JEPI - JEPI Is Not The New ARKK

Summary

- Investors often chase performance and end up buying a popular ETF near the top.

- One year ago the renowned journalist Jason Zweig warned investors ARKK became too large for its own good. We all know what happened afterward.

- Recently Zweig wrote an article highlighting the big inflows into JEPI.

- Is the JEPI the new ARKK, or not?

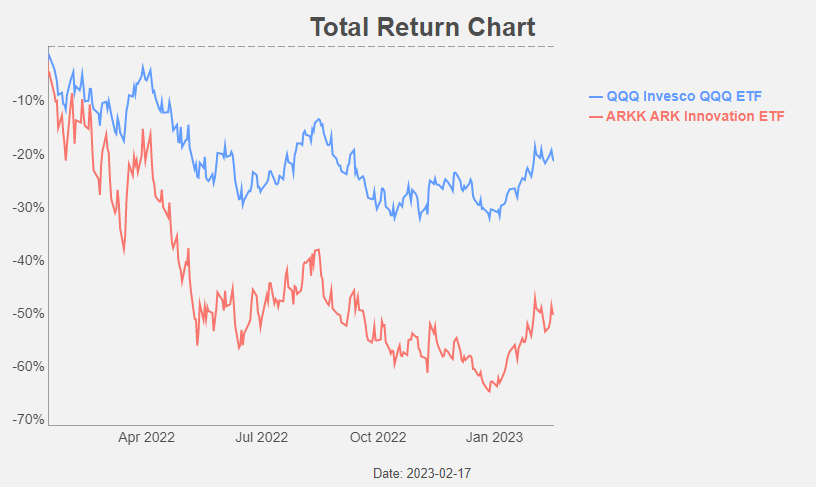

One year ago Jason Zweig wrote an article in the Wall Street Journal about the ARK Innovation ETF (ARKK). Thanks to a stellar performance, ARKK received massive inflows of investors chasing that performance. Figure 1 shows ARKK's performance since the article was published.

Figure 1: Total return chart (Yahoo! Finance, Author)

{kind=link}

Recently Zweig wrote another article in the Wall Street Journal highlighting the big inflows into the JPMorgan Equity Premium Income ETF (JEPI) after it's stellar performance. Is JEPI the new ARKK? Will JEPI suffer the same fate as ARKK?

For us the short answer is clear: no!

Why? The performance of ARKK is dependent on easy money conditions, while this is not the case for JEPI. The latter performed very well both in 2021 and 2022. It performs well both in a low and a high rate environment.

The long answer you can find below. We take a look at the beta exposure, the equity duration and the volatility sensitivity of both ARKK and JEPI.

Beta exposure

Both ARKK and JEPI are long equities. But ARKK is high beta and JEPI is low beta.

Covered call writing is a defensive, low(er) beta, strategy. When the markets rise, you get a nice return. That return will probably lower than the return of the equity markets itself, but that's something you know in advance.

When the equity markets fall, you outperform thanks to the collected option premiums. Of course, when the market really tanks, you will still have a negative return. Another way to frame this: the upside beta is lower than the downside beta.

Let's give an stylized example. Suppose we have a stock with a price of $100. We write a call with strike price $110 and we collect $3 option premium. When the stock moves to $120, we "get" $13 (or upside is capped at $110 plus the $3 premium), or an upside beta of 65%. When the stock drops 20%, we "get" a result of -$17 (a price drop of $20% plus the $3 premium), or an downside beta of 85%.

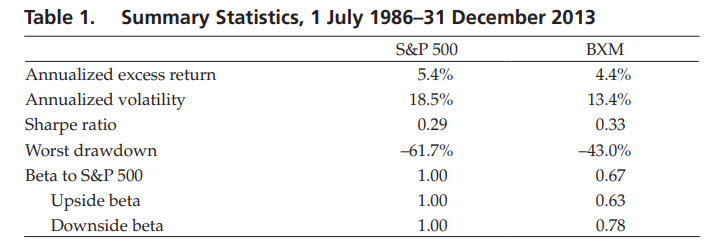

An 2014 AQR study showed and upside and downside beta of 0.63 and 0.78 for the CBOE S&P 500 BuyWrite Index (BXM) for the period 1986 to 2013.

