PDO - JEPI: 2 Better Long-Term Big Yields

Summary

- If you love income and hate volatility, JEPI is hard to ignore.

- But if you want to maximize long-term income and total returns, JEPI should be totally avoided.

- We review JEPI's strategy and offer our opinion on who should (and who should NOT) consider investing.

- We share two alternative long-term big-yield opportunities that are far superior to JEPI (and it's not even close!).

At first look, the JPMorgan Equity Premium Income ETF (JEPI) appears to be an income investor's dream. It offers a very high current yield (11.8%, paid monthly) and it has significantly less volatility than the stock market (as measured by the S&P 500 ( SPY )). However, a look under the hood reveals JEPI is not exactly what a lot of investors think it is. In fact, its yield is positioned to decline significantly, and it will almost certainly underperform the S&P 500 dramatically over the long term. In this report, we review the JEPI details, share our opinion on who should (and who should NOT) consider investing, and then offer two far superior long-term big-yield investment opportunities.

JEPI Overview:

{kind=link}

Per the fund's summary prospectus , JEPI is:

"designed to provide investors with performance that captures a majority of the returns associated with the S&P 500 Index, while exposing investors to lower volatility than the S&P 500 Index and also providing incremental income."

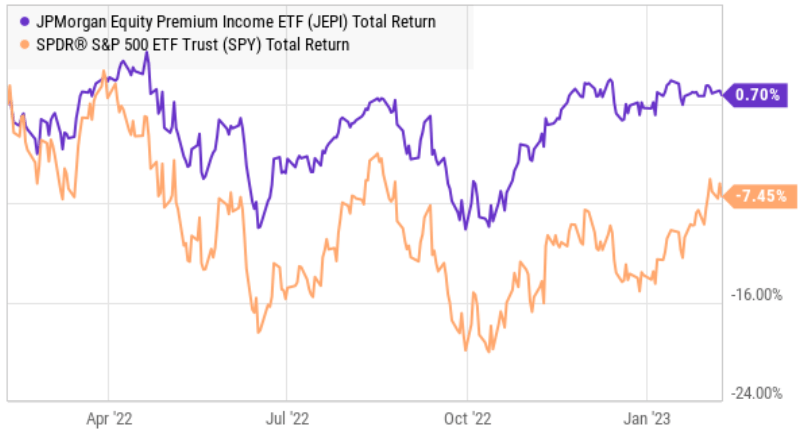

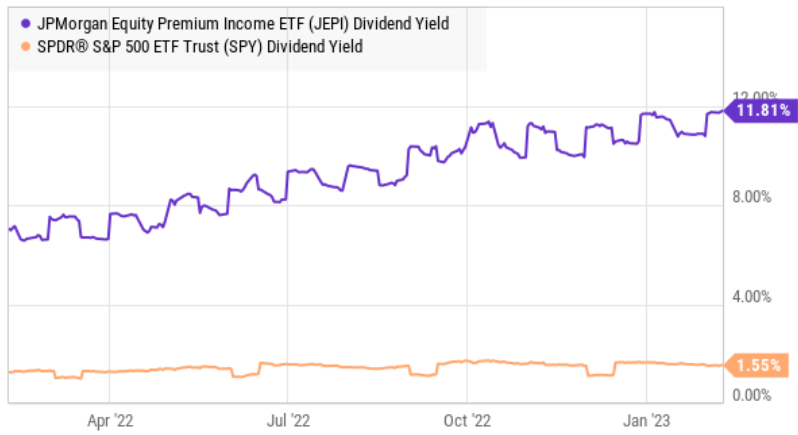

That sounds like a good thing, and the fund has recently delivered with flying colors as you can see in the following charts (i.e. it's recently beaten the S&P 500 and delivers a dramatically bigger dividend yield).

{kind=link}

{kind=link}

For a little more color, JEPI invests at least 80% of assets in stocks (mainly selected from the S&P 500) while also investing in equity-linked notes ("ELNs") to employ a covered call option strategy which enhances income and lowers volatility (more on covered calls later in this report).

