JD - JD.com: China's Economy In Recovery

Summary

- We’re bullish on JD.com. We believe the company’s online shopping platform has been relatively resilient to China’s lockdown regulations and macroeconomic headwinds.

- We expect the company to benefit from demand tailwinds as China slowly but surely exits the COVID restriction environment.

- JD is one of China’s top two B2C online retailers, operating in an industry forecasted to grow at nearly 21% between 2022-2025.

- We believe JD provides a favorable entry point at current levels and recommend investors buy the stock as China’s economy slowly recovers.

We’re buy-rated on JD.com ( JD ). While JD is not necessarily a household name for the average retail investor in the west, the company gets major buzz in China. JD is one of China's top two Business-to-Company (B2C) online retailers, alongside Alibaba ( BABA ). We’ve been bullish on BABA and are now adding JD to our list of bull stocks. JD trades on the Hong Kong stock exchange; investors can be hesitant to invest in Chinese stocks, but we believe JD is well-positioned to grow meaningfully in 2023. We believe JD’s retail and logistic markets have been relatively resilient to China’s economic slowdown resulting from COVID regulations. JD dropped around 5% over the past year, outperforming the SPY Index, which declined 19% during the same period. We believe JD is better positioned to outperform in 2023 as China rapidly takes measures to shift away from the COVID restriction-heavy environment. We recommend investors buy the stock at current levels.

Already a household name in China

JD operates in a quickly expanding market, and we believe the company’s well-position to ride demand tailwinds in online retail shopping. The retail online shopping industry is forecasted to grow at 22.73% between 2022-2025. JD is currently ranked as the top platform for online Electronics and Media in Greater China by EcommerceDB. We like JD’s position in Chinese markets and believe the company’s established customer base as a top retailer in China will boost revenue growth in 2023.

Our bullish sentiment on the stock is based on our belief that JD’s business model replicates that of Amazon ( AMZN ) in China. In 3Q22 , JD’s net revenue hit RMB 20.2B yuan, achieving a 48% increase Y/Y. We attribute the growth to JD’s Amazon-like strategy of selling high-quality consumer products at lower prices and delivering them quickly. JD’s annual active customer accounts increased 6.5% to 588.3M Y/Y despite the economic slowdown. We believe JD’s focus on long-term relationships keeps customers happy and incentivizes them to spend more money on the e-commerce platform. We believe bulk purchases have also made the company relatively resilient to demand headwinds from individual consumers resulting from the harsh macroeconomic environment.

China easing lockdown regulations will boost sales

We ended the year on a positive note for Chinese stocks as China shifts away from its COVID zero regulations. We believe JD will experience demand tailwinds as China surprises the market by taking measures to reopen. JD had rough 4Q21 and 1Q22 earnings periods missing EPS expectations in both quarters. We believe JD’s now recovering, with the company reporting a 40.44% surprise on EPS expectations in 3Q22 but coming in short on revenue by 0.11%. We expect JD is better positioned to outperform as China’s economy is revived. We saw China move away from COVID regulations when the nation issued 20 guidelines to local officials with looser rules. In early December, China’s National Health Commission jump-started the reopening by setting out ten new measures to ease COVID zero regulations. We don’t expect the reopening process to be smooth; China’s already getting a lot of backlash over fears of increasing infection numbers. Regardless, we believe China is on the way to returning to normalcy after a rough three-year adherence to strict COVID regulations. We believe JD will benefit from the Chinese economy's recovery.

We also expect the company will see increased demand as the Chinese New Year approaches, set for February 2023. We believe the Chinese New Year is a major opportunity for the e-commerce space. According to Pattern Research, e-commerce companies in China typically enjoyed heightened sales during the Chinese New Year, also known as the Spring Festival- until the pandemic began in 2020. During the pandemic, online retailers tried to move the festivities online but still did not achieve pre-pandemic sale growth. Now that the pandemic environment is quickly lifting in time for the new year, we believe the company will be able to leverage higher sales this February.

JD is the simpler pick in the e-commerce market

While JD is a dominant player in the retail market, that is about it. The company does not have other sources of meaningful revenue besides its retail and logistic segments, making it the simpler pick compared to competitor Alibaba which achieves significant revenue streams from its Alibaba Cloud.

