XYLD - JEPI Vs. DIVO: One Is The Ultimate High-Yield Retirement Dream ETF

2023-06-17 07:45:00 ET

Summary

- Covered call ETFs are a potentially great choice for certain kinds of investors seeking high income and low volatility in tax-deferred accounts.

- JPMorgan Equity Premium Income ETF is the most popular high-yield ETF in this space and for good reason. JEPI management is guiding for 8% long-term returns, 80% of the S&P's with 35% lower volatility.

- Amplify CWP Enhanced Dividend Income ETF is a 5-star rated alternative that has historically delivered superior returns to JEPI. BUT there are several very important facts you need to know before buying the DIVO ETF.

This article was published on Dividend Kings on Wed, June 14th.

---------------------------------------------------------------------------------------

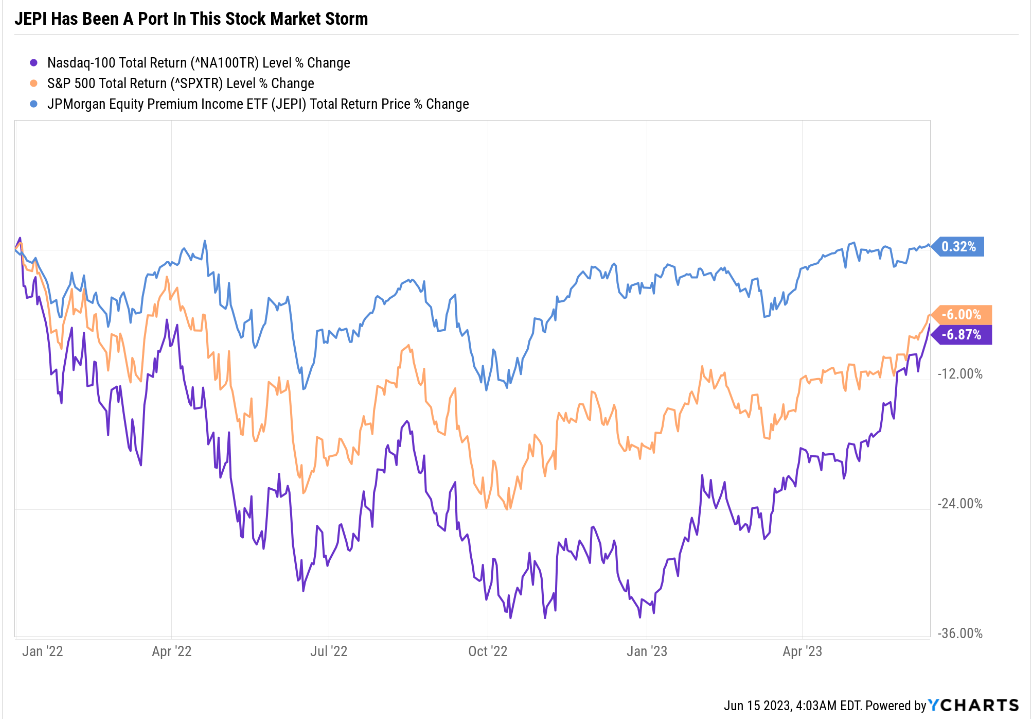

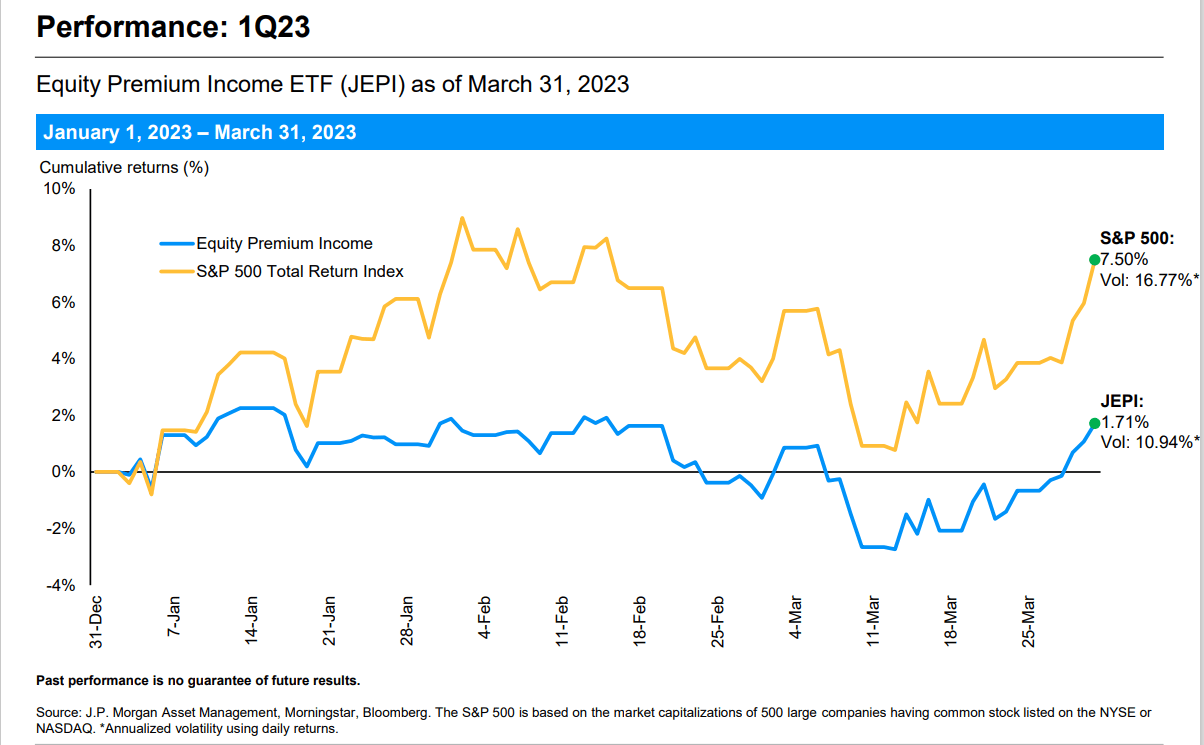

JPMorgan Equity Premium Income ETF (JEPI) was one of the most popular exchange-traded funds ("ETFs") of 2022, and for good reason. It's been a low volatility port in the storm, harnessing the market's high volatility to generate 12% income, paid monthly.

{kind=link}

As I explained in this deep dive introductory article, JEPI is the gold standard of covered call high-yield ETFs.

And that's not just from me, but from my accountant, from a tax perspective!

{kind=link}

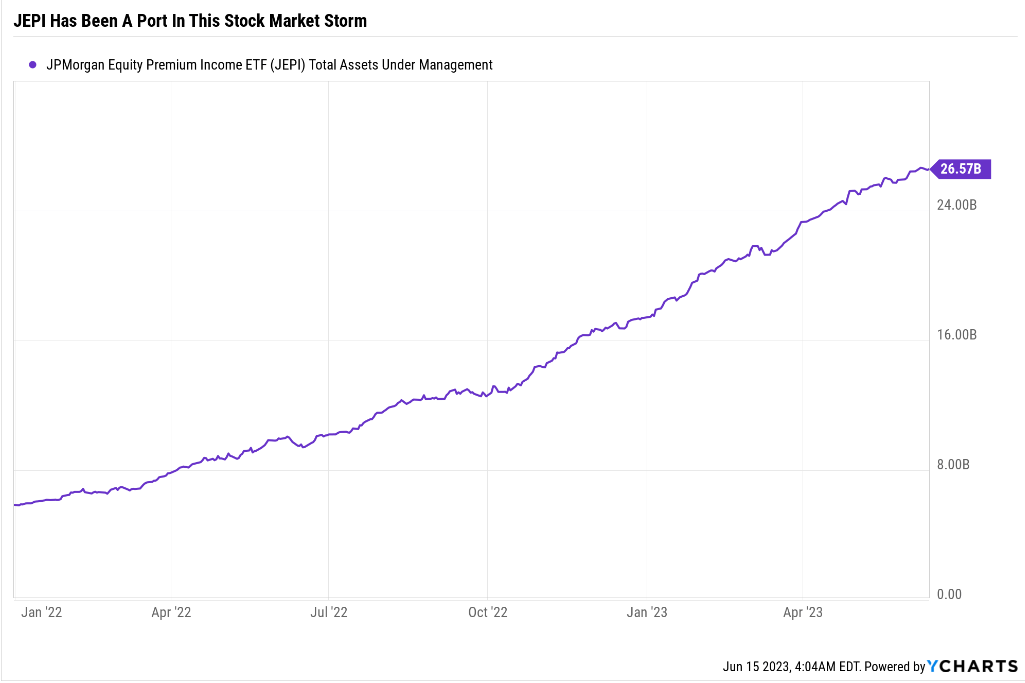

Since the bear market began, JEPI's assets under management are up 352%.

Naturally, JEPI is a highly specialized ETF tailored for three kinds of investors, and is a perfect choice for two kinds of investors.

But in my never-ending quest to research world-beater ETFs for my own needs and those of Dividend Kings members, I come across great alternatives to our favorite gold standard ETFs.

{kind=link}

During my latest ETF screening session, searching for 5-star ETFs to test head-to-head with "gold standard" ETFs, I came across Amplify CWP Enhanced Dividend Income ETF (DIVO).

This is an ETF that several Dividend Kings members have asked me about, so here is a perfect opportunity to challenge the current king of high-yield retirement account ETFs against a potentially better option.

The great thing about such head-to-head comparisons is that no matter who comes out on top, the winner is the best ETF you can buy.

So let's take a look at how DIVO stacks up to JEPI for the title of the ultimate high-yield dream retirement account ETF.

