JEPI - JEPI Could Become A 13% Yielding Rich Retirement Dream In 2024

2023-11-18 07:20:00 ET

Summary

- JEPI is one of the best run-covered call ETFs I've ever seen. It's designed for 6.5% monthly yield, 8% returns, and 35% lower volatility than the market.

- JEPI has benefited from increased volatility and from its low volatility blue-chip portfolio consisting of the world's best companies.

- The economic data indicates that in a mild recession in 2024, a historically average bear market decline could send option premiums soaring, and JEPI's yield could return to 13%.

- While JEPI's historical performance has blown away management's guidance, remember its purpose in your portfolio.

- JEPI is perfect for two kinds of investors, and in a taxable account, historically gives back 40% of gains to the IRS.

The JPMorgan Equity Premium Income ETF ( JEPI ) exploded in 2022 with $13 billion in new inflows, the eighth most popular ETF in America.

That's because JEPI got lucky and launched before a 28% bear market.

Well, I have wonderful news for fans of JEPI. The stars are aligning for what could be a repeat of 2022's volatility spike, and that means JEPI will get another chance to shine brightest.

Let me show you why the data points to a potential return of 2022 levels of volatility and 13% yields for JEPI and why that makes this a potentially rich retirement dream machine for anyone looking for intelligent income ideas next year.

Wall Street Is Missing Something Pretty Important

Wall Street is excited that weakening economic growth and falling inflation will cause the Fed to start cutting interest rates next year.

For 15 years, the market was obsessed with interest rates, thinking low rates permanently justified higher valuations.

| Weekly Decline In S&P EPS Consensus |

| Last Week's EPS Consensus |

| Year |

| EPS Consensus |

| YOY Growth |

| Forward PE |

| 0.00% |

| $206.04 |

| 2021 |

| $206.04 |

| 50.03% |

| 21.9 |

| -0.07% |

| $215.66 |

| 2022 |

| $215.50 |

| 4.59% |

| 20.9 |

| -0.10% |

| $219.05 |

| 2023 |

| $218.84 |

| 1.55% |

| 20.6 |

| -0.48% |

| $245.22 |

| 2024 |

| $244.05 |

| 11.52% |

| 18.5 |

| -0.46% |

| $274.20 |

| 2025 |

| $272.95 |

| 11.84% |

| 16.5 |

| Recession-Adjusted Forward PE |

| Historical 2024 EPS (Including Recession) |

| 12-Month forward EPS |

| 12-Month Forward PE |

| Historical Overvaluation |

| PEG |

| 21.21 |

| $212.32 |

| $241.14 |

| 18.673 |

| 10.95% |

| 2.20 |

| Historically Overvalued |

| 25.49% |

(Source: Dividend Kings S&P 500 Valuation Tool, FactSet)

The bottom-up analyst consensus is for 12% earnings growth in the next two years, which is optimistic to say the least.

