TSN - JBS: Q3 Earnings Strain Continues But Glimmers Of Recovery (Rating Upgrade)

2023-11-18 07:53:03 ET

Summary

- JBS faces challenges in 2023 linked to increased exposure to the North American market.

- Q3 performance highlights ongoing issues in Beef North America but shows improvements in the U.S. beef sector.

- Financial metrics reveal increased leverage but reduced net debt, with free cash flow rising in Q3.

- Despite challenges, positive indicators and anticipated improvements in 2024 make JBS shares more appealing.

- I'm shifting my recommendation from neutral to overweight, considering the potential for share appreciation, the upcoming dual listing, and the positive trajectory in the cattle cycle.

JBS (JBSAY) continues to confront challenges in the second half of this year, primarily attributed to its increased exposure to the North American market. This was the initial reason for my neutral stance towards the company in my previous article .

In the United States, the cattle cycle is currently experiencing a decline in the available headcount, leading to increased costs for meatpackers who need to invest more in acquiring animals. However, there is a possibility that the inflection point has already passed.

In the third quarter, there was still no significant positive news in JBS' Beef North America, reflecting the ongoing challenges posed by the cattle cycle and the decline in beef prices.

Initiatives in the U.S. beef sector aimed at maximizing cattle profitability have resulted in sequential improvements, aligning the profitability of JBS's operations with its peers and mitigating risks. The positive margin recovery following reported operational issues in the first quarter also contributes to a more favorable outlook.

With this in mind, anticipating that JBS may trade at an EV/EBITDA of around 6.2x next year, I see a more attractive valuation for the company. The modest margin progress in Q3 leads me to adopt a more bullish stance.

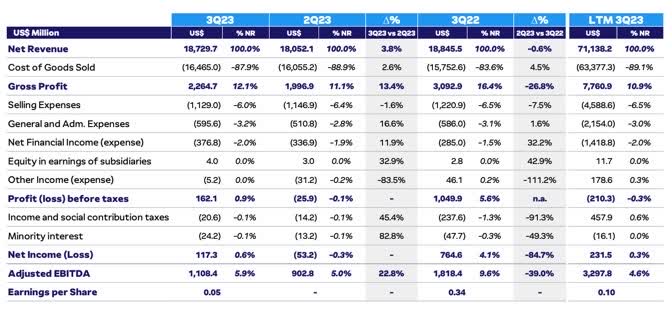

JBS 3Q23 Earnings Results

JBS's third-quarter results generally remained weak, reflecting the bearish cattle cycle in the U.S. However, there were signs of improvement.

JBS' IR

On the negative side, there was little progress in margins at JBS Beef North America, standing at 1.7%, up a meager 0.2 p.p from the previous quarter. This segment continues to suffer significantly from the negative cattle cycle in the U.S. Margins at JBS Australia also remained low at 8.6%, declining 0.9 p.p. quarter over quarter despite yearly expansion.

On the positive side, JBS USA Pork achieved an EBITDA margin in the high single digits, consistent with historical levels. There was also increased free cash flow generation, reaching R$3.4 billion, a yearly increase of 6.3%. This was driven by the release of working capital, offsetting the retraction in EBITDA and presenting favorable prospects for the coming years in all segments, excluding JBS Beef North America.

In the adjusted EBITDA ranking, Pilgrim's Pride led with R$2.195 billion, down 25.7% year over year. Following were JBS USA Pork (R$1.021 billion, up 2.2%), JBS Australia (R$664.6 million, up 34.7%), Seara (R$566.4 million, down 68.2%), JBS Beef North America (R$502.7 million, down 80.1%), and JBS Brasil (R$484.4 million, down 41.3%).

Pilgrim's Pride and the U.S. pork division were JBS's best-performing divisions, benefiting from reduced grain costs, strong demand, and positive seasonality, resulting in an 86% improvement in combined EBITDA. The company's net profit stood at R$572.7 million, down 85.7% year over year.

Regarding operations in Brazil, lower beef and chicken prices on the international market impacted revenues and contributed to a sequential compression of margins at JBS Brasil and Seara. JBS Brazil recorded a 10% reduction in export revenue, but revenue from beef sales in the domestic market rose 3%, driven by supply growth and lower prices.

