JDSPY - JD Sports: Strategy Looks On Course

2023-09-25 08:05:58 ET

Summary

- JD Sports' aggressive growth strategy is yielding positive results, with sales and profits growing year-on-year.

- The company is making strategic progress through store expansion and acquisitions, aiming to open over 200 stores worldwide.

- JD Sports has significantly increased its dividend and has a strong balance sheet, making it an attractive investment opportunity.

JD Sports ( JDSPY ) released its interim results last week and I think that, broadly speaking, they demonstrate that the company's aggressive growth strategy adopted this year is already starting to yield positive results.

My last piece on the name was a "strong buy" piece in June ("JD Sports: Long-Term Superstar Potential"), since when the share has lost 16%. I see this as presenting an even better buying opportunity from a long-term investment perspective.

Ongoing Sales Growth

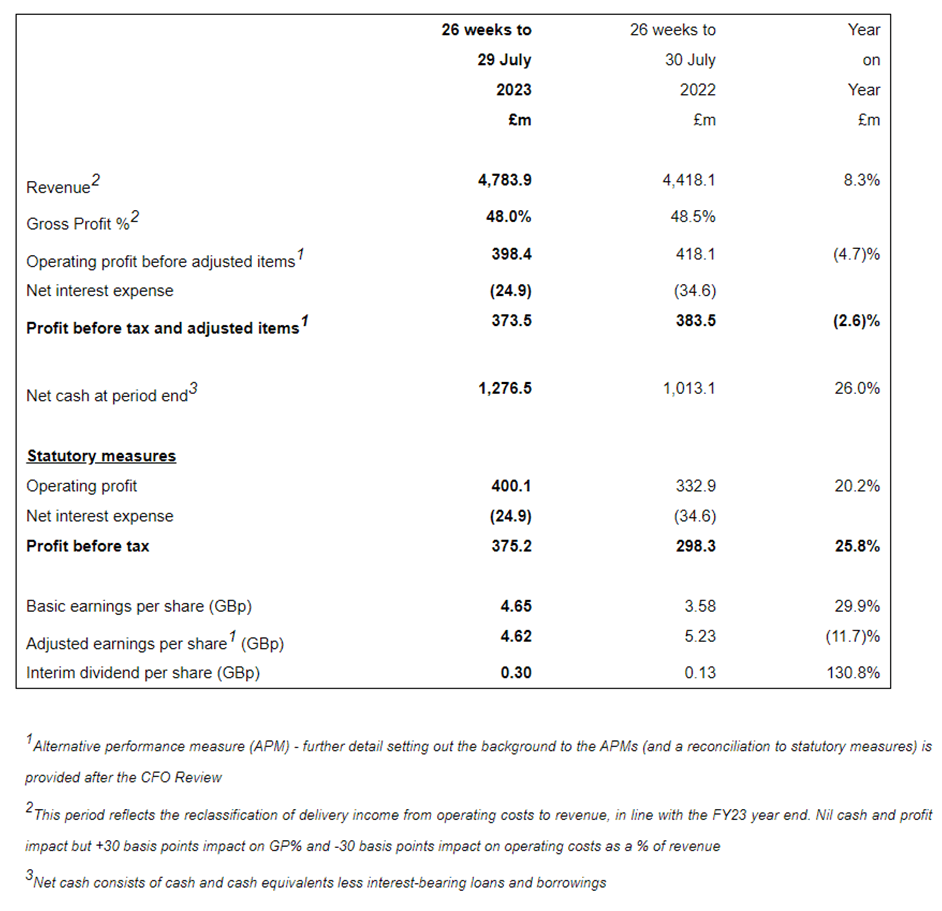

The results showed that first half sales grew year-on-year, by 8.3%. Organic sales growth was 12%. That is a solid performance, though in an inflationary environment, it is not a spectacular one.

Pre-tax profits grew by 25.8% year-on-year. Gross profit margin slipped by 50 basis points, while despite the pre-tax profit increase, it is worth noting that operating profit before adjusting items slipped by 4.7%.

