JRONF - Jerónimo Martins: My Only Portuguese Stock Moving Up (Rating Upgrade)

2023-10-30 12:07:21 ET

Summary

- Jerónimo Martins is a Portuguese-based corporate group operating in the food distribution and specialized retail sectors.

- The company owns market-leading brands and operations, including Pingo Doce and Biedronka.

- Despite margin pressures and challenges in its markets, Jerónimo Martins has held its ground and remains an investable company.

- I shift my rating to "BUY" with a price target of €16/share.

Dear readers/followers,

Jerónimo Martins ( JRONY ) is a Portuguese-based corporate group that operates food distribution and specialized retail, with operations in Portugal, Poland, and Colombia that I've been investing in and covering for over a year - one of the very few Portuguese stocks that I cover, and the only one that I invest in.

The company's main operations include Discount and Convenience stores, Supermarkets, and Cash-and-Carries, and you know how I like these sorts of operations given their overall resilient profiles, which I believe weighs up any sort of mediocre growth, provided it is bought at the right or appealing sort of valuation.

In my last article , I was neutral on the company - a "HOLD". I believe my rating was very justified, and this rating actually paid off even in the shorter term.

Seeking Alpha Jeronimo Martins (Seeking Alpha)

I could tell you I timed things well enough to where I bought at the dip/bottom - but that wouldn't be true. I added my first shares at about the first leg up, meaning I am in the green, but not as much as I could have been. Overall though, I'm very happy with my base investment in this company, and here I will show you why.

Jerónimo Martins - Plenty (more) to like about groceries and trade retail

This is the sort of company you want to own. Why do I say this? Because the company has large similarities to companies like Kesko ( KKOYF ), which I invest heavily in. I actively seek out publicly traded companies that offer exposure to a nation's or an area's food distribution. This company offers exactly that.

JRONY IR (JRONY IR)

So, you may say that these are not the fundamentally most attractive markets in existence, and you'd be correct in that assertion if you were to compare them to say, the USA, Canada, or other Western nations. However, every nation and every geography needs groceries, and the operational specifics of good companies or good players in these fields are, I've found, quite similar.

Also, when it comes to JRONY, you have an extremely capable majority owner in this case - and one you may already be invested in, as I am.

The group is the majority owner of Jerónimo Martins Retail, which operates among other things the Pingo Doce super- and hypermarket chain in Portugal. JMR has been run as a 51%-49% joint venture with the Dutch firm Ahold Delhaize ( ADRNY ) since 1982.