{kind=link}

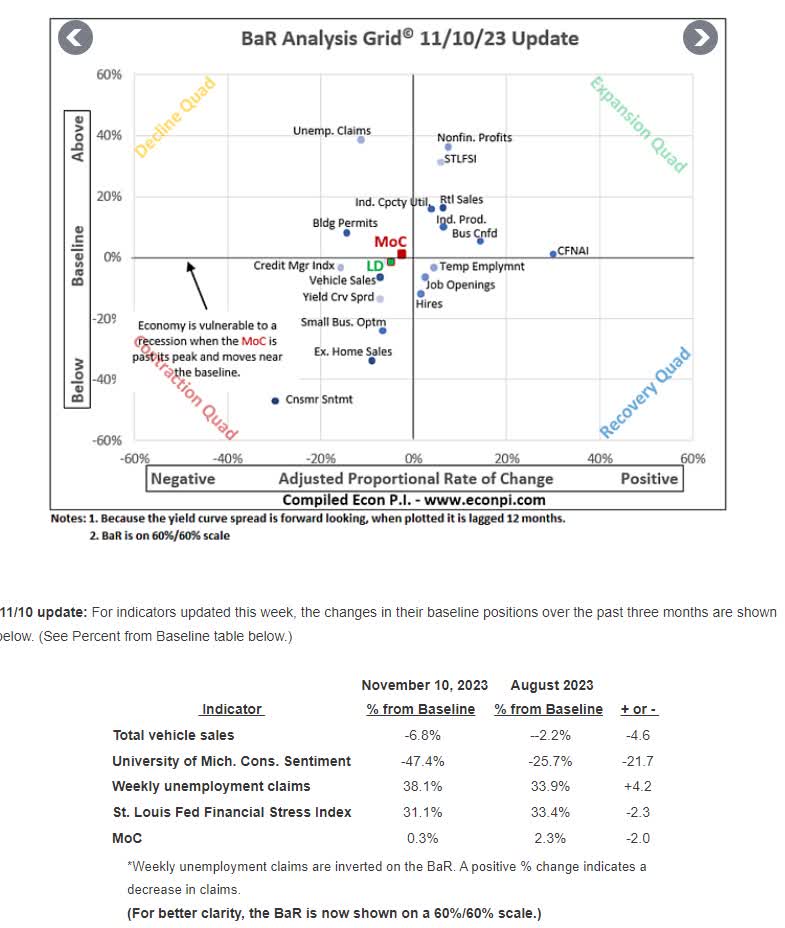

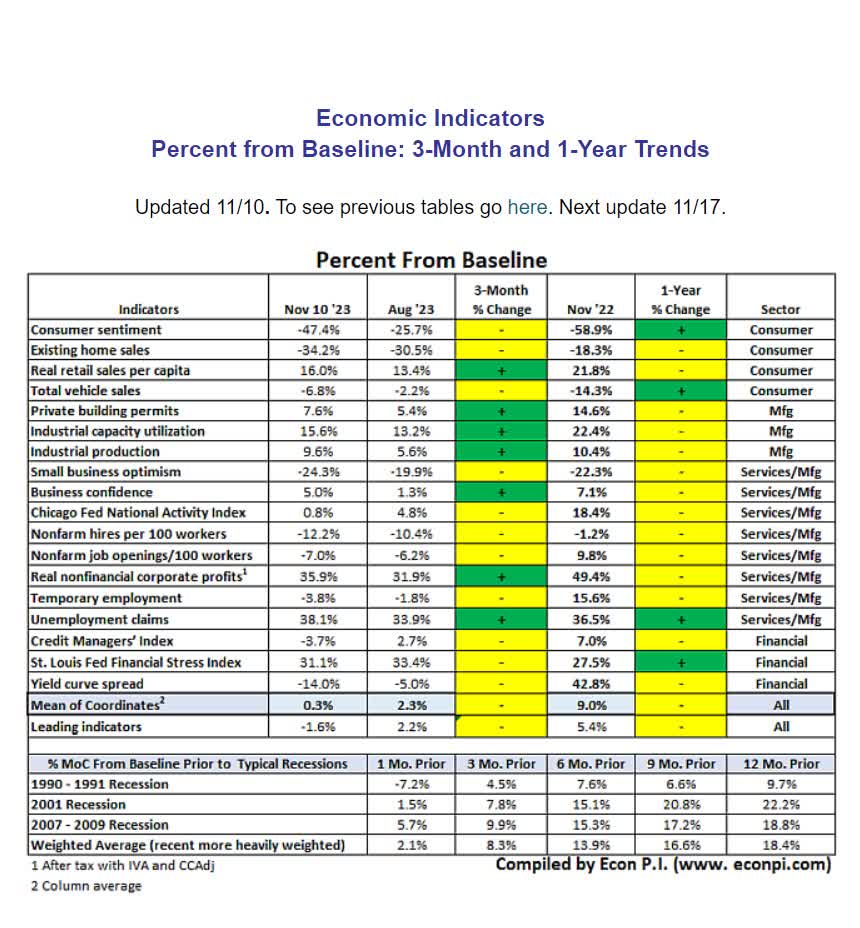

The economic data is rolling over and now points to a recession in 2024. In fact, JPMorgan thinks it might begin in December.

