JEPI - JEPI's Underperformance Explained

2023-08-20 04:24:37 ET

Summary

- JEPI is one of the most popular income ETFs in the market.

- The fund has underperformed the S&P 500, and most of its close peers, YTD.

- An explanation as to why follows.

The JPMorgan Equity Premium Income ETF (JEPI) has been one of the most popular, fastest-growing ETFs in recent history, and for good reason. The fund combines a strong 10.2% dividend yield, with the potential for moderate capital gains, and below-average losses during bear markets. It is a strong overall value proposition, especially for income investors and retirees.

JEPI had an outstanding 2022, outperforming most U.S. equity indexes, and most of its covered call equity peers. It has had a much more lukewarm 2023, underperforming relative to both YTD. JEPI's underperformance was due to the fund's reduced potential capital gains, product of its covered call strategy, and due to being underweight tech, which has performed exceedingly well YTD.

In my opinion, JEPI's underperformance is not indicative of strategic or fundamental issues with the fund, and so its overall value proposition and long-term expected returns remain quite strong. JEPI remains a buy, present weakness notwithstanding.

Equity Positions

JEPI invests around 80% - 90% of its assets in large-cap U.S. equities with strong fundamentals, including low volatility and high (expected) risk-adjusted returns. The result is broadly similar to that of most value and dividend ETFs, with sizable investments in most well-known mega-caps, as well as a tilt towards old-economy industries and away from tech (too volatile).

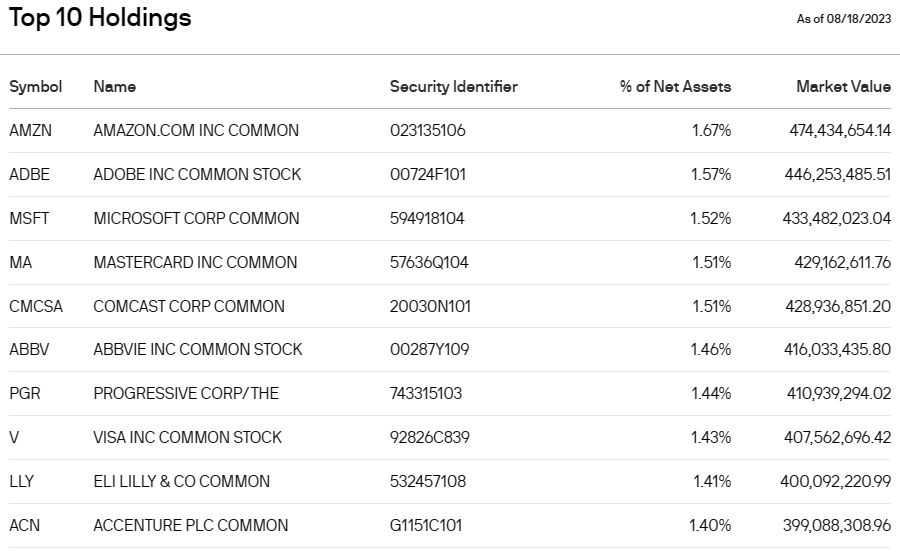

JEPI's largest holdings are as follows.

{kind=link}

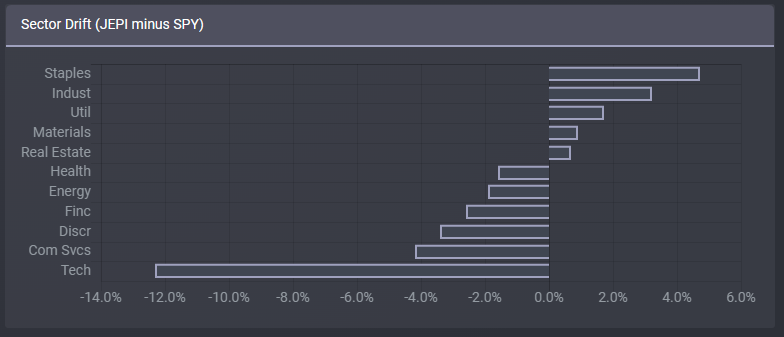

JEPI's industry exposures relative to the S&P 500 are as follows.