{kind=link}

The company, which does not typically disappoint investors, affirmed that it is on track to meet its full-year profit target. It said this is being driven by strong performance in Europe and North America as a more modest but still strongly positive performance in its more mature U.K. business.

Strategic Progress

My bullishness on the company is driven by ongoing strong performance in its extant business, combined with the additional driver of ambitious growth plans I laid out in my last article.

JD said it is making good progress in delivering on its strategic pillars. It expects to open over 200 stores worldwide in the current financial year. As well as its proposed acquisition of Courir to grow European sales, it also plans to acquire GAP stores in France and buy out minority shareholders in a couple of its European businesses.

Without underestimating the skill of what it does, I see JD as a pleasingly simple business. It has figured out a highly successful business model, both offline and online. Rather than tinkering with that, it is now seeking to grow significantly year after year by rolling out that model through expanding its estate.

Massive Dividend Increase

The company acknowledged in the results that it is highly cash-generative. That could help fuel its large-scale store estate expansion programme as well as possible acquisitions. But it can also fund dividends.

After taking a cautious approach to dividends during the pandemic era (when sales boomed) to give it a sizable cash buffer, the company has now returned to pre-pandemic dividend coverage levels, as it had previously indicated it would.

The interim dividend went up 131% to 0.3p per share. The company indicated that it planned to return to the historical practice of the final dividend equalling double the interim dividend, suggesting a prospective full-year dividend of 0.9p per share.

That equates to a yield of 0.6%. That is still pretty unexciting in my view. However, I see the scale of the increase and the strategic approach to shareholder returns as a positive sign of management intention when it comes to dividends.

Some Risks

I think the store expansion programme could yield great results and am upbeat about its impact on the investment case. That said, many other retailers are closing stores and complaining about a gamut of challenges, ranging from high rent to shoplifting. So JD is going rather against the wider trend here. Setting up hundreds of new stores annually is an expensive business, and if the strategy turns out poorly could saddle the company with costs that eat into profits.

On this, the company made the following interesting observation in the results:

As we accelerate our store opening programme, we will maintain our demanding performance targets for new stores. Sales uplifts from conversions, globally, are 20% while payback on our new JD stores continues to be within three years.

What about consumer spending? After all, if the economy weakens, or we enter a deep recession in the company's key markets, surely expensive logoed hoodies could be seen as a discretionary item a consumer will stop buying? Apparently not, based on what the company has repeatedly communicated about this point and indeed its sales performance.

Specifically, this time around, JD had the following to say:

We are acutely aware of how tough the macro-economic environment is for consumers across the world. Despite this context, assuming current exchange rates, we expect the Group's headline profit before tax and adjusted items for the 53-week period ending 3 February 2024 will be in line with the current market consensus expectations of £1.04 billion.

That is a less clear signal than previously that the company sees little or no big impact on demand from a tough macroeconomic environment. But it seems like the mood music remains broadly unchanged viz. JD recognises the risks inherent in a wider economic slowdown but is not expecting it to affect the business badly, if at all. In itself - if that continues to be true - I think that further demonstrates the strength of the JD business model.

Balance Sheet is Strong

The company reported an improvement in its net cash position of 26% over the past year, to £1.3bn. JD is a cash machine and despite funding its growth strategy and more than doubling its interim dividend, it continues to throw off cash.

I see this strong balance sheet, along with the business' disciplined approach towards expenditure, as further evidence of the attractiveness of the company.

Valuing JD Sports shares

The shares are up 14% this year and 61% over the past five years.

How much is the market capitalisation? It currently stands at £7.6bn. Considering that net cash position, that makes for an enterprise value of £6.3bn. For a business in strong growth mode with a proven and highly profitable model that looks set to generate over £1bn in headline profit before tax and adjusting items this year alone, I regard that as a veritable bargain.

In line with that, I maintain my "strong buy" rating.

For further details see:

JD Sports: Strategy Looks On Course