Figure 2: Covered call statistics ((AQR))

{kind=link}

Despite the fact that the downside beta is bigger than the upside beta, covered call strategies are able to deliver equity-like returns with lower volatility.

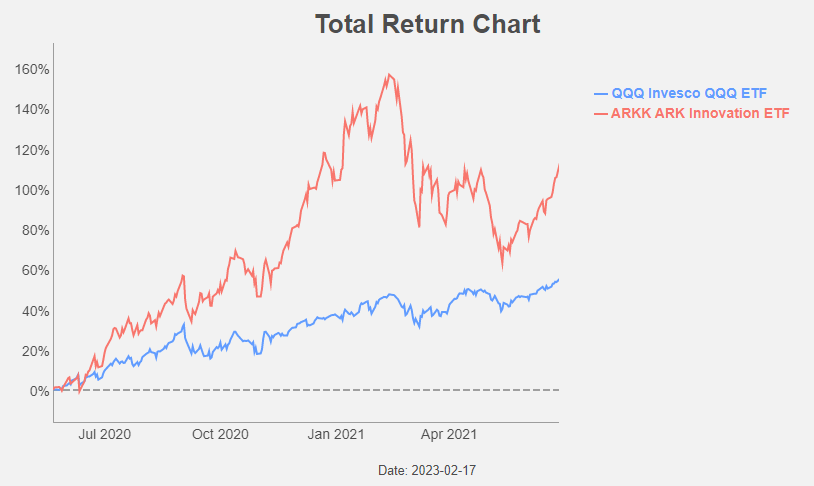

Regarding ARKK's beta-exposure we can be short: it's a high beta-ETF.

Figure 3: Total return chart (Yahoo! Finance, Author)

{kind=link}

And ARKK is high beta both in up markets (figure 3) as in down markets (figure 4).

Figure 4: Total return chart (Yahoo! Finance, Author)

{kind=link}

When the backdrop for equities is positive (cheap money, low inflation, low interest rates) ARKK will outperform. And vice versa, it will underperform.