{kind=link}

And it's not just these 18 leading indicators that have correctly predicted every recession for 30 years, saying recession is likely.

{kind=link}

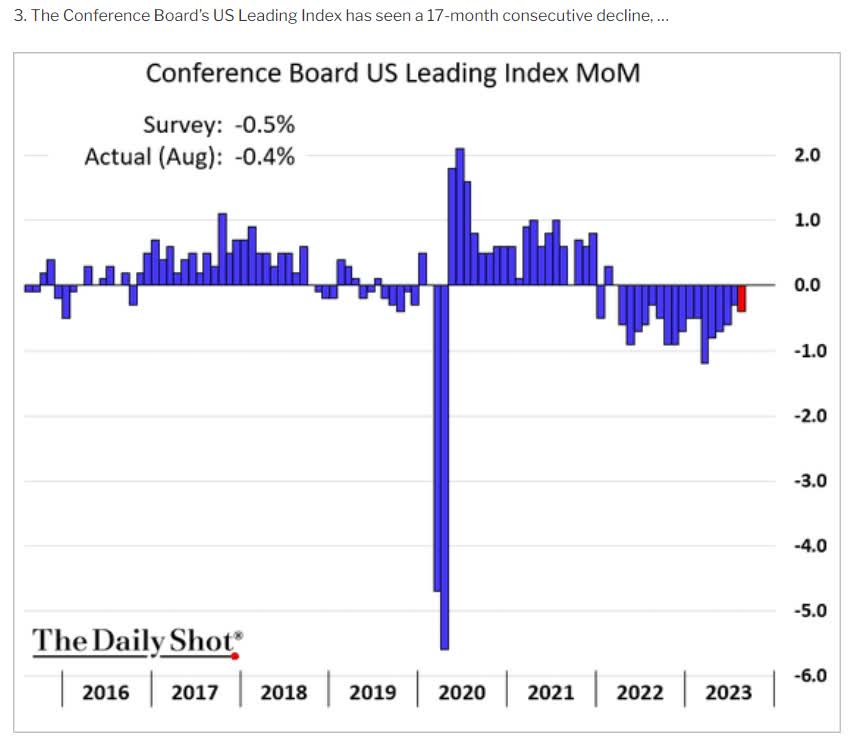

The conference board shows the second strongest signal for an impending recession.

{kind=link}

Manufacturing is in a recession and historically we've never had 12 months of contraction without a full economic recession.

