SBUX - JDE Peet's: Not Doing Well And Down 30% For A Reason

2023-09-13 08:25:01 ET

Summary

- Jacobs Douwe Egberts (JDE) Peet's stock has dropped by about 40% since its IPO in 2020.

- The company is trading around fair value in a best-case scenario, but appears overvalued if a recovery does not materialize.

- JDE Peet's is losing market share to competitors, has significant debt, and trades at a valuation that is not attractive. Hold recommendation.

JDE Peet's (JDEPF), has gone down by about 40% since its IPO in 2020. Despite the share price falling so much since IPO, we believe the company is still not cheap enough to be a good investment.

JDEP share price since IPO (Google Finance, 2023)

{kind=link}

Most importantly, we find that the company is losing to its competitors in its key markets, decreasing margins, and that it carries a large debt load. We conclude that the company is trading around fair value in our best case scenario, accounting for a strong recovery play in 2024. In the case where this recovery does not materialize, the company appears considerably overvalued.

We therefore provide a hold recommendation, waiting for better entry points such as 15 Euros per share to get a larger margin of safety.

Company overview

The company is primarily a coffee business, accounting for over 80% of its revenue. JDE Peet's sells coffee to consumers in the form of packaged goods in supermarkets, and it owns café's to sell coffee out-of-home to consumers. The company also sells coffee B2B as a supplier to restaurants and businesses to keep their staff productive on high doses of caffeine. Additionally, JDE Peet's owns tea brands (Pickwick) and sells food in their café's, which accounts for around 15% of revenue.

The company is one of the largest players in the coffee business, with operations all over the world. The company has Jacobs, L'OR, Senseo, and Douwe Egberts which are relatively popular brands in Europe. The company is also active in emerging markets such as China and Latin America, where they are growing with higher rates than in Europe.

In the US, the company owns Peet's which is an artisanal coffee business similar to Starbucks (SBUX). Peet's has a very loyal customer base, calling themselves " Peetnicks ". However, Peet's is much smaller in size than Starbucks and other competitors selling coffee on-the-go, such as Dunkin' Donuts (privately owned).

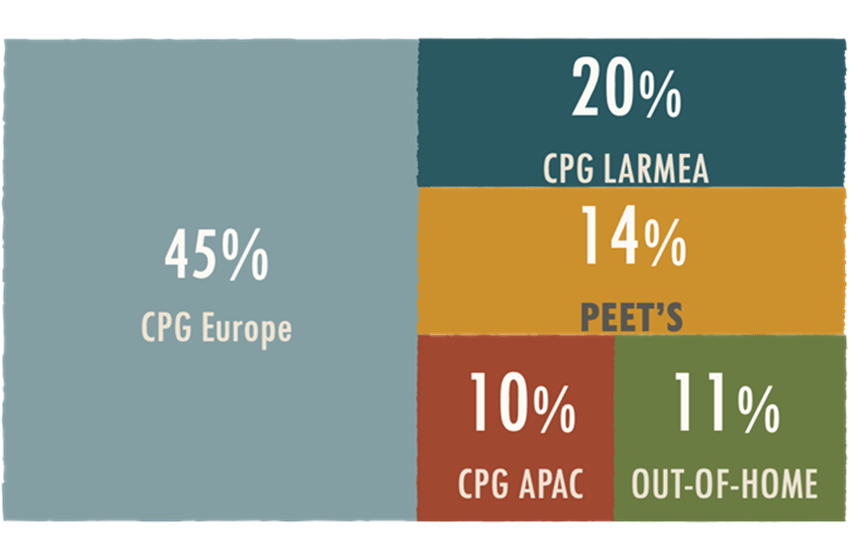

Revenue split by region (JDEP, 2023)

{kind=link}

Recent developments

The CEO made some strange remarks about Russia. Despite strong political pressures in Europe, the company still operates in Russia with its Jacobs brand and refuses to leave . Russia accounts for a considerable amount of their LARMEA region revenue, and it is one of the few areas with strong growing profits . While profitable, the activities in Russia present a risk to the company, but it is not disclosed how large their position exactly is there. Their stance on Russia is bad press for the business. The Dutch Government, a big customer of JDE Peet's, threatened to break its supply contract with JDE Peet's over this controversy.