JEPI: The Reigning Champion

{kind=link}

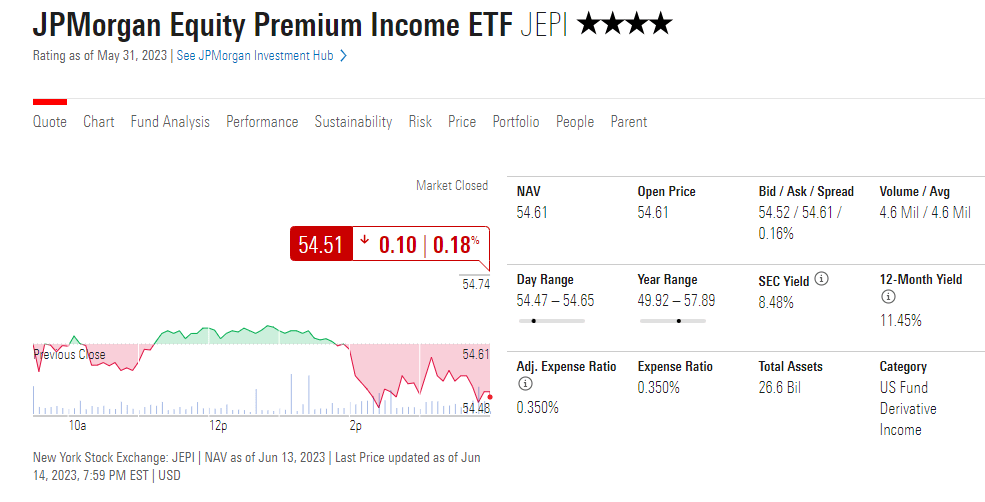

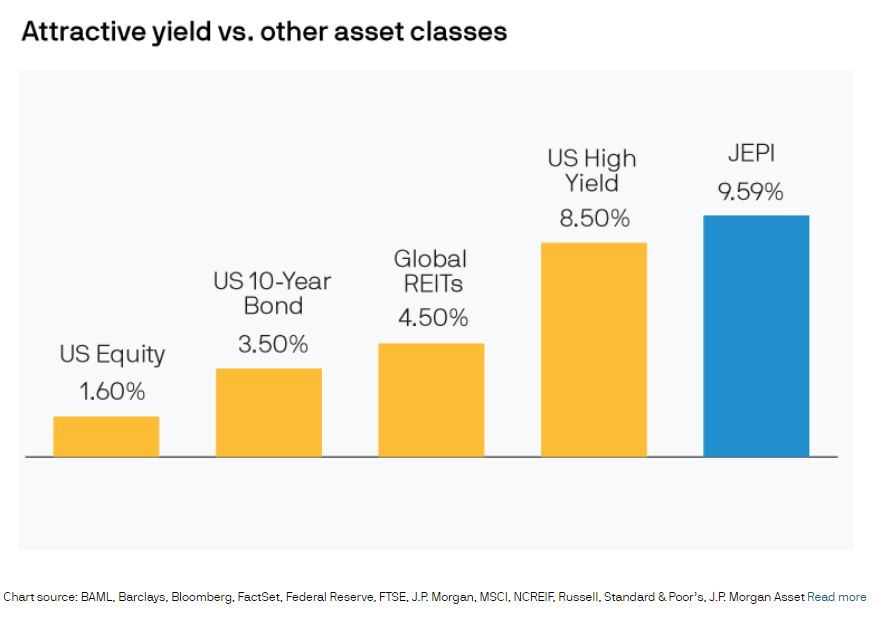

JEPI's yield is down to 8.5% based on its most recent dividend payment, which is what you should expect in a freakishly low volatility environment. It's down to a 4-star rated ETF, according to Morningstar .

{kind=link}

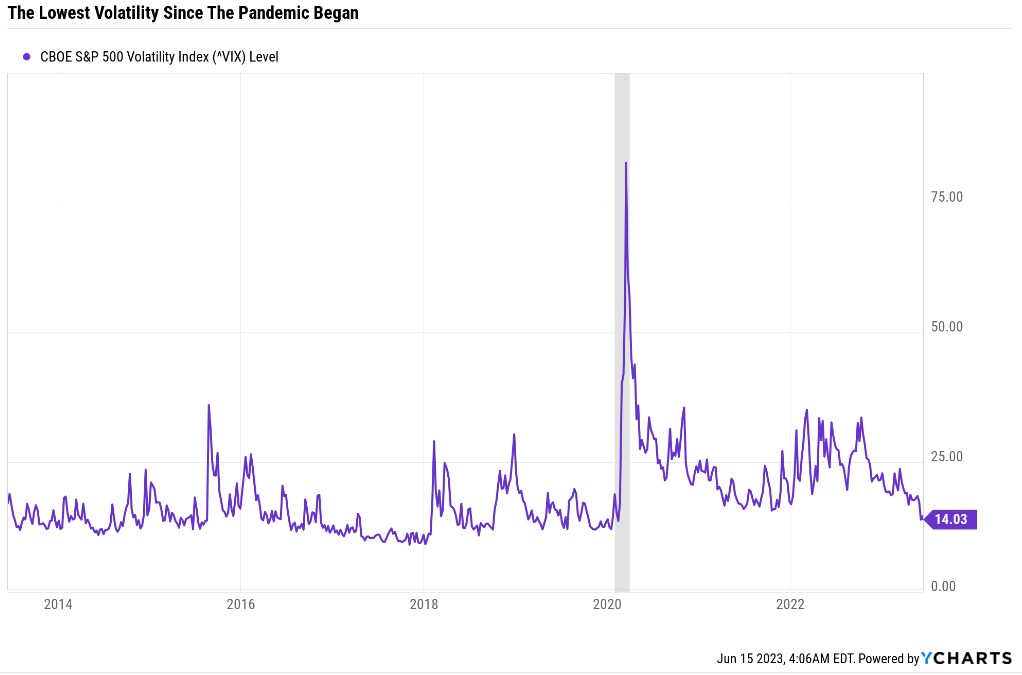

We're headed into a recession, and yet market volatility has collapsed.

{kind=link}

Compared to other income alternatives, JEPI remains an attractive 4-star option.

Why does Morningstar rate it four stars? Because its historical returns are in the 4th quintile, the top 21% to 39% of its peers.

{kind=link}

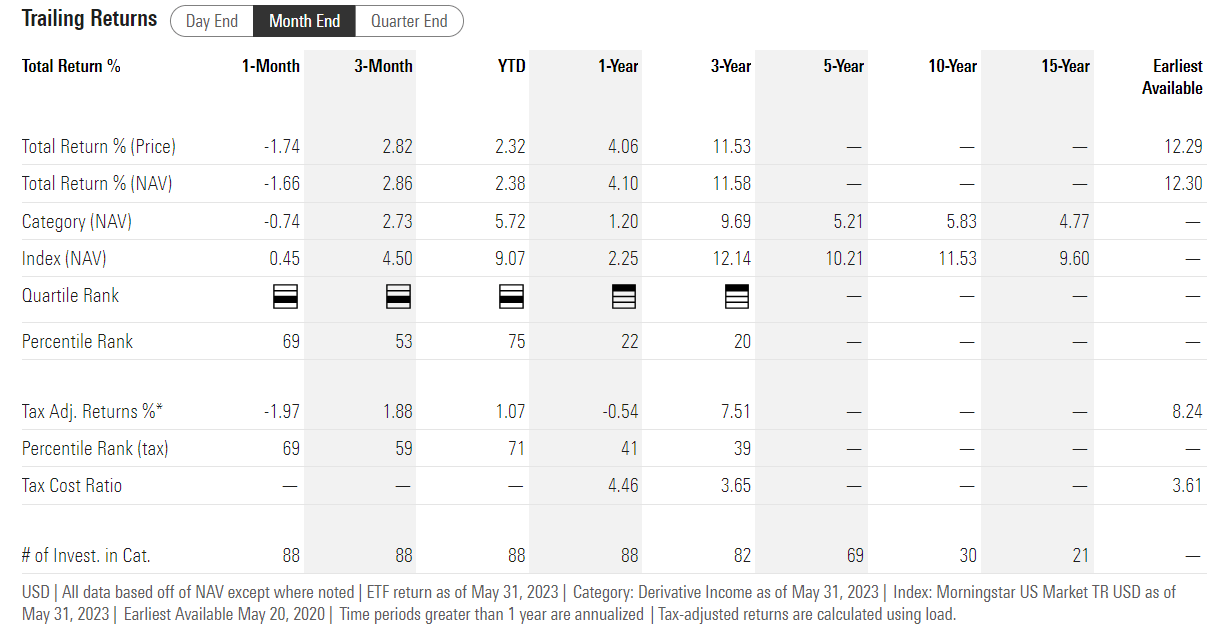

JEPI's historical return since inception is 12.3%, or 8.2% adjusted for taxes.

In the last three years, its 11.5% annual return puts it in the top 20% of its peers, and its tax-adjusted 7.5% return puts it in the top 39% of peers.

{kind=link}

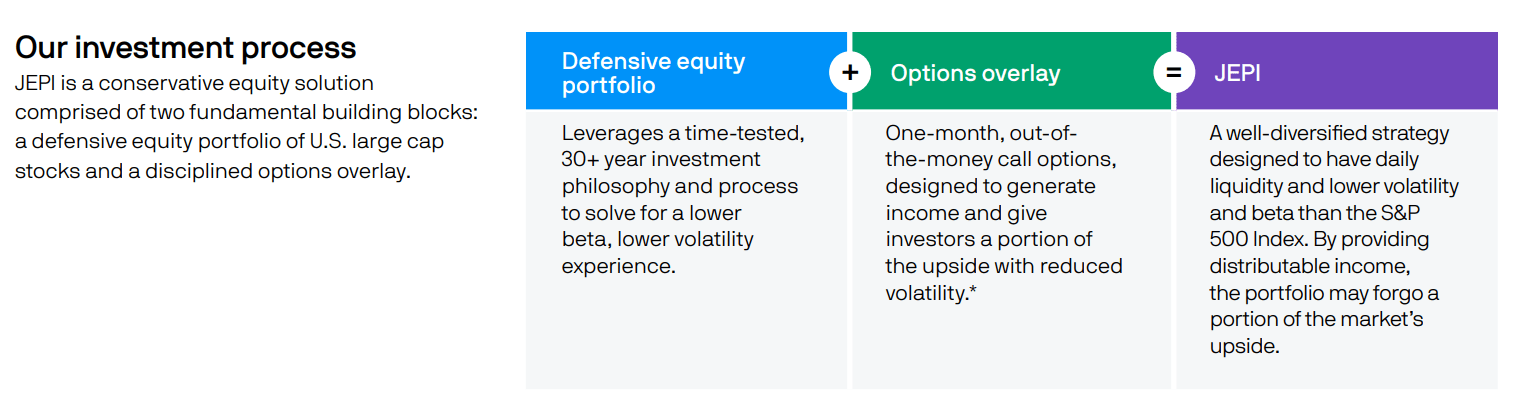

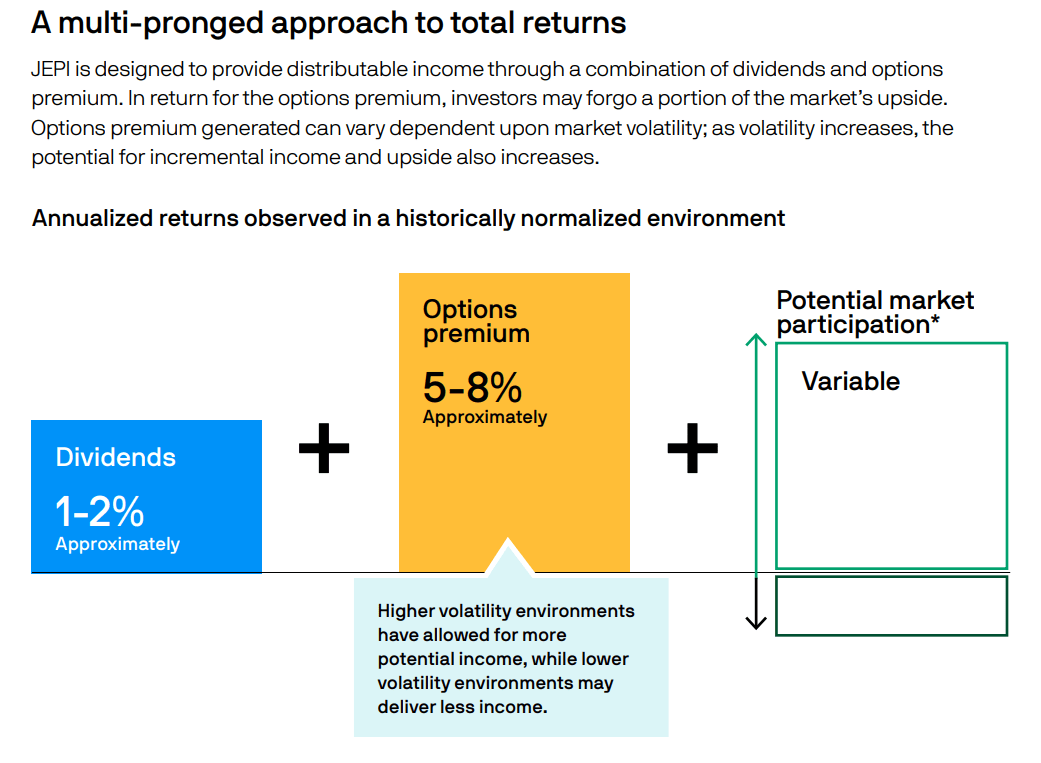

JEPI's managers use an underlying low-volatility blue-chip portfolio combined with one month out of the money options, specifically, exchange-traded notes ("ETNs," 15% of the portfolio), to generate 5% to 8% annual income.

