SAVE - JetBlue: An Unattractive Risk-Reward Profile

2023-08-24 13:44:40 ET

Summary

- JetBlue's Q2 2023 results were solid, with increased revenues and a profit due to lower fuel costs.

- However, the company is facing challenges in Q3 2023 and the future, including the wind-down of the Northeast Alliance and shifts in demand.

- The risk-reward profile for investing in JetBlue is not favorable, and the stock is recommended as a Hold.

I am generally not a fan of investing in airline names for the longer term as airlines have the tendency to “self destruct” by throwing capacity on the market, bringing fares down. Currently, that self destruction is on the weaker side due to airplane and pilot shortages, but we see that some airlines are not quite benefiting from strong fares because of these issues as well. JetBlue (JBLU) is one of those airlines, and on top of that the company is facing some specific issues. Overall, the investment case for JetBlue is not looking strong, but before discarding the idea of a JetBlue investment I want to analyze the results, guidance and forward fundamentals before making a gut call.

JetBlue Posts Solid Q2 2023 Results

{kind=link}

jetBlue

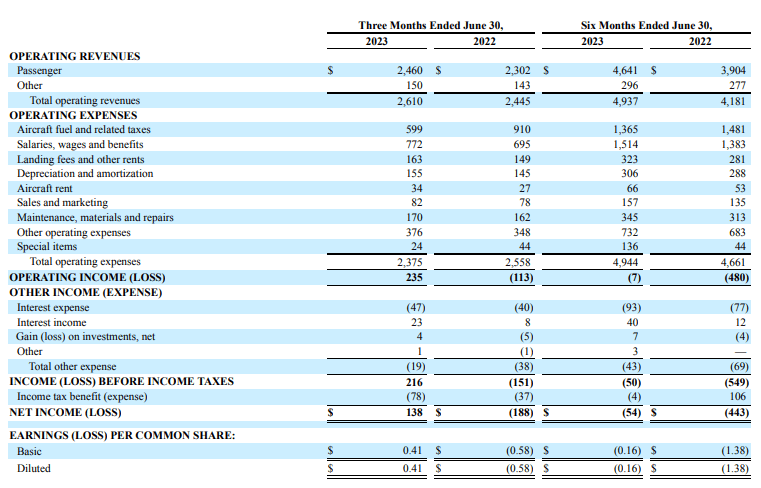

During the second quarter, revenues increased 6.7% on 5.8% higher capacity, which was in line with the guidance. We're not seeing major increases in either the capacity or the revenues and that's because airlines such as JetBlue do not have a big long-haul network that fuels the final stage of the recovery of the industry and feeds into the results. And we're now having some negative comp effects as the comparable period last year was also a high-fare quarter. So we're comparing high-fare and high demand quarters now and that provides for lower growth year-over-year.

Helped by a lower fuel bill, JetBlue turned a $113 million loss last year into a $235 million profit or 9% operating margin this year. The unit costs decreased by 12.2%, but this was driven by lower fuel costs which are not controllable. The unit costs excluding fuel increased by 3.2% which included a 1.5 point drag from flooding in Fort Lauderdale and air traffic control challenges plus one point for investing in the business to improve the operational environment.