On a more positive note, JDE Peet's announced that it has acquired Maratá. This company is a Brazilian Coffee & Tea producer and market leader in Brazil. The acquisition could help to spur some growth into JDE Peet's portfolio of brands in emerging markets. Maratá reported over BRL 1.1 billion annual sales on average in the last 3 years. The acquisition will be completed in FY2024, further details of this deal were not disclosed.

Competitors

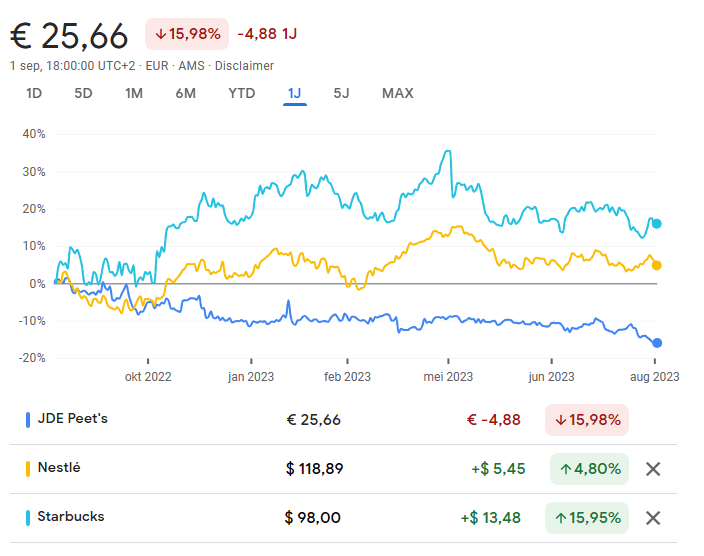

Given the mature nature of the coffee market, there is a lot of competition. JDE Peet's share price has underperformed its largest competitors. Is JDE Peet's undervalued or is this underperformance justifiable?

Stock prices over the past year vs. Competitors (Google Finance, 2023)

{kind=link}

Starbucks : In the out-of-home (OOH) segment, JDE Peet's is competing against big players such as Starbucks and Dunkin' Donuts. Starbucks in particular is the largest pure coffee company by market cap; their market cap (110 billion USD) is about 10 times larger than JDE Peet's (12 Billion Euros). With good reason, Starbucks dominates the US market with almost 60% market share , followed by Dunkin with a 20% share, Peet's makes up just 0.8%.

Market share in the US (Euromonitor, 2022)

Nestlé: In the consumer packaged goods ((CPG)) segment, JDE Peet's is competing against large international players. Most notably Nestlé, which owns brands such as Nespresso and Nescafé. Compared to JDE Peet's, Nestlé has a larger market share and better financial performance for its coffee segment at 4.5% organic growth versus JDE Peet's 3.5%. Nestlé also made a smart 7 billion USD deal with Starbucks back in 2018 for the permanent right to sell Starbucks' branded coffee as packaged goods in supermarkets and so on. Thereby increasing its market share and consolidating its strong position.

JDE Peet's is kind of stuck in the middle here. Their brands are not as strong as Nespresso and Starbucks, but they are significantly more expensive than store brands (private label). As a result, JDE Peet's is losing market share to Nestlé and their other competitors. The CEO admitted this fact in the earnings call :

On this page, you can, in a very transparent way, see JDE Peet's' market share evolution per geography on the left side, and per category on the right side. We have been losing share in Europe, on the back of retaliations in H2 of last year, that we are slowly rebuilding, but is not yet completed.

Losing market share in developed markets (JDEP presentation HY2023)

The company has responded by investing more into marketing to re-gain their market share, and their long-term strategy is to focus on emerging markets such as China and Latin America. Time will tell if this turns out well for them, but for now the company is losing to its competitors in its key markets. They are growing in emerging markets, as the CEO pointed out in the earnings call :

But in parallel, our strategic acceleration in the US, in APAC and in LARMEA is more than compensating the share loss in Europe. Not only we did grow more than in Europe in these regions, but as well outperformed competition there. ...

We mentioned in the past that Greater China has the potential to be one of the top five largest markets for JDE Peet's. In that journey, H1 marked a nice milestone, with Greater China joining the top 10 markets for the first time of JDE Peet's in revenue.