{kind=link}

Per management guidance, the result is a 6% to 10% return ETF before taxes.

Or, to put it another way, according to management, JEPI is designed to offer about 80% of the market's returns with 65% of volatility and high monthly income.

{kind=link}

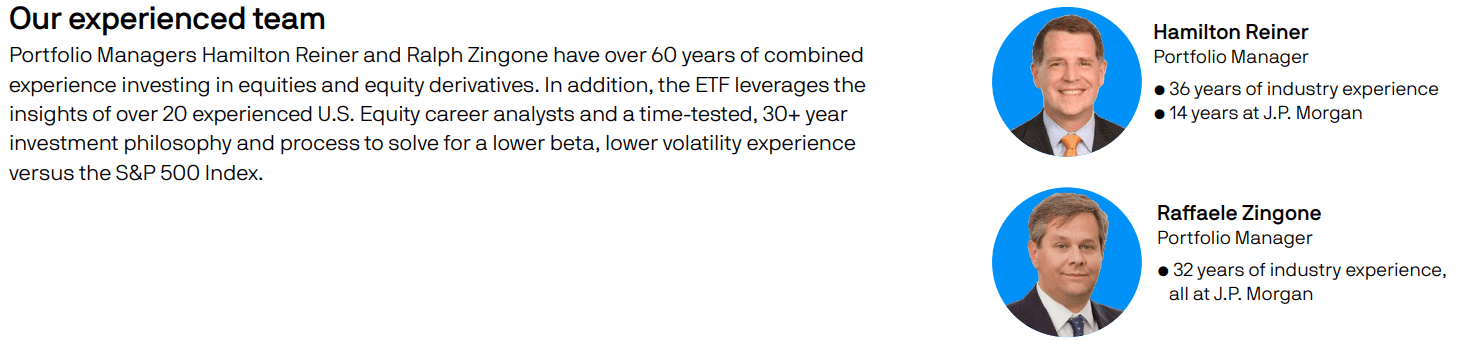

Speaking of management, here is who is running JEPI, with over 60 combined years of experience in options, covered calls, and exchange-traded notes.

{kind=link}

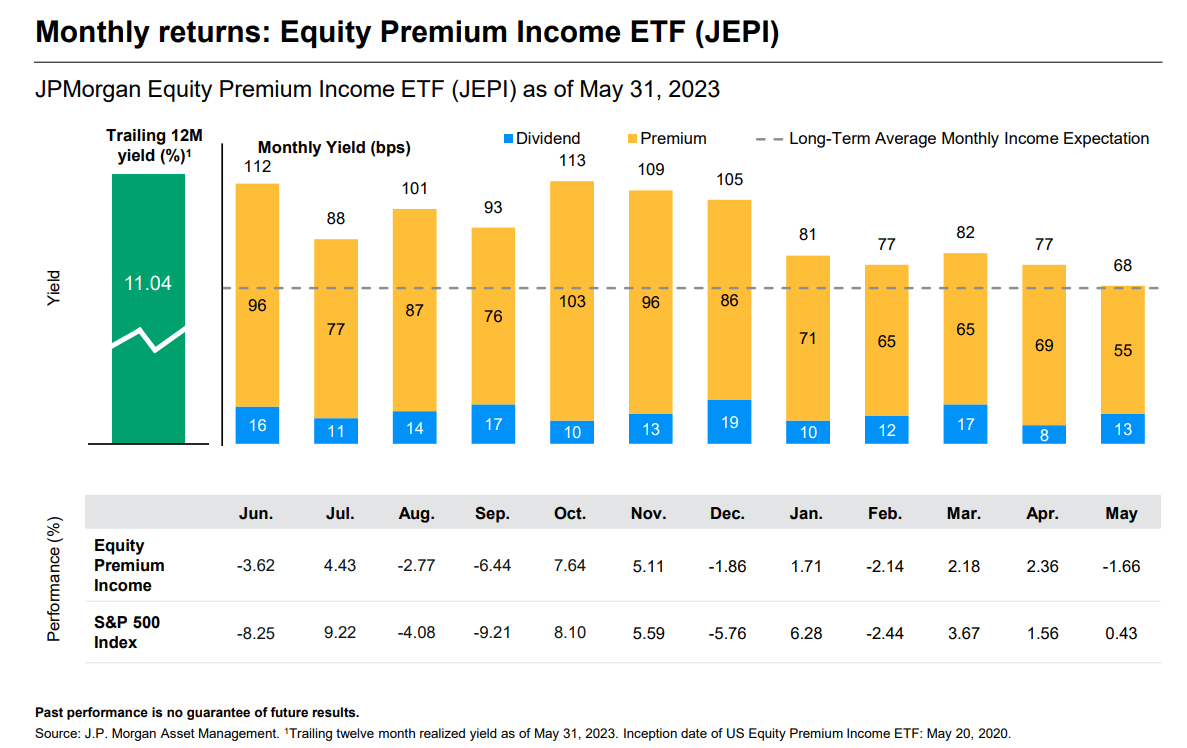

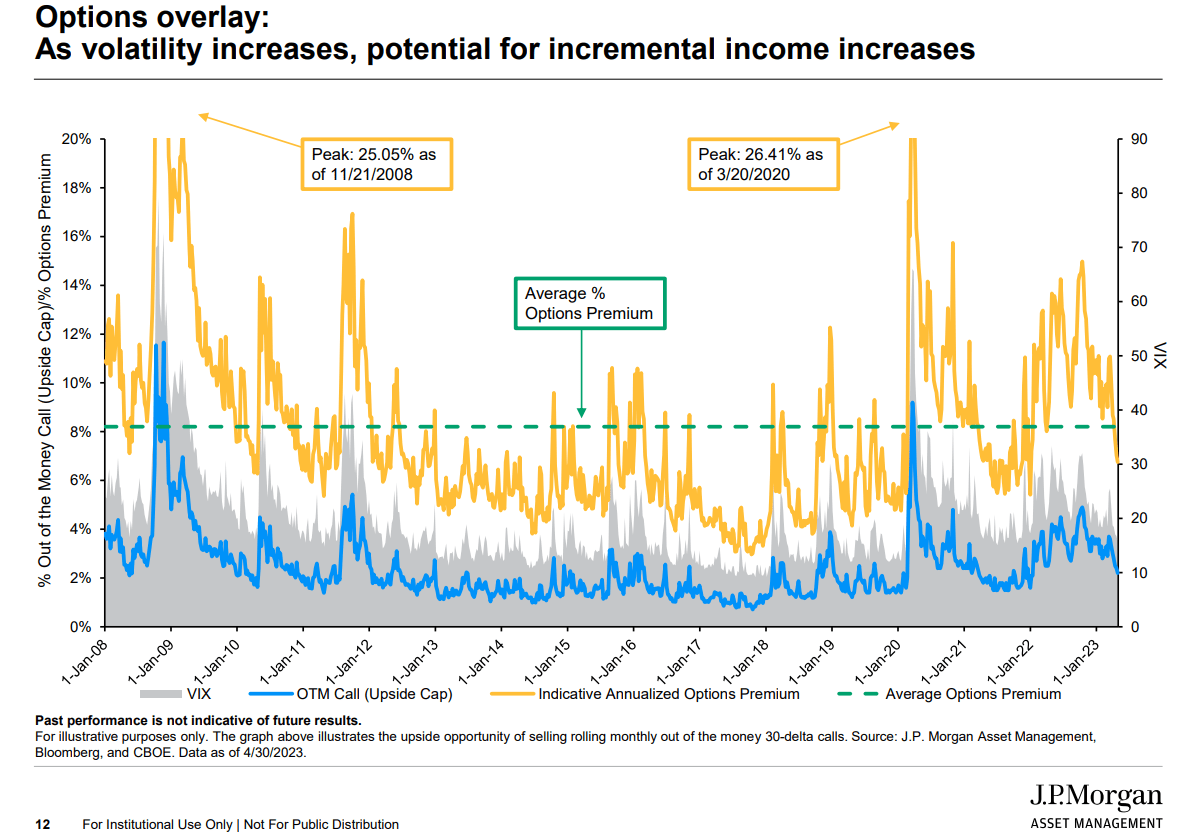

With 15% of the portfolio invested in ETNs, JEPI is able to achieve remarkable monthly income.

The expertise to safely do this (at least so far) is what investors pay JPMorgan 0.35% per year for.

Notice the peak monthly yield in October, the current bear market bottom.

Management guidance is for 6.5% annual income from ELNs over the long term or 54 basis points per month.

