JEPI - JEPI Is One Of My Favorite Income Funds For The Foreseeable Future

2023-08-22 08:45:00 ET

Summary

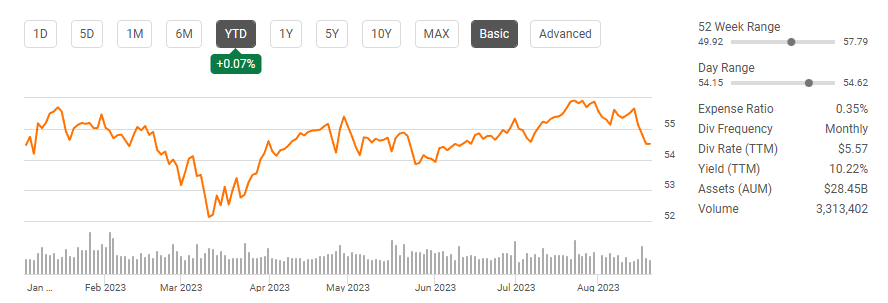

- JPMorgan Equity Premium Income ETF has grown to $28.45 billion in assets under management and has appreciated by 3.65% since September.

- JEPI generates income through monthly distributions and capital appreciation, with a portfolio designed to offer less downside volatility than the S&P 500.

- The fund allocates 80% of its assets to equities and 20% to exchange-linked notes, allowing for continuous income generation without sacrificing upside potential.

The JPMorgan Equity Premium Income ETF ( JEPI ) continues to become increasingly popular throughout the income investor community. Last September, I wrote an article about JEPI ( can be read here ), and it had just over $12 billion in assets under management ((AUM)) while trading at $52.59. Since then, shares of JEPI have appreciated by 3.65% and generated $5.57 of distributed income which is 10.59% of its share value from September. In addition to appreciating and generating a large amount of distribution income on a percentage basis, JEPI has added roughly $10 billion in AUM, as it's grown to $28.45 billion. JEPI has become one of my favorite income funds, and I think it's going higher in the future while continuing to produce double-digit yields.

{kind=link}

If you're unfamiliar with JEPI, here is an overview of the fund structure and how it generates income

J.P Morgan Asset Management which is under the JPMorgan Chase ( JPM ) umbrella, created JEPI, which is a hybrid fund. The dual approach has been established to generate large amounts of income through monthly distributions while delivering capital appreciation. Risk mitigation is at the forefront of JEPI's roots as its portfolio has been constructed to generate less volatility than the market as the fund managers select companies for JEPI's holdings that they feel will offer less downside than the average company found within the S&P 500.

The structure of JEPI's fund allocates 80% of its assets toward investing in equities. The other 20% is allocated toward generating income through exchange-linked notes (ELNs). ELNs are structured as notes issued by counterparties, including banks, broker-dealers, or their affiliates, and designed to offer a return linked to the underlying instruments within the ELN. By investing 20% of its assets in ELNs, JEPI can create monthly income for its investors. Instead of writing covered calls on its positions, JEPI generates recurring cash flow from the premiums on the call options the ELNs write.

This structure allows JEPI to generate income on a continuous basis without sacrificing the majority of its upside potential. Traditional covered-call funds write at the money covered calls, and there is a significant trade-off between the immediate income generated and potential future capital appreciation. I like JEPI's structure because the equity side isn't capped, and it is running an options overlay strategy within the ELNs, which is only 20% of the portfolio. This creates what I consider to be a best-of-both-worlds combination. JEPI may not ft your investment needs, so please read through the prospectus ( can be read here ) prior to investing.

JEPI has continuously delivered for its shareholders by generating large amounts of income and establishing a multi-year track record.