{kind=link}

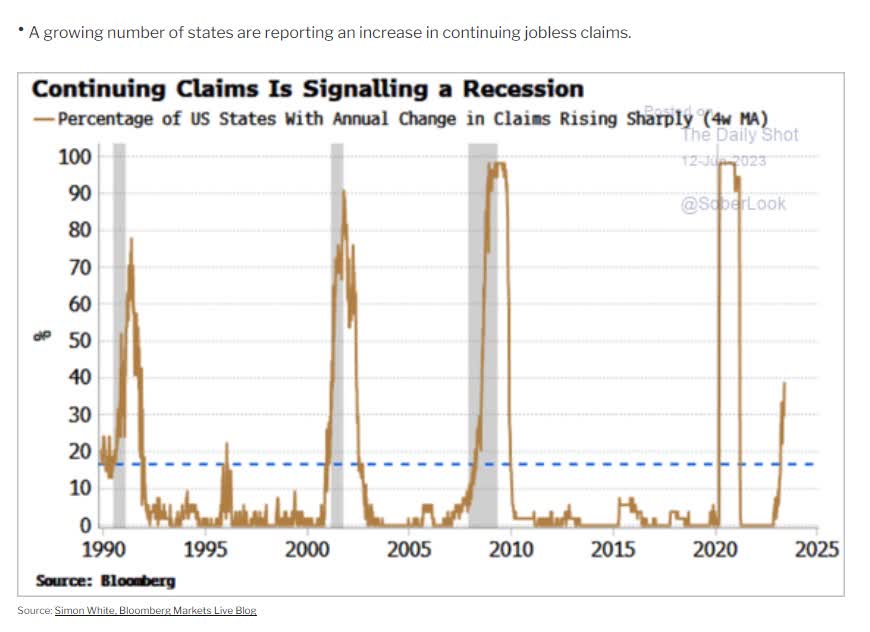

The jobs market is also signaling a recession.

Bad News Isn't Actually Good News For Stocks

The market is trading at almost 19X forward earnings vs a historical average of 17 over the last ten years, 25 years, and 50 years.

That assumes 25% earnings growth in the next two years.

How often do earnings grow in a recession?

{kind=link}

They don't. Ever.

{kind=link}

Could this be the first time in history that the Fed pulls off a soft landing with inflation peaking above 5%? Sure. Is that a good base-case? Given the current data... no.

Could the market ignore that earnings expectations are deeply negative and that every step higher the market takes pushes the PE to ever higher levels? Sure.

But ask yourself this. Why will investors pay a 10%, 15%, or 20% historical premium for stocks going into a recession? Once it becomes obvious that earnings won't grow at 11% next year?

What Happens To The S&P If There Is A Recession In 2025

| Earnings Decline |

| S&P Trough Earnings |

| Historical Trough PE Of 14 (13 to 15 range) |

| Decline From Current Level |

| Peak Decline From Record Highs |

| 0% (unprecedented bull case) |

| 273 |

| 3821 |

| 15.1% |

| -20.7% |

| 5% (consensus recession scenario) |

| 259 |

| 3630 |

| 19.4% |

| -24.7% |

| 10% (Goldman recession scenario) |

| 246 |

| 3439 |

| 23.6% |

| -28.6% |

| 13% (Average since WWII) |

| 237 |

| 3325 |

| 26.2% |

| -31.0% |

| 15% (BAC recession scenario) |

| 232 |

| 3248 |

| 27.9% |

| -32.6% |

| 20% (Moody's, Morgan Stanley recession scenario) |

| 218 |

| 3057 |

| 32.1% |

| -36.6% |

| 25% |

| 205 |

| 2866 |

| 36.4% |

| -40.5% |

| 30% |

| 191 |

| 2675 |

| 40.6% |

| -44.5% |

| 35% |

| 177 |

| 2484 |

| 44.8% |

| -48.5% |

| 40% |

| 164 |

| 2293 |

| 49.1% |

| -52.4% |

| 45% |

| 150 |

| 2102 |

| 53.3% |

| -56.4% |

| 50% |

| 136 |

| 1911 |

| 57.6% |

| -60.4% |

(Source: Dividend Kings S&P Valuation Tool, FactSet, Bloomberg)

It doesn't matter when a recession arrives next year; if there's a recession, the market will likely fall hard, just like in 2022.

And that's where JEPI is going to shine.

Why Market Timing Is Never the Answer

{kind=link}

Timing the economy is impossible; market timing would be impossible even if you could do it.

{kind=link}

If possible, market timing wouldn't really boost long-term returns more than about 0.5% per year.

{kind=link}

In 20 years of market timing, the average investor achieved 38% inflation-adjusted returns while the S&P tripled.

Time in the market, not market timing, is always and forever the right answer in a world where nothing is 100% certain and everything is probability curves.

Why JEPI's Yield Could Soar To 13% In 2024 - Video

- JEPI: This 12% Yielding ETF Is Perfect For 2 Kinds Of Investors - this is my introductory deep dive on JEPI.

