JDSPY - JD Sports Fashion: H1 2024 Performance Imparts Confidence On Business Growth Momentum

2023-09-26 03:56:16 ET

Summary

- I recommended a buy rating, with expected growth momentum for the next 2 years.

- The company has experienced significant revenue growth and improved operating efficiency over the past two decades.

- 1H24 results were promising, with strong sales and a robust performance in North America, inspiring confidence in future growth.

Overview

My recommendation for JD Sports Fashion PLC (JDSPY) is a buy rating, as I believe the business growth momentum can continue for the next 2 years. Notably, management has implicitly guided to 10+% growth for 2H24, which indicates the business is on track to regain its low-to-mid-teens revenue growth pace, just like it did historically.

Business

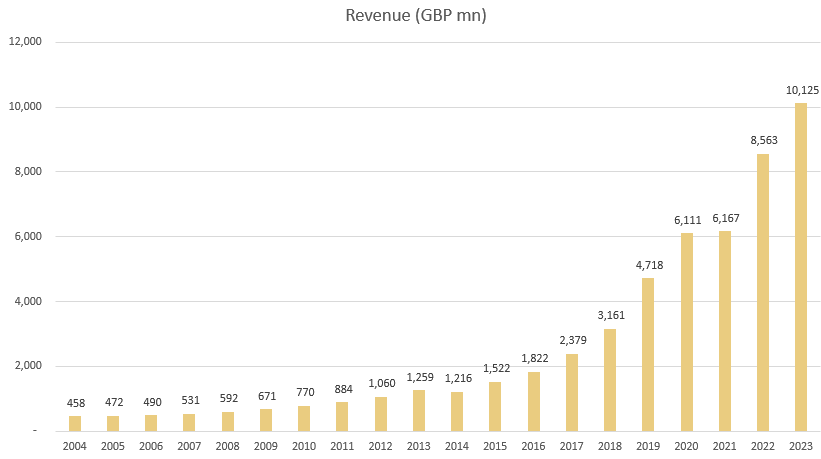

JDSPY runs a series of retail outlets specializing in the sale of branded sports and casual apparel. Their product range includes sports and casual footwear, clothing, accessories, and more. Over the last two decades, the business has experienced remarkable success, with their revenue surging from GBP 470 million to slightly over GBP 10 billion in FY23. This growth was accompanied by consistently positive adjusted profit before tax figures, rising from GBP 5 million in FY24 to GBP 991 million in FY23. Notably, the adjusted profit before taxes margin has also expanded from 1% to 10% during the same period, highlighting the business's improved operating efficiency.

{kind=link}

Recent results & updates

1H24 adj PBT for JD Sports came in at GBP375 million, and adj EPS came in at 4.62p. Overall group sales were up 8.3%, with gains of 9% in Sports Fashion and 2.2% in Outdoor leading the way. 1H24 EBIT of GBP398 million was GBP20 million below consensus due to a decline in gross margin of 50 bps to 48% and an adjustment to EBIT margin of 113 bps to 8.3%. Sales were positive. The UK contributed negatively (-8%) to 1H24 performance, while the rest of Europe (21.5%), North America (16.9%) and the Rest of the World (17.7%) drove the expansion.

The 1H24 results, in my opinion, were very promising, and they removed any doubts about JD's potential for growth. Most importantly, my calculations show that 2H24 performance is consistent with an organic growth trajectory of 10%+, lending credence to the story that the company is returning to its mid-teens growth profile as the COVID growth benefits fade. Management has stated that they are on track to produce a profit of over GBP1 billion in FY24. If "more than GBP 1 billion" is GBP 1.05 billion (my guess), then the 2H24 adj PBT would be around GBP 670 million. This would mean GBP6.3 billion in revenue, an increase of 10%+ from 2H23, based on the average 2H adj PBT margin over the past two years.

{kind=link}

“As you remember, we say double-digit growth, we are delivering 12% organic growth; double-digit market share, we are gaining share in every market we operate, including U.K., which is a more mature market; and double-digit profit, and as you have seen, we are on track to deliver more than GBP1 billion profit for the full year in line with our guidance”