The Future Is Not Looking Bright For JetBlue

{kind=link}

jetBlue

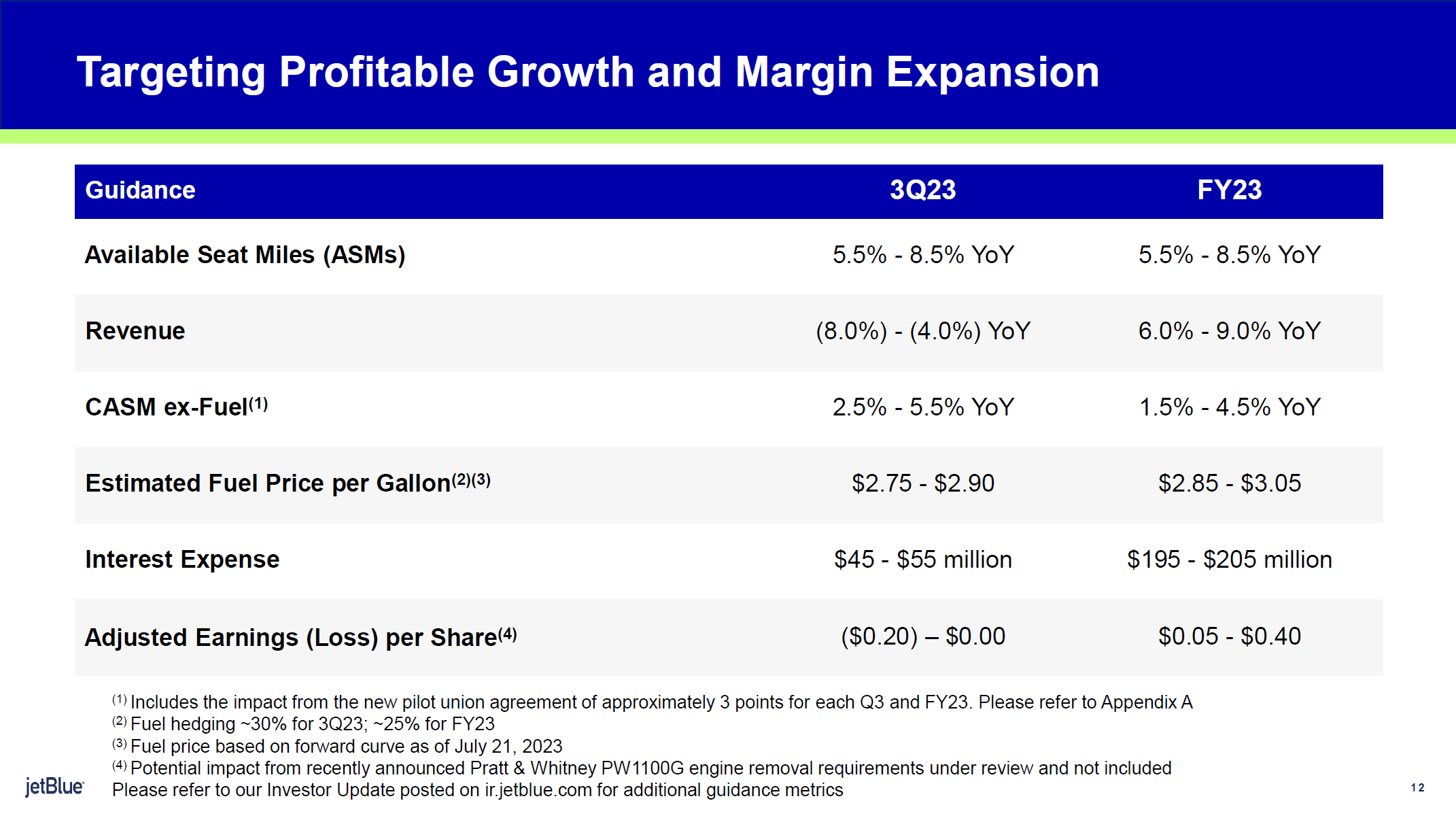

While the second quarter results are quite good and gave no reason for concern, the guidance for Q3 2023 and the update for FY2023 does show the challenges for the company. In Q3 2023, the capacity is expected to be increased by 5.5 to 8.5 percent, but that will not be visible in the top line where the Northeast Alliance Wind Down will have an adverse impact. JetBlue will be reallocating the capacity, but the effects of that distribution will become visible from Q1 2024.

For the full year, the company has kept its revenue and capacity guidance in place while the revenue guide has been updated from high single-digit to low double-digit growth of 6% to 9%. Unit cost guidance has been maintained as cost cutting initiatives are offsetting the air traffic control challenges. At the end of the day, however, the EPS guidance has been cut from $0.70-$1.00 to $0.05-$0.40 reflecting a $0.20-$0.25 negative impact from the Northeast Alliance wind down, a similar negative impact due to ATC and weather challenges and $0.15-$0.20 negative impact on pent up COVID demand shifting toward long-haul rather than the domestic market and shorter flights.

JetBlue was one of the companies of which it became clear early on that they couldn’t scale at all in line with demand increases and the company even would pull forward aircraft redeliveries and maintenance due to the significant shortages on the staffing side. Add to that the wind down of NEA, uncertainty about the combination with Spirit Airlines ( SAVE ) and pent-up demand shifts and JetBlue is not looking attractive at all.