Further, JEPI uses an active stock selection process relying heavily on JP Morgan's research to select attractive individual stocks (typically 90 to 120 positions) mostly from the S&P 500. Further still, the fund over weights (versus the S&P 500) more defensive sectors of the economy, such as Utilities, Staples and Healthcare. Its largest holdings includes companies you likely know and trust, such as UnitedHealth Group ( UNH ), Coca-Cola ( KO ) and Honeywell ( HON ).

Overall, JEPI's fund manager expects the fund to have about 35% less price volatility than the S&P 500 (something that can be very attractive to income-focused investors). Again, this is accomplished through stock selection and the covered call strategy employed by the fund.

JEPI's Covered Call Strategy:

JEPI pursues its covered call options strategy by purchasing equity-linked notes (ELNs) which "combine equity exposure with call options." JEPI uses ELNs (instead of writing its own covered calls) because option premium income is not considered bona fide income (it's considered a gain and/or return of capital), whereas ELNs count as income thereby allowing the fund to produce its very high "dividend" yield. Other covered call strategy funds (that actually use covered calls instead of ELNs) generally report much lower yields, even though the income is similar (although taxed differently-more on this later).

If you don't know, a covered call strategy is basically the most conservative options trading strategy whereby you collect upfront premium income by selling an out-of-the-money call option on shares you already own. For example, if Apple trades at $150, you may sell a covered call option with a strike price of $160 thereby giving someone else the option to call Apple shares away from you at $160 even if the share price rises to $170 (thereby giving you some share price appreciation potential, but capping that upside gain potential in exchange for the upfront option premium income you received). Essentially, the covered call strategy limits your upside potential in exchange for upfront premium income. The strategy also helps in down markets (like 2022) because your account value won't fall as far because you will keep collecting that upfront option premium income (as long as you keep writing new call options).

Volatility Matters:

One of the brilliant things about JEPI is that it makes more income when the markets are volatile because options premium income goes up when volatility increases (like it did in 2022) because people are scared and willing to pay more to compensate for the increased uncertainty protection. To put that in perspective, 2022 was a really good income year for JEPI because volatility was high (see JEPI's dividend yield chart earlier), but in a more typical year the fund managers expect the dividend to be in the high single digits-not the 11.8% yield we see currently.

So again, the brilliant thing about JEPI is that it offered a low volatility strategy (the fund typically has 35% less price volatility than the S&P 500) at a time when market volatility was up (i.e. 2022) and it also offered a bigger-than-normal dividend yield at exactly the same time. For many investors, this exactly meets their needs: Less volatility and more income--especially when the market goes down!

JEPI's Long-Term Returns Will Lag:

JEPI gives away significant long-term return potential (as compared to the S&P 500) by employing an options strategy that increases income and reduces volatility. In a down market, this is great (because you are avoiding some of the price declines). But in the long-term, the market tends to go up (and we believe it will continue to go up significantly in the long-term based on the incredible strength of the US and economy), therefore you're giving away a lot of long-term upside return potential (as we'll explain with the chart below).

{kind=link}

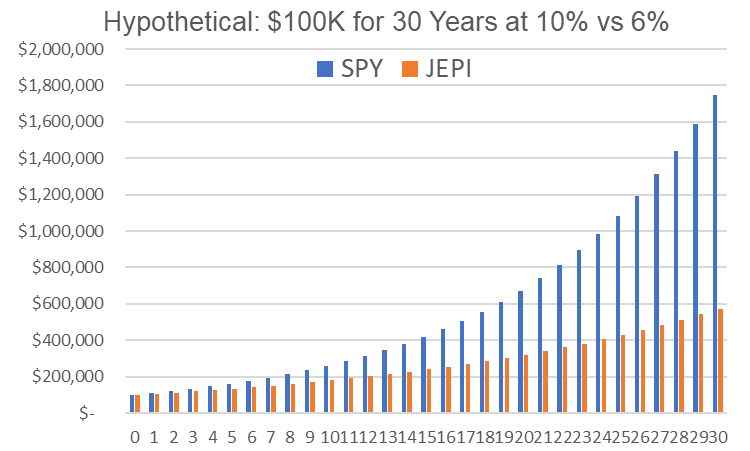

On one hand, you may think 35% less price volatility versus the S&P 500 ( SPY ) is not a big deal, but over the long-term you will miss out on dramatic compounding of returns. For example, if you invest $100,000 in the S&P 500 and it gains 10% per year for the next 30 years, versus $100,000 in JEPI, JEPI may only gain 6.0% per year over the same time period (after the 35% volatility reduction, fees and trading costs--more on this in a moment). You will have essentially given away over $1.1 million dollars in returns for yourself and/or your heirs.

