JFR - JFR: A Good Fund For High Rates Or A Pair Trade

2023-10-09 13:59:27 ET

Summary

- The Nuveen Floating Rate Income Fund offers a high level of income with a current yield of 12.72% and increasing distributions.

- The fund has outperformed traditional fixed-rate bond indices YTD and has a positive total return despite a price decline.

- The fund's focus on floating-rate securities make it attractive during periods of rising interest rates, which could very easily be the case for a while due to US fiscal policy.

- The fund may work best in a pair-trade with a traditional bond fund just in case interest rates drop.

- The fund's distribution is entirely covered by NII and it is trading at a deep discount on NAV.

The Nuveen Floating Rate Income Fund ( JFR ) is a closed-end fund aka CEF that has proven itself to be an excellent investment for people who are seeking to earn a high level of income from the assets in their portfolios. The fund’s 12.72% current yield is a testament to this, as is the fact that this is one of the few closed-end funds that has been increasing its distribution over the past twelve months. The reason for this can be quite simply stated as high-interest rates generally benefit the assets in which this fund is invested. That stands in stark contrast to pretty much all other debt funds and allows this fund to act as a good diversifier for a portfolio.

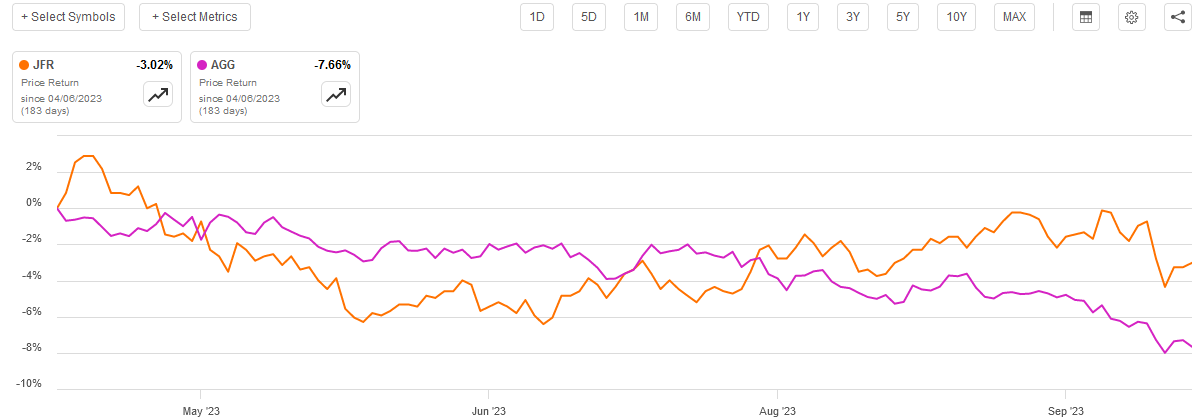

I last discussed this fund back in April, and its performance since that time has not been stellar, although it has held up better than many other things. In particular, the Nuveen Floating Rate Income Fund has experienced a price decline of 3.02%, which is much better than the 7.66% decline in the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

The fund looks even better when we consider the distribution that it pays out. This is because, like most closed-end funds, the majority of this fund’s returns are delivered in the form of direct payments to the shareholders and not through price appreciation. Since April 6 (the date that my last article was published), the fund has paid out sufficient distributions to not only fully offset the share price decline but also give the fund a positive 2.74% total return. Thus, investors who purchased into this fund on that date have managed to make money.

As several months have passed since we last discussed this fund, today would be a good time to revisit our thesis regarding its future outlook. After all, there have been a great many changes in the market over the intervening period and it is always important to remain cognizant of these things. In addition, the fund has released an updated financial report, so we will want to have a look at that and see how well the fund’s portfolio is faring in the current climate.

About The Fund

According to the fund’s website , the Nuveen Floating Rate Income Fund has the primary objective of providing its investors with a high level of current income. As is usually the case, the fund’s website goes into a bit more in-depth description of the fund’s objectives and strategies:

The Fund seeks to achieve a high level of current income by investing in a portfolio of adjustable rate senior loans and other debt instruments.

At least 80% of its managed assets will consist of adjustable rate loans; at least 65% of these must be senior loans secured by specific collateral. Other loans may include unsecured senior loans and secured and unsecured subordinated loans. The fund uses leverage.