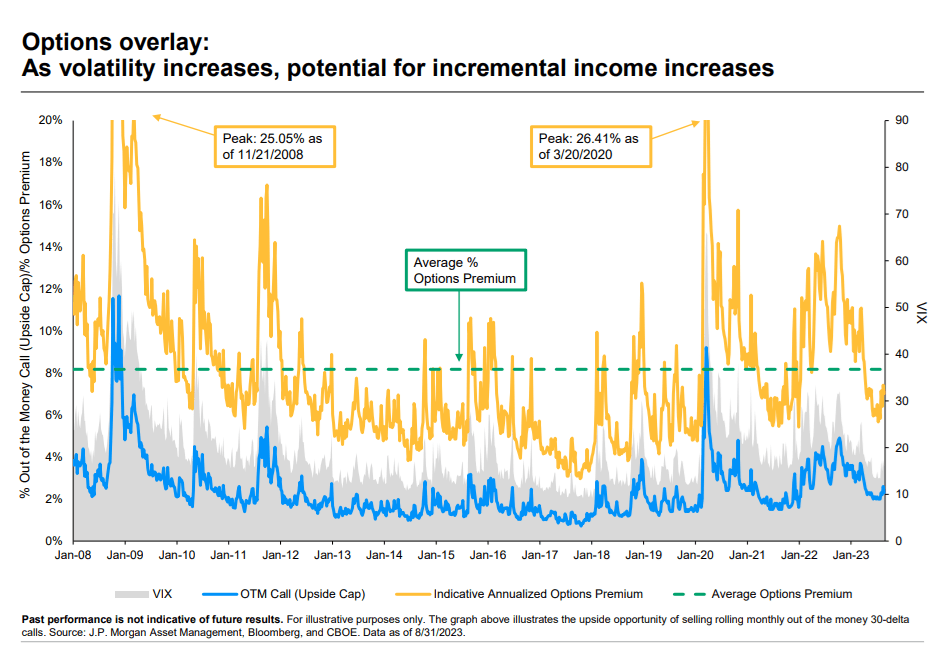

JEPI profits from high volatility. The faster stocks fall, the more yield they will generate.

JPMorgan Asset Management JPMorgan Asset Management

{kind=link}

{kind=link}

Reasons JEPI Isn't Right For Everyone

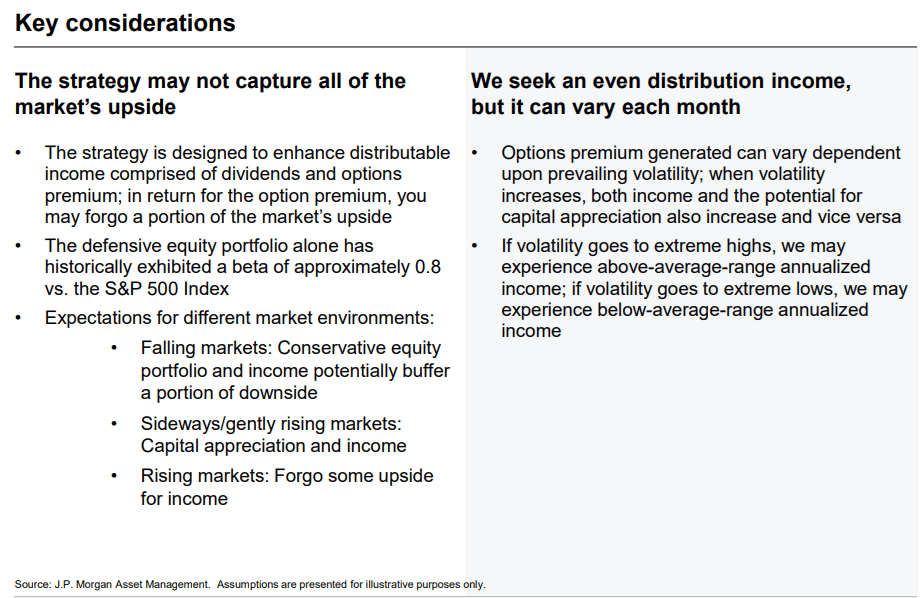

Covered call ETFs generally perform best in volatile sideways markets and don't tend to lose as much when we see a bear market.