On the other hand, if you're goal is simply high income payments with less volatility, then you still may be 100% comfortable owning JEPI. Just know that the dividend yield is likely to shrink (as volatility falls), your opportunity cost will be very large, and some investment banker behind the scenes is profiting by writing those ELNs and arbitraging massive profits off your strong aversion (perhaps too strong) to short-term market volatility. Again, you may be totally fine with this.

More JEPI Costs and Expenses:

Expenses and High Portfolio Turnover : The total expense ratio on JEPI is 0.35%-mostly reasonable for an ETF, but absolutely a detractor from your total returns as an investor. What's more, the fund has a very high turnover ratio (recently 195%) which can add significant hidden and implicit trading costs that are not included in the total expense ratio. Here is how JEPI describes it in their summary prospectus :

"The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund's performance. During the Fund's most recent fiscal year, the Fund's portfolio turnover rate was 195% of the average value of its portfolio."

Taxes : Taxes are another important consideration. As you can see in the chart below, after-tax returns for JEPI have been significantly lower than before-tax returns (and all that high trading described earlier makes things worse).

JEPI Summary Prospectus

Here is one way JEPI describes taxes in its summary prospectus (with regards to taxable and non-taxable accounts):

To the extent the Fund makes distributions, those distributions will be taxed as ordinary income or capital gains, except when your investment is in an IRA, 401(k) plan or other tax- advantaged investment plan, in which case you may be subject to federal income tax upon withdrawal from the tax-advantaged investment plan.

ESG Considerations : As part of its investment process, JEPI seeks to assess the impact of environmental, social and governance ("ESG") factors on many issuers in the universe in which the Fund invests. To some investors this is a good thing; to others it is a distraction. Like other strategies, ESG investing goes in and out of favor. For example, it was very popular a couple years ago when JEPI was launched, but is falling out of favor with some investors (as some US states continue to sue large investment managers , such as BlackRock ( BLK ) over their ESG practices which arguably are a clear dereliction of their fiduciary responsibilities to investors). From a marketing standpoint, JP Morgan probably thought the ESG factor was a good marketing strategy when the fund was launched. As an investor, you need to know what is important to you and what is not.

Who Should (And Should NOT) Invest in JEPI?

If your goal as an investor is high income with less volatility, JEPI may be a suitable investment for you. Just know the yield will likely fall (to the high single digits, and at times even lower) and you are giving up dramatic long-term return potential (through the reduced volatility of the ELN covered call strategy). Also know that JEPI's expense ratio is relatively low, but still a significant detractor from your long-term returns, and so are the fund's high implicit trading costs (related to very high portfolio turnover), the ELN strategy and potentially the ESG considerations, as well.

On the other hand, if your goal is to maximize long-term total returns, JEPI is likely an absolutely terrible investment for you (for all of the reasons described above). Said differently, if your investment horizon is 10 years or less, JEPI might be just okay (but not great), but if your horizon is more than 10-years--avoid JEPI like the plague!

Two (2) Better Long-Term Big Yields:

If you are a long-term investor, an S&P 500 index fund ( SPY ) will likely dramatically outperform JEPI, but it won't pay you the big income you want. And since some investors aren't willing to just withdraw some of their S&P 500 gains to use as spending cash (they just want those big JEPI-style dividends), here are a couple better big-yield opportunities (described below). We believe both big-yield opportunities should be considered within the constructs of a prudently diversified long-term income-focused portfolio. They'll both likely lead to dramatically better long-term high-income results than JEPI, especially when held within a more broadly diversified high-income-focused portfolio.

