JRSH - Jerash Books Strong Q3 FY23 Results And The Prospects Are Good (Rating Upgrade)

Summary

- The company generated record Q3 fiscal year revenues of $43 million as its sales grew even when excluding the delayed orders from the previous quarter.

- Jerash had a net cash position of $20.2 million as of December as well as a decent dividend yield of 4.26%.

- In my view, the deal with Busana should help Jerash to grow its sales in FY24 and I think the company should be valued at above 8x EV/EBIT.

- I’m upgrading my rating to speculative buy.

Introduction

I’ve written three articles on SA about Jordan-focused apparel products manufacturer Jerash Holdings (JRSH). The latest of them was in December and in it I said that I expected at least a few challenging quarters ahead from a financial standpoint due to global macroeconomic challenges.

Well, the company recently released its Q3 FY23 financial results and I was pleasantly surprised that it managed to keep its facilities running at full capacity during the period. The Q4 FY23 revenue outlook looks a little disappointing but the margins should be decent. It seems I was too pessimistic back in December. Let’s review.

Overview of the Q3 FY23 financial results

In case you haven't read any of my previous articles about Jerash, here's a brief description of the business. The company specializes in the production of t-shirts, polo shirts, pants, shorts, and jackets and it has six factories near Jordan’s capital Amman with a combined annual production capacity of about 14 million pieces. Jerash also has four warehousing facilities, and it employs about 5,800 people. About a quarter of the workforce includes native Jordanians, while the remainder is comprised of contracted workers from Bangladesh, Sri Lanka, India, Myanmar, and Nepal. The main clients of the company include several U.S. apparel brands such as The North Face, Timberland, Calvin Klein, Tommy Hilfiger, and American Eagle, and about three-quarters of sales are comprised of jackets and pants and shorts.

{kind=link}

The competitive advantage over rivals in low-wage countries like China and Bangladesh is a free trade agreement between the USA and Jordan which has been in place for over 20 years now. The exports of Jerash to the USA are exempt from customs duties and import quotas and the company has been expanding its capacity rapidly over the past several years. Jordan also has a similar free trade agreement with the EU.

Jerash

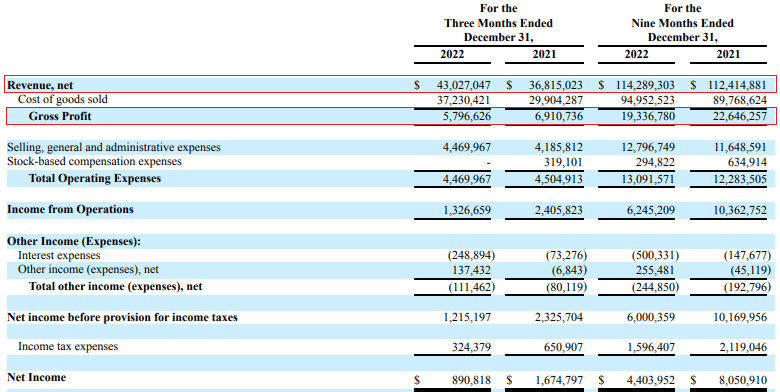

Turning our attention to the Q3 FY23 financial results, Jerash returned to growth following the soft previous quarter as revenues rose by 16.9% to $43 million. Jerash thus achieved record third quarter fiscal year revenues and the main reason behind this was the company was able to keep its facilities running at full capacity despite smaller orders from its large customers. Jerash added supplementary production for small and new customers and it also began to ramp up production on orders from Timberland and Skechers in Q3 FY23. However, the gross margin slumped to 13.5% due to the lower share of orders from the USA, which typically generate higher margins.

{kind=link}

{kind=link}

However, it’s worth noting that Jerash said during its Q2 FY23 earnings call that revenues back then were about $4 million lower than expected due to shipment delays as retailers sold through excess inventories. Without these delays, the revenue growth in Q3 FY23 could’ve been about 6% year on year. Considering Jerash has been able to run its factories at full capacity, I think it’s underwhelming that revenues for Q4 FY23 are expected to be in the range of $26 million to $28 million. The midpoint of the range represents a year-over-year decline of 7.8%. On a positive note, Jerash usually has a conservative approach to guidance and also it seems that the decrease in sales is forecast to come mainly from non-US orders as the gross margin goal for the full fiscal year is forecast to be in the range of 16% to 18%.

Looking at what to expect in FY24, Jerash said that its plans to create a joint venture company with Indonesian sector player Busana Apparel Group are progressing well and that this new unit should be operational in the early part of the next fiscal year. Considering, that Busana is a major apparel manufacturer with around 50 million pieces produced per year and that the joint venture company will produce garments for its retail customers, I expect this deal to enable Jerash to operate at high levels of capacity during FY24.

Turning our attention to the balance sheet, the situation looks a little better compared to September 2022 as cash increased by $1.6 million to $24.6 million and inventories decreased by $9.8 million. It seems that Jerash is no longer being affected by supply chain issues as inventories are back to their usual levels. The company had a net cash position of $20.2 million as of December.

{kind=link}

Jerash has an enterprise value of just $37.8 million as of the time of writing, which means that it’s trading at around 5.9x its TTM operating income. Overall, I expect a single-digit revenue growth for FY24 and an improvement in the company’s profitability and I think it should be valued at something like 8x EV/EBIT. This translates into $6.36 per share, which represents a nice upside potential of 35.6%. In addition, Jerash has a decent dividend yield of 4.26% and it bought back 51,767 shares in Q3 FY23.

Looking at the risks for the bull case, I think the major one is the macroeconomic situation in the USA as a prolonged recession is likely to affect demand for discretionary goods such as clothes. The orders placed by the top global brand customers have been smaller for several months now and is unclear when the situation could improve.

Investor takeaway

Jerash surpassed my expectations for Q3 FY23 as its sales grew even when excluding the delayed orders from the previous quarter. While revenues for Q4 FY23 are forecast to be weaker, I think that the company is being conservative and I find it encouraging that the expected gross income margin for the full fiscal year is 16% to 18%. In my view, the deal with Busana should help Jerash to grow its sales in FY24 and I think the company should be valued at above 8x EV/EBIT. I’m upgrading my rating to speculative buy.

For further details see:

Jerash Books Strong Q3 FY23 Results And The Prospects Are Good (Rating Upgrade)