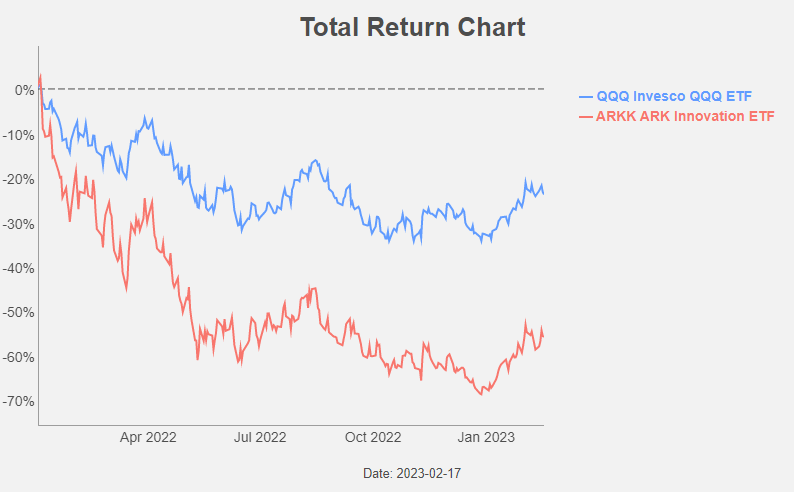

Equity duration

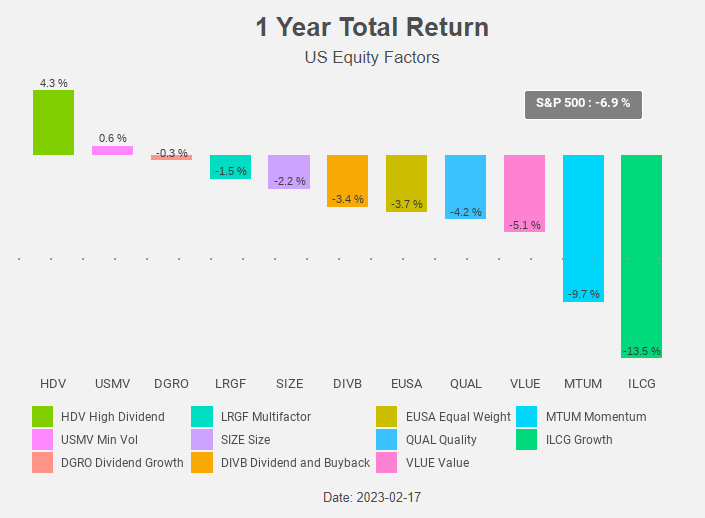

The past year was not good for equities. The same can of course be said of most equity factors.

Figure 5: Total return chart (Yahoo! Finance, Author)

{kind=link}

The worst equity factor was growth. Those low dividend, "long duration" growth equities were heavily hit by the rising interest rates. Dividend stocks sit on the other end of the duration spectrum and hence less impacted by the higher rates.

ARKK is a growth-ETF with a high equity duration, while JEPI is rather a dividend ETF with a low equity duration and hence less impacted by rising interest rates.

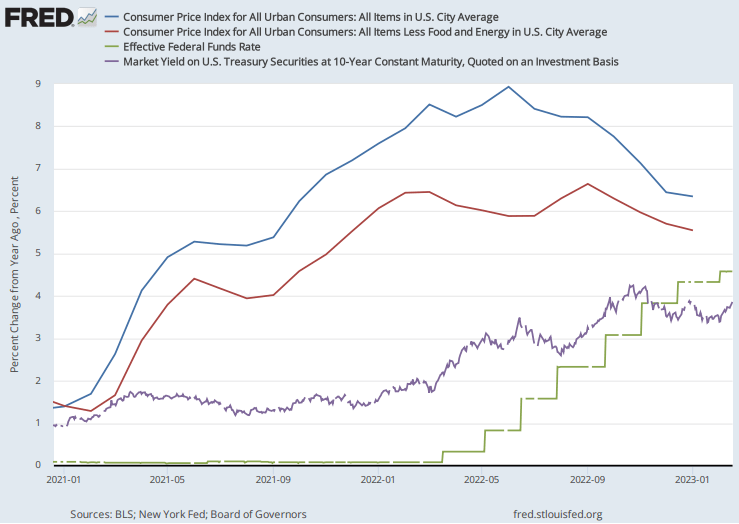

Inflation and longer term treasury yields started to rise in 2021 and ARKK started to underperform.

Figure 6: Inflation and interest rates ((FRED))

{kind=link}

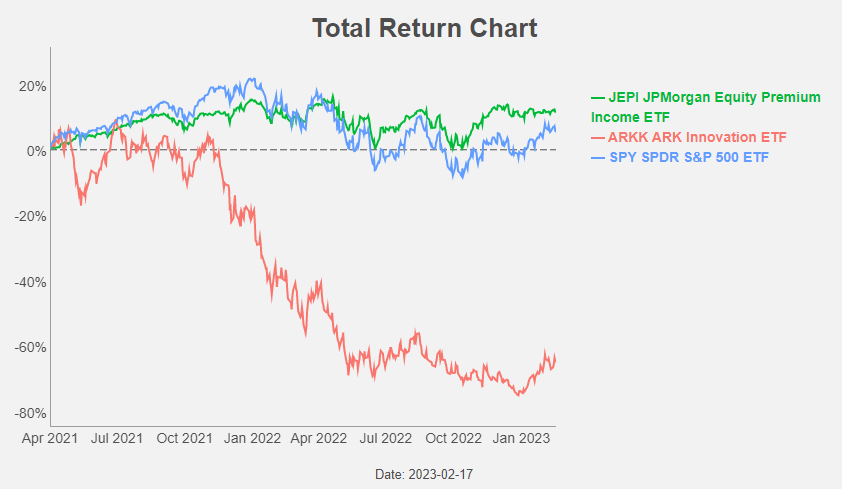

JEPI was less impacted and not only kept pace with rising equity markets in 2021. Last year, equities fell and JEPI outperformed.