Financials

FY2022 had nice results, but the current year (FY2023) is not going well for JDE Peet's. The company looks cheap based on these backward-looking ratios such as P/E using last years' earnings, but this year profits are a lot lower and the market is always forward-looking.

This year, net earnings and free cash flow have almost disappeared. The CEO played this off as "post-covid normalization", which simply seems like a bad excuse to me. This large drop requires more explanation.

For FY2023, the company is projecting FCF numbers of 400 million Euros, which is a 70% drop compared to FY2022 when they achieved 1,358 million Euros in FCF. The reason for this big drop included rising input costs such as coffee bean prices, and labour costs. Because some of these inflationary pressures are subsiding, JDE Peet's margins could recover to historical averages.

Coffee prices in USD cent per pound (Trading Economics, 2023)

{kind=link}

However, JDE Peet's competitors have also struggled with these issues, but they achieved better performance. As noted before, Nestle reported higher growth for its coffee segment in the same period. Similarly, the biggest coffee roaster in the US by market share, Keurig Dr. Pepper, reported high single digit earnings growth due to their more diversified portfolio of products. However, their coffee segment also suffered decreasing net sales and profits. That being said, JDE Peet's is a higher risk "pure play" with more expose to coffee prices.

Net debt position over time (JDEP, HY 2023 Presentation)

{kind=link}

The company holds a significant amount of debt, more specifically, 4.2 billion Euros in net debt. They have been paying it down over recent years, and they target a net debt ratio of 2.5 times EBITDA. They intend to achieve that next year, before they're able to do buybacks and increase the dividends. As a result, Fitch has upgraded JDE Peet's credit rating to BBB.

JDEP debt (JDEP debt info, 2023)

It is positive that the company is paying down this debt, but it is a big burden because it needs to be paid back and there are increasing interest payments. There is 500 million Euros of debt due both in 2024 and in 2025 . Moreover, this large amount of debt will have to be refinanced later at a higher interest rate, which will have a large and negative impact on their net profits.

DCF valuation

We provide three scenarios: one using the current FY2023 results and forward guidance of the company, and one pricing in a recovery play in FY2024. Finally, we use the historical average 1bn FCF, to account for working capital changes.

The company provided guidance of 400 million in Free Cash Flow for FY2023 with 3-5% organic growth. Using this guidance of 400 million FCF and growing at 3-5% for the next ten years, we come to an intrinsic value of just 13 euros of a share, meaning that the company is overvalued at 25 euros a share.

In our more realistic scenario, we are estimating a recovery next year back to the historical average of 1 billion Euro in FCF and 3.5% growth thereafter. We come to an intrinsic value of 20 euros per share, which is 20% less than the current market cap. If this recovery back to historical averages does not materialize, the company is massively overvalued.

Finally, using the historical average of 1 billion in FCF, because of working capital changes, and growing this at the guided 3-5% range. We come to an intrinsic value of about 30 euros a share, represent a small upside of 20%.

In all cases, the margin of safety is not large enoug h to warrant such an investment, in my opinion. In the best case with stable FCF of 1bn annually, we still only have a small upside and it is unclear if this assumption is valid. Using the guidance of the company for 400m FCF this year, the company looks slightly overvalued. We target a 15 euros margin of safety buying price.

Conclusion

The company is performing relatively poorly compared to its competitors, it's losing market share, and it trades at a valuation that is not very attractive. To achieve a good margin of safety, the company is too expensive, and the share price should come down to about 10-15 euros a share.

The competition has outperformed JDE Peet's both in terms of stock price and business performance. JDE Peet's has lost market share across key markets in the US and the EU. Moreover, JDE Peet's is investing in emerging markets, which could be a good long-term strategy. However, this adds significant risks to its portfolio, with exposure to countries such as Russia and China. All in all, the 30% drop from its IPO price in 2020 therefore seems like a reasonable drop, instead of simply a strong undervaluation and good buying opportunity.

In conclusion, we provide a hold recommendation for this business. Although the business performance is not great, we will follow the company, and we would be interested at a lower entry point such as 15 Euros per share.

For further details see:

JDE Peet's: Not Doing Well And Down 30% For A Reason