MDLZ - JDE Peet's NV: A True Comeback Story

Summary

- JDE Peet's is the world's leading pure-play coffee & tea company.

- JDE Peet's has a global presence serving +100 markets with several strong brands across the coffee industry.

- JDE Peet's is a well-run company with an outstanding management team and shareholder group.

Business Overview and Investment Thesis

JDE Peet 's NV (JDEPF) is the world 's leading pure-play coffee & tea company. The company serves customers and consumers with coffee & tea in more than 100 markets through a portfolio of over 50 brands, including L 'OR, Peet 's, Jacobs, Senseo, Tassimo, Douwe Egberts, etc. JDE Peet 's is well run with an outstanding management team and a dominant position in a stable industry.

The company had its comeback to the public markets in 2020 when it had its IPO recording a market capitalization of €15.6 billion on the day of listing. Despite having a lower market capitalization today and possessing even better-looking financials than back in 2020, I believe it is advisable to wait for a more attractive entry point before investing. My main reason for this stance is the fact that JDE Peet 's does have to repay on average €650 million in debt for the next 6 years. This will constrain the company to pursue growth opportunities through bolt on acquisitions, increase dividends or put in place a share buyback program. Let 's take a deeper looking into the company 's history.

The Comeback Story

JDE Peet 's is the story of an outstanding management team coupled with a robust financial support system. What I mean by this is that the debt capital markets along with financial institutions gave the company the necessary tools to have more leeway despite its highly leveraged position. Before discussing this, I will first do a quick recap of what happened over the last decade. Peet 's was bought by JAB Holding in 2012 for approx. $1 billion. JAB Holding would then buy Douwe Egberts for ten times that amount in 2013. For reference JAB Holding is an investment firm holding investments in coffee and beverage, fast casual restaurants, pet care, and other industries.

For various years JAB expanded both companies ' global presence until 2019, when it decided to merge both companies and create the biggest pure-play coffee & tea company in the world. Just a few months later in 2020, JDE Peet 's announced that it would once again go public. The company raised €2.25 billion through its IPO, using part of the proceeds to repay debts. The company was highly leveraged at the time, and management had a clear goal. Deleverage the company and do it fast! To get an understanding of the amount of debt JDE Peet 's held at that moment, we could compare the company 's revenues and debt position during 2019. At the end of 2019 the company held a debt position totaling €7.3 billion while revenues generated stood €6.9 billion. Furthermore, finance expenses depressed the company 's net profits by €302 million which equated to over 50% of the total net profits of €585 million.

Management deleveraged the company efficiently through a strategic use of various financial instruments such as term loans, supply chain finance facilities, revolving credit facilities and the issuance of bonds in the capital markets. This financial support system allowed management to optimize the capital structure of the company while at the same time mitigating the impact of its highly leveraged position.

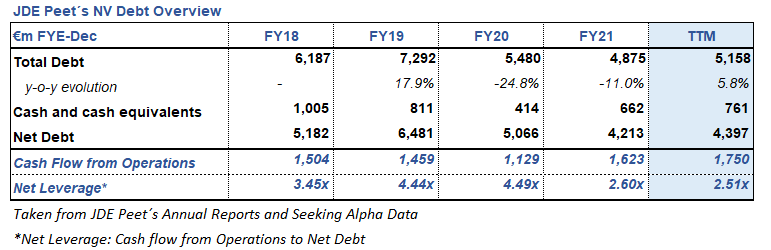

The result was nothing but spectacular, since 2019 the company has decreased its total debt position by over €2 billion. Going from a net leverage position (net debt / cash flow from operations) of 4.4x to 2.5x during the most recent results.