(1) The Reaves Utility Income Fund ( UTG )

{kind=link}

The Reaves Utility Income Fund is a closed-end fund ("CEF") that invests in securities (mostly stocks) operating mainly in the Utilities sector (a sector known for lower volatility and higher dividend income). And despite its higher management fees and expense ratio, it will likely handily outperform JEPI over the next decade (higher returns and comparable monthly income payments) for the reasons described below.

First, UTG's holdings naturally have lower volatility than the typical S&P 500 stock (this is a general characteristic of Utilities stocks), but unlike JEPI, UTG will benefit more fully from the stock market's long-term gains. Specifically, JEPI limits its upside by only participating in around 65% of the markets long-term gains (due to its covered call ELN strategy), whereas UTG uses a prudent amount of leverage (i.e. borrowed money) to more fully participate in the market's long-term gains (UTG recently employed ~19.3% leverage). Said differently, JEPI's long-term gains are hamstrung whereas UTG's long-term gains are prudently enhanced. Not only does the UTG leverage improve long-term returns, but it does so enough to offset the strategy's higher management fee and expense ratio.

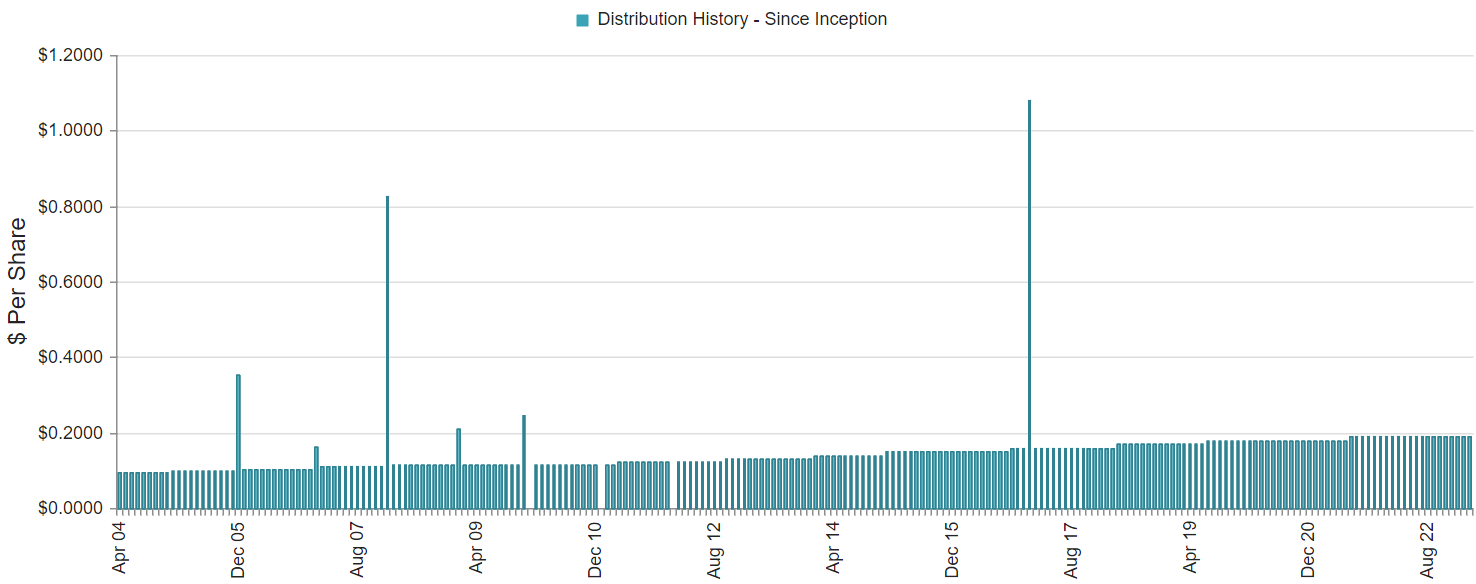

Further, both fund's pay monthly income, but JEPI's yield is set to fall, whereas UTG's yield is set to remain strong (see UTG's since-inception distribution payments in the chart below).