In the consolidated result, JBS's net revenue fell 7.6% for the year, totaling R$91.4 billion. However, its U.S. arm, Beef North America, once again led in net revenue from July to September, surpassing Pilgrim's Pride with R$29 billion in sales.

{kind=link}

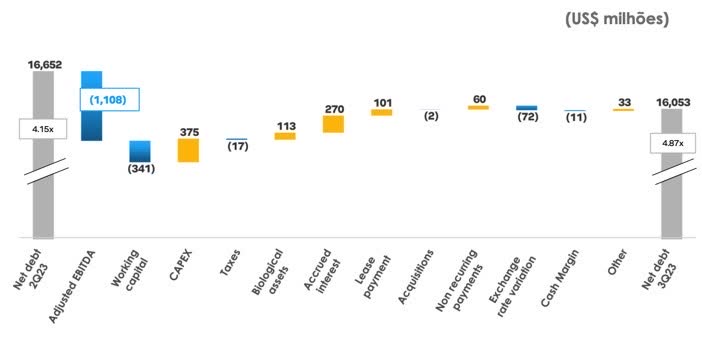

Leverage increased to a level of 4.87x Net Debt/EBITDA, up from 3.9x in the second quarter, driven by a decline in EBITDA over the trailing twelve months. On a positive note, net debt decreased from $16.65 billion to $16.05 billion. This reduction was attributed to the company releasing R$1.7 billion in working capital, primarily due to lower inventories and improved accounts receivable. As a result, the company generated R$3.4 billion with a yearly increase of 6.3% in free cash flow.

{kind=link}

Challenges Persist in Beef North America While Brazil's Livestock Cycle Thrives

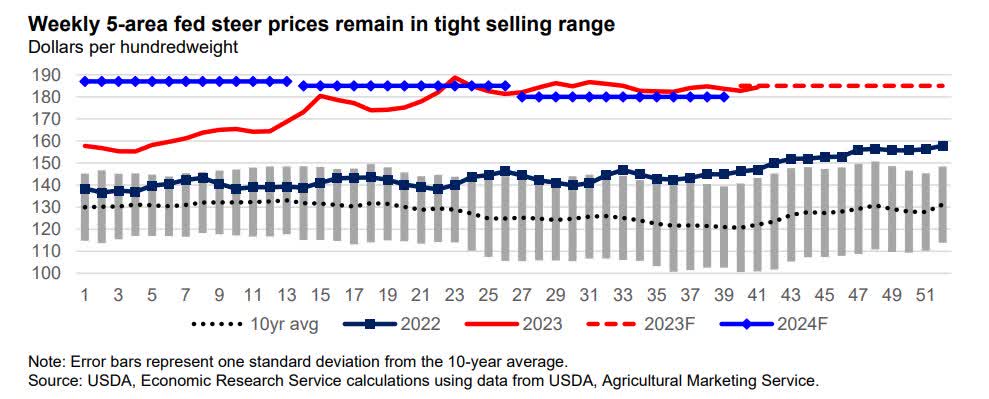

With the supply of cattle remaining tight in the US, despite resilient demand, the spread in 3Q23 exerted sequential pressure, causing the EBITDA margin to remain relatively stable compared to the previous quarter but down 5.7 percentage points year-over-year. During 3Q23, the cutout price marginally decreased, while the cost of cattle rose slightly, providing evidence of the critical moment in the current cattle cycle in the US.

However, the situation could have been worse. This quarter, JBS addressed some internal setbacks both commercially and concerning the White Bone plan (linked to initiatives to maximize cattle profitability). These corrections partially offset the industry's deterioration and helped the EBITDA margin to remain stable.

When examining the estimated cattle prices in the five major cattle-producing regions in the United States, the outlook for 2024 has decreased from $190 per hundredweight to $180 per hundredweight. Although this remains considerably higher than the historical average of $130 per hundredweight, which would be optimal for JBS, it is now more likely to envision a scenario approaching $150-$160 per hundredweight for 2025 and beyond.