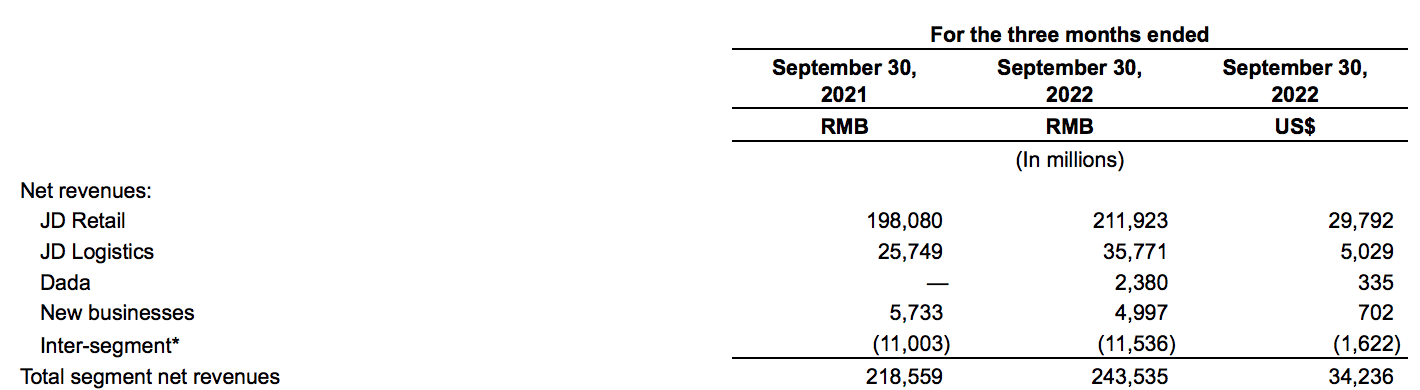

The following table outlines JD’s net revenues for 3Q22.

{kind=link}

JD does not heavily invest in non-commerce markets; the company operates smaller cloud, fintech, and healthcare subsidiaries compared to those of Alibaba. JD’s only significant subsidiary is its first-party logistics network that provides its services to external customers. We believe JD is for investors looking for a simple e-commerce company that focuses on doing one thing and doing it well.

Stock Performance

JD grew around 44% over the past five years. Over the past year, the stock declined by about 5%. We attribute the decline to the economic slowdown in China. JD still outperforms the competition on the one-year metric, with the competition down Coupang ( CPNG ) by around 38%, Amazon by about 49%, and Alibaba by nearly 14%. We’re constructive on JD as we believe the company’s business has been relatively resilient to macroeconomic headwinds in China and expect a clearer growth path for JD as China reopens.

The following graphs outline JD’s performance over the past year and five years.

Seeking Alpha Seeking Alpha

Valuation

Regarding JD’s valuation, the stock is trading at 41.57x on a P/E basis. JD’s P/E ratio is the best way to examine if the stock is overvalued or undervalued. We believe JD is undervalued and hence believe JD is a value stock. We believe JD is undervalued because we believe the market has yet to factor in the growth potential JD has as China’s economy reopens. We expect the stock to surge as China rapidly takes more serious steps to lift the lockdown regulations. The stock has already more than doubled, growing nearly 67% in the past two months. We expect JD to grow meaningfully in the first half of 2023, specifically with the approaching Chinese holiday season, and we believe the stock’s valuation provides a favorable entry point to invest in JD’s 2023 growth.

The following table outlines JD’s valuation.

Macrotrends

Word on Wall Street

Wall Street seems to be overwhelmingly bullish on JD stock. Of the 41 analysts covering the stock, 37 are buy-rated, and four are hold-rated. The current price target is $64. The median sell-side price target is $81, and the mean is $80, with a potential upside of 25-26%.

The following table outlines JD’s sell-side ratings and price targets.

TechStockPros

What to do with the stock

We’re bullish on e-commerce giant JD. We believe the company’s online shopping platform has been resilient to China’s economic slowdown due to COVID zero regulations. We expect the company to experience demand tailwinds as China rapidly shifts away from COVID regulations and the Chinese New Year approaches. JD is one of China’s top online retailers and is an industry forecasted to grow exponentially. We think JD is relatively cheap, providing a favorable entry point at current levels, and recommend investors buy the stock at current levels.

For further details see:

JD.com: China's Economy In Recovery