Figure 7: Total return chart (Yahoo! Finance, Author)

{kind=link}

It will be no surprise that JEPI is a low duration ETF and ARKK a high duration ETF. If interest rates remain high (or rise even further) JEPI will be less negatively impacted than ARKK.

When interest rates fall and the fall is not caused by a recession, this would be good news for equities in general and high duration stocks in particular. JEPI would have a positive return, although it would probably lag the overall market. ARKK would again be firing on all cylinders.

When interest rates fall due to a recession, it remains to be seen how equity markets will perform.

Short volatility

A covered call ETF has actually two sources of return: the equity risk premium and the volatility risk premium. They are long equities (albeit with a low beta) and short volatility.

Being long equity is more straightforward for most investors compared to being short volatility.

When you sell options, you are short volatility. We can compare selling options with selling insurance. Just as an insurance policy provides protection against a potential future event, an options contract can provide protection against adverse price movements in an underlying asset. And in the insurance industry, the received premiums typically exceed claims on those contracts. People pay "too much" for their insurance. Likewise they pay too much for the options they are buying. As a result they drive up the price (and hence the implied volatility). And when realized volatility is low relative to implied volatility, the short position is profitable for option sellers like JEPI.

Realized volatility is a backward-looking and describes how an asset actually performed in the past, i.e. the historical or actual volatility achieved. Implied volatility on the other hand is a forward-looking estimate of volatility derived from the price of an option through the use of a theoretical pricing model like the Black & Scholes model.

Option prices reflect several factors that are directly observable or known such as the underlying price, the time until expiration, and strike price.

Figure 8: Implied volatility ((CBOE))

The Black & Scholes formula utilizes those observable parameters to calculate the average future volatility of the underlying asset, the "implied" volatility.

A covered call ETF's short position is profitable when realized volatility is low relative to implied volatility and unprofitable when realized volatility is high relative to implied volatility. Historically, we observe a propensity for the option market to price in slightly more expected volatility than what is subsequently realized (as is the case in the insurance business).

ARKK uses no options and doesn't try to capture the volatility risk premium, but there is nevertheless a link with (expected) volatility. The VIX Index is a measure of expected volatility that is derived from prices of options set to expire 30 days in the future. Expected and implied volatility are related but unique.

Figure 9: Expected volatility ((CBOE))

Generally, the VIX Index tends to have an inverse relationship with the equity markets. This negative correlation has led to the nickname "fear index" because the VIX Index has a tendency to move up quickly when the broad market falls sharply. Expected volatility typically increases when markets are turbulent or the economy is faltering. In contrast, if stock prices are rising the VIX Index tends to fall or remain steady at a low level. In this sense, one could call ARKK a short volatility investment, that performs well when expected volatility is low and vice versa.

Macro backdrop

Both ARKK and JEPI like an environment in which equities are rising with low volatility.

When equity markets perform strongly, JEPI will have a nice return albeit that it will trail the broader equity market. But that's something we know in advance. In this benign environment ARKK can be expected to outperform the broader market, given its high beta.