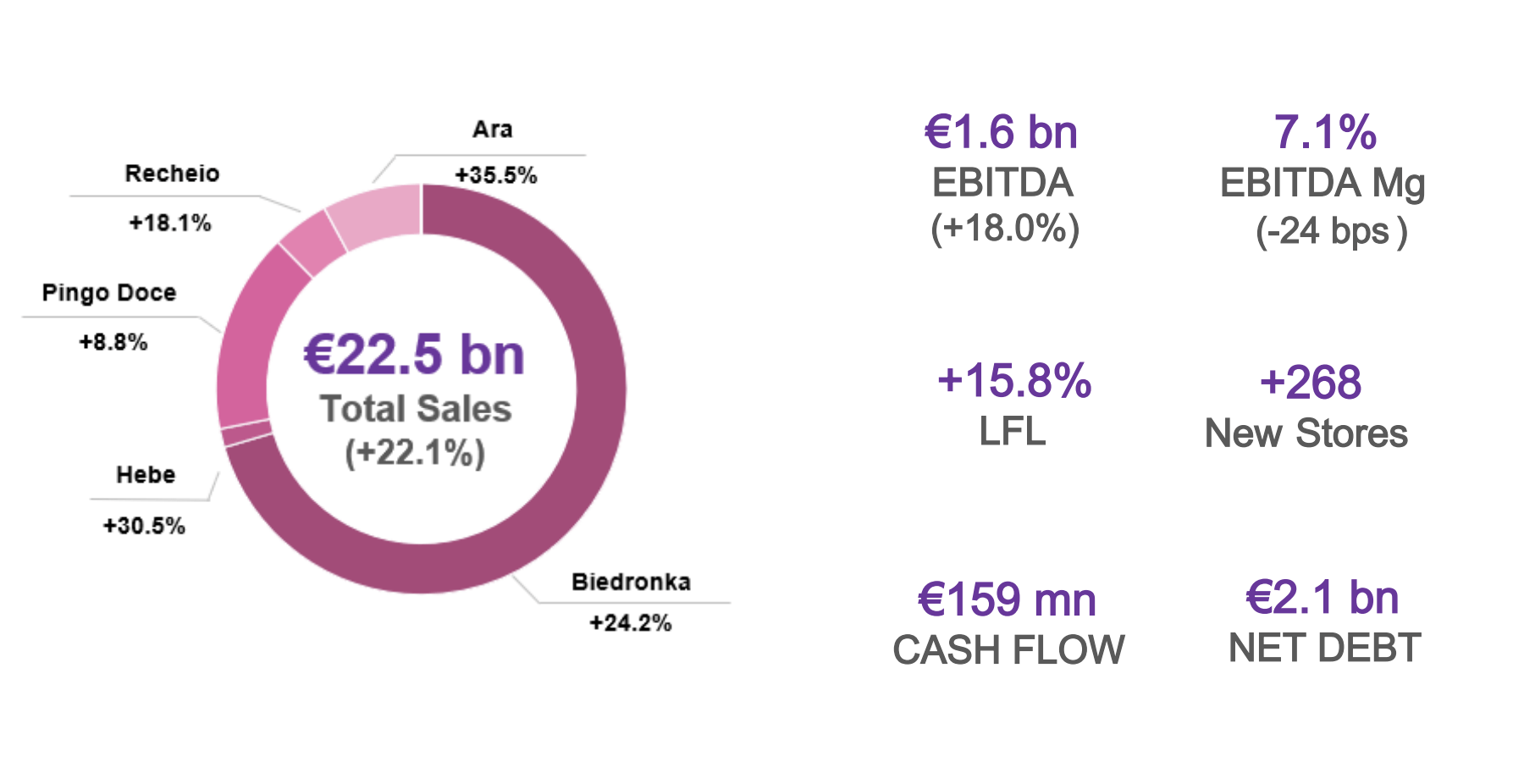

Pingo Doce and Recheio are the company's largest brands in the home market. However, it also owns the Jeronymo Coffee Shops and the Hussel Chocolate boutiques, and in Poland, it's known for the Biedronka, the largest in no-frills supermarkets as well as the Hebe beauty and cosmetics store. These are the reasons why I am positive about this business - they own market-leading brands and operations.

The fact that JRONY, on a comparative basis, isn't quite as good as many of its European or US peers in terms of margins, that's something you'll have to accept.

We have 9M23 results. Those results are "okay." We're talking a growth in EBITDA, but most of that growth came from price realization, not necessarily pure volume - though the company did open up or include 268 new stores in the past 9 months, which is of course amazing. Sales are up 22.1%, again though mostly due to price (excluding the new stores), and the company managed an operational cash flow of around €160M which is again...."okay".

Much of things are "okay" here. €2.1B net debt is above where I would like, but it's okay. The company is experiencing significant EBITDA pressure due to both investment and inflation, but the execution of the CapEx program is on track.

Positives mixed with clear challenges

{kind=link}

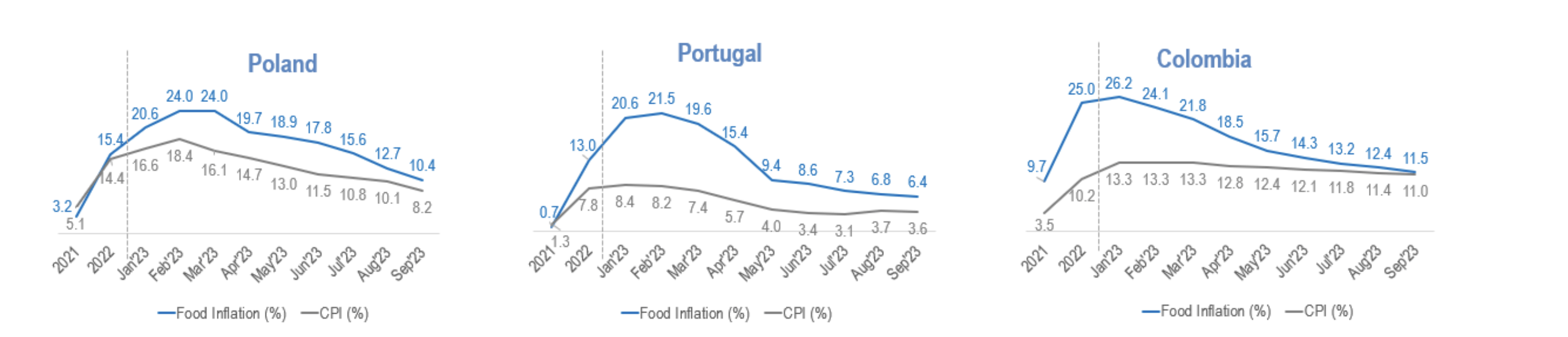

The very clear reason for this is that the company operates perhaps in three of the most food-inflated (price-wise) markets that exist in the EU and South America, where the most positive thing that can be said is that they are slowly normalizing towards low double-digit food inflation prices, with the exception of Portugal which is looking better.

