JAZZ - Jazz Pharmaceuticals: Depressed Valuation Opens Up Potential

2023-07-25 04:47:39 ET

Summary

- Jazz Pharmaceuticals' current valuation is significantly lower than the sector average, despite strong margins and a positive growth outlook, presenting a potential investment opportunity.

- The company is making progress in its clinical trials and is diversifying its product offerings to mitigate the impact of generic drugs entering the market.

- Despite some challenges, such as a lengthy regulatory approval process for a new product, Jazz Pharmaceuticals is well-positioned to achieve its target of $5 billion in revenues by 2025.

Investment Outline

When you are looking at Jazz Pharmaceuticals ( JAZZ ) one has to wonder what has made the current valuation so depressed in comparison to the rest of the state. The p/e is nearly a third of the sector but JAZZ still has fantastic margins with a 38% FCF margin for example. There seems to be an indifference between what JAZZ is and what the market thinks of it. This opens up a great opportunity for us to invest accordingly and get into a solid company at a great price.

JAZZ operates in the pharmaceutical industry and focuses on developing and commercializing pharmaceutical products for unmet medical needs with an international market to serve. Founded back in 2003 the market cap has grown significantly and now sits at $8.4 billion. The last report perhaps showed JAZZ missing expectations, but the expectations were set very high and revenues still grew 9.7% YoY, driven by net sales increases in many of the key products JAZZ has. I find myself bullish about the outlook for the company and will be rating JAZZ a buy now actually.