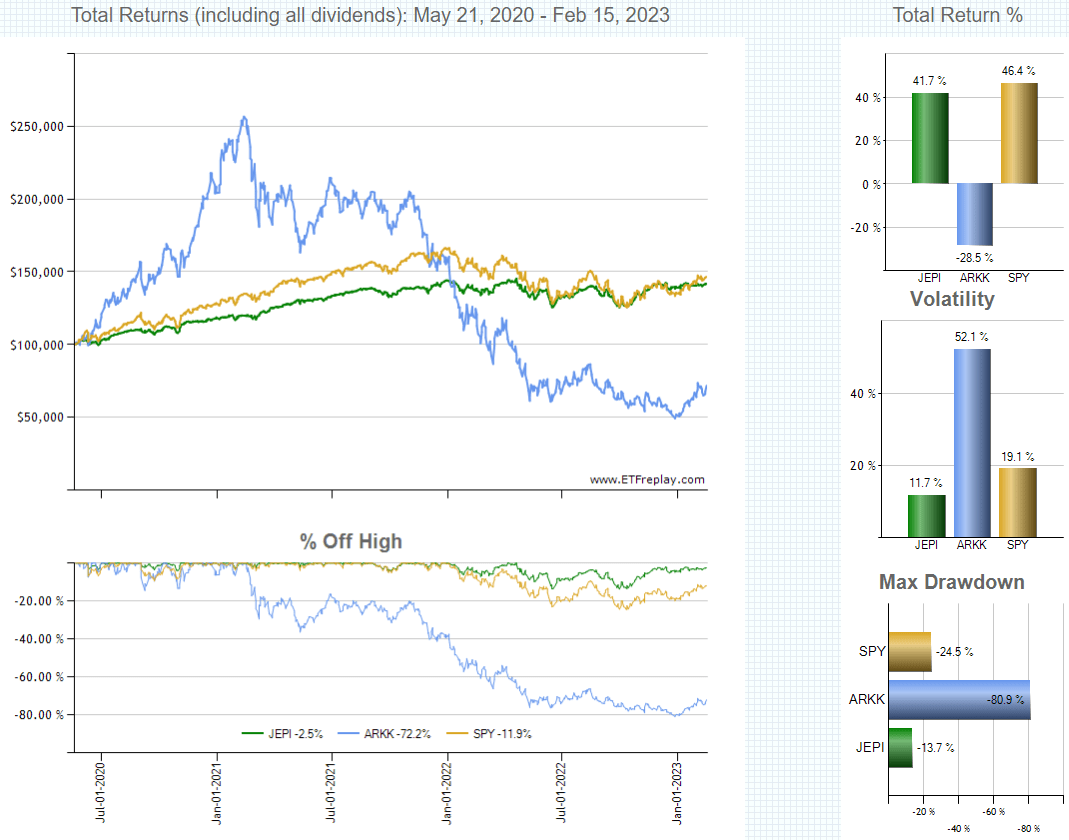

Last year, we had actually the opposite: an environment with falling equities and high volatility. ARKK performed horrible, while JEPI had a great year. That's the point we want to make: JEPI performs well no matter what the macro backdrop is.

Figure 10: ARKK vs JEPI (ETFreplay.com)

{kind=link}

Will we return to an environment with low volatility or is the higher macro volatility due to the high inflation here to stay?

