JDEPF - JDE Peet's: A Coffee Giant At A 8% Free Cash Flow Yield

2023-06-17 11:35:00 ET

Summary

- JDE Peet's is one of the largest coffee distributors in the world.

- The free cash flow remains strong, and I'm not worried about the upcoming jump in the cost of debt.

- Even at a low single-digit EBIT growth (the current guidance), the EBIT growth will neutralize the impact of higher interest rates.

Introduction

As it has been more than eighteen months since I last discussed JDE Peet's (JDEPF) (JDEPY), I think it's time for an update. Surprisingly, the share price has barely moved in those 20 months and the chart below must be one of the more boring share price charts in the universe. That's perhaps surprising as JDE Peet's is still generating very strong cash flows which help to reduce the net debt but perhaps the market is a bit worried about the 4B+ EUR debt pile and the impact of the increasing interest rates on the financial markets on the debt. People continue to drink coffee whether it's at home or at the office, and as JDE Peet's sells coffee in both a B2C and B2B format, the company remains exposed to its consumers no matter how and where they consume their coffee.

{kind=link}

JDE Peet's has its primary listing in Amsterdam where it is trading with JDEP as its ticker symbol . The average daily volume is just over 330,000 shares and that makes Amsterdam the most liquid listing to trade the common shares of JDE. The company reports its financial results in EUR and I will use the Euro as base currency throughout this article.

The 2022 results confirm JDE Peet's is a free cash flow monster

Unfortunately JDE Peet's only provides half-year updates so we will have to wait a bit longer to check up on the company's performance in 2023 so far. But this is a nice opportunity to have a look back at the FY 2022 results and get familiar with the outlook for 2023. This article will mainly look at the company's future, and I'd recommend you to have a look at my previous article to get a better understanding of JDE Peet's business model and historical performances.

The total revenue in 2022 increased by in excess of 15% to 8.15B EUR but unfortunately the COGS increased by in excess of 25% and this obviously didn't really help the reported operating profit. The operating profit, which also includes the SG&A expenses (+10% YoY) fell to 949M EUR but thanks to a net finance income, the pre-tax income jumped to 1.02B EUR while the net income was a very robust 761M EUR.

{kind=link}

This included a 10M EUR net loss attributable to non-controlling interests and the net income attributable to the shareholders of JDE Peet's was 771M EUR or 1.57 EUR per share (based on the 491M shares outstanding).

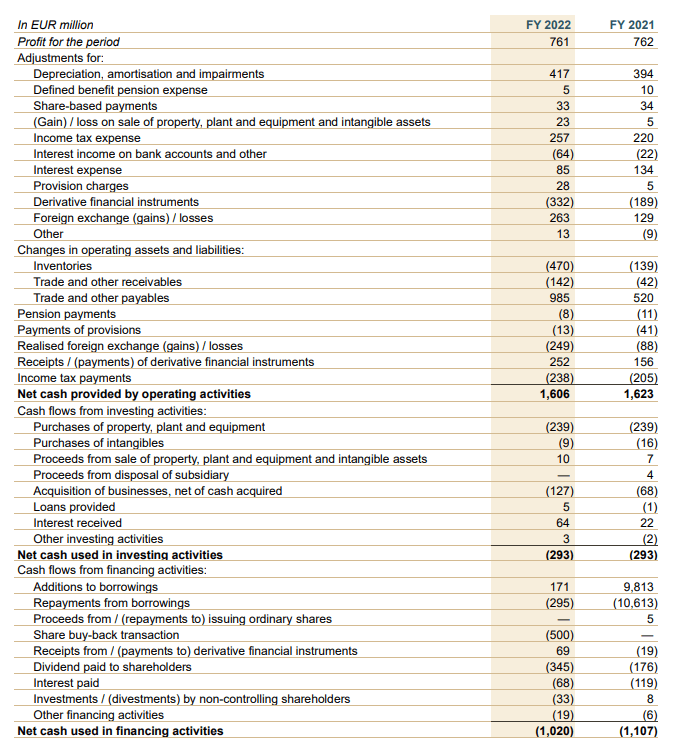

The cash flow was even stronger as the total capex is substantially lower than the depreciation and amortization expenses. The total reported operating cash flow was 1.61B EUR but this includes a contribution of approximately 373M EUR from changes in the working capital position. We also should add back the 64M EUR in interest income but deduct the 19M EUR in difference between taxes owed and taxes paid in FY 2022.