JetBlue : Upside At A Price

{kind=link}

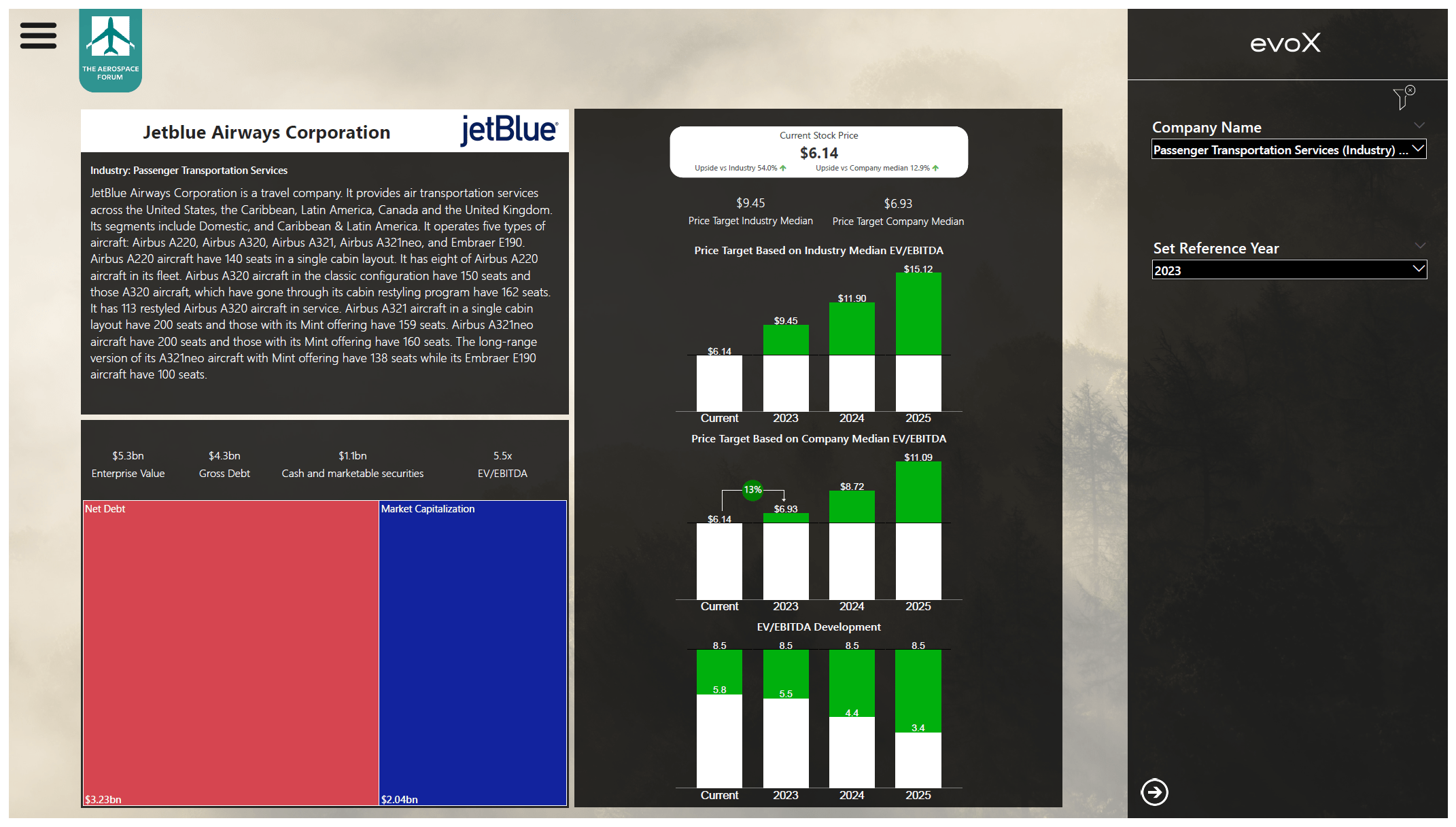

jetBlue stock price valuation using evoX Financial Analytics (The Aerospace Forum)

When entering the expected values into my model, things actually don’t look bad for JetBlue over the longer term. Normally I would issue a buy rating based on the upside in the years to come. However, for JetBlue I don’t consider the risk-reward profile to be favorable with a broken alliance with American Airlines ( AAL ), a combination with Spirit Airlines of which we don’t know whether it will happen or not and demand shifts. Furthermore, for 2023 the remaining upside is only 13% which I don’t deem to be attractive As a result, I'm marking the stock a Hold.

Conclusion: JetBlue Too Many Uncertainties

While the Q2 2023 results were good, the guidance for the full year has been brought down due to air traffic control and weather problems, as well as shifts in pent-up demand to long haul and the North East Alliance being dissolved. With so many uncertainties ahead, I deem the upside for 2023 to be too limited to be of any interest to investors. The upside in the years beyond is more attractive but we have yet to see how JetBlue performs this year and whether its efforts to combine with Spirit Airlines will be fruitful.

For further details see:

JetBlue: An Unattractive Risk-Reward Profile