As we can clearly see, the Nuveen Floating Rate Income Fund is a debt fund. As might be expected, a substantial percentage of its assets are invested in debt securities. As we can see here, 97.08% of the portfolio consists of bonds, with the remainder invested in a combination of common stock, cash, and other things:

CEF Connect

Despite CEF Connect describing the fund’s assets as bonds, these are not the traditional bonds that most of us picture. Ordinary bonds are issued at face value, pay a fixed regular coupon to the investor, and then get redeemed at face value when they mature. The bonds that the Nuveen Floating Rate Income Fund invests in are different because the coupon is not fixed. Rather, the payment changes so that the bond delivers an annualized yield based on some benchmark at the time of payment. Usually, the yield on these bonds is expressed as something like LIBOR+XXXX, where XXXX is some percentage. The fact that these securities have a yield that changes based on the market interest rate allows them to avoid one of the biggest problems with traditional fixed-coupon bonds.

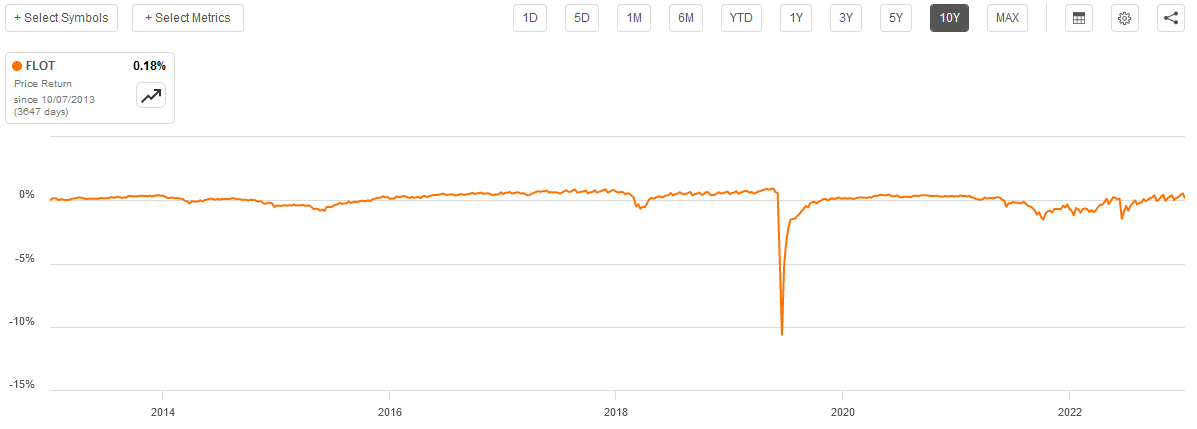

Most notably, these securities always deliver a competitive interest rate, so they do not decline when interest rates go up. In fact, apart from the market panic that occurred around the start of the COVID-19 pandemic, the Bloomberg Floating Rate Note < 5 Yrs Index ( FLOT ) has been perfectly flat over the past decade:

{kind=link}

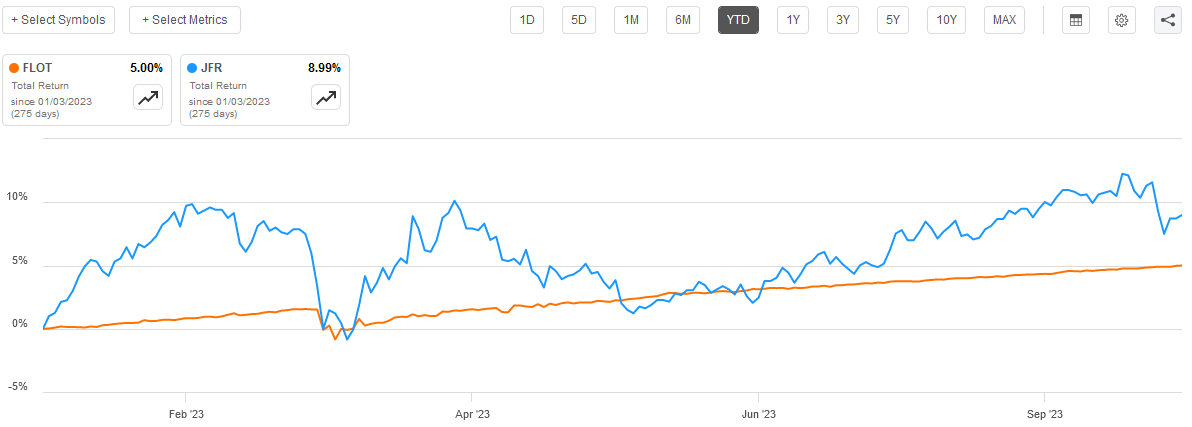

This makes the securities held by the fund very attractive during periods of rising interest rates, such as what we are experiencing now. It is, for example, the biggest reason why the Nuveen Floating Rate Income Fund has been outperforming the Bloomberg U.S. Aggregate Bond Index, which consists solely of traditional fixed-rate bonds. The fund has also outperformed the Bloomberg Floating Rate Note < 5 Yrs. Index year-to-date, albeit with significantly more volatility:

{kind=link}

One of the biggest reasons for the year-to-date outperformance of the Nuveen Fund is its use of leverage, which we will discuss later in this article. However, it still speaks fairly highly about the quality of the fund’s management. It is important to remember though that past performance is no guarantee of future results.

Recently, we have seen interest rates go up as the market begins to accept that the Federal Reserve is serious about its “higher for longer” policy and will not be cutting rates anytime soon. This would mean that this fund will probably outperform traditional bond funds as rates continue to rise. However, the market still anticipates that rates will drop in 2024 and beyond. This view is confirmed by officials at the Federal Reserve, as the current median prediction among the members of the Federal Open Market Committee is that the federal funds rate will be at 5% to 5.25% at the end of 2024, which is a quarter point below today’s rate. Any decline in interest rates will cause traditional bond prices to rise, however, the floating rate securities held by the Nuveen Floating Rate Income Fund will not really be affected in terms of price. Thus, it is possible that this fund will underperform traditional bonds as the rate starts to fall next year. However, this assumes that the Federal Reserve will actually be able to reduce rates next year and that the market has not already priced this in. As the yield curve has been inverted for a while now, the market is clearly already assuming that rates will be cut in the near future.

The big question is whether or not this will be possible. As I have pointed out in various previous articles, right now the Federal Government is effectively starving the private sector of capital. Matt Piepenburg of Matterhorn Asset Management recently stated ,

Foreigners hold about $18 trillion worth of US assets, of which $7.5 trillion are Uncle Sam’s increasingly embarrassing and unloved IOUs.

But those IOUs are looking a lot less attractive as an increasingly debt-soaked USA ($33 trillion and counting of public debt) seeks to borrow an additional $1.9 trillion (net) into the back-end of 2023 and issue another $5 trillion of USTs into the next year, all of which has even Jamie Dimon pulling at his hair.

Admittedly Matt Piepenburg is injecting some hyperbole into his statements as he attempts to make the case for gold, but he makes a very good point. The United States Treasury is issuing an enormous amount of debt into a market that increasingly cannot afford them or does not want them. For example, American banks have historically been the biggest buyers of U.S. Treasuries, but they have started to reduce their exposure to these securities recently:

{kind=link}

We have been seeing the same thing abroad, as foreign central banks have started to shed some of their U.S. Treasury holdings in favor of gold or securities issued by other countries. This begs the question of who will buy Treasuries going forward. The answer to this question will have a huge impact on the future trajectory of interest rates:

- If the Federal Reserve stands pat in its attempts to keep inflation at its target level, then it will not be a buyer. Thus, the Federal Government will need to continue to sell its Treasury securities into an increasingly unfriendly market. This will push up interest rates as the government will need to offer increasingly higher coupon rates to entice potential buyers.

- If the Federal Reserve decides to abandon its quest against inflation, then it will begin buying U.S. Treasuries and hold interest rates down. This will cause inflation to spike but will prevent interest rates from rising.

The Federal Reserve has no good options here, and which one it ultimately takes will determine the forward trajectory of this fund. As such, it might be a good idea to hold the Nuveen Floating Rate Income Fund alongside a good traditional bond fund. A position such as this should serve as an effective hedge against political risk, considering that politicians in Congress and the White House will almost certainly apply increasing pressure on the Federal Reserve to monetize the debt as the Treasury issuance continues on its current trajectory.

Leverage

As mentioned earlier in this article, the Nuveen Floating Rate Income Fund employs leverage as a method of boosting its yield beyond that of any of the underlying assets