- With face-ripping bear market rallies that fail

- And big crashes that result in high-option premiums

- An overall sideways market that generates massive option income

What does JEPI's management expect long term from their super popular ETF?

{kind=link}

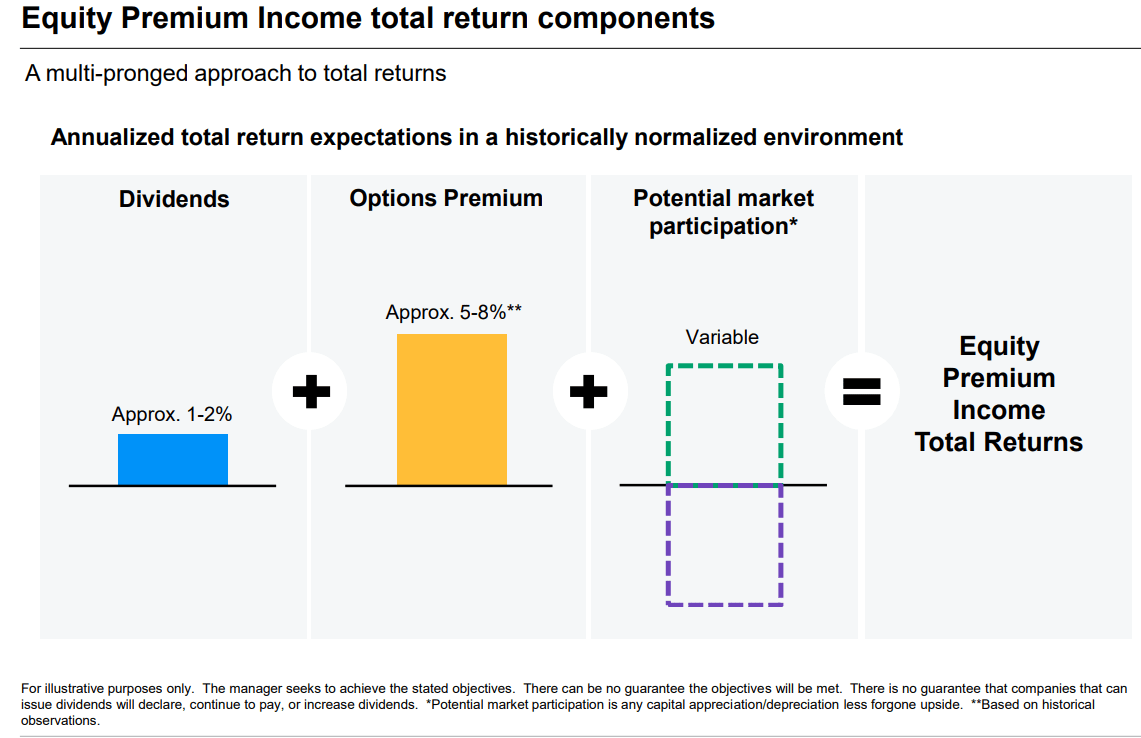

About 6% to 8% returns, or roughly 85% of the market's long-term upside potential, but with 5% to 8% yield and about 35% less volatility.

That's the true investment thesis for JEPI, which all investors need to realize.