{kind=link}

This is without a doubt the most fragile FMCG company that I invest in, reflecting the underlying fragility of those markets. Portugal, despite positives, is complex for its own reason due to the pressure on household real income and the crucial role of tourism in all of the HoReCa performance - which directly affects JRONY.

The company claims solid cash flow delivery. I say it's okay - because it's over €100M lower YoY, though mostly due to CapEx. The company claims a solid balance sheet. I say it's okay - because net deb is up above €2B, compared to €1.6B during the YoY period. All of the company's brands, except Pingo Doce and Hebe are seeing LFL sales volume growth declines, meaning that sales are growing, but not as quickly as they once were.

The overall picture that I want to give for JRONY as of the 9M period or the 3Q23 period, is that the company has held its ground. It's seeing pricing pressures, it's battling inflation, it's doing what it can to remain competitive, but it's not outperforming as some of its peers in other European locales or international markets are. This is perhaps not something that is fair to expect from the company either, given its markets. It can be said that the company might be doing well enough, simply because it's maintaining as it is.

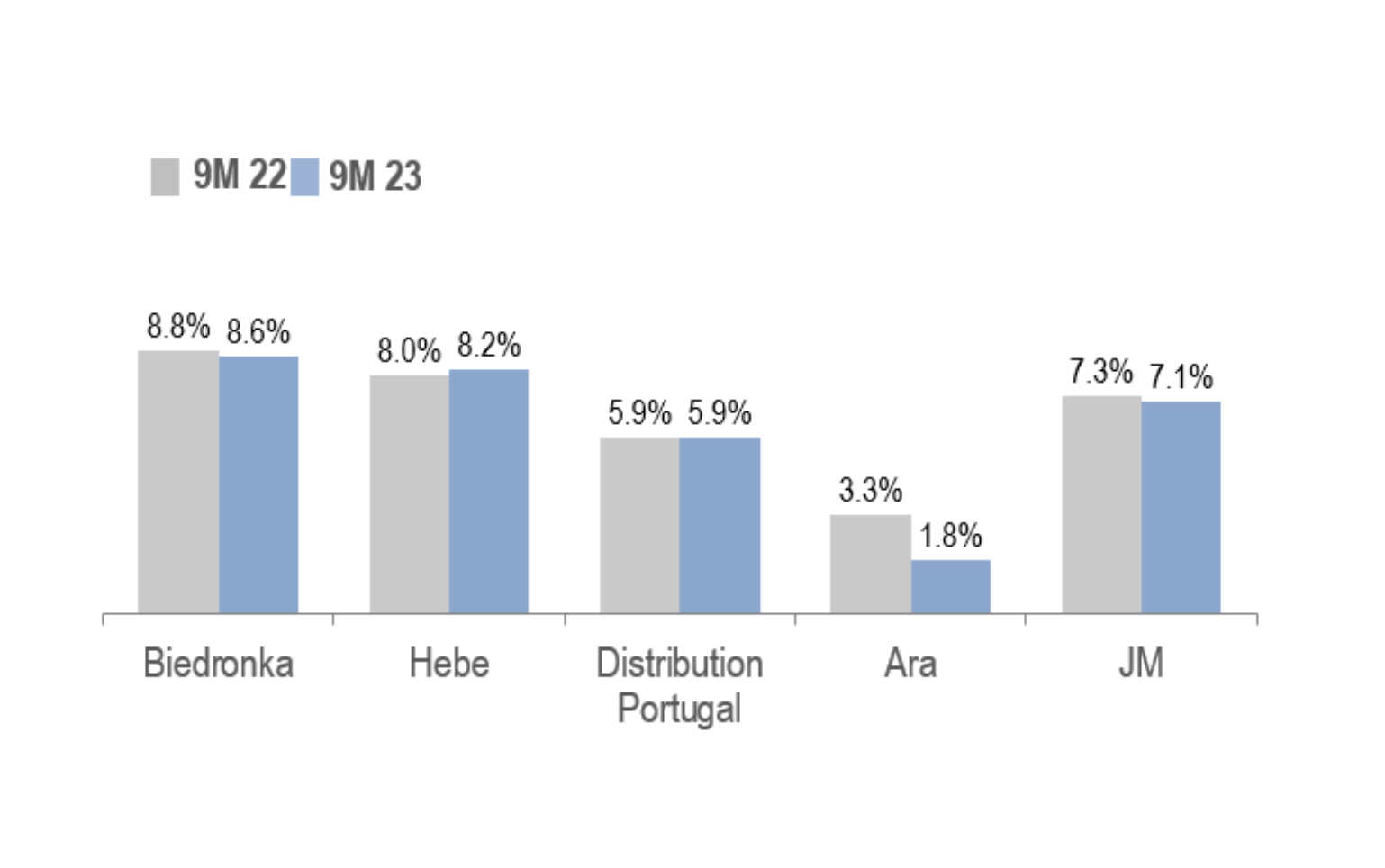

However, it's important to understand the margin pressure the company is under, and what the company is doing to try and solve it. What you see below is the company's EBITDA margin.

{kind=link}

The targets that the company has are exactly the same as the targets for any company in this sector, or in any sector going into this environment. Growing sales in challenging environments not only due to price but also volume while protecting profitability and margins. It's a simple target, but very difficult to execute in this market. Ara especially, which has never been all that profitable in terms of EBITDA or net margins, is sticking out like a sore thumb, now below 2% in EBITDA margin according to IFRS16, dropping by almost 50% in less than 1.5 years.

The best performer out of the bunch is Hebe, and Hebe isn't even food, but a drugstore - which showcases the strength of the multi-sector trading company model to survive environments such as this one.

I am in no way "worried" about Jeronimo Martins. This is an FMCG company, a grocer, mixed with a trading company that appeals in the same way that Kesko is. A downturn here doesn't really worry me unless the reason is fundamental. JRONY was, in fact, overvalued when I last wrote about it, so the correction here was fully justified in my view.

And despite everything that I've said here and the negativity that can be said, I still believe this company to be incredibly investable.

The company's dividend yield is only 2.5% here. It also has less than 2.5% net margins in its current business model, which is less than what I typically look for - but it's still a grocer in some very good markets (Colombia isn't a bad market, if a risky one, once the company gets this under control).