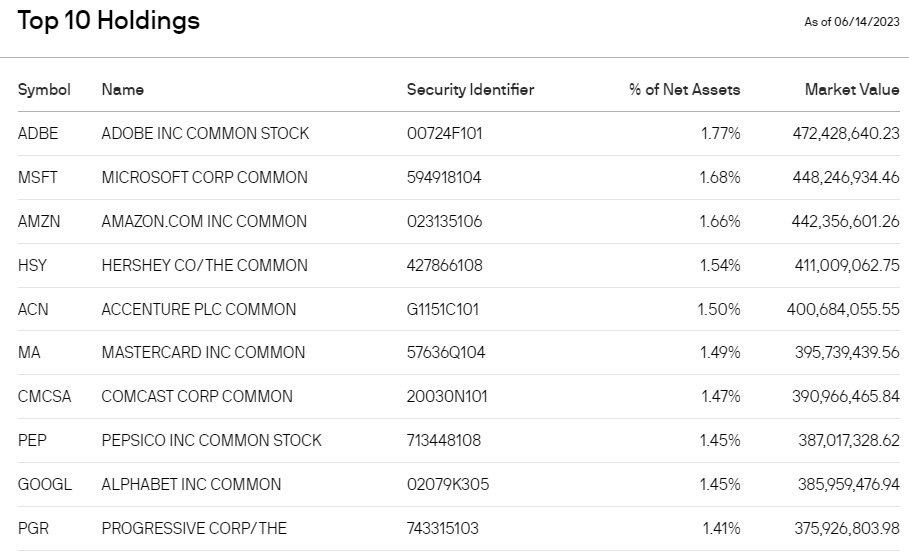

What JEPI Owns Today

{kind=link}

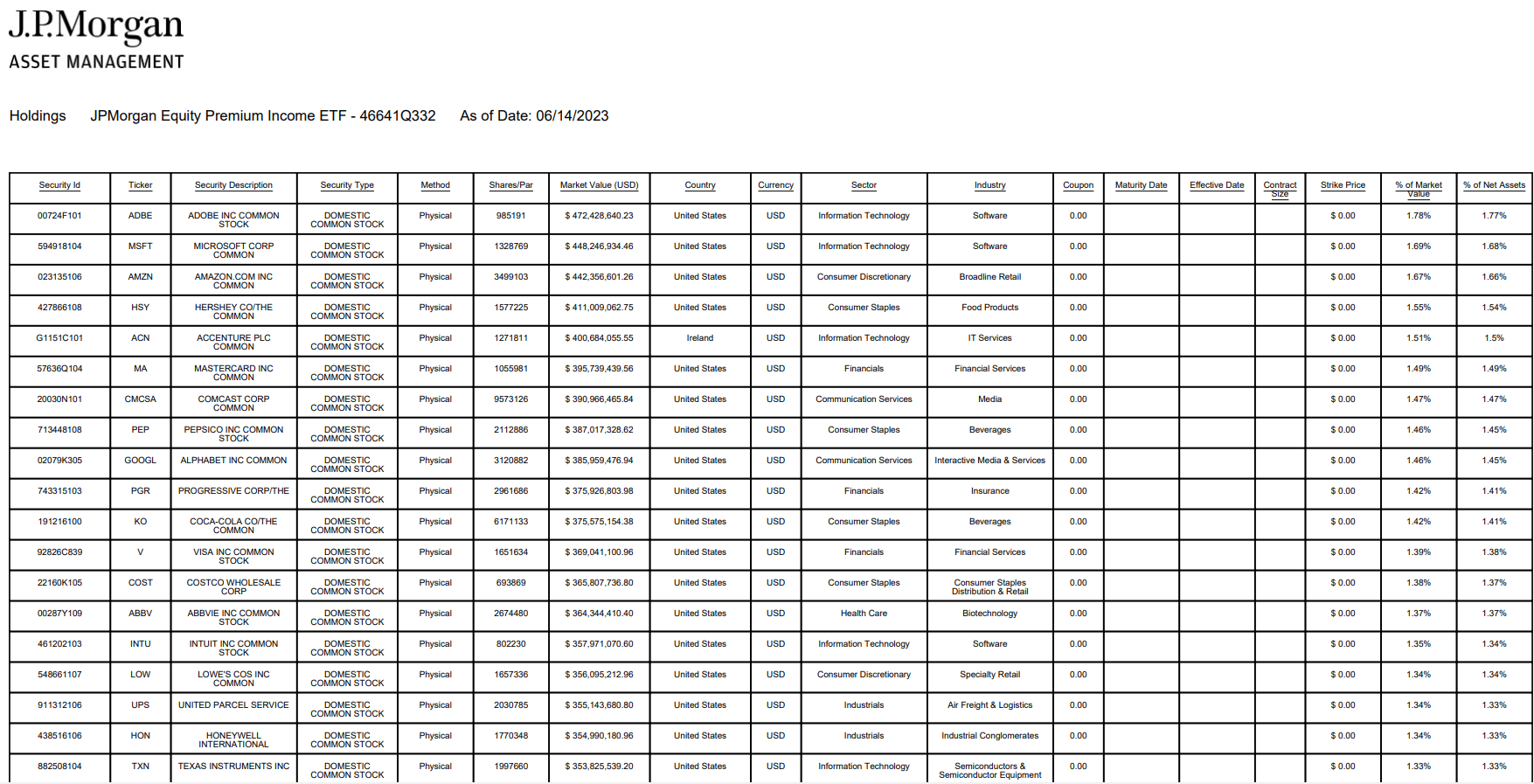

JEPI is actively managed for low volatility, and in today's AI-tech bubble, that means a lot of tech stocks. JEPI currently owns 118 stocks in total.

{kind=link}

Note the 195% turnover is sky-high because of the monthly options and active management.

That's why the historical tax cost ratio is 3.6%.

- Since its 1993 inception, SPY (S&P 500 ETF) has averaged a 0.59% tax expense ratio

- 2% annual turnover.

{kind=link}

Including true tech (AMZN and TSLA are consumer cyclical, and GOOG, NFLX, and META are communications), JEPI is currently 33% tech.

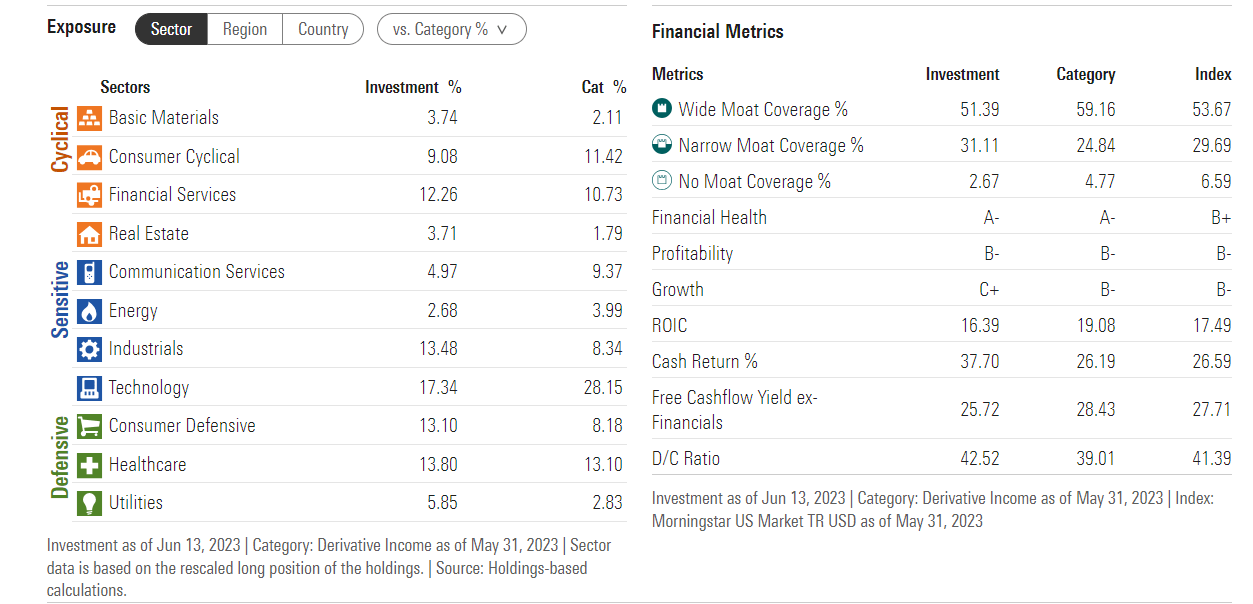

Thus, it's a very wide moat, with A-rated financial strength scores and 26% free cash flow margins. This is a world-beater Super SWAN portfolio.

It's likely this will make for much higher volatility in the coming 25% to 30% decline.

S&P Bear Market Bottom Scenarios

| Earnings Decline |

| S&P Trough Earnings |

| Historical Trough P/E Of 14 (13 to 15 range) |

| Decline From Current Level |

| Peak Decline From Record Highs |

| 0% (Mildest recession in blue-chip history consensus) |

| 232 |

| 3243 |

| 25.8% |

| -32.7% |

| 5% (Mild recession consensus) |

| 220 |

| 3080 |

| 29.6% |

| -36.1% |

| 10% |

| 208 |

| 2918 |

| 33.3% |

| -39.4% |

| 13% |

| 202 |

| 2821 |

| 35.5% |

| -41.5% |

| 15% |

| 197 |

| 2756 |

| 37.0% |

| -42.8% |

| 20% |

| 185 |

| 2594 |

| 40.7% |

| -46.2% |

(Source: Dividend Kings S&P 500 Valuation Tool, FactSet, Bloomberg.)

Mike Wilson, the Chief Investment Officer of Morgan Stanley, has recently lowered his S&P 500 (SP500) bottom forecast to 3,400.

Think Wilson is overly bearish? His 12-month forward EPS forecast on S&P is 215, so that's a 15.8X trough P/E, and he doesn't think it will be a recession, just a 20% decline in earnings from margin compression.

So far, the bottom trough P/E was 15.5, historically 13 to 15. He's not actually bearish. It's just that everyone else is wildly bullish;)

But that coming volatility could result in record yield for JEPI, but of course, the stock portion of the portfolio is likely to decline.

- JEPI isn't a bond alternative.

{kind=link}

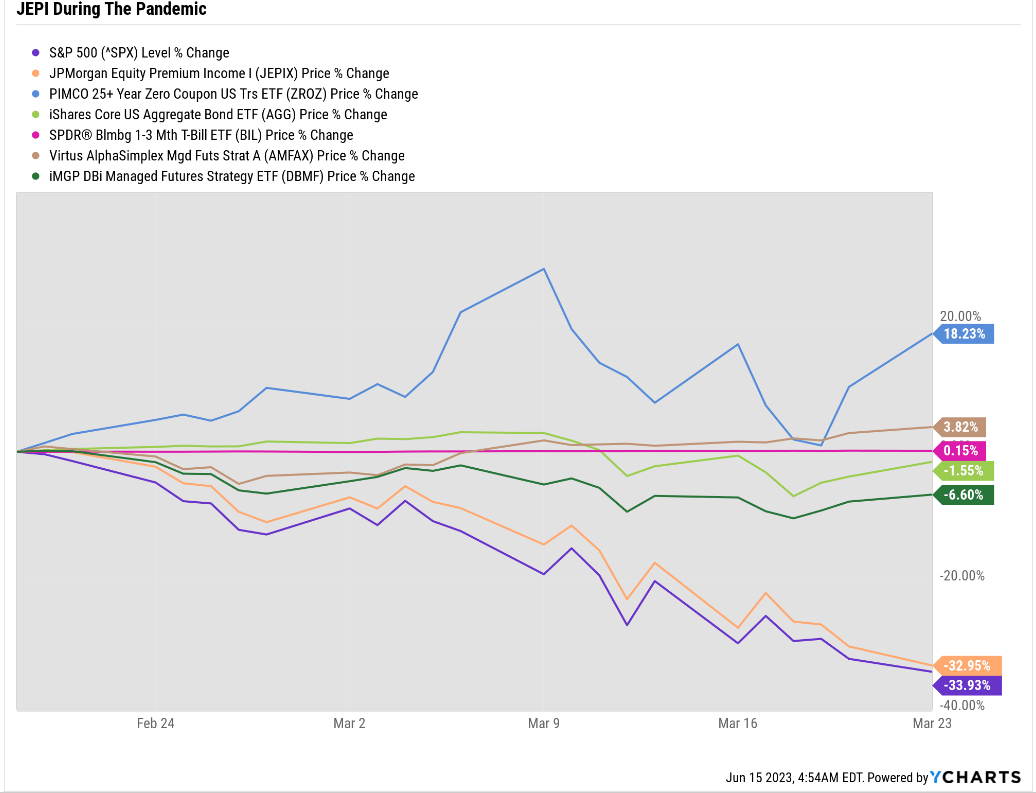

At peak volatility during the Pandemic, JEPI's yield would have been 26% had that volatility persisted for 12 months.