USDA, Agricultural Marketing Service

{kind=link}

For the coming quarters, I anticipate that cattle availability will remain low in the US, contributing to the segment's EBITDA margin remaining in the low single digits in the next quarter and possibly into 2024. I anticipate a gradual return to a more excellent cattle supply in the country and, consequently, higher margins, likely only in mid-2025.

Regarding the Brazilian segment, weakened sales prices on the international market have negatively impacted the segment's net revenue, leading to an annual decline. As the drop in prices has outpaced the decrease in the cost of cattle, margins have also been adversely affected.

Looking ahead to 2024, I expect the cattle cycle in Brazil to remain favorable, given the high supply of animals in the slaughter phase. If prices on the international market rise again, and the USD/BRL exchange rate remains stable at around the $1 to R$5 range, I believe the EBITDA margin should stay in the mid to high single digits over the quarters.

If one of these two factors does not occur, it is possible to see the EBITDA margin remaining in the mid-single numbers. I anticipate the operation will benefit from higher beef exports to the US as long as the cycle remains negative there.

Valuation: More Attractive

It's noteworthy that, in addition to my expectation of a gradual improvement in the figures for most of JBS's segments in 4Q23 and throughout 2024, the approval and eventual completion of the dual listing process for the shares in the US is likely to occur soon.

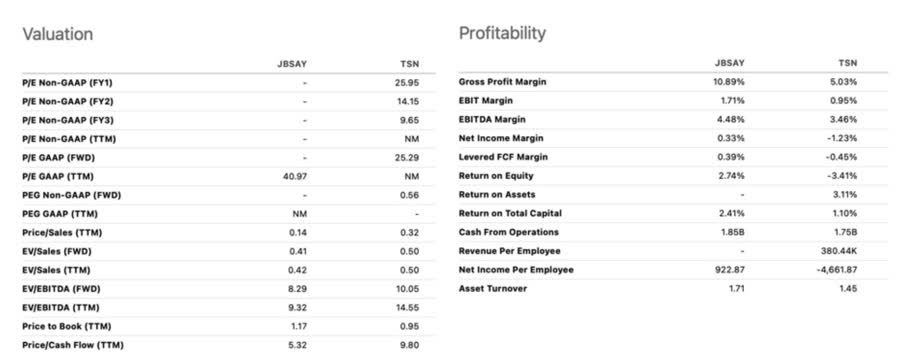

This process can potentially unlock the company's value, especially considering JBS's discount compared to its US peers. I believe this could serve as a catalyst for the company's share appreciation. Despite a 20% increase since the announcement of the viability process in early July, I think the market has not fully priced in this movement. My belief is supported, for example, by Tyson Foods ( TSN ), which is trading at a forward EV/EBITDA of 10x, a significant difference from JBS's 2023 estimated trading range and much less attractive margins compared to the Brazilian company.

{kind=link}

In this context, analyzing the S&P Global Intelligence consensus for 2024, it is projected that JBS may be traded at an EV/EBITDA multiple of 6.2x as the company is expected to deleverage and improve its margins with the overall cycle getting better. The current multiple at which JBS is traded is much more comfortable and closer to its historical average of 5.5x.

The Bottom Line

Even amidst a challenging cattle cycle, where JBS reached a low point in the first quarter of this year, the company generated $572.7 million in profit, elevating its EBITDA margin from 2.5% in Q1 to 5.9% in Q3. Simultaneously, it generated $3.5 billion in cash while successfully reducing its net debt.

JBS' IR

In 2024, as the cycle is expected to improve, JBS is anticipated to deleverage, potentially leading to even more robust cash generation, thereby creating value for its shareholders. Even if this progress unfolds gradually, some short-term catalysts, such as the dual listing of JBS shares in New York and Sao Paulo between the end of this year and the beginning of 2024, could prove interesting.

Given these positive developments, I believe JBS shares are currently at an intriguing level, especially considering the likelihood that the cattle cycle has bottomed out this year and the trajectory for the next few quarters appears promising. With the enhancement in the EBITDA margin, the company, presently trading at an EV/EBITDA close to 6.2x for next year, seems more compelling this time, suggesting potential appreciation at the current level.

Consequently, I am revising my previous neutral recommendation to overweight.

For further details see:

JBS: Q3 Earnings, Strain Continues, But Glimmers Of Recovery (Rating Upgrade)