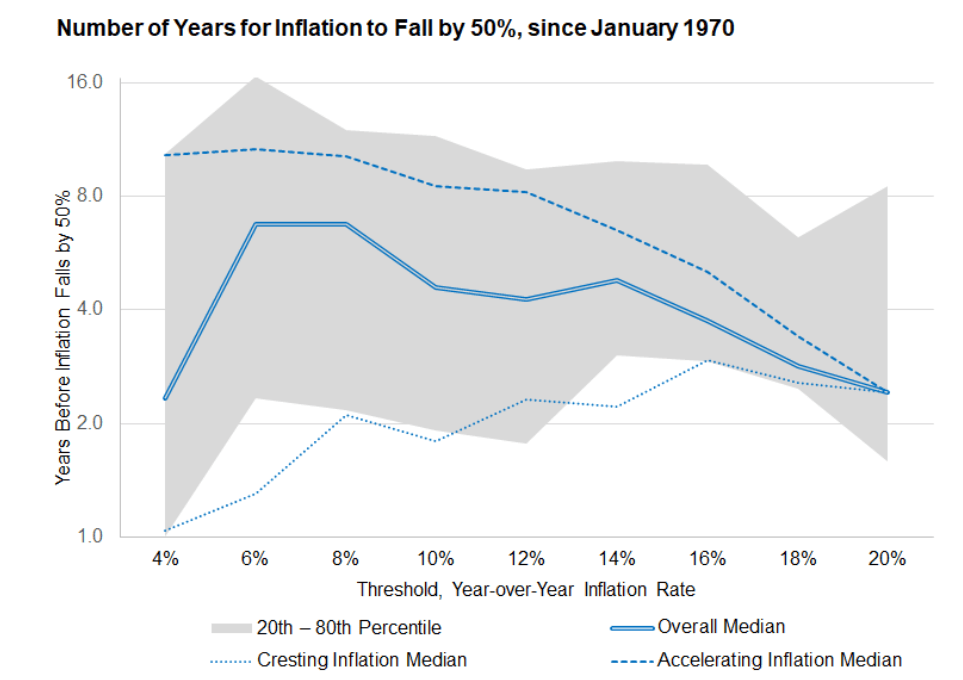

Research Affiliates last year investigated how quickly inflation returns back to an acceptable level once it crossed certain thresholds. They make a difference between cresting inflation and accelerating inflation. Cresting inflation crosses the 4% level, but doesn't reach the 6% inflation level. Accelerating inflation does cross the 6% level. The historical record is like this:

If inflation is cresting, inflation levels revert by half in about a year. If inflation is accelerating, 6% inflation reverts to 3% in a median of about seven years. Above 8%, reverting to 3% usually takes 6 to 20 years, with a median of over 10 years.

Figure 11: Years for inflation to fall by 50% (Research Affiliates)

{kind=link}

We think inflation is here to stay. It will probably cool, but we believe it will remain the coming years at a level above the 2% FED-target. De-globalization, de-carbonisation and demographics are pushing inflation figures higher than we were used to in the past decade.

JEPI has also a cost advantage compared to ARKK. ARKK has an expense ratio of 0.75%, while JEPI is at 0.35%. This cost advantage is present no matter what the macro backdrop.