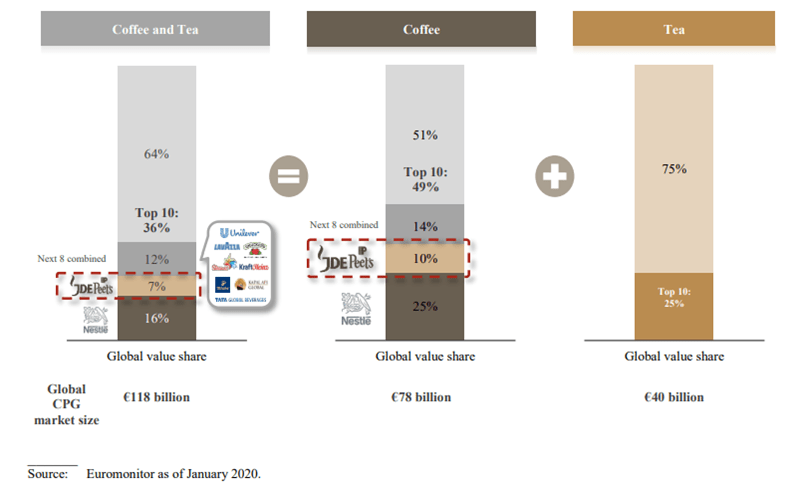

Industry at a Glance

Please take into consideration that the graph below is from 2020, however it should also be noted that the coffee and tea industries do not see much fluctuations year on year. It is clear that the $78 billion coffee market is dominated by 10 companies holding about 50% of the global market value. As for tea market, this number stands at 25%. JDE Peet 's competes in these markets with well known and established companies such as Nestle (NSRGY), Unilever (UL), Kraft Heinz (KHC), etc.

Furthermore, it can be appreciated that both industries are dominated mainly be European and North American companies. This is because these companies are able to have presence in the biggest markets for coffee. For example, Europe consumes on average about 3 million tons of coffee every year. At the same time the combined North America and Latin American regions consume approx. 3.8 million tons of coffee every year.

Coffee and Tea Market Valuation (Euromonitor & JDE Peet´s IPO Prospectus)

{kind=link}

Financial Overview

JDE Peet´s Financial Highlights (Company´s Annual Reports)

As previously mentioned, JDE Peet 's is the world 's leading pure-play coffee & tea company. The company operates in over 100 markets with a strong presence in Europe with a growing presence in North and South America. During the trailing twelve months revenues stood at €7.6 billion, cash flow from operations of €1.75 billion, and free cash flow at €1.5 billion. This performance indicates an improvement compared to FYE 2021.

During 2021, JDE Peet 's generated revenues of €7 billion through its 5 segments consisting of CPG Europe, CPG LARMEA, CPG APAC, Out-of-Home and Peet 's. The segments are organized based on the reporting structure (by the geographies and/or the nature of the products and services) of JDE Peet 's. CPG Europe is the company´s top revenue generating segment. This should not be a surprise as Europe as a continent typically consumes about 3 million tons of coffee each year. It should also be mentioned that 78% of revenue came from 43 markets where JDE Peet 's holds the #1 or #2 position in CPG and Out-of-Home.

The company holds a strong liquidity position, which currently stands at €2.3 billion, consisting of cash and cash equivalents of €761 million and a €1.5 billion committed revolving credit facility. The reason for this strong liquidity position is the fact that JDE Peet 's still has a relatively high debt position of €5.2 billion. As it will be seen later, management has been doing a great job deleveraging the company.

Shareholder Returns

JDE Peet´s Shareholder Returns (Company Annual Reports)

JDE Peet 's has consistently increased shareholder returns during the past 4 years. Management approved a dividend of €0.70 per share in 2021 and during the first half of 2022 it bought back shares from the share percentage owned by Mondelez International ( MDLZ ).

Management has stated that it will prioritize stable dividends over share repurchases while its leverage is above its optimal level of 2.5x. So, investors should not expect a share buyback program in the coming months.

Achieving Optimal Leverage and Comfortable Debt Maturity Profile

JDE Peet´s Debt Overview (Company Annual Reports and IPO Prospectus)

{kind=link}

Since 2019 JDE Peet 's has paid down about €2.1 billion in debt. This has allowed the company to achieve a net leverage position of 2.5x. Please note I am using a different net leverage formula than what the company uses. I am using cash flow from operations instead of Adjusted EBITDA as I believe we should always focus on the actual cash flow the company brings in. The company actually reported a net leverage position of 2.8x in its latest financial report. The company did pay €500 million to buy back shares from its shareholder Mondelez International. Payments like this are not expected to keep happening.

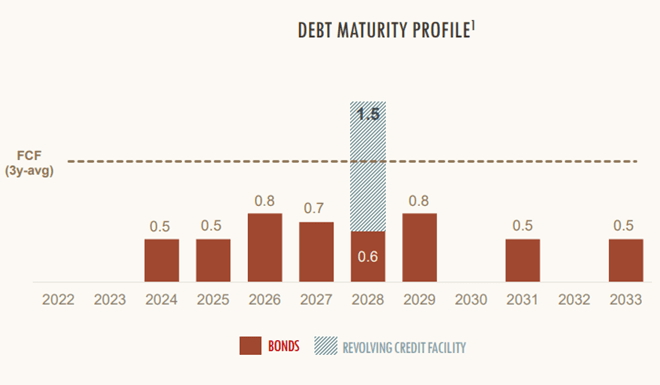

Management was able to spread out the bond repayments throughout a decade. Something truly impressive to highlight here is the fact that the €750 million bonds due in 2026 and 2029 have a rate of 0% and 0.5%, respectively. Talk about free money! Additionally, management armed the company with €1.5 billion committed revolving credit facility.

