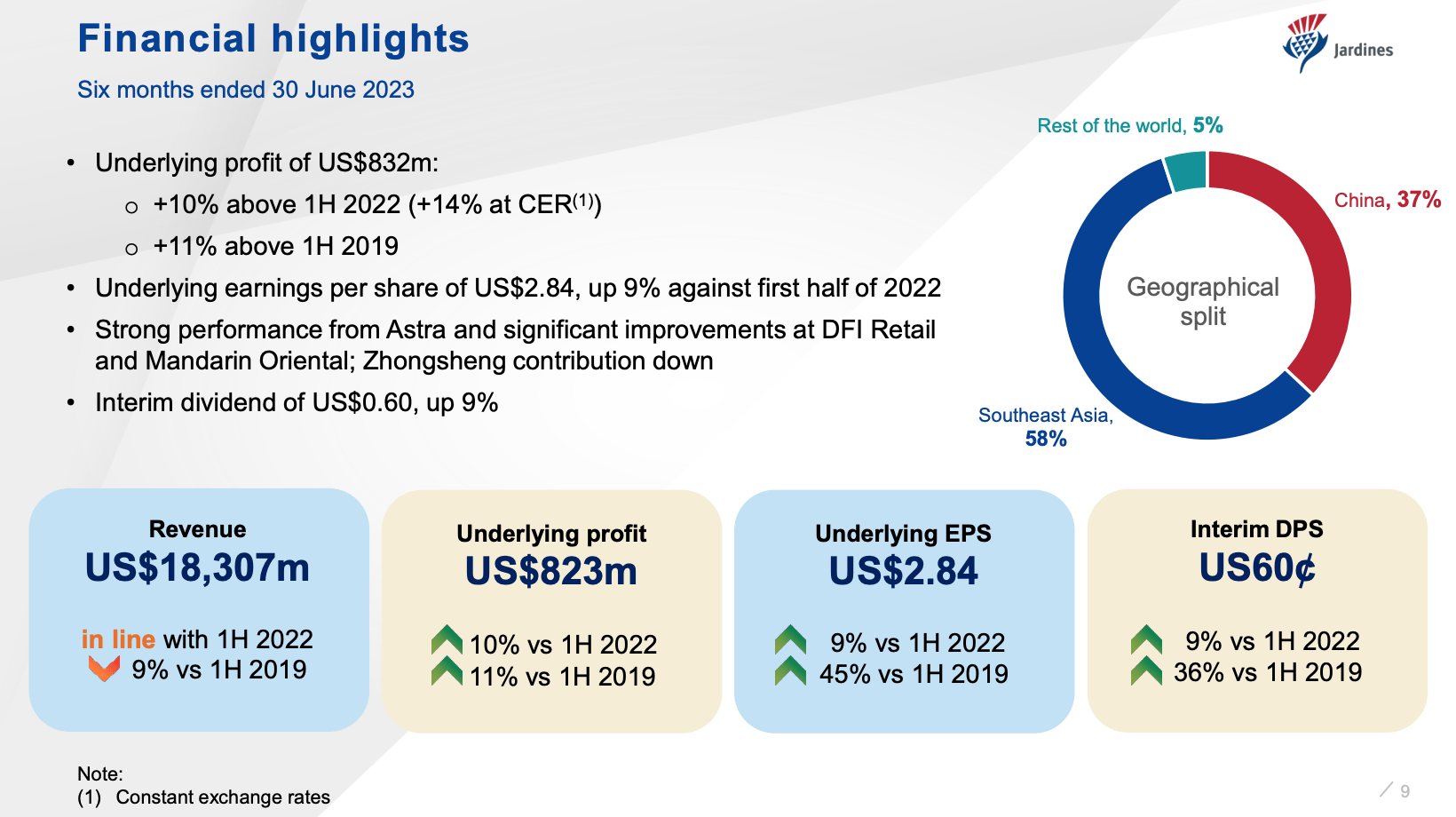

Fig 2. (Source: Jardine Matheson 1H 2023 Results Presentation)

Jardines' business is humming along nicely. The company was hit fairly hard by COVID, but earnings have recently recovered beyond immediate pre-pandemic levels. The company posted underlying net profit of $823 million in H1, which was around 12% higher than it earned over the same period in 2019 (~$738m)(Fig 2). Incidentally, this is another good example of Jardines' business diversity benefitting shareholders, because some segments are still significantly underperforming their pre-COVID marks. At DFI, for example, H1 2023 underlying profit of $26 million was still around 75% below the same-period 2019 figure. Growth in Astra and HKL was more than enough to offset this, and management expects growth to continue for the rest of the year too.