{kind=link}

If you are seeking a high-monthly-income fund and strong returns, UTG's total returns will likely beat JEPI's very significantly over the next decade and beyond. Especially considering we like the Utility Sector right now (it's been relatively weak year-to-date in a bit of short-term mean reversion as compared to growthier sectors which have been whipsawed by unusually strong year-end tax loss selling followed by early 2023 strong gains).

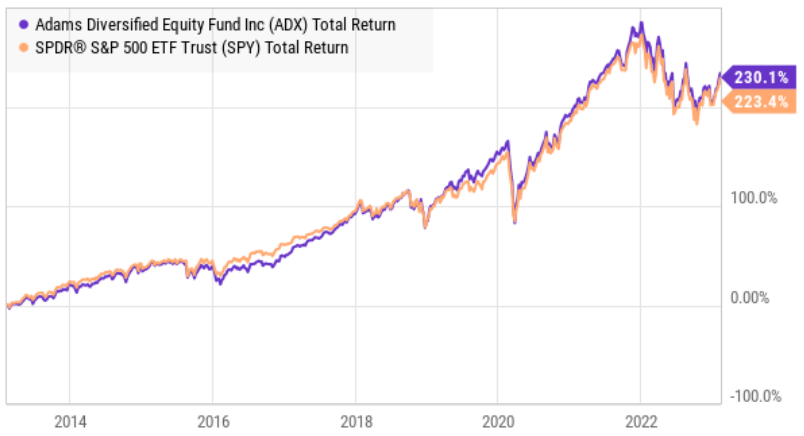

(2a) The Adams Diversified Equity Fund ( ADX )

{kind=link}

If you are a long-term income-focused investor, the Adams Diversified Equity Fund is simply a better option than JEPI. Period. It will offer better total returns with a comparable amount of income.

For starters, ADX is a closed-end fund that has been paying big dividends to investor for over 80 years straight. It guarantees at least a 6% distribution each year, and it is usually significantly higher. The average annual distribution on ADX is comparable to what JEPI's average annual distribution will be in the years ahead (for the reasons we explained earlier). Further, ADX currently trades at ~14.9% discount to its net asset value (i.e. "NAV" or the aggregate value of its underlying portfolio holdings). This type of large discount is a unique characteristic of closed-end funds (it's generally not allowed on ETFs, and there are mechanisms and arbitrageurs in place to make sure it essentially never happens for ETFs, like JEPI). And this discount helps more than offset ADX's 0.56% annual expense ratio.

ADX invests actively in US equities across market sectors, and it has historically delivered net returns that are comparable (usually better) than the S&P 500--a feat JEPI will simply not be able to accomplish over the long-term. What's more, ADX can be a great compliment to income-investor portfolios because it invests across sectors, including sectors that many income-focused investors (and JEPI in particular) significantly miss out on (such as technology and discretionary).