JDE Peet´s Bond Issuances (Company Investor Presentation)

Despite JDE Peet 's having a well spread-out debt maturity profile, it 's important to note the company will have to pay an average €650 million during the next six years. Let 's then put the cash flow from operations against the cash outflows the company will have. If we assume cash flow from operations will average about €1.5 billion per year and capital expenditures of about €250 to 300 million, this leads to a free cash flow of approx. €1.2 billion. With the current dividend per share, we have a dividend payment of approx. €350 million. Finally, JDE Peet 's will need to pay on average €650 million on debt repayments for the next six years. Taking these cash outflows into consideration we end up with a remaining cash of approx. €200 million.

This remaining cash flow can be used for bolt on acquisitions, increase of dividends, share buybacks, or pay down debt even further. From these calculations it can be appreciated that JDE Peet 's will be somewhat constrained in the coming years.

JDE Peet´s Debt Maturity Profile (Company Investor Presentation)

{kind=link}

Valuation

With the current market valuation at €14 billion, I believe the company is well priced. At the current share price, the dividend yield is ~2.3% with the opportunity to grow constrained by debt repayments. I believe there are other companies offering a more attractive dividend yield with a robust business model to keep delivering stable and growing dividends.

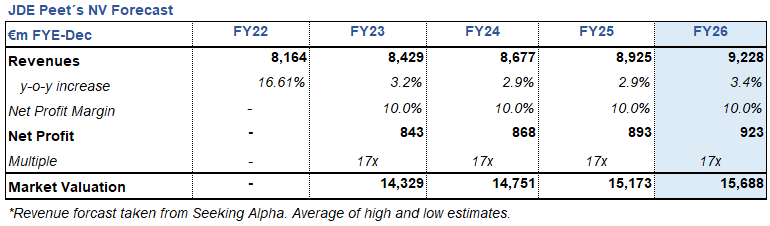

For the valuation of the company, I have used the market multiple method, using future forecasted earnings to a 17x multiple. This is a high multiple, but due to the company 's dominant position in the coffee and tea industries I believe it is reasonable. I have obtained analysts ' revenues forecast from Seeking Alpha data and have applied a net profit margin of 10% due to the continued financial improvements seen during the previous years. I arrive at a market valuation of €15.7 billion by FYE 2026.

{kind=link}

Risks

Commodity price risk: Given coffee is a commodity, it is subject to fluctuations due to inflation, larger than expected crops, smaller than expected crops, natural disasters, etc. As such JDE Peet 's is subject to fluctuations in coffee prices, which can impact their profitability.

Currency risk: As a result of operating in over 100 markets JDE Peet 's is exposed to currency fluctuations, this can have an impact in the company 's bottom line. This risk is mitigated by the knowhow management has and risk mitigant strategies they implement.

Supply chain risk: Given coffee as a crop is not present in Europe or North America, JDE Peet 's must rely on a complex supply chain process the coffee through the whole value chain. This mean the complexity of the supply chain is quite high, any and disruptions here can impact the company 's ability to serve customers.

Bottom Line

In conclusion, JDE Peet 's is well-positioned to remain the world 's leading pure-play coffee & tea company. The company had its comeback to the public markets in 2020 and has been able to deleverage in a steady manner since then. Further, management has found attractive funding opportunities in the capital markets with some bond rates at 0% or 0.5%. This is pretty much free money. Management has positioned the company well to keep deleveraging and achieve its optimal net leverage position of 2.5x. Despite this, JDE Peet 's does have to repay on average €650 million in debt for the next 6 years. Of course, the company can refinance and extend bond maturities, however management has not been vocal about this. As such with the combination of capital expenditures, dividend payments and debt repayments, the company will have extensive cash outflows during the upcoming years.

I do believe this is a great company, well run by an outstanding management and shareholder group. Saying this I believe it is advisable to wait for a more attractive entry point or until debt has been reduced to a greater extent.

For further details see:

JDE Peet's NV: A True Comeback Story