{kind=link}

JPMorgan Equity Premium Income Fund Inst (JEPIX) is the mutual fund version of JEPI and is run by the same managers with the same strategy. It shows that had JEPI been around in the pandemic; it would have fallen 33%, as much as the S&P.

So that 26% annual option yield would have resulted in -7% returns compared to the market's -34%.

- 80% less volatility than the S&P in a time of maximum market panic.

IF YOU THINK JEPI WILL MAKE MONEY IN A BEAR MARKET, YOU ARE WRONG. IT IS NOT A BOND ALTERNATIVE.

{kind=link}

And don't forget that JEPI was built for 66% to 80% of the market's long-term returns over time with 35% lower volatility.

IF YOU THINK JEPI WILL BEAT THE S&P OVER TIME, YOU ARE WRONG. IT IS NOT AN S&P Alternative.

JEPI is amazing at what it does, but it is not right for everyone. In fact, only three kinds of investors should ever consider owning it.

Three kinds of investors can or should own JEPI as a great or ideal choice.

- Only own JEPI in a tax-deferred account (a good to a great choice in this case)

- Roth IRA investors who want a single stock retirement plan with better returns, yield, and lower volatility than a 60/40 (perfect solution)

- Tax-deferred (401K, IRA, 403B) investors who want a single stock retirement plan better than the 60/40 AND plan to donate their entire account to charity (perfect solution)

If you're one of these three kinds of investors, then JEPI is a potentially good or even ideal solution for your needs.

If you're not one of these three kinds of investors, then avoid JEPI.

DIVO: The Challenger For The Throne

{kind=link}

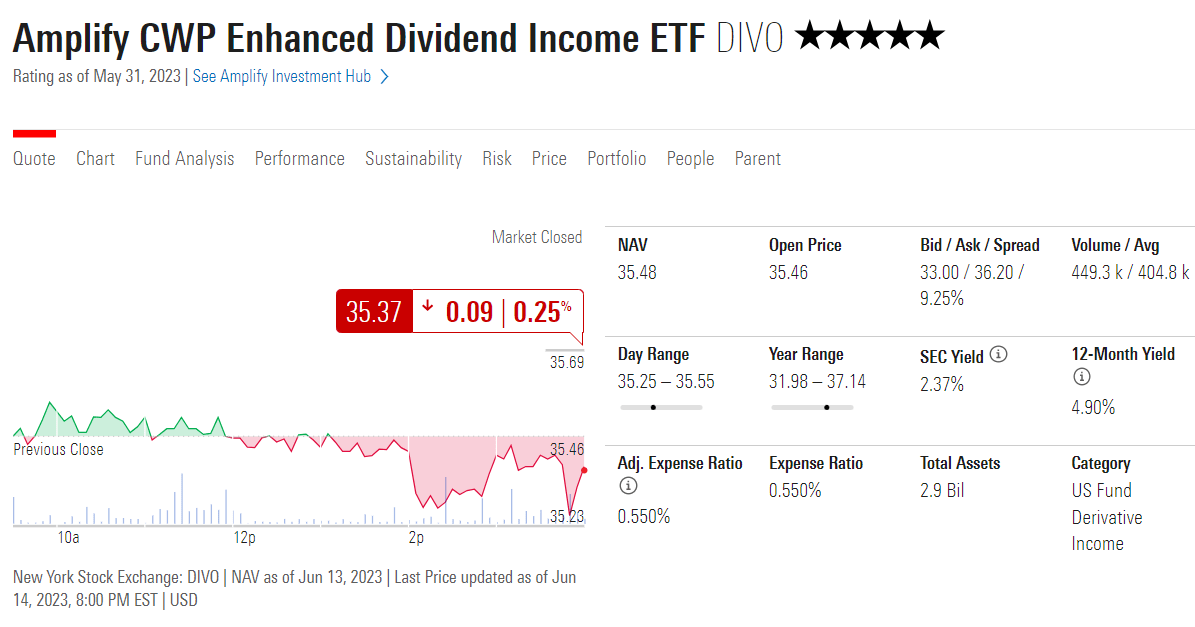

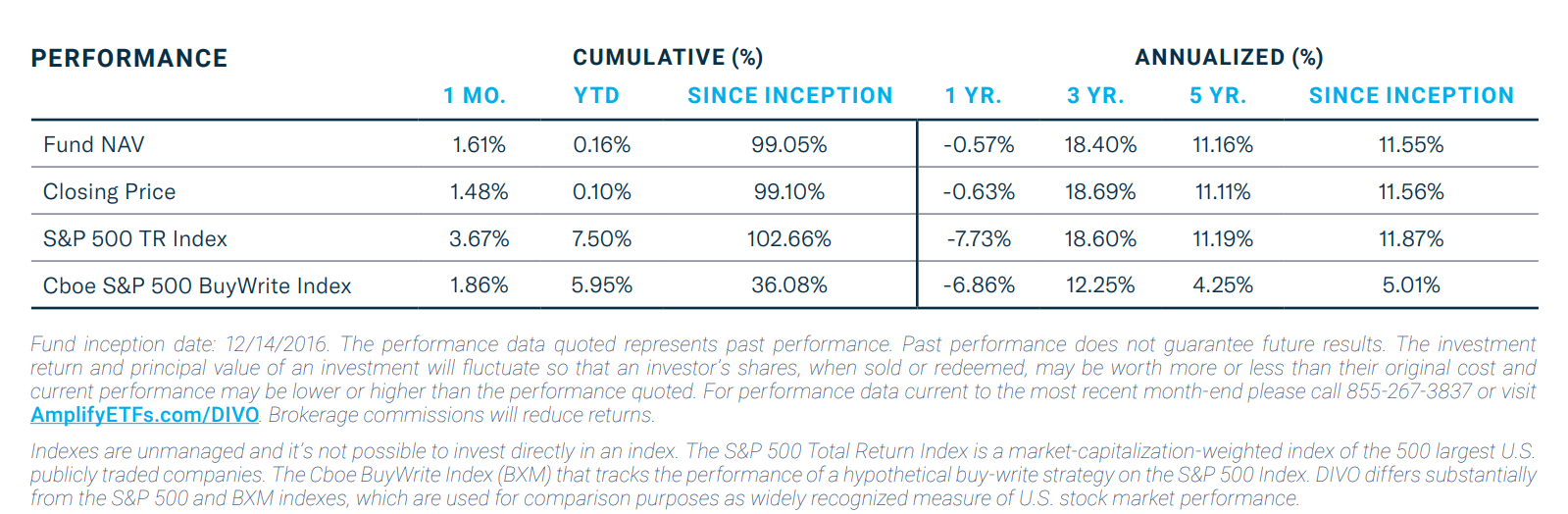

So we can see that DIVO is a 5-star rated ETF, better than JEPI, though we'll have to check how long it's been around. The yield is much lower, and the expense ratio is 0.55% or 0.2% more than JEPI.

{kind=link}

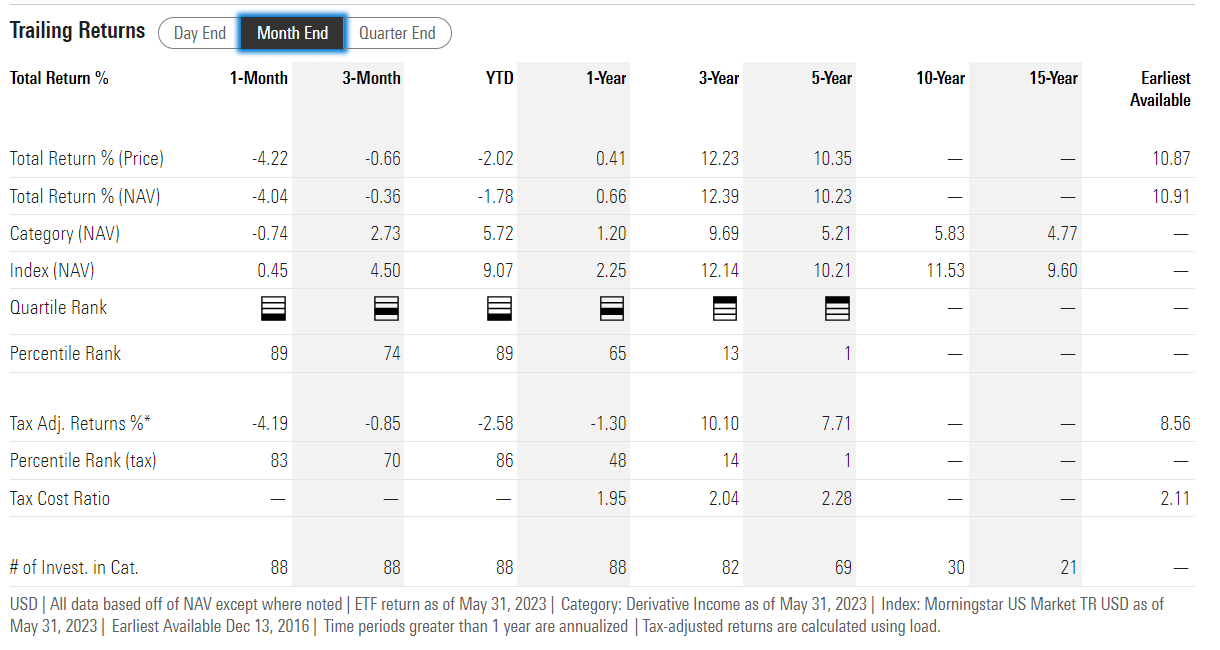

DIVO has been around since December 2016, older than JEPI or JEPIX, and has delivered 10.9% annual returns or 8.6% after taxes.

In the last five years, it was in the top 1% of its peers for both total returns and tax-adjusted total returns.

So DIVO is bringing the heat, and so far, it looks like a very worthy contender to JEPI.

{kind=link}

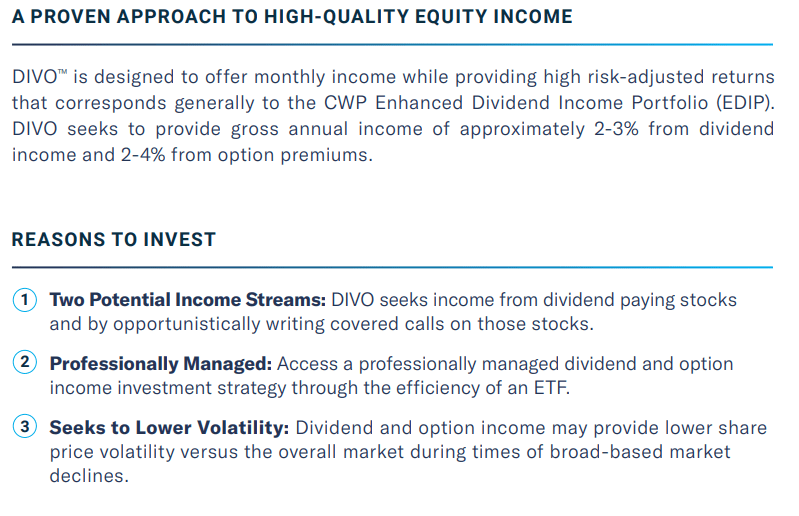

DIVO is designed to deliver 4% to 7% long-term returns.