{kind=link}

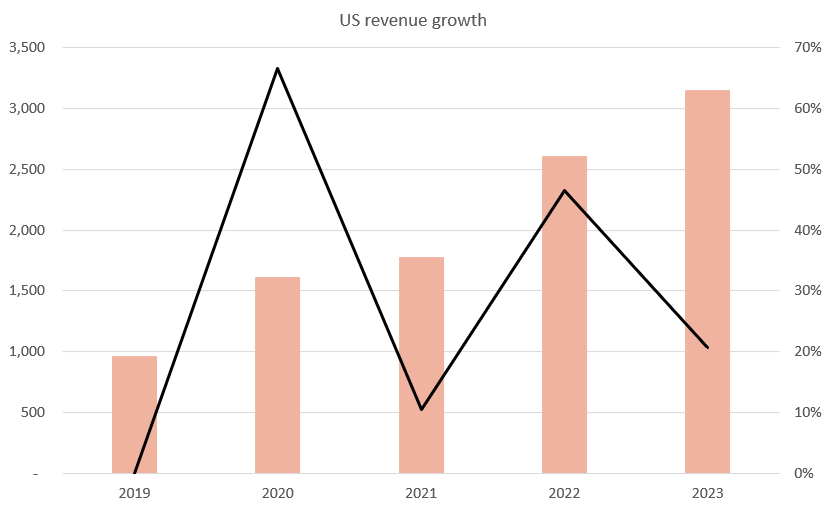

Notably, this also includes a more robust North America, which bounced back in July after a lackluster June. This is significant because, before this, I was skeptical that the US segment could sustain the rapid expansion it has seen in recent years (Revenue literally more than 3x over 4 years). This, along with the slowing economy evidently caused by inflation and high interest rates, was cause for concern. I'm feeling more optimistic now that management has acknowledged that "done particularly well in North America," with strong reported results like premium organic sales.

And when the new season come and start in July, you have seen some of our competitors in July was difficult. July was a very good month for us, because we had new stock and it was a full price month. From: 1H24 earnings call

The US performance was also encouraging in that it is in contrast with what Footlocker mentioned during their 2Q24 earnings call.

With that said, we are continuing to operate in a highly dynamic retail environment and while we develop the Lace Up plan with the knowledge that 2023 would be a reset year, sales have been softer than expected through the first half.

The lower end contemplates modest weakening in trends to reflect macro risk including potential pressure from factors like the resumption of student loan payments.

So we feel like we're set up well in terms of having the products that our customers want from back-to-school, but it's a little bit softer for us and we would add that pressure on our customer skews a little bit more towards pressure on discretionary expense with people being a little more price sensitive and a little more choiceful on their selection.

With sales softer than anticipated, we are taking more aggressive actions on promotions to drive demand and manage our inventory to ensure we are best positioned for the upcoming holiday season and for clean transition into 2024.

Considering the factors mentioned above, I am confident that JD can surpass the consensus estimates for 2H24 (currently projecting 5% revenue growth). I would also note here that there should be no concerns about lack of inventory, as management has confirmed that they have sufficient inventory in the US. It's worth recalling that limited inventory was a contributing factor to weaker performance in the US in June, so it's reassuring to know that management is now well-prepared in this regard.

Regarding profitability, I anticipate further improvement, unlike what we saw in 1H24 when the EBIT margin declined. This is because in 1H23, operating costs included GBP 10 million associated with the acquisition of Courir and former Conbipel and GAP stores , as well as a GBP 10 million investment in cybersecurity, a new HR platform, and duplicated warehousing costs in the UK and Europe. These costs will no longer affect the P&L in 2H24, providing a GBP 20 million boost.

Valuation and risk

Author's valuation model

According to my model, JDSPY is valued at GBP189 pence in FY24, representing a 28% increase. Note that my target price is at the same level as where the stock traded in the early part of CY23 (peak of GBP186 pence). My target price is based on my growth forecast for the low teens over the next 2 weeks (12% in FY24 and FY25).

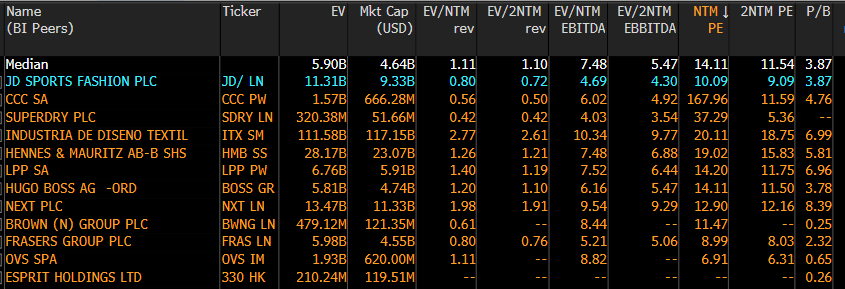

JDSPY is now trading at 10 forward PE, which I believe to sustain at this level, especially when compared to its peer Foot Locker ( FL ), which is trading at 9.5x forward PE. JDSPY should trade at a premium because of its better growth profile (10+% growth vs. FL’s negative growth)

{kind=link}

The downside to JDSPY's performance is that it sells a product that is not a necessity and is largely reliant on consumers' spending abilities. JD’s consumers could be more impacted by the current macroenvironment (inflation, rising rates, etc.), thereby putting more pressure on demand.

Summary

I recommend a buy rating for JDSPY. The 1H24 results, while slightly below consensus, were promising, confirming JD's growth trajectory. Management's target of over GBP1 billion profit for FY24 and a robust North American performance, along with adequate inventory levels, inspire confidence. The expectation of improved profitability in 2H24, with reduced operating costs, further strengthens the outlook.

For further details see:

JD Sports Fashion: H1 2024 Performance Imparts Confidence On Business Growth Momentum