{kind=link}

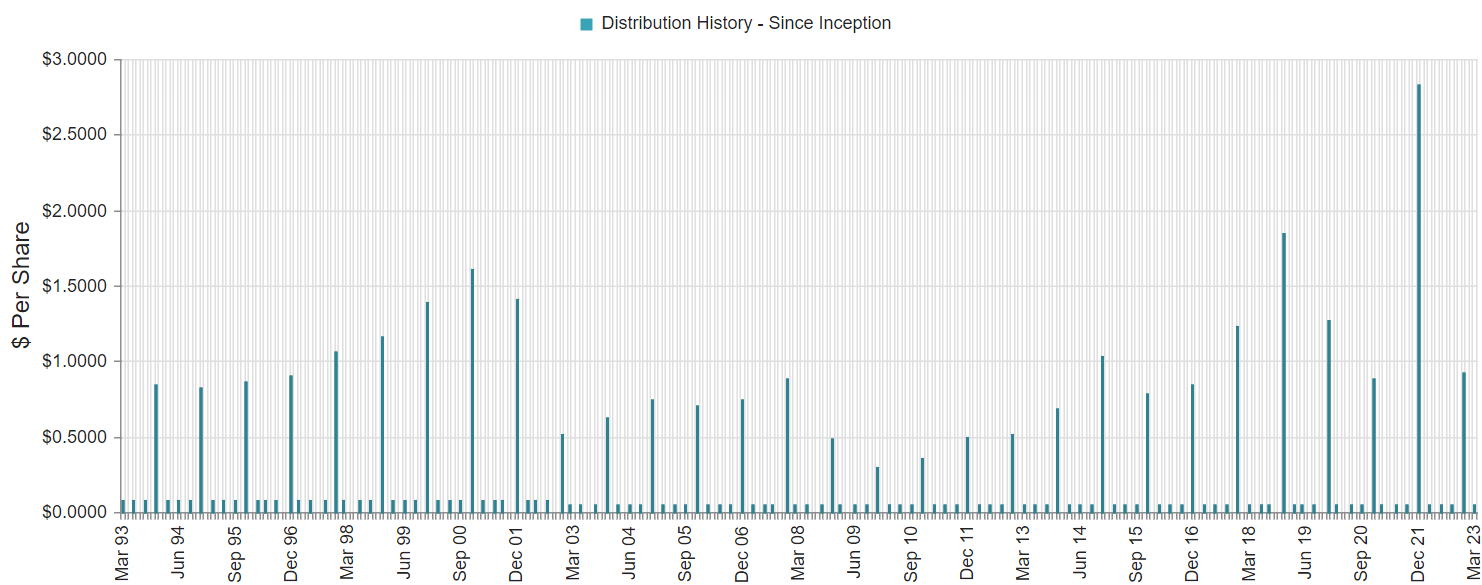

One common complaint with ADX is that is pays dividends quarterly. Specifically, it pays a smaller dividend in quarters one, two and three, followed by a larger fourth quarter dividend to bring the annual yield significantly higher. Here is a look at its recent dividend history.

{kind=link}

Investment websites notoriously misreport the ADX dividend because their yield calculation methodologies simply cannot handle the annual ADX small-small-small-big distribution cadence. But if you can handle that pattern--you will do dramatically better with ADX (than with JEPI) over the long term.

(2b) 25% PIMCO Dynamic Income Opps ( PDO )

{kind=link}

If you simply cannot sleep at night with the full volatility of the S&P 500, you might also consider adding an allocation to PIMCO's popular bond fund ( PDO ). It gives you big steady monthly distribution payments (the current yield is 10.9%--above what JEPI's long-term average will be), and typically reduces your aggregate volatility when paired with an allocation to a stock fund such as ADX. For example, a 25% allocation to PDO plus a 75% allocation to ADX will likely dramatically outperform JEPI over the next decade in terms of total returns; and it will also give you big steady income, plus significantly less volatility as compared to the S&P 500. For perspective, PDO:

- invests opportunistically across the bond markets, including corporate bonds, bank loans and asset-backed securities, to name a few.

- has never decreased its distribution (only increased it).

- has a history of occasionally paying additional special dividends.

- trades at only a 4.1% premium to NAV, which is relatively quite small for a PIMCO bond fund (PIMCO is the market leader in bond funds).

- uses ~50% leverage to magnify returns and income (this is a healthy "full" dose of borrowing that we're comfortable with considering the competencies and resources of PIMCO).

And also extremely important, such a combination (25% PDO, 75% ADX) may get you thinking about investing from the aggregate portfolio perspective (instead of just looking at each investment in isolation--the error many investors make when considering JEPI); the aggregate portfolio approach can help you reduce risks while keeping your income and total returns high.

The Bottom Line:

If you are looking for bigger monthly income and lower price volatility (as compared to the S&P 500) JEPI may be suitable. Just know that over the long-term, JEPI's yield will likely fall significantly and your total returns are set to dramatically underperform other big-yield opportunities, such as those discussed in this report. In fact, we recently ranked the other opportunities in this article (including ADX, PDO and UTG) in our new free report: Top 25 Big-Yield CEFs, ETFs (6% to +12% Yields). And for comparison purposes, we also include a ton of current data on over 100 big-yield CEFs and ETFs in that report for you to consider.

However, at the end of the day, you need to invest only in opportunities that are right for you and your personal situation. We believe disciplined, goal-focused, long-term investing will continue to be a winning strategy.

For further details see:

JEPI: 2 Better Long-Term Big Yields