{kind=link}

Since its inception, the covered call index has delivered 5% returns, and DIVO is designed to beat that slightly.

It's managed to crush its peers, and thus the 99th percentile returns and a 5-star rating from Morningstar .

{kind=link}

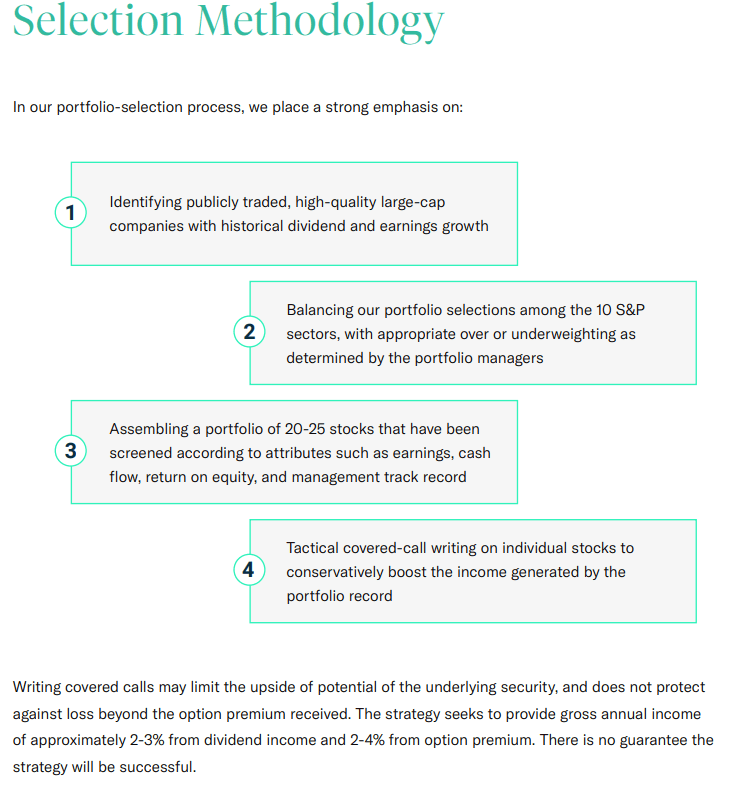

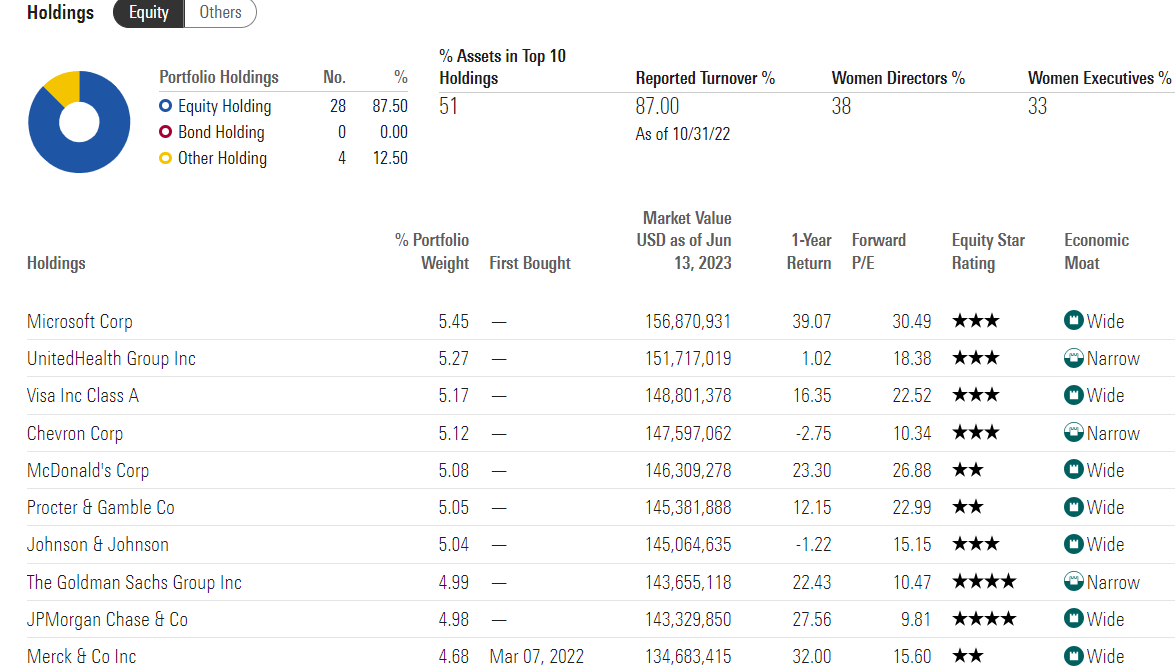

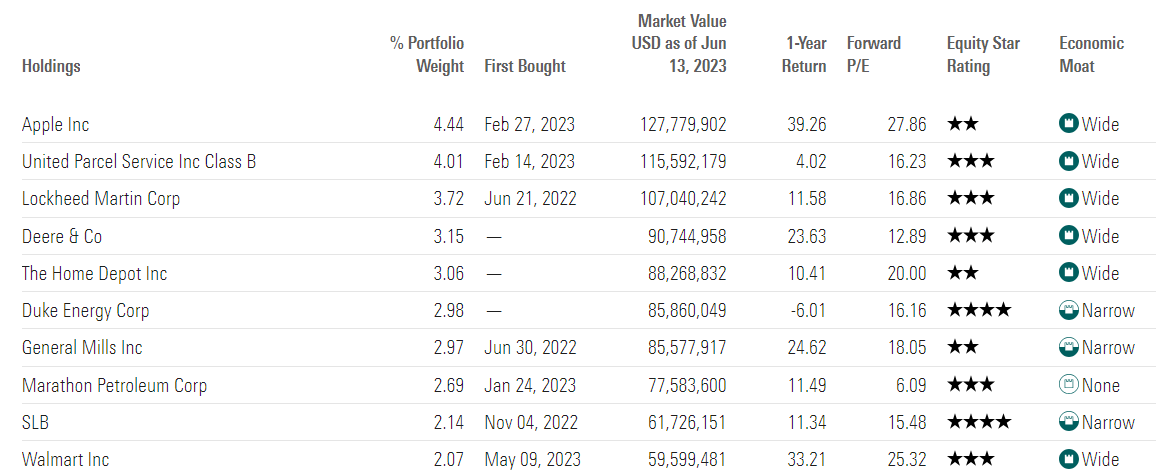

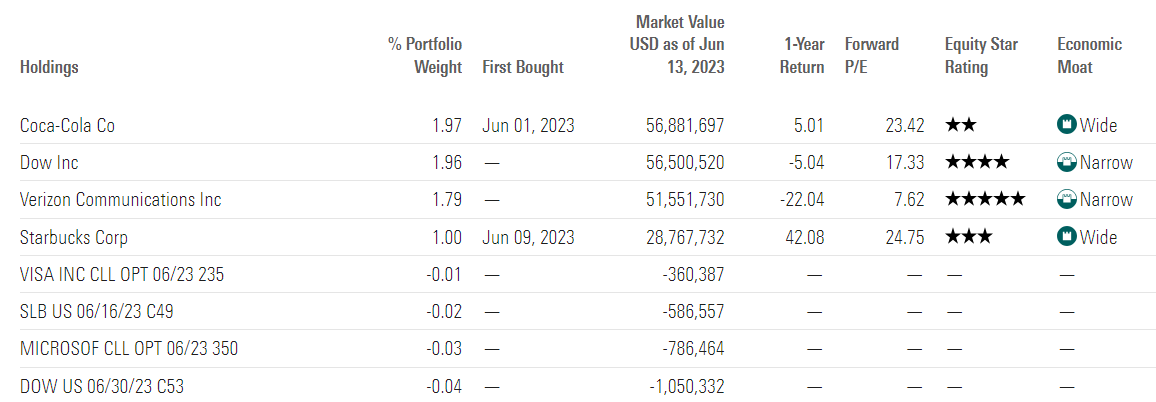

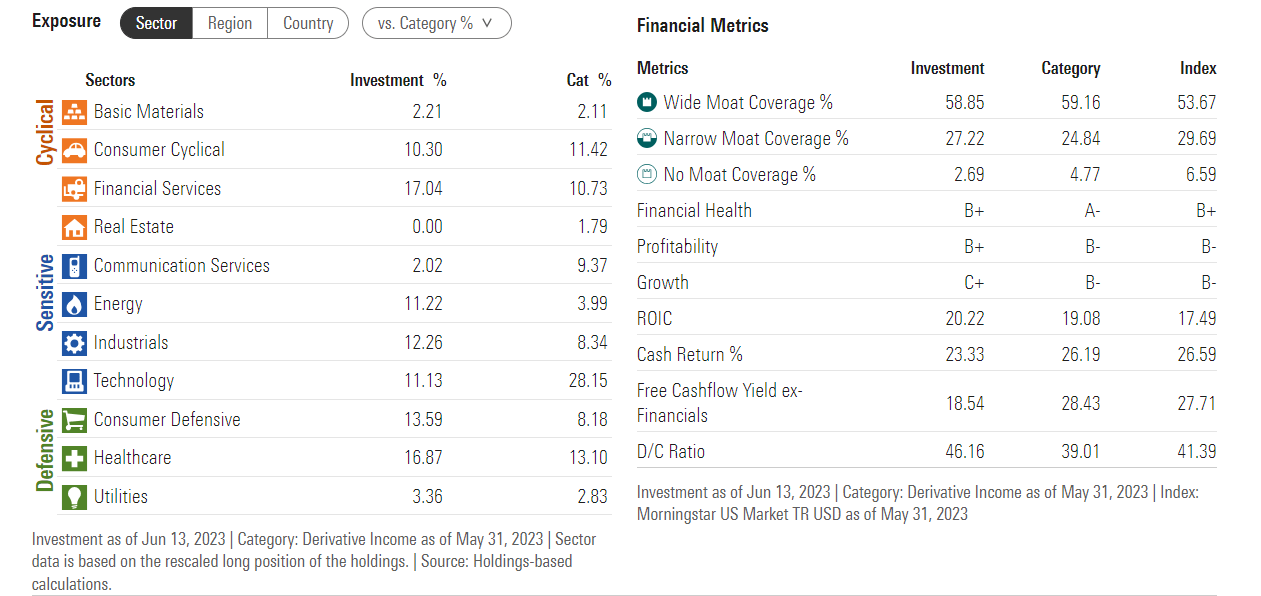

DIVO uses a sound overall strategy, though it runs a concentrated portfolio currently consisting of 28 stocks.