...Yet The Share Price Has Fallen

Albeit in a somewhat lumpy fashion, Jardines has now seen earnings growth rise above 2019 levels. Furthermore, because the company has engaged in a significant amount of share repurchases in the interim period, growth on a per-share basis is even better than implied above. 1H 2023 underlying profit per share ($2.84) was a little under 45% higher than over the same period in 2019 ($1.96 per share). I would also add that Jardines has maintained its dividend, which has increased by around 35% since 2019. It hasn't cut its dividend in many years.

Despite that, the share price here has done nothing but fall recently, with the ADSs currently down around 40% from their 2019 highs:

Those dynamics – sharply higher earnings; sharply lower share price – imply a very deep cut to the stock's P/E ratio. Sure enough, investors buying the 2019 high were paying around 23x underlying EPS. Today, investors only need to pay 7.5x underlying FY 2022 EPS to own the stock. Earnings are still growing, too. If Jardines makes around $5.80 in FY 2023 EPS, the P/E is more like 7x.

Risks And Valuation

So, what could explain such a sharp valuation de-rate? Firstly, I don't deny that Jardines faces some risks and uncertainty. HKL, for example, generates around 30% of its earnings from property development, which is not a great business to be in right now in China. Furthermore, although its rental properties are extremely high quality, the overall market is fundamentally weak in Hong Kong. Office vacancies are high, release spreads are negative, and that puts downward pressure on operating profit.

More generally, I would also be concerned about an economic slowdown, but that is really a generic point you could make about any non-defensive stock/sector. Besides, many of the company's markets are doing okay. Indonesia's economy, for instance, to which Jardines has a fair amount of exposure, is growing at a healthy clip. Moreover, it's not like you're paying a high multiple to own said risk. If earnings fall by half on a 20x P/E, you end up at 40x. If they do so from 7x, you only end up at 14x. The stock price is already baking a lot of downside in.

What about the balance sheet? Net borrowings amount to around $6.5 billion (excluding financial services), while annual retained earnings are currently in the $1 billion region. Debt is not a massive concern here.

Given all that, my main explanation is that Jardines is simply a victim of being overlooked. Global investment cash has been chasing US big tech stocks, and that has left pockets of global equities facing contracting valuation multiples. Jardines and many of its peers are in that group.