Jeronimo Martins's native symbol, if you can trade it, is JMT on the Lisbon stock market. I would say you should if you want to invest - JRONY is a bit too thinly traded.

Let me show you the upside that's causing me to change my thesis here.

Jerónimo Martins - Valuation is now looking far better

So, in my last article, I gave the company a PT of €22/share and a hold. If you follow my work, you'll know that I very rarely change my price targets. The fact is, that this article, if I am being 100% fair, is coming about 1-2 days too late because the company is currently trading at €22.16. When I started writing it, however, it was still below €22/share, making it a "BUY".

What can be said for the company here is that it's teetering on the edge of "HOLD" and "BUY". I would say until the price reaches €22.5, you can still "BUY" it, and I would personally do so as well.

It was of course far more attractive to buy it at below €20/share, as I managed to do due to sheer luck and a price alert on my broker, but even here, the upside is non-trivial.

I would estimate the company at 21-22x P/E on a forward basis. This is what the company traded at when I last wrote about it. It's now at 18.65x. The upside based on a 7-9% EPS growth rate estimate comes to around 19.2% at 21.5x, or 46.8% for 3 years. That being said, that's a high target for a company that over the past 10 years has missed their estimates over 50% of the time, and going into this inflationary and macro period, especially with key segments of the company declining, you would be justified estimating it at a lower price, or discounting the company more.

You could, however, discount it to 18-19x, and still end up with a double-digit annualized upside. Not 15%, but 10-13%. For a 15% annualized upside, the company has to manage 20x P/E. I acknowledge that this may be difficult in the next 2 years, but I do believe that based on operational resilience and the sheer weight of FMCG, the company will eventually normalize to this level.

For that reason, JRONY is a "BUY" to me here. it's the first time in over a year that I believe the company is priced for buying, even if as I said, this article might be one or two days late given the company going over €22/share.

I believe this to be strong enough for a thesis change. I don't change my PT, but I do believe the company is still a "BUY" here if you're willing to give it some premium and some room to run in the next few years.

Thesis

- Jerónimo Martins is a company I do want to own, and now own - and I managed to get in at €19-€20/share. The higher-than-average forecast uncertainty currently remains, but I do believe that even at €22.16/share, you can buy this with a 15% upside due to the potential premium.

- I want 15% or above out of the investments that I put my money in, on an annual basis. It's now high enough.

- I stick to my PT of €22/share and a "BUY" rating here, which means that this is an official rating change for JRONY.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I cannot call JRONY cheap here, but I can call it a "BUY". I believe the company warrants "cheap" at below €20/share.

For further details see:

Jerónimo Martins: My Only Portuguese Stock, Moving Up (Rating Upgrade)