{kind=link}

This means the adjusted operating cash flow was approximately 1.3B EUR and after deducting the 250M EUR in capex, the underlying free cash flow was 1.05B EUR before changes in the working capital. As there are 491M shares outstanding, the free cash flow result was approximately 2.13 EUR per share which means the stock is currently trading at a free cash flow yield of almost 8%.

The stock will trade on an ex-dividend basis on July 10 as a 0.35 EUR dividend will be removed from the shares.

Although the company has a lot of debt, the increasing interest rates aren't something I worry about

Given the "sticky" nature of the consumer items (consumers continue to buy coffee and tend to stick with a brand they like) I would actually expect the stock to trade at a premium valuation. Some were pointing at the increasing coffee prices to justify a more conservative stance but the company explained that its recent price hikes would have a very minimal net impact for the end user as it estimates the price hikes will increase the cost by just 5 EUR per year.

{kind=link}

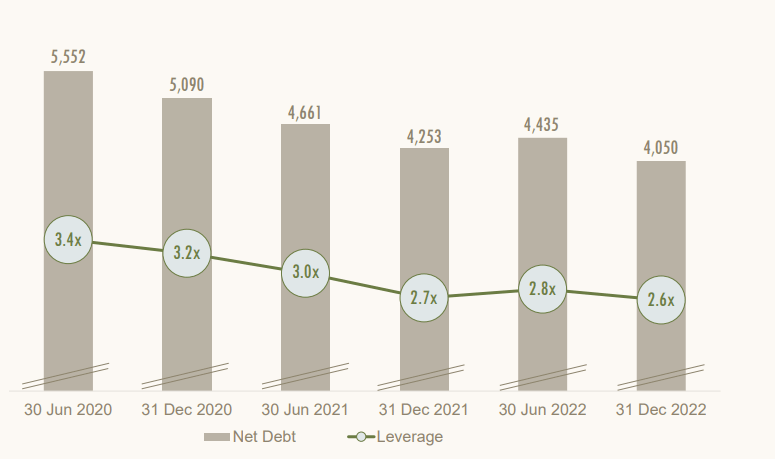

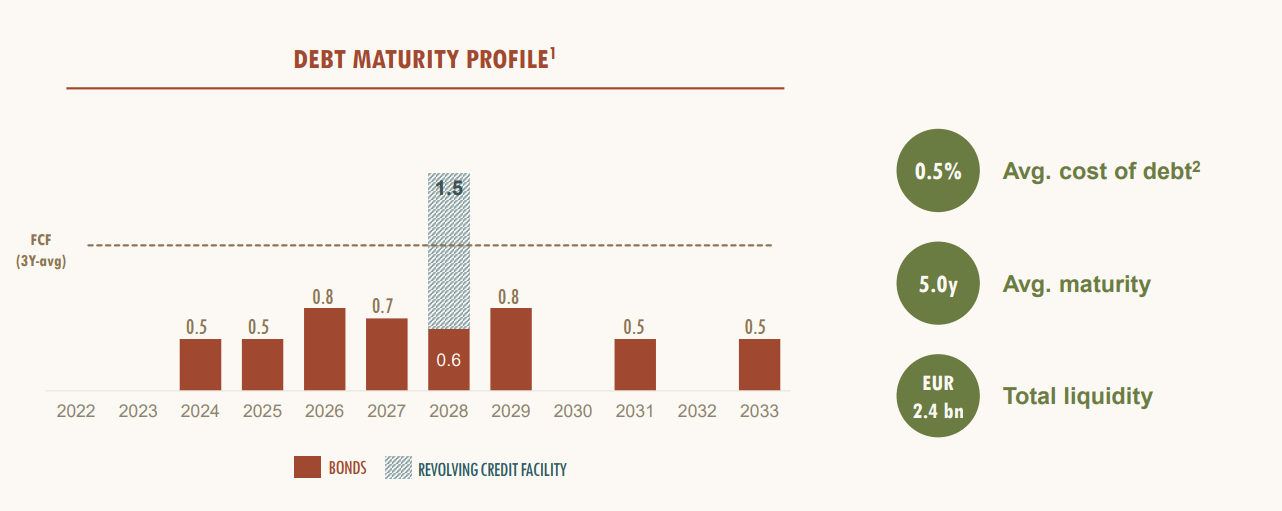

The only other reason I can think of to explain the relative weakness is the relatively high gross debt and net debt level at JDE Peet. The image below shows the company has done a good job to reduce the net debt and the leverage ratio.