Recent Developments

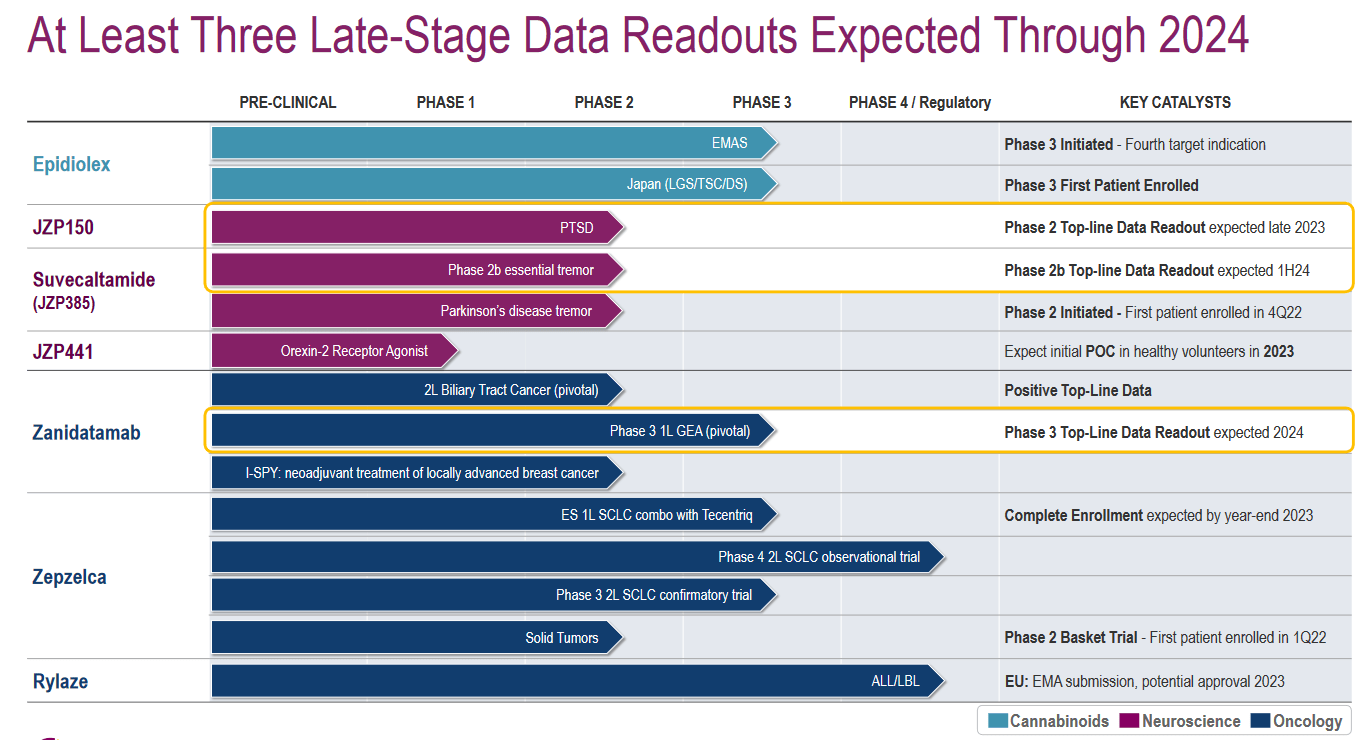

In recent news, JAZZ had some positive progress in a recent trial. On June 2 , 2023, JAZZ announced that together with Zymeworks ( ZYME ) they have had some positive progress on their pivotal phase 2b trial data regarding the bispecific antibody zanidatamab in previously treated HER2-amplified biliary tract cancer, or ((BTC)).

Results (Earnings Presentation)

{kind=link}

This partnership and cooperation mark the strong capabilities that JAZZ has to grow efficiently thanks to peers in the same industry. Trials are often what many investors are looking at to get an idea of the future potential. But seeing as JAZZ has established a solid base of offerings already, the share price is likely not going to be that volatile regarding the results of trials like these.

Product Launch (Earnings Presentation)

