JCE - JCE: Some Potential But Looking For A Discount

- JCE has declined along with the rest of the markets this year; it stubbornly hangs onto its premium valuation.

- The fund has generated alpha this year on a NAV basis, as its name implies, but it has only been very minimal.

- The fund boosted its distribution since we last touched on the name but is now pushing an over 11% distribution rate.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on July 21st, 2022.

Nuveen Core Equity Alpha Fund ( JCE ) continues to hang on right near a premium despite the volatile markets. Generally, we see closed-end fund discounts widen out during volatile periods. 2022 has been delivering just such an event, with most CEFs experiencing the widening discounts that we anticipate.

JCE delivered solids results in the prior year, as did the broader market. Basically, JCE is an options writing fund that invests primarily in large-cap names. They write index options with a target of up to 50% of the notional value of the portfolio. They are running at only a 28% call covered at this time.

Indexes can't be owned directly, so they are cash-settled contracts. In theory, the losses on these options contracts are unlimited as an index can rise to infinity. We know that obviously won't happen. However, they are hedged if the indexes start to run higher. They are hedged simply by being long on constituents of the index itself.

It is quite similar to the S&P 500 in its exposure, which is 50% of its blended benchmark. The other 50% is the S&P 500 Buy/Write Index. The fund will primarily follow the broader market's returns, with options writing potentially limiting some of the downside.

On a YTD basis, this has only slightly helped offset some of the declines experienced by the SPDR S&P 500 ( SPY ). With the total NAV return of JCE outperforming SPY, we are achieving "alpha," as the name implies. If they were closer to the 50% level, they could have potentially achieved an even better result.

On a share price basis, it hasn't helped at all. The share price will be at the mercy of buyers and sellers. Since the fund was at a bit higher of a premium previously , this is why I was more cautious.

Ycharts

The fund continues to flirt between a premium and discount relative to its NAV per share. It has come down only slightly. Therefore, I still am cautious at this time.

Overall though, with the declines in the equity space we've already experienced, it could still be worth taking a look. At the very least, I don't see it as a strong sell candidate. Holders hanging onto the shares already should do okay going forward.

The Basics

- 1-Year Z-score: 0.66

- Premium: 0.85%

- Distribution Yield: 11.12%

- Expense Ratio: 0.99%

- Leverage: N/A

- Managed Assets: $217 million

- Structure: Perpetual

JCE's investment objective is "to provide an attractive level of total return, primarily through long-term capital appreciation and secondarily through income and gains."

To achieve this, the fund will invest "in a portfolio of actively managed large-capitalization common stocks, using a proprietary quantitative process designed to provide the potential for long-term outperformance." They will additionally; "sell call options with a notional value of up to 50% of the Fund's equity portfolio in seeking to enhance risk-adjusted performance relative to an all-equity portfolio."

The fund is quite small, and the losses mounting this year have only served to reduce the size further. Unfortunately, the way that CEFs are designed to pay out almost all of their earnings (which JCE is pretty much doing) doesn't lend a way for them to grow meaningfully. There are exceptions to this, of course, as there always are.

This smaller size means a lower relative trading volume for the fund. That being said, for most retail investors, the volume should still be mostly sufficient. According to Yahoo Finance, the average daily trading volume is around 57k.

The fund doesn't operate with any leverage, so that is one less concern in this environment of rising rates and rising risks. The expense ratio is also reasonable within the CEF space.

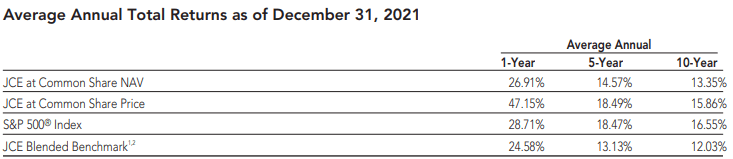

Performance - Alpha Producer Relative To Benchmark

On a YTD basis, we saw that JCE had outperformed SPY. That is the investible comparison for the S&P 500. While that is happening during this downturn, it has underperformed this index over the long run. However, when looking at its benchmark, it has outperformed. This data was as of the end of 2021, and it can be found in the last annual report available.

