JDSPY - JD Sports: Long-Term Superstar Potential

2023-06-27 18:32:53 ET

Summary

- JD Sports has consistently strong financial performance and ambitious growth plans, including opening 250-350 new stores annually in underpenetrated markets.

- The company has a strong balance sheet with net cash of £1.5bn and potential for dividend growth over the long term.

- Despite risks such as supply chain inflation and execution challenges in expansion, JD Sports' attractive valuation and growth potential make it a strong buy.

One of the best-performing shares in the U.K. stock market over the past 10 or 20 years has been JD Sports ( OTCPK:JDSPY ). It has been a sixteen-bagger in the past decade alone.

Yet despite its ongoing success, massive expansion plans and relatively attractive valuation, the share continues to offer what I see as good value.

Long-term Success Drivers

At first glance I think it is easy to misunderstand the JD Sports investment case.

The company has a lot of retail stores (and plans to open many more) at a time when bricks and mortar retail is supposedly on its way out. The shops sell sports gear that is easily available online and its customer base looks like a lot of spotty teenagers spending their pocket money.

However, the apparent simplicity of this model in fact masks some of the drivers for its success.

Demand for sportswear is both high and resilient. Teenagers, students and young adults often have limited expenses due to living with their parents, so can keep spending on sportswear even during a recession. The industry remains fragmented, giving JD both economies of scale and lots of white space for expansion.

By building an omnichannel brand, JD is able to make money from stores while also building a massive online business. Meanwhile, it has figured out how to expand internationally, rolling out its success model in different markets. Currently, JD operates in 32 markets, stretching from New Zealand in the east to the U.S. in the west.

Impressive Financial Performance

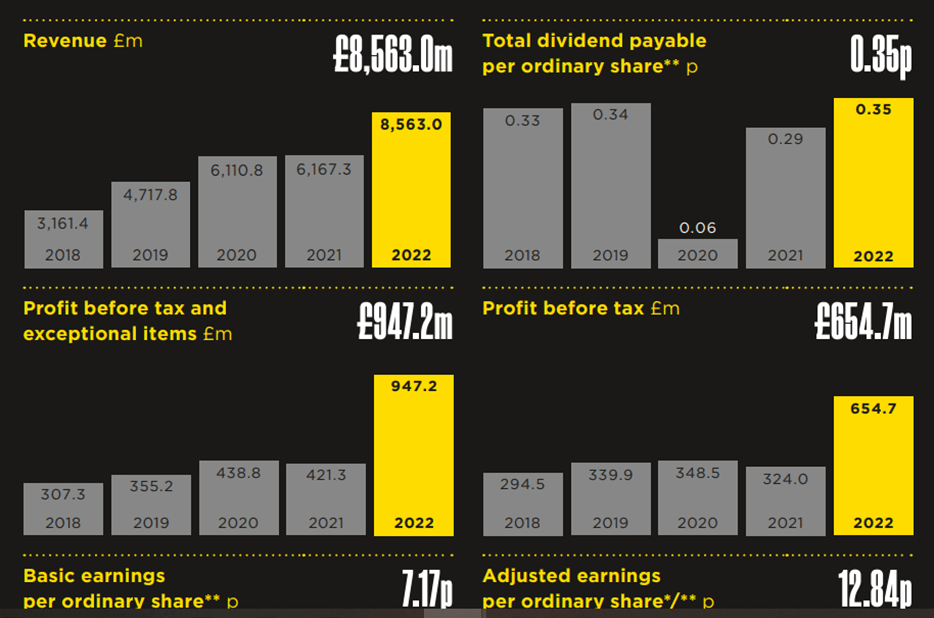

It is a simple model but a consistently profitable one. In its most recent financial year, the company grew revenues 18% to £10bn. Post-tax profits slipped, but still came in at £226m. The company has consistently been in the black in recent years.

The long-term revenue trajectory remains one of strong growth. The chart below shows up to 2022. The recently released numbers for the firm's 2023 financial year show strong revenue growth. In five years, revenues have more than tripled.

{kind=link}

Huge Growth Plans

What I think is most exciting about JD Sports at this point in its 40-year history is that it is doubling down on its success rather than resting on its laurels.

A change in long-term management last year made some investors nervous that performance would slip. So far, however, that has not been the case. Indeed, this year the company unveiled an ambitious new growth strategy .

The key financial highlights are, over the next five years,

- Double-digit revenue growth;

- Double-digit operating margin;

- Annual capex of £500-600m, of which 50% - 60% will focus on store expansion in underpenetrated markets with 250-350 new JD shops annually; and

- Cash generation from operating activities of £1 billion per year.