{kind=link}

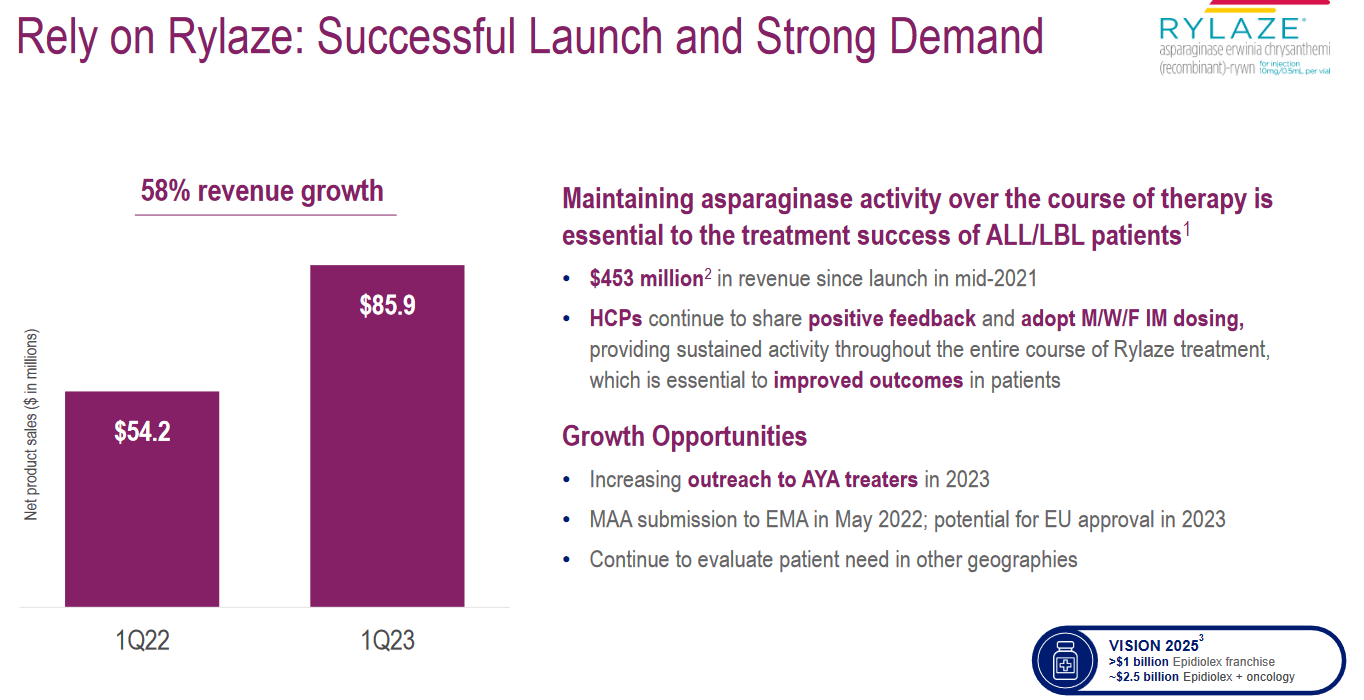

We are also not that far off from the last earnings report from JAZZ, on May 10 they announced their Q1 results. The company continues to see strong growth in many of its vital radical offerings. The revenue growth for Rylaze for example was 58% YoY, resulting in $85 million for Q1 2023. Since its launch in mid-2021, the product has netted JAZZ nearly half a billion in revenues. This is showcasing very well how JAZZ is capable of finding solid opportunities and jumping at the quickly to deliver solid results. The Q1 report reiterated the target of $5 billion in annual revenues by 2025 for JAZZ. With JAZZ having a historical net margin of 10% that would mean an EPS of $7.94 based on $500 million of net incomes and 62.9 million shares outstanding. If we apply the sector standard earnings multiple we land at a target price of $158.

Net Margin (Macrotrends)

Historically though the net margin has been far higher than 10%, somewhat above 20% instead. That leaves us with a target price closer to $300, leaving a significant upside potential from here. Looking at the estimates the EPS for 2023 is predicted to come in at $17.5. Perhaps the recent report though missing high expectations has led to the suppressed valuation, if Q2 surprises I expect to see the share price improve exceptionally from here on out.

Q2 Expectations

We are not far off from its next Q2 report for 2023. As far as the street expectations for it an EPS of $4.43 and revenues landing at $942 million. As for what I have seen in the markets I think a solid upbeat in the top and bottom line seems reasonable. JAZZ has continued to see solid demand and this I think will be reflected in the next report.

Even though the report is soon to come I think rating it a buy is a great way to benefit from the likely beat on earnings. That would mostly likely send the stock price up and we could miss out on some short-term gains. I will be keeping an eye on the management comments on the market situation, but I think given the interest rates are slowing we are entering a market that is still growing but looking ahead where rates are lower and capital spending higher. That sort of scenario is putting JAZZ in a great place to grow rapidly. I think the market that JAZZ seems to have been doing very well so far as demand remains, and that could result in a raised guidance for 2023. A surprise to the market that could send the share price higher. These are the factors I am confident in rating JAZZ ahead of earnings.

Margins

Margin Profile (Seeking Alpha)

The margin profile for JAZZ is very good in my opinion. It might be worrying that the net margin is negative, but it seems shortlived as we are recovering as the picture above here showed. The last 5 years have meant a 10% average net margin, but before that, it was closer to 20%. The rise of inflation in the last 12 months and higher interest rates seem to dig into earnings for JAZZ right now. Interest expenses are at nearly $300 million which of course hurts the already struggling operating income of $1 billion TTM. The debt that JAZZ took on in 2021 seems to have significantly increased this and continued high interested expenses should be expected going into the next 4 quarters at least. Beyond that though I expect margins to significantly recover and the share price will follow. This suggests that right now is a great time to start a position in the company before it takes off.

Risks

In response to the anticipated decline in revenue resulting from the entry of generic drugs into the market, the company is actively exploring opportunities to diversify its product offerings beyond Oxybate. This strategic move aims to mitigate the potential impact of the revenue decline and safeguard the company's overall revenue stream. The successful expansion into new product lines could play a crucial role in sustaining the company's financial health and long-term growth prospects.

However, it is important to note that any delays or challenges in effectively diversifying the product portfolio may heighten the risk posed by the revenue decline. As such, careful and well-executed planning will be crucial to navigate this transitional phase successfully.