{kind=link}

One of the reasons that the options writing strategy would have resulted in reduced performance over the last decade is simply due to the raging bull market. During massive run-ups, they will underperform due to positions being called away.

Their true strength lies in a mostly flat market when there isn't much of anything going on. It also works out okay in declining markets simply by reducing some losses through the collected premiums. Of course, it isn't a sufficient amount to offset massive declines. That's why we still see the fund negative for the year.

If one is expecting challenges to continue going forward while the Fed is hiking rates, that's what makes call writing funds so appealing at this time. The fact that they can still generate some capital gains, compared to a long-only fund that can have a more difficult time finding those capital gains. Capital gains are important for equity CEFs, as that's how they fund their distributions and, essentially, how they make returns for shareholders.

One way to juice these returns potentially for CEF investors is to buy when the funds are at deeper discounts. That's a way to produce a better chance of achieving alpha. Unfortunately, that isn't the case for JCE at this time. Despite the fund's premium coming down some, it isn't in what I'd consider overly compelling.

Ycharts

We need more blood in the streets to get this fund to drop to its longer-term decade average ~4% area discount. Ideally, an even deeper discount of 6 to 10% would be even more attractive. That could really compel me to consider adding the fund to my roster. Where we have good news is that the overall market has come down substantially from the start of the year. That puts the underlying valuations at a better place than where we started.

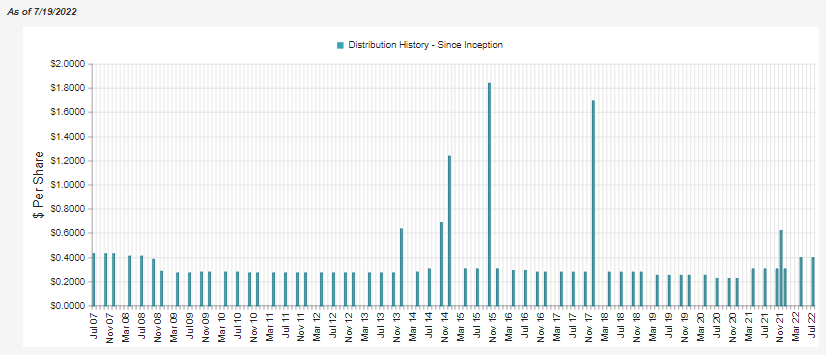

Distribution - An 11.12% Rate

Since our last update, the fund has boosted its distribution quite materially. It went from a quarterly $0.3040 to the now $0.3952. That was a 30% boost for shareholders.

{kind=link}

That's certainly positive for the fund. However, considering they hiked it when the market is slowing is something to be cautious about. Now at an 11.22% distribution yield on a NAV basis, that's what the fund would have to earn to achieve this new payout. That's a high hurdle going forward.

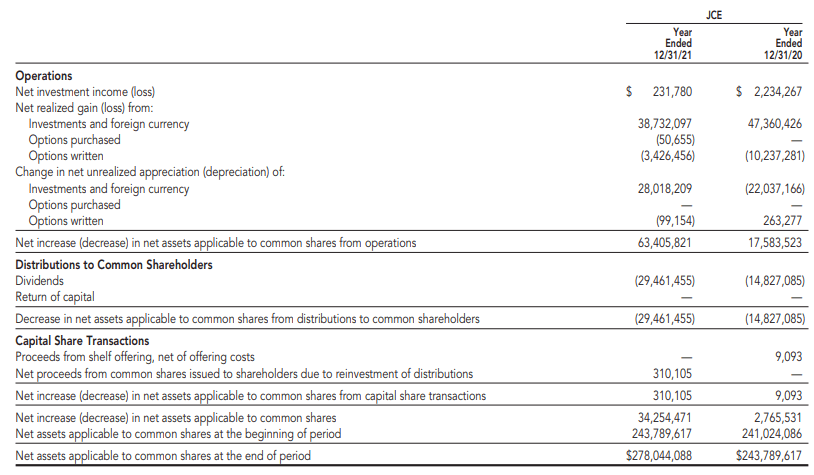

With their last report available, JCE's net investment income was almost nonexistent. It fell dramatically from the previous year period. Due to the strong 2021 market, though, they had more than enough to cover the distribution through capital gains.