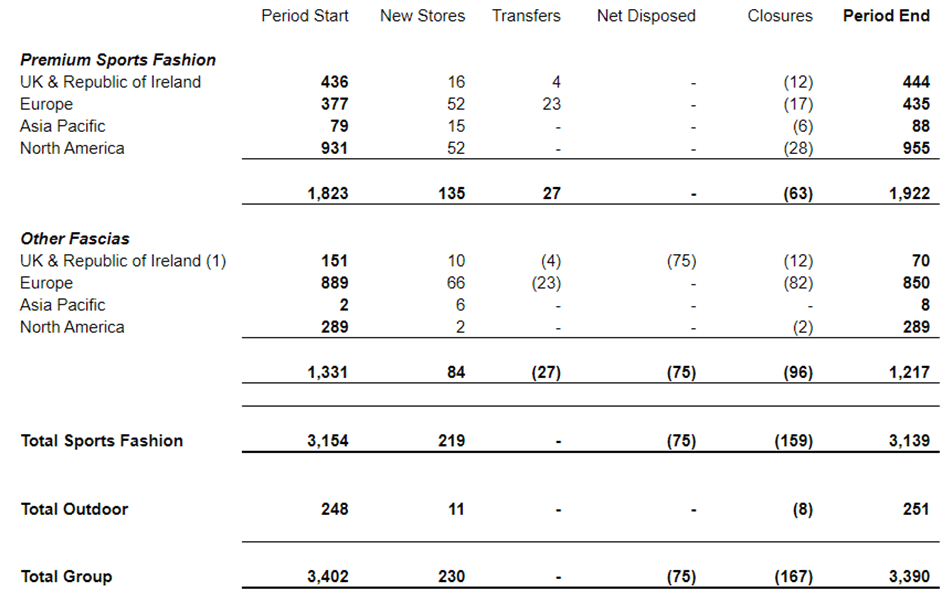

This week the company announced that it has opened a net additional 32 JD shops in the first four months of the year and is on track to open more than 150 JD shops across the year. Although it noted some softening in its North American business in June, it stuck to its guidance of headline profit before tax of just over £1bn.

Alongside growing the estate organically, the company continues to build by acquisition. The company is in the process of buying French retailer Courir for around half a billion euros. That will add over 300 stores in six European markets, primarily France. The 2022 year saw 13 acquisitions. Last year was more quiet, but acquisitions included swim school operators Total Swimming Holdings.

Although it is based in the U.K., the main market for the company's premium sports fashion fascias is now the U.S. The company plans to open 500 - 600 new JD stores over the next five years in North America. That is on top of stores it operates under other fascias.

{kind=link}

It is not expanding willy-nilly though. For example, last year it pulled out of the South Korean market.

There are also non-store businesses, like the swimming schools and a chain of gyms. I see potential for complementarity here and in the long run I think such ancillary propositions could be a substantial driver for growth. For now, though, I pin my main growth hopes on the store and online commerce business growing.

Interestingly, though, the company notes,

We firmly believe that JD, as a brand, has a deep relationship of trust with its consumers and that this relationship can be extended into other categories to create a lifestyle ecosystem of relevant products and services. We have already started to do this through the rollout of JD Gyms but we believe that this can be extended to other categories such as gaming and music, potentially through third-party partnerships.

So maybe those non-retail businesses will develop into something much bigger, which I think would be positive for the investment case.

Dividend Potential

Although JD pays a dividend each year the yield has been small and is currently under 1%. The company almost doubled its recent final dividend, to bring it closer in line with historical norms. But at 0.67p per share it is still small. Indeed, it remains at a little below half its pre-pandemic level.

Still, dividend coverage last year sat at over 20 times earnings. Even the recent jump will leave the dividend unusually well-covered compared to almost any other FTSE 100 company.

For now, I do not think the dividend is a compelling reason to buy JD Sports. But clearly, there is substantial scope for it to grow over the long term.

Strong Balance Sheet

JD ended its most recent financial year with net cash of £1.5bn. That compares to its current market capitalisation of £7.2bn.

The store expansion programme the company is currently undertaking could involve significant capital expenditure. But the business is run in a cost-efficient manner and I see the balance sheet as attractive.

Risks

One current risk I see is supply chain inflation. JD has been handling that well, but it remains as a risk.

Earnings in the most recent year were hit by impairments and restructuring costs. Given the evolving structure of the group, that remains a risk though hopefully will not materialise to the same extent.

I also think those ambitious growth plans are themselves a risk. They are one reason I am bullish about the business, but wide-scale expansion always brings risks especially if execution is harder than expected. That said, JD already has substantial experience of overseas expansion, and I am confident in its executional capabilities.

Attractive Valuation

JD has risen 19% over the past year but remains well below its highs.

The P/E ratio of 50 looks high to me. But that partly reflects the adjusting items from last year. With a billion and a half pounds of cash, the market cap suggests an enterprise value beneath £6bn. That is six times the forecast headline pre-tax profits. As a fast-growing business, I expect the financial performance to improve over time. I see JD as a strong buy.

For further details see:

JD Sports: Long-Term Superstar Potential