2023 Guidance (Earnings Presentation)

{kind=link}

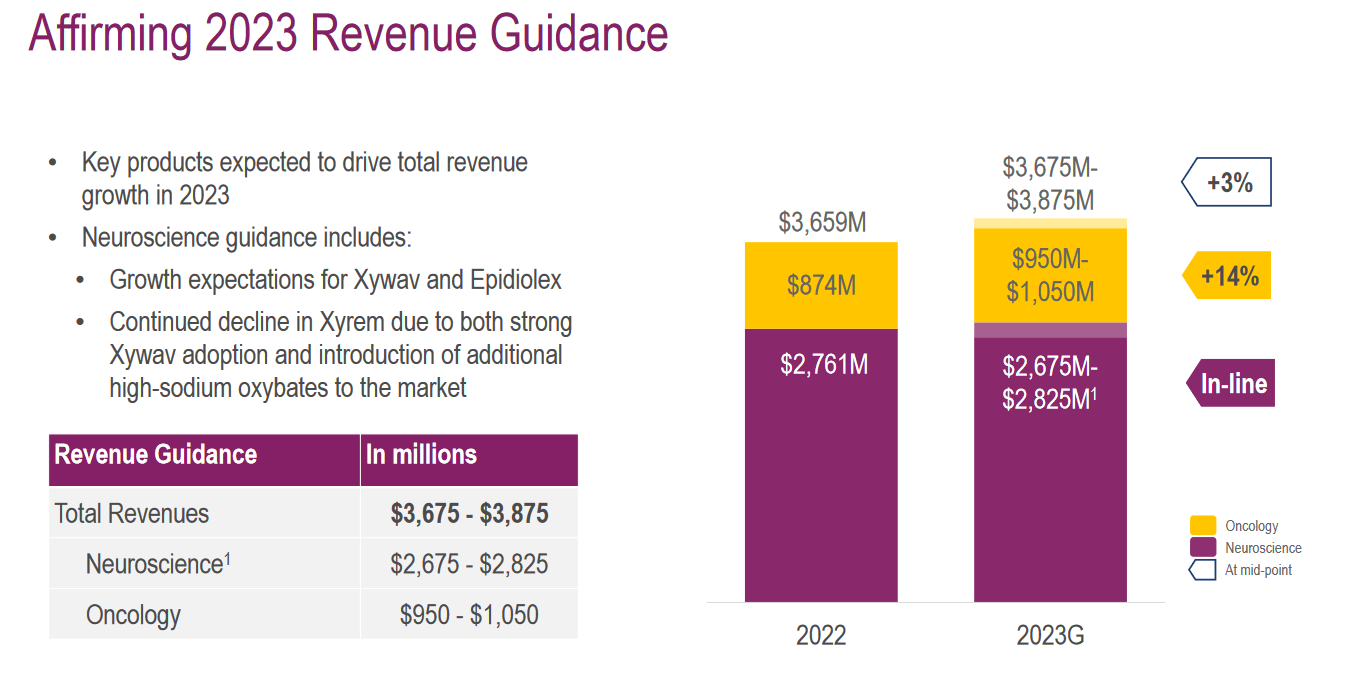

One of the primary challenges Jazz Pharmaceuticals faces is the lengthy regulatory approval process for zanidatamab, which may extend over 2-3 years. While the company is keen on diversifying its product offerings with the introduction of zanidatamab, this prolonged timeline poses a potential risk to its revenue stream in the interim. Delays in obtaining regulatory approval could hamper Jazz's ability to capitalize on the new product's potential benefits and market opportunities during this time. Diversifying revenue streams will be crucial for the longevity of the company, but so far I don’t see any risks in their path to $5 billion of revenues in 2025, the affirmed guidance for 2023 is setting them up well to achieve it.

Investor Takeaway

The depressed valuation right with JAZZ is presenting a very solid opportunity to investors. The target for 2025 is to reach $5 billion in revenues, and with a historical net margin of over 20%, the potential upside here seems too far to not be a part of right now. JAZZ is actively diversifying its revenue streams and with the Q2 yet to be announced though, investors will wait eagerly to see progress on margin expansion. A surprise for the top and bottom line should result in the share price jumping significantly. The p/e is around a third of the sector and with the margins that JAZZ has it seems fair to suggest a multiple of around 16x at least. This concludes my rating of JAZZ a buy right now.

For further details see:

Jazz Pharmaceuticals: Depressed Valuation Opens Up Potential