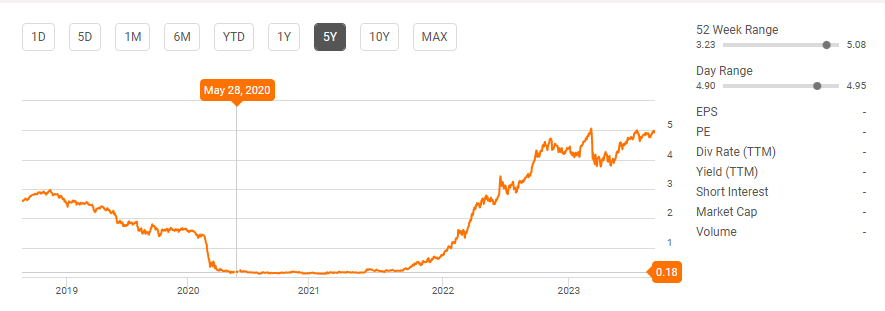

In May 2020, JEPI was launched and has grown into one of the largest high-yield ETFs in the market. JEPI debuted for $50 per share, and in just over 3 years, the fund has appreciated by 9.02% as it's added $4.51 to the share price. Generating a 9% return in just over 3 years may not seem like a great place to park capital, but at the time, risk-free assets such as the 2-year T-bill generated less than a .25% yield. We lived in a yield-starved environment, and risk-free assets only started becoming a viable option again in 2022. From an income perspective, generating a monthly distribution while seeing the underlying asset appreciate has been a lucrative income investment over the years through JEPI.

{kind=link}

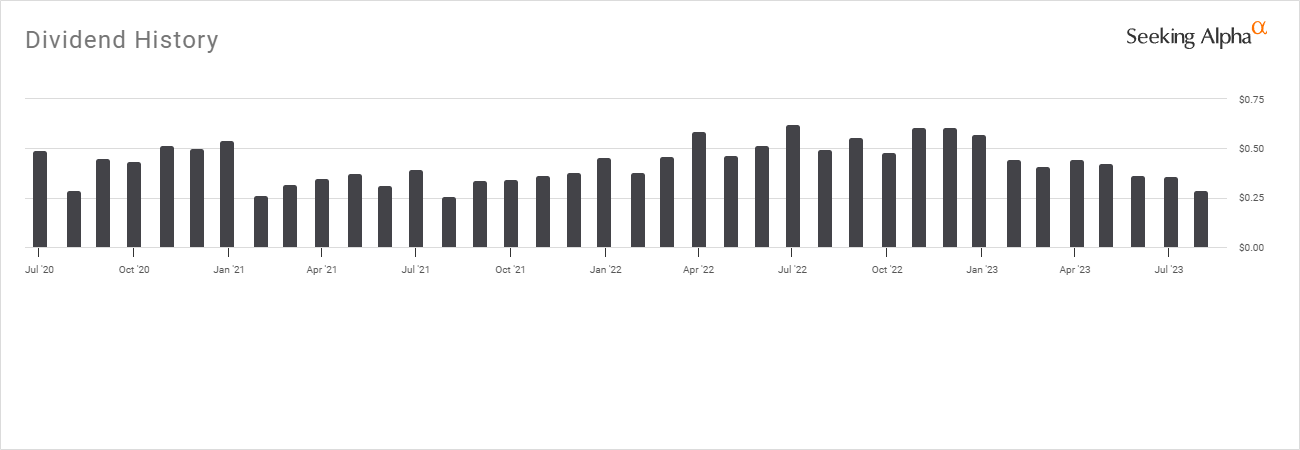

JEPI has generated 38 consecutive monthly distributions since going public. If you had purchased shares when it went public, each share would have generated $16.49 in distribution income. This is a 32.99% yield on capital that works out to an annualized yield of 10.42%. The price fluctuation in the distribution is normal, considering they are generating different amounts of premium from the covered call strategy based on the market volatility. Despite the fluctuations in the distribution, JEPI has delivered 9.02% in capital gains and 32.99% in distributions since going public, placing its total ROI at 42.01%. When you look at this on an annualized basis, JEPI has returned 13.27% on an annualized basis when combining its capital appreciation and distribution income since inception.

JEPI's track record now spans over 3 years, and there is no reason to doubt its ability to generate income. While its share price and income levels will fluctuate over time, it's been a strong income investment for investors. We live in a world where risk-free investments such as the 2-year are offering close to a 5% yield, making some equity investments less attractive. JEPI has become a strong alternative to risk-free assets as you are being paid more than double the yield to take on equity risk. JEPI continues to work in a high-yield environment, and I think more people will look toward JEPI when the Fed starts cutting rates and risk-free assets become less attractive.

{kind=link}

I think we're headed into a multi-year bull market and that JEPI will become more attractive than it already is.

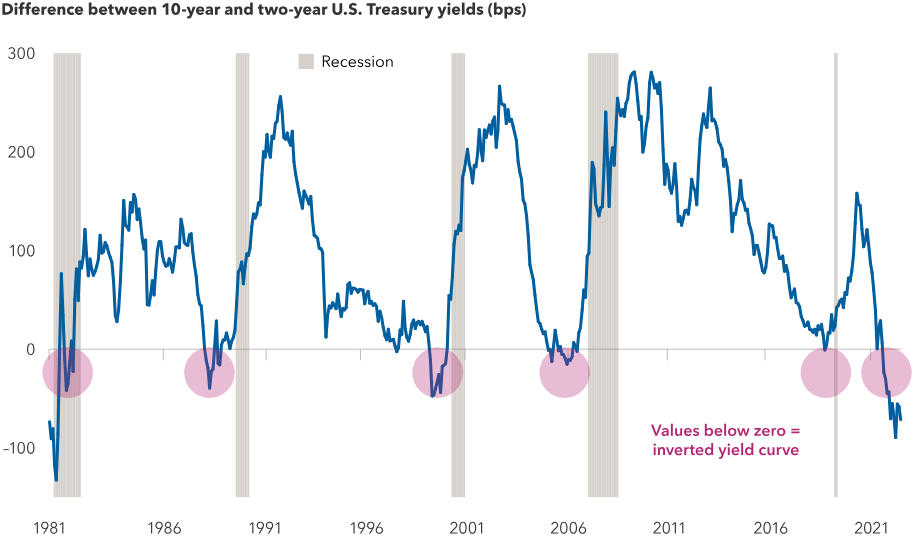

There continues to be increased discussions regarding a looming recession in the media. I have heard some analysts cite the inverted yield curve. When short-term rates are higher than long-term rates, you get an inverted yield curve as your being paid a higher rate for a shorter duration. Since 1981 an inverted yield curve has occurred at the beginning or right before a recession. While we have an inverted yield curve now, I don't believe we're headed into a recession based on other economic factors.

{kind=link}

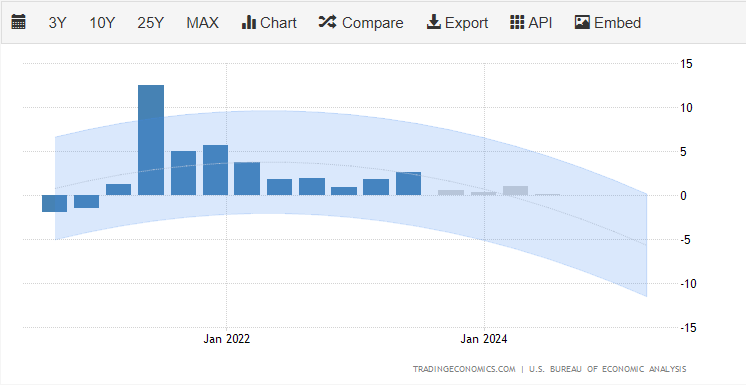

In order to have a recession, we need to see 2 consecutive quarters of negative GDP. We have seen positive GDP growth over the last 10 quarters, and the forecast going into 2024 is that we will see positive GDP growth over the next 4 quarters. The current forecast shows a downward slope, but there is no way to forecast accurately when the economy will be 6-8 quarters in the future, and this slope could easily change in the next 6 months.

GDP Forecast

{kind=link}

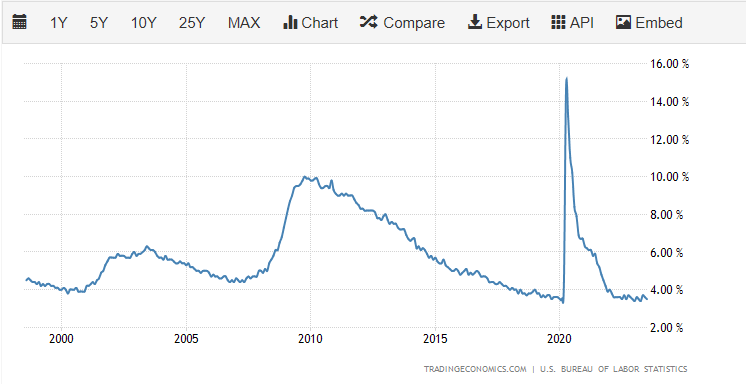

Every time we have seen negative GDP growth and a recession occur in the last 2 decades, we have seen unemployment surge above 5%. Despite the Fed increasing rates, the economy has remained strong, GDP has increased, and unemployment has stayed below 4%. We're not seeing unemployment anywhere near the 5% number, and it's very hard to have a recession when the job market is strong.

Unemployment

{kind=link}

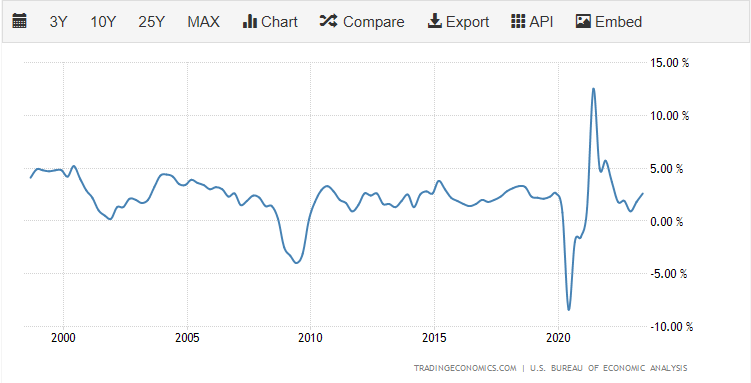

GDP

{kind=link}

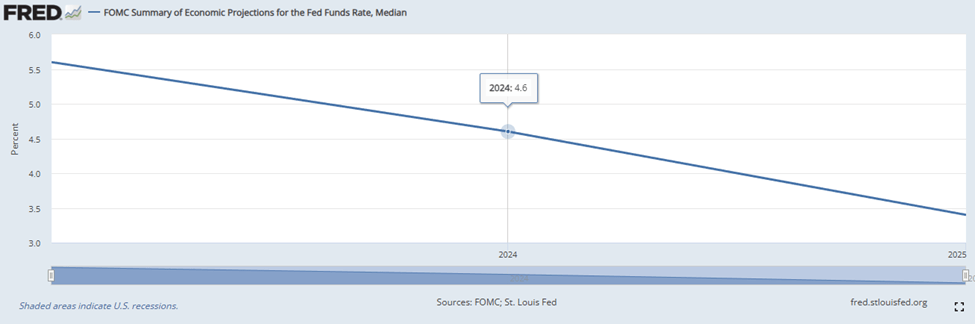

The St. Louis Fed indicates that rates will decline to 4.6% in 2024 and 3.4% in 2025. When rates start to decline, the cost of capital becomes cheaper, and we are likely to see expansion in business. When businesses go through an expansion cycle, it is typically beneficial to the labor market directly and indirectly, which creates a strong economy. Lower rates also improve personal finance, and individuals are more likely to spend as borrowing costs are lower.

Rates

{kind=link}

While the yield curve is inverted, too many other factors indicate we're not headed toward a recession. My feeling is that we're headed into a bull cycle, and JEPI will benefit greatly as its portfolio has an 80% allocation toward equities. Many of the companies in JEPI's portfolio will benefit from economic expansion, and I believe JEPI will continue to do well going forward.

Conclusion

I plan on adding more to my position in JEPI as time goes on. JEPI has established a strong track record of generating distribution income for its shareholders since its inception. I believe that JEPI will gain more popularity as short-duration risk-free assets mature, and some of that capital finds its way into the market over the next 2-years if rates decline in correlation to the St. Louis Fed projections. JEPI may not be suitable for everyone, but from an income perspective, it has outpaced inflation and the risk-free yield through its distributions and should continue to deliver large amounts of income in the future when rates decline.

For further details see:

JEPI Is One Of My Favorite Income Funds For The Foreseeable Future