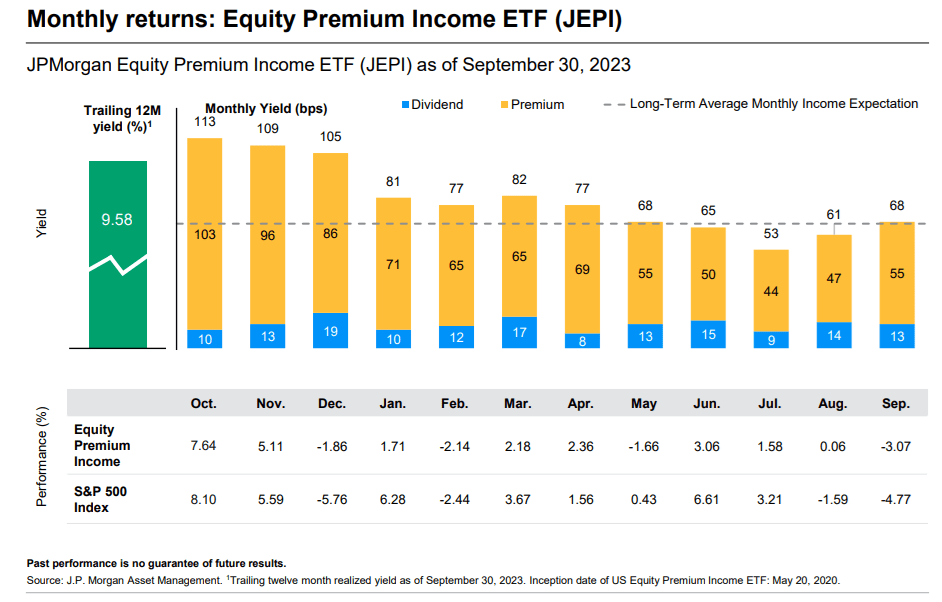

JEPI's long-term yield, per management guidance, is 6% to 7%. So far they have outperformed that by a wide margin, but don't buy JEPI planning on double-digit yields.

Let's not forget that a key reason JEPI has such a great yield and such remarkable returns so far is its use of ELNs. The risk with those is that if counterparties default on those contractual obligations, JEPI can blow up.

- Not necessarily the portfolio itself, which is 80% to 85% blue chips

- But 80% to 85% of the income could potentially collapse in another financial crisis

In other words, those who think they can safely buy 100% JEPI and retire rich are taking on much more income risk than they believe, especially if they think JEPI's income will keep rising yearly.

You should know that ELN and covered call income are generally taxed at ordinary rates.

- Just like REIT dividends

Rather than 0%, 10%, 15%, 20%, or 23.8% tax rates, as with qualified dividends, just 15% to 20% of JEPI's dividends are qualified.

This means owning it in a tax-deferred retirement account is optimal.

The effective JEPI tax rate for high-income investors is close to 50% if owned in taxable accounts.

- A post-tax yield of closer to 6% for investors in the top tax bracket

- And management guidance for post-tax 2.5% to 4% yields

If you're in the top tax bracket, a 2.5% to 4% yield would equate to much lower total returns than 6% to 8%.

That's because JEPI's annual turnover is 195%.

Since its inception, JPMorgan estimates the average investor, net of fees and taxes, made 18% compared to 25% pre-tax returns.

- Taxes ate 28% of gains.

But in the past year, 40% of returns were reduced by taxes and high turnover-related expenses.

And remember, this is just for the average American, with a 28% tax bracket.

- The top income tax bracket saw 8% returns over the last year and 12% since inception

- Up to 50% of your returns could go to taxes

What does that mean for long-term investors? If you're rich enough to be in the top tax bracket, management's guidance for 6% to 10% returns could end up being 3% to 5%. 4.2% to 7.0% for the average American investor in the 28% tax bracket.

5.6% mid-range post-tax returns compared to about 8.5% for the S&P is a lot less exciting.

But there's one final important thing to know about covered call ETFs like JEPI.

You Can't Spend All The Dividends, Or You'll Lose Money Over Time

Even a 6.5% yield over time, as management is guiding for, still sounds great. But here's the catch. If you don't reinvest significant dividends, your initial investment will lose money over time.