In each of the two previous years, written options had actually produced losses for the fund. That goes back to being cash-settled positions and the market performing so strongly. 2020 started extremely rough with the COVID sell-off but quickly rocketed higher and rebounded. I'd be looking to see positive gains attributed to their option writing this year in their next report.

{kind=link}

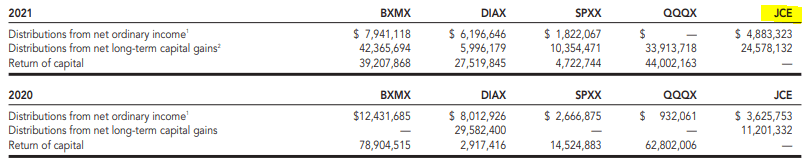

Despite what the earnings suggest above, for tax purposes, a sizeable portion was still attributed to ordinary income. The bulk of the distribution has been classified as long-term capital gains in the past two years.

{kind=link}

A further breakdown of the distribution shows just 4.82% was non-qualified dividend income, 11.55% was qualified, and another 0.20% was section 199A in 2021. That means that most of the distribution was tax-friendly.

JCE's Portfolio

As mentioned previously, the portfolio is essentially just a large-cap fund with a heavy focus on the S&P 500 names. ~98% of the fund is classified as large-cap, with 139 positions in total. This all makes the portfolio rather boring, but it is by design. Being boring isn't necessarily a problem, as it is the options strategy that gives the fund its "twist."

{kind=link}

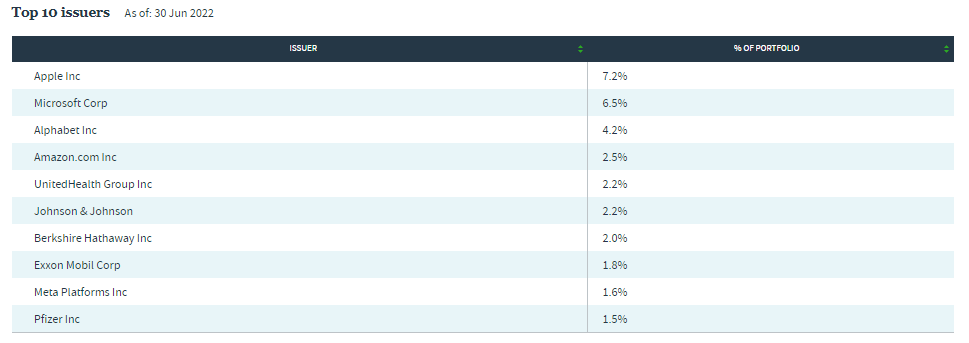

A position that has slid off this list was Tesla ( TSLA ) since we last took a look. NVIDIA ( NVDA ) is another one. This isn't too surprising, given that the shares of those companies have been under significant pressure. Instead, we see names such as Berkshire Hathaway (BRK.A) (BRK.B) and Exxon Mobil ( XOM ) in the top ten.

The relative performance between these names from the end of November 2021 to the end of June 2022 suggests much of this fluctuation is due simply to price changes in the underlying stocks. XOM has blasted higher in this period due to surging crude oil prices. Even despite the more recent declines in crude, energy stocks are way up. BRK.B has simply not lost as much relative to higher growth stock names.

Ycharts

If one looks at the full holding list , we will see that is the case. NVDA is still a holding but comes in at only a 0.72% weighting now. TSLA fell to a 1.26% allocation.

Conclusion

JCE is more interesting at this time due to the broader equity declines. However, the fund continues to remain stubborn and hang onto its premium. A valuation that the fund hasn't historically maintained for extended periods. That suggests the potential that more downside through discount expansion exists.

On the other hand, going back to the overall market declines and a potentially sideways market, it does make a stronger case for JCE. With the fund's options writing, it can still produce gains easier if the market moves sideways. Therefore, those already holding the position probably shouldn't feel compelled to let go at this time.

For further details see:

JCE: Some Potential, But Looking For A Discount