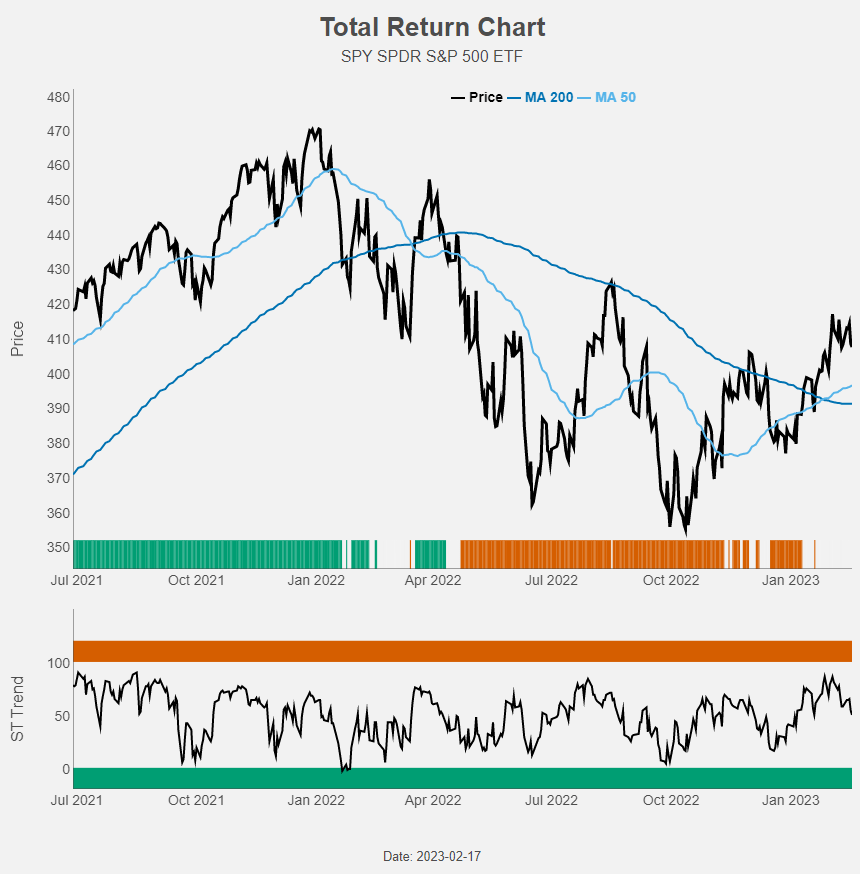

Equity markets

When the equity market really tanks, JEPI will have a negative return. That's why we prefer not to invest in a covered call strategy when the equity market is in a long term down trend. This is no longer the case.

Figure 12: Total return chart Figure 12: Total return chart (Yahoo! Finance, Author)

{kind=link}

When the LT trend is clearly up, we get a green light/colour. Vice versa, when the LT trend is clearly down, we see a red light/colour. In between the colour is orange.

The ribbon in the price-part of figure 12 shows the LT trend-colour, while the lower part of the chart shows the ST trend. We left out the orange colouring to avoid overloading the chart.

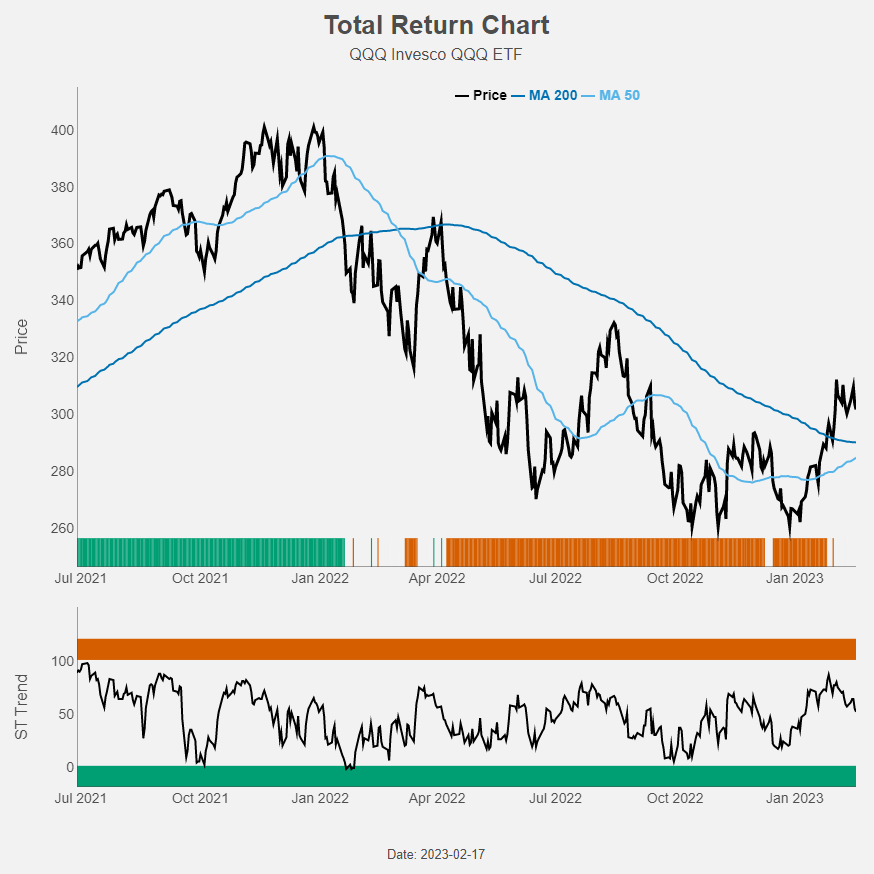

Likewise, we prefer not to invest in ARKK when the equity market in general and technology stocks in particular are in a long term down trend. You buy ARKK because you expect it to outperform in a rising market. Currently the NASDAQ is no longer in a downtrend.