Morningstar Morningstar Morningstar

{kind=link}

{kind=link}

{kind=link}

The turnover is much lower than JEPI's 195%, and that's why the historical tax expense ratio is 2.11%, or about 65%, that of JEPI.

- 19% of historical returns go to taxes

- vs. 29% for JEPI.

{kind=link}

Historical Returns/Future Expected Returns

DIVO Portfolio Future Return Potential (Excluding Covered Calls)

Morningstar

Morningstar's analysts think that long-term DIVO's current portfolio is capable of 10% to 11% annual returns.

- Morningstar analysts think S&P will do around 12%

- a high turnover means DIVO and JEPI own very different portfolios over time.

JEPI Portfolio Future Return Potential (Excluding Covered Calls)

Morningstar

Morningstar thinks JEPI's current portfolio has a market-like 12% return potential.

- Covered call ETFs sacrifice returns for monthly income

- DO NOT expect 10% to 12% returns from DIVO, JEPI, or any covered call ETFs over the long term.

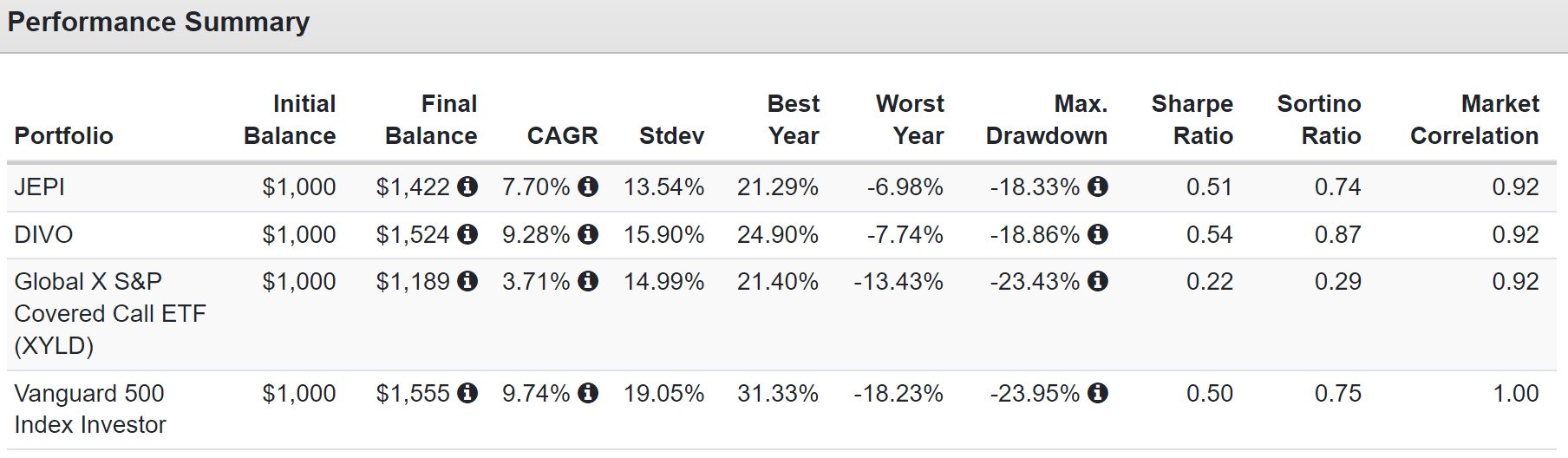

Total Returns Since 2018

{kind=link}

JEPIX is standing in for JEPI since it's been around since September 2018.

- it's the mutual fund version, but otherwise identical.

DIVO has generated superior returns to JEPI, with slightly higher volatility and equal peak declines.

Its negative-volatility-adjusted total returns (Sortino ratio) are 18% better.

JEPI's negative volatility-adjusted total returns are equal to the S&P over time, while DIVO's are superior.

If maximum returns per unit of negative volatility are your goal, DIVO is superior to the S&P (not factoring in taxes).

- S&P's historical tax bill is 0.6% or 6% of returns

- DIVO's is 19%, and JEPI's 29%.