{kind=link}

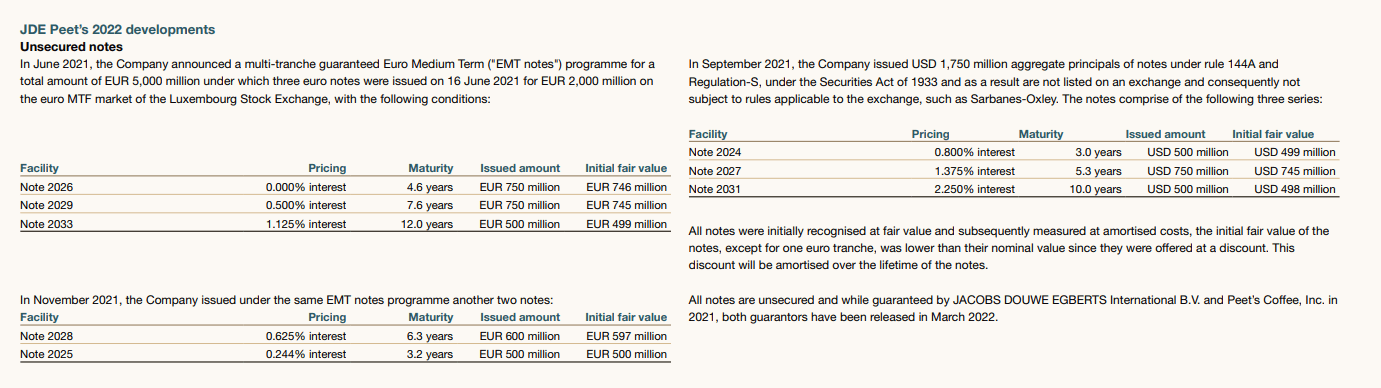

But a declining net debt obviously doesn't mean JDE won't be hit by the increasing interest rates. The image below provides a breakdown of the outstanding debt. JDE Peet's bonds all have a fixed interest rate and the first ones to mature are the $500M 0.80% note in 2024 and the 500M EUR 0.244% note in 2025.

{kind=link}

If we would assume the cost of debt will increase by 450 bp for the USD bond and by 350 bp for the EUR note, the total interest expenses will increase by approximately 40M EUR and the after-tax free cash flow would decrease by around 30-32M EUR. Which means that applying market rates for debt refinancings between now and 2026, JDE Peet's will only see its free cash flow decrease by 3%.

And considering the company is guiding for low single-digit EBIT increases for the next few years, the anticipated EBIT increases will take care of the impact of the higher interest expenses on all debt refinancings in the next three years.

Of course the road could be quite bumpy, but in general, I expect JDE Peet's to be able to compensate the higher interest expenses by increasing its EBIT (while it could also decide to retain more cash and reduce the total debt outstanding). And it doesn't need much for that.

{kind=link}

Even if you would apply a 500 bp increase across the entire debt pile, we're talking in just about 250M EUR in additional interest expenses, of which 10-15% would only materialize in the 2030s. I have very little doubt JDE Peet's can grow its EBIT result faster than the higher interest rates are kicking in.

According to the analyst estimates , the median EBIT expectation for 2025 already is 180M EUR higher than the median for 2023. So rather than seeing the earnings and free cash flow decrease due to higher interest expenses, I still think JDE Peet's will be able to continue to increase its net income and free cash flow.

Investment thesis

JDE Peet's share price has been pretty disappointing. Back in October 2021, when my previous article was published , the stock was trading at 25.30 EUR, and as the current share price is just 27.20 EUR, the stock is up by just 7.5%. The company also paid out 1.05 EUR per share in dividends which means the absolute total return was 11.6% or roughly 7% on an annualized basis. Despite that being a strong outperformance versus the negative 3% return on the S&P 500, I am somewhat disappointed in the share price.

But this also creates a new opportunity for me to finally obtain a long position. The past eighteen months I have continued to write out of the money put options on JDE Peet's in an attempt to get the stock at a lower price. But as the Implied Volatility has strongly decreased to low double-digit percentage, the option premiums are now too low to bother anymore.

JDE Peet's spent 845M EUR on shareholder rewards in FY 2022 which included a 500M EUR share buyback program which reduced the share count to 485M shares (compared to the weighted average of 491M EUR which I used for the EPS and FCFPS calculations). I'm very confident JDEP will be able to keep its adjusted free cash flow per share above 2.00 EUR and it will likely see its FCFPS grow towards 2.30-2.40 EUR per share by 2025 despite the upcoming debt refinancings.

I currently don't have a position in JDE Peet's, but I will likely start building a long position.

For further details see:

JDE Peet's: A Coffee Giant At A 8% Free Cash Flow Yield