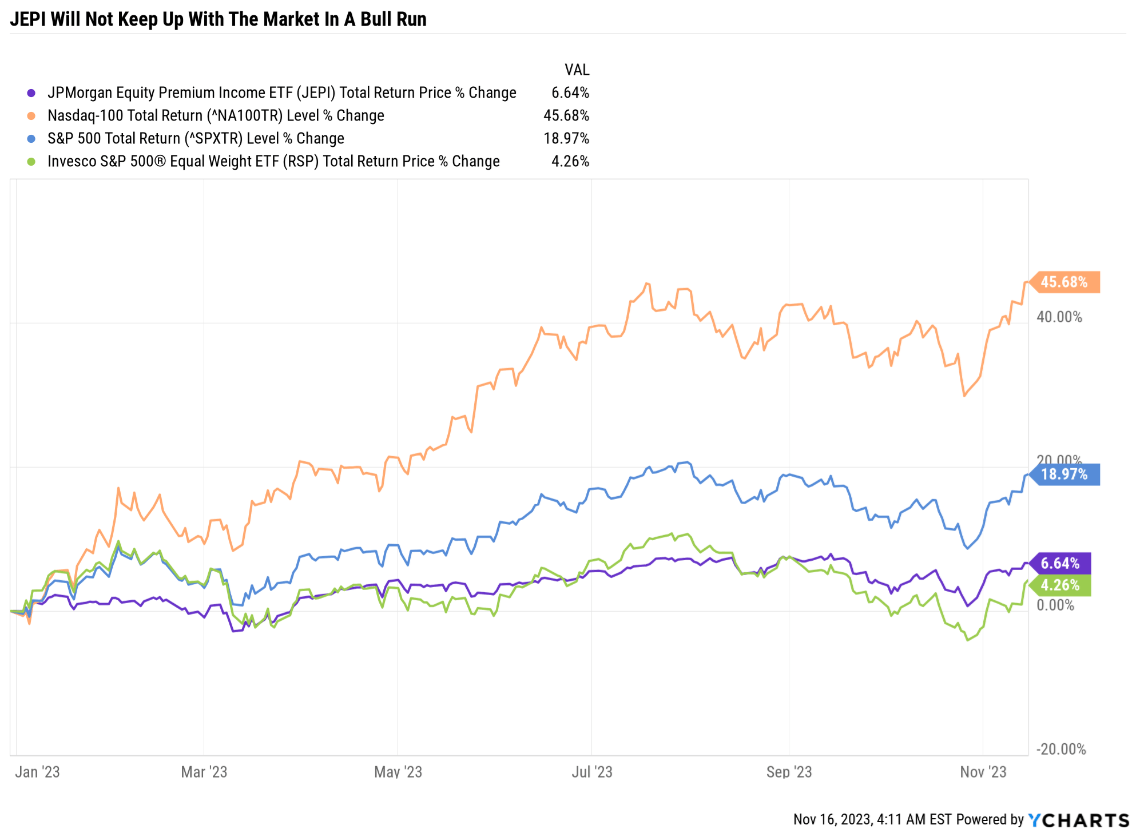

And while it should be common sense, let's not forget that in a raging market, JEPI was never designed to keep up with the S&P or the Nasdaq.

JPMorgan Asset Management YCharts

{kind=link}

{kind=link}

The S&P 7 is unbeatable this year. Remember, JEPI is designed for income and low volatility. At the cost of lower returns when stocks are roaring higher.

Bottom Line: The Return Of Volatility In 2024 Could Cause JEPI's Yield To Return To 13%

- JPMorgan thinks JEPI's yield will be 6.5% long-term

- but it's currently 9%, above the 5% to 8% yield guidance range

- a return to 2022 levels of volatility could send ELN premiums soaring and put the yield back at 13%

- JEPI was a rockstar in 2022 because its well designed to combine an advanced form of covered call writing with low volatility blue-chips

- JEPI is designed for 35% lower volatility than the S&P (much like a 60/40)

- and for 6% to 10% long-term returns, which it has historically outperformed

- JEPIX illustrates how JPMorgan's return guidance is accurate

- JEPI is best owned in retirement accounts, especially Roth IRAs

- in taxable accounts, the high tax nature of ELN income means that anyone not reinvesting all the dividends will eventually lose purchasing power to inflation

For further details see:

JEPI Could Become A 13% Yielding Rich Retirement Dream In 2024