Figure 13: Total return chart (Yahoo! Finance, Author)

{kind=link}

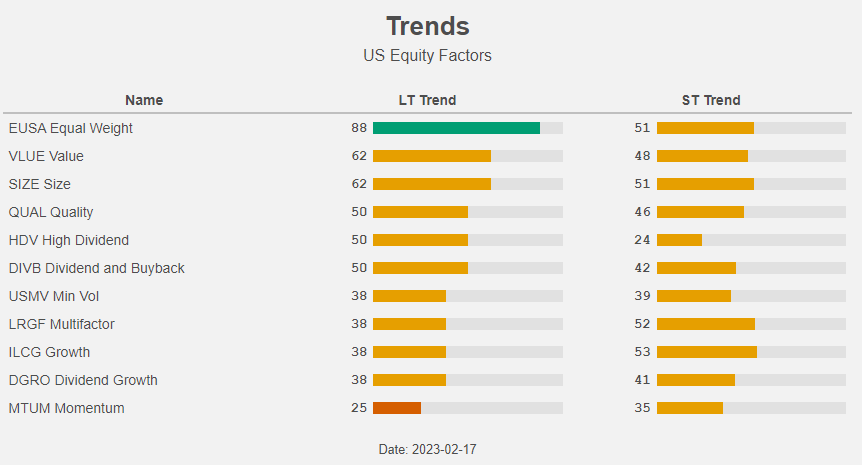

But trend-wise, the outlook for high div, value stocks is still better than the outlook for growth stocks, even after the nice recent performance.

Figure 14: Trends (Yahoo! Finance, Author)

{kind=link}

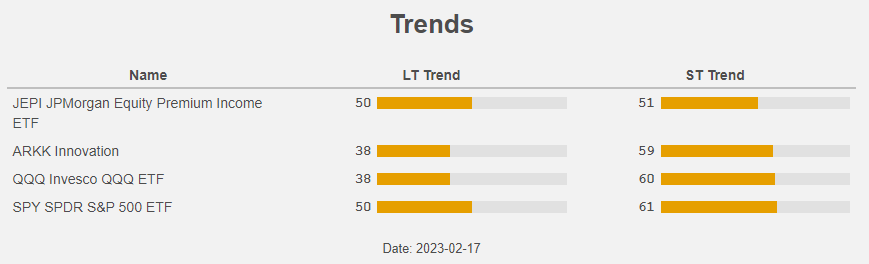

This is also reflected in the long term trend of JEPI (and SPY) versus ARKK and QQQ.

Figure 15: Trends (Yahoo! Finance, Author)

{kind=link}

Conclusion

JEPI performs as expected no matter what the macro environment. When the markets rise, JEPI will get a nice return. That return will probably be lower than the return of the equity markets itself, but that's something we know in advance. When the equity markets fall, JEPI will outperform thanks to the collected option premiums. Of course, when the market really tanks, JEPI will have a negative return. That's why we prefer not to invest in such a strategy when the equity market is in a long term down trend. This is no longer the case.

We cannot say that ARKK will perform well no matter what the environment. ARKK only thrives in a cheap money environment. And that train has left the station. We expect inflation to cool, but we do not envisage a return to cheap money environment of the past decade.

We would like to conclude with a quote from the AQR study we mentioned before: "Selling covered calls may be a good stand-alone strategy when implied volatilities are high relative to expectations and, in particular, a good strategy when combined with earning the equity risk premium."

According to us, JEPI is not the new ARKK.

For further details see:

JEPI Is Not The New ARKK