{kind=link}

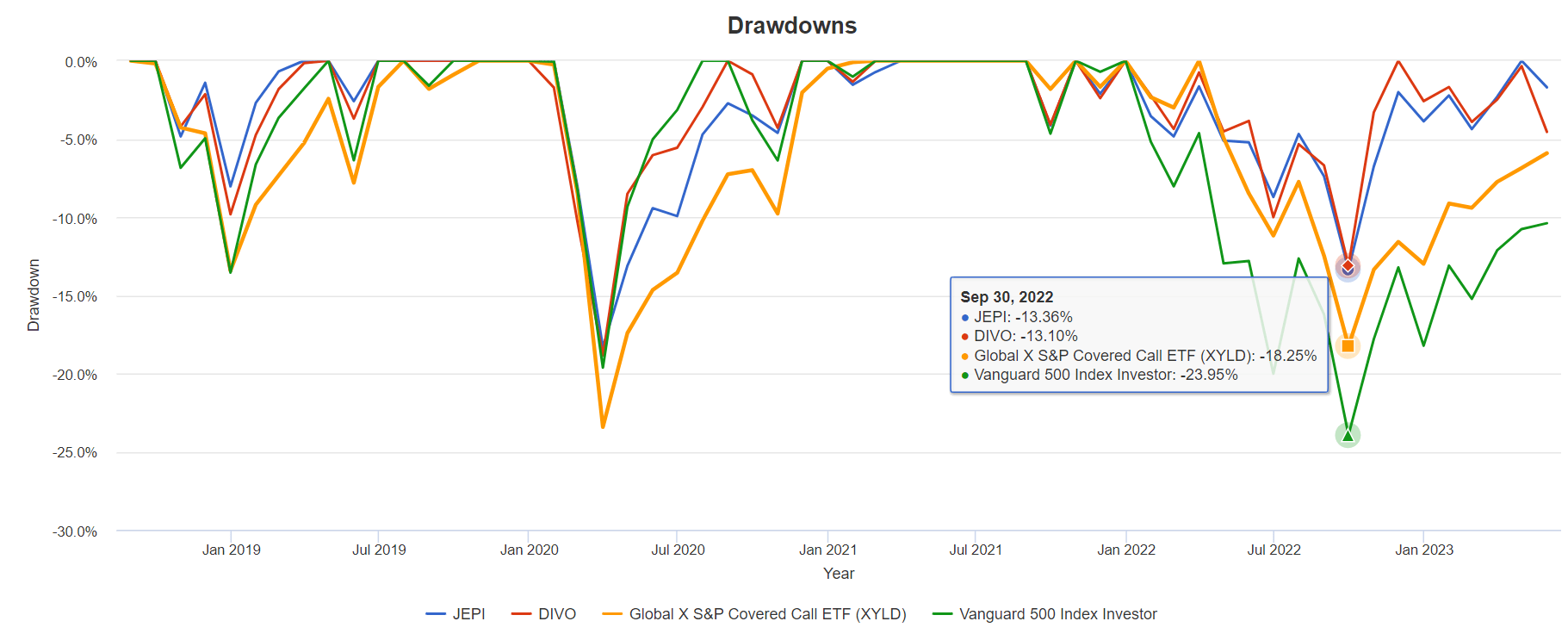

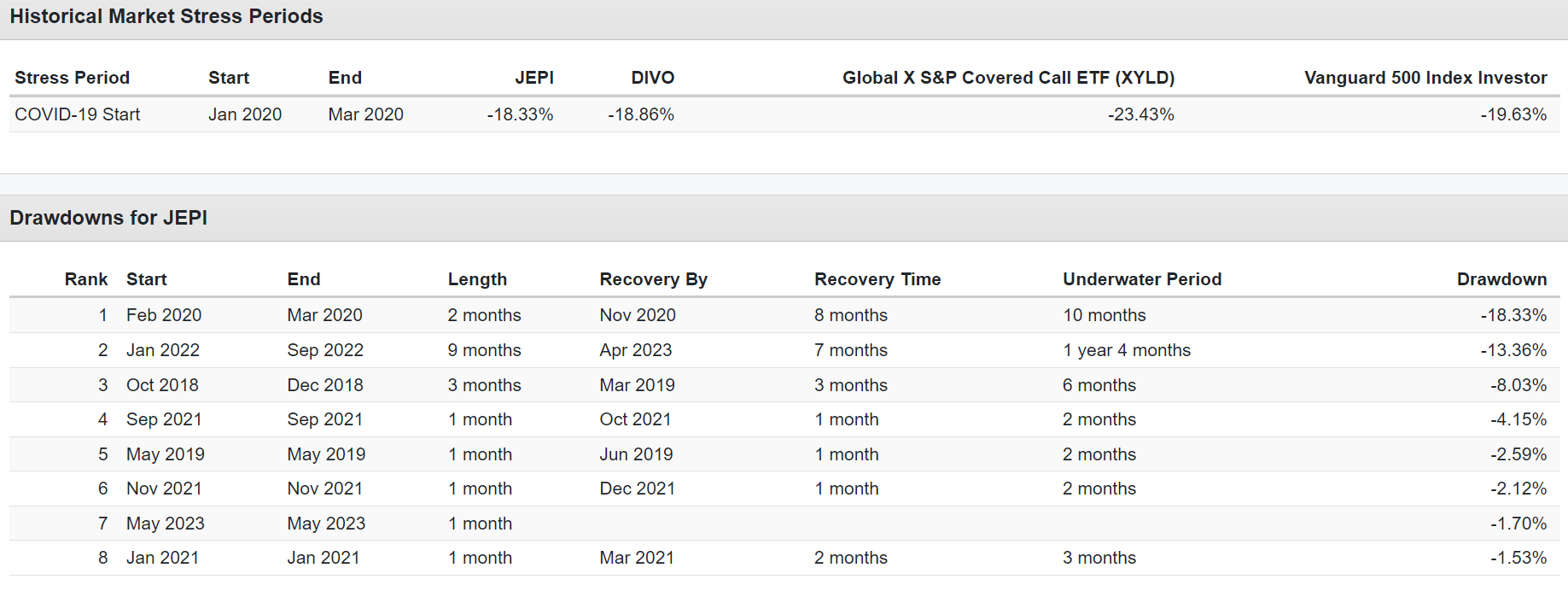

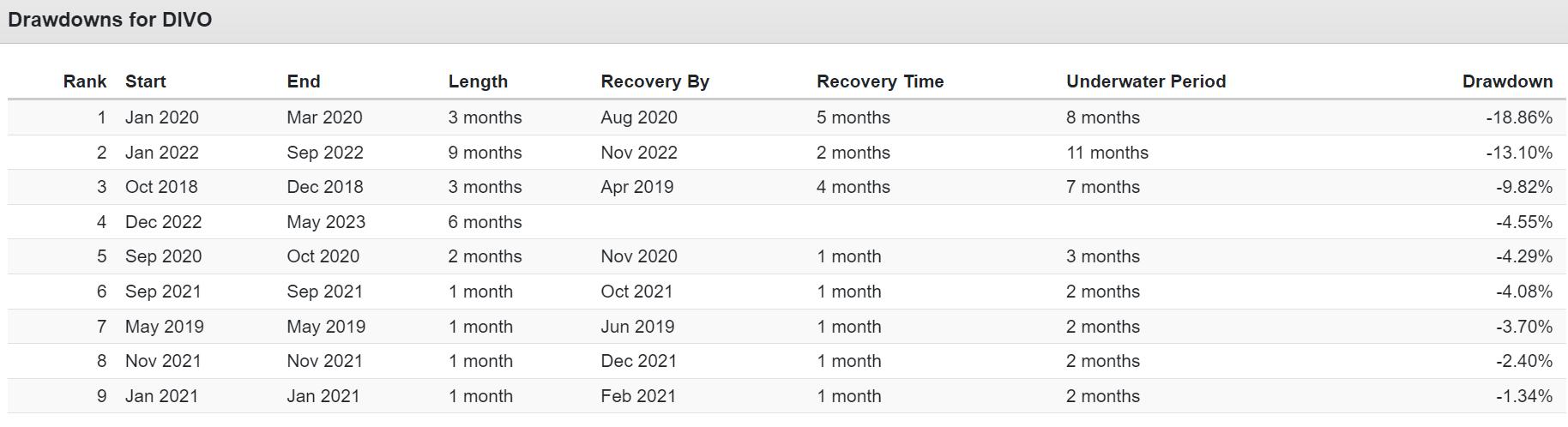

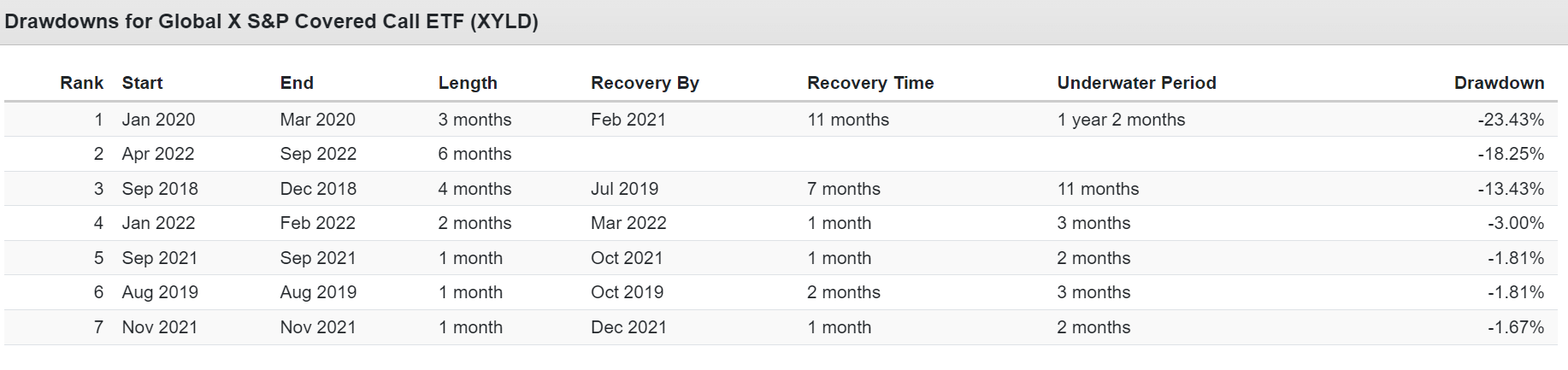

DIVO and JEPI did a good job during the 2022 bear market, generating 45% smaller declines than the S&P and 30% smaller declines than XLYD.

Portfolio Visualizer Premium Portfolio Visualizer Premium Portfolio Visualizer Premium

{kind=link}

{kind=link}

{kind=link}

Both JEPI and DIVO have done a great job of reducing volatility during corrections.

Don't Forget About Taxes! Why Covered Call ETFs Aren't Right For Everyone

JEPI Prospectus

Since its inception, JPMorgan estimates the average investor, net of fees and taxes, made 18% compared to 25% pre-tax returns.

- Taxes ate 28% of gains.

But in the past year, 40% of returns were reduced by taxes and high turnover-related expenses.

And remember, this is just for the average American, with a 28% tax bracket.

- the top income tax bracket saw 8% returns over the last year and 12% since inception

- up to 50% of your returns could go to taxes if you're rich

Morningstar estimates that the average American would have paid 29% of JEPI gains in taxes since inception.

- 3.6% per year.

And don't forget, JEPI is designed to deliver 66% to 80% of the market's returns over time.

{kind=link}

And another reminder: JEPI is NOT a bond or S&P alternative.

It's a specific tool ideally suited for three kinds of investors and only three kinds. Everyone else is better off without JEPI or ANY covered call ETF, mutual fund, or CEF.

Tax Efficiency Over Time (How Much Of The Long-Term Returns Do You Keep After Taxes)

- S&P 94%

- DIVO: 81%

- JEPI: 71%

- Global X S&P 500® Covered Call ETF (XLYD): 66%.

In terms of tax, efficiency. DIVO and JEPI are superior to XYLD, the oldest covered call ETF.

Don't Forget About The Important Of Dividend Reinvestment

Dividend reinvestment or DRIP is ALWAYS assumed when you see historical returns.

Total Returns Since 2018

Total Returns Since 2018 (WITHOUT DRIP)

Portfolio Visualizer Premium Total Returns Since 2018 (WITHOUT DRIP)

{kind=link}

{kind=link}

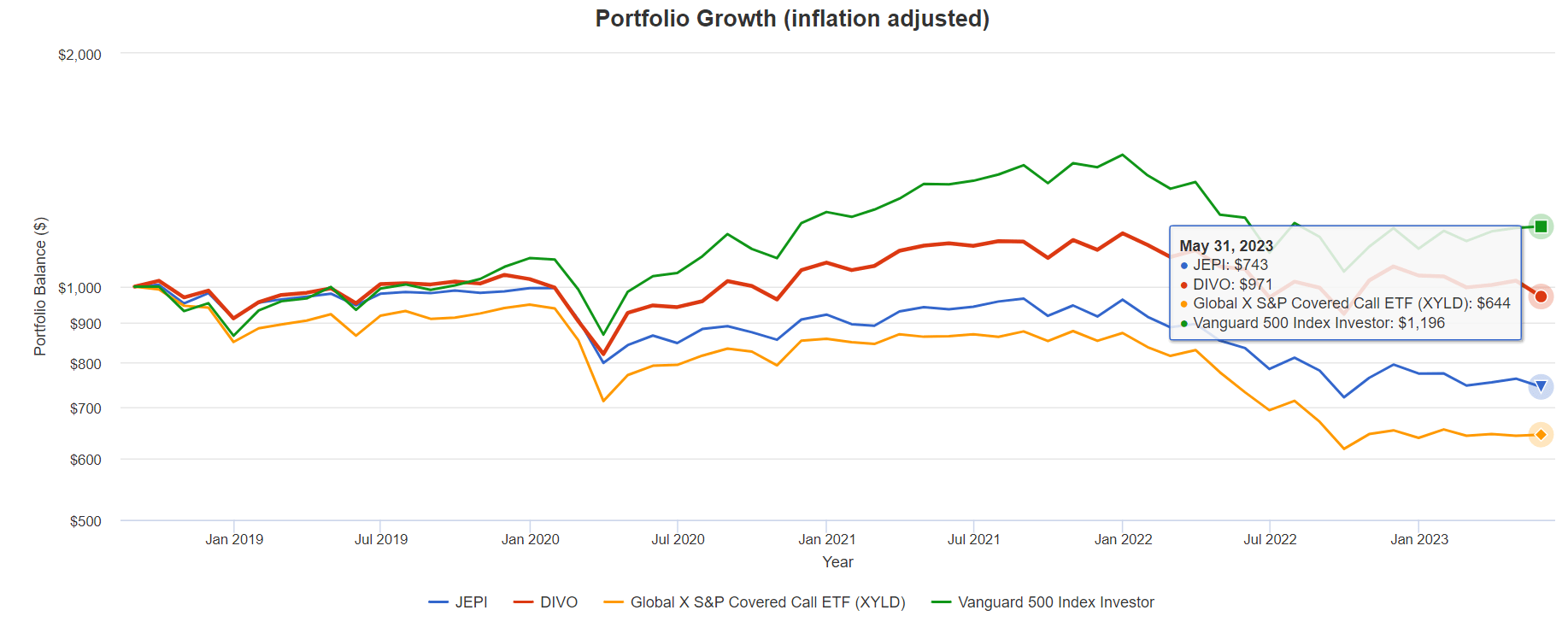

If you adjust for inflation, in a TAX-FREE account, JEPI, DIVO, and XYLD have all seen small to significant erosion of principal.

- XLYD is down 36% (-56% after tax)

- JEPI -26% (-34% after tax)

- DIVO -3% (-23% after tax).

The total returns were all paid out as income if you're not DRIPing.

- 29% of JEPI's returns go to taxes outside of retirement accounts (-34% after tax)

- 19% of DIVO's returns go to taxes

- 34% of XYLD returns go to taxes (covered calls are not tax efficient).

Remember, ALL covered call income is taxed as ordinary income, top marginal tax rate, Federal and state.

- Up to 55% in NYC for the top tax bracket.

What this means is that if you own any covered call ETF or fund or CEF in a taxable account , and you spend the income over the long term, adjusted for taxes and inflation, you are steadily losing money.

- covered call funds of all kinds are inherent value traps for this reason.

Bottom Line: DIVO Is The Superior Covered Call ETF, BUT Most Income Investors Will Still Want JEPI

DIVO is a superior cover call ETF in terms of historical returns and tax efficiency.

However, most JEPI investors are going to want to stick with JEPI for a few key reasons.

- lower expenses (future returns aren't guaranteed, but costs are)

- higher yield (JEPI is built for maximum monthly yield, DIVO is not)

- higher long-term management guidance: 8% long-term returns vs. 5.5% from DIVO.

But remember that there are three kinds of investors, and only three kinds should own JEPI or DIVO, or any covered call ETF, Mutual Fund, or CEF.

- Only own covered call ETFs or funds or CEFs in a tax-deferred account (a good to a great choice in this case)

- Roth IRA investors who want a single stock retirement plan with better returns, yield, and lower volatility than a 60/40 (perfect solution)

- Tax-deferred (401K, IRA, 403B) investors who want a single stock retirement plan better than the 60/40 AND plan to donate their entire account to charity (perfect solution)

If you're one of these three kinds of investors, then these kinds of high-yield funds are a potentially good or even ideal solution for your needs.

If you're not one of these three kinds of investors, then there are better alternatives to reach your financial goals.

Let me repeat it one more time so you don't miss it.

If you own any covered call ETF or fund or CEF in a taxable account and spend the income over the long term, adjusted for taxes and inflation, you are steadily losing money.

JEPI and DIVO are potentially useful if you know how they work, their limitations, and how to use them appropriately.

If you blindly buy them chasing low volatility yield? You could spend years or even decades lighting your savings on fire.

For further details see:

JEPI Vs. DIVO: One Is The Ultimate High-Yield Retirement Dream ETF