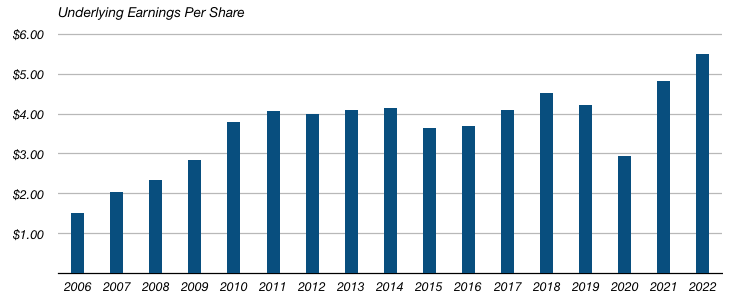

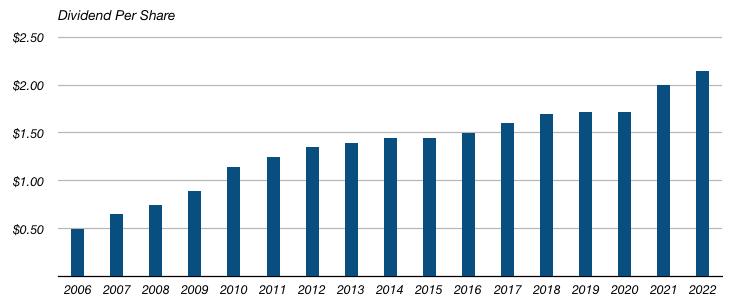

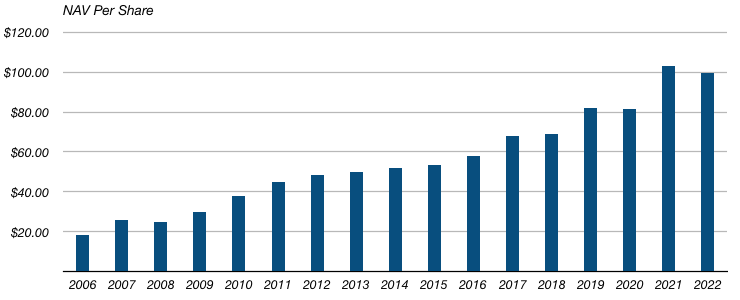

As frustrating as that may be for current shareholders, it is good for buyers. I mean, here is what the company has done over the past fifteen years in terms of growing EPS (Fig 3), DPS (Fig 4) and net asset value per share ("NAV")(Fig 5). They have variously grown at an 8-11% CAGR depending on the metric.

{kind=link}

Fig 3. (Source: Jardine Matheson Annual Reports)

{kind=link}

Fig 4. (Source: Jardine Matheson Annual Reports)

{kind=link}

Fig 5. (Source: Jardine Matheson Annual Reports)

{kind=link}

Fig 6. (Source: Yahoo Finance)

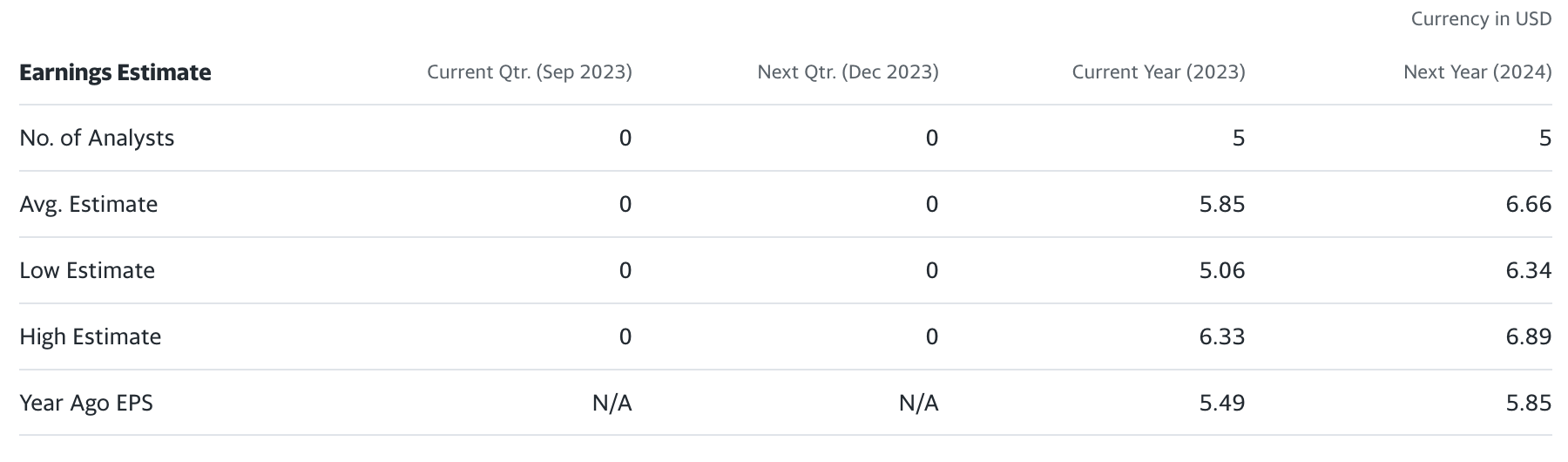

Currently, the stock trades on a prior-year P/E of around 7.5x, a prior-year dividend yield of 5.4% and for around 0.4x NAV per share. Growth could collapse to zero and these shares could still deliver 10% annualized returns without multiple expansion. Earnings would have to go into structural decline for the current share price to make any long-term sense. With analysts predicting strong growth in the near-term (Fig 6), risk/reward appears to be skewing heavily to the latter. I rate Jardine Matheson stock a Strong Buy.

For further details see:

Jardine Matheson: A Cheap Way To Play Asian Growth