{kind=link}

JEPI's industry exposures have led to significant underperformance YTD, as the fund is underweight best-performing industries:

while being overweight some with below-average returns:

Subpar industry exposures have led to underperformance YTD. By my calculations, these are responsible for around half of the fund's underperformance:

Although JEPI's industry exposures have led to underperformance in the past, I don't believe that this will necessarily be the case in the future. This is because growth stocks and industries, including tech, remain somewhat overvalued. Current valuations do not support significant growth capital gains moving forward, so these seem unlikely, in my opinion at least.

JPMorgan Guide to the Markets

Being underweight tech like JEPI will, sometimes, lead to underperformance, as has been the case YTD. That does mean, however, that being underweight tech is a certain negative, nor will it necessarily lead to underperformance moving forward.

ELNs Positions

JEPI invests around 10-20% of its assets in equity-linked notes, or ELNs. Exposure is higher, as these are (effectively) leveraged investments. JEPI's ELNs are derivatives which provide exposure to S&P 500 returns plus written call options on the same. As per the fund's prospectus : ELNs in which the Fund invests are derivative instruments that are specially designed to combine the economic characteristics of the S&P 500 Index and written call options in a single note form.

JEPI's ELNs serve to boost the fund's dividend yield to 10.2%, but moderately decrease potential capital gains. The net effect tends to be positive when capital gains are low, negative when these are high. Equity capital gains have been very high YTD, with the S&P 500 up almost 14.1% YTD, over 22% annualized. JEPI's ELNs reduce these gains and, as these have been incredibly massive, the result has been for the fund to underperform.

Although it is impossible for myself to calculate the exact impact these ELNs have had on the fund, it is possible for me to have a rough estimate. The Global X S&P 500 Covered Call ETF (XYLD) uses a similar covered call strategy to JEPI, but without ELNs, and without focusing on stocks with strong fundamentals and low volatility. XYLD has underperformed the S&P 500 by 6.7% YTD, due to its covered call strategy.

JEPI, on the other hand, has underperformed the S&P 500 by 9.2% YTD.

From the above, it seems that JEPI's covered call strategy led to around 6.7% in underperformance, as per XYLD's results, and its equity strategy led to the remaining 2.5%. JEPI's covered call strategy almost certainly led to less than 6.7% in underperformance, considering some other smaller differences between JEPI and XYLD (the former does not overwrite its entire portfolio, and the calls are slightly more out of the money).

JEPI's covered call strategy reduces potential capital gains. As equities mostly go up, the strategy is likelier than not to result in long-term underperformance for the fund moving forward, in my opinion at least. Although this is undoubtedly a negative, in my opinion the fund remains a buy, for two reasons.

First, is the fact that JEPI's long-term performance track-record remains adequate, with the fund only underperforming somewhat since inception.

Importantly, almost all of the fund's underperformance was in 2021, during which tech rallied. Performance is much stronger for other time periods, with the fund sometimes outperforming too.

As an example, looking at some of my past articles on JEPI, it seems that the fund has outperformed the S&P 500 three times out of four, including the first time I covered the fund.

JEPI

JEPI has underperformed YTD, but the fund's overall performance track-record remains more than adequate enough, and lots of JEPI's investors have done very well for themselves. Recent losses are, off course, regrettable, but the long-term results are adequate enough.

Second issue with the fund's recent losses, is the fact that equity capital gains have been incredibly strong YTD, and these are unlikely to persist long-term. The S&P 500 has seen annualized returns of more than 20% YTD. JEPI does underperform under these conditions, but these conditions rarely persist long-term (equities have not posted 20% returns long-term). As such, current conditions, including JEPI's recent underperformance, are not particularly representative of what investors should expect moving forward, in my opinion. More aggressive, bullish investors might disagree, at least in the short-term.

Conclusion

JEPI has underperformed YTD due to its reduced potential capital gains, product of its covered call strategy, and due to being underweight tech, which has performed exceedingly well YTD. In my opinion, JEPI's underperformance is not indicative of strategic or fundamental issues with the fund, and so the fund remains a buy.

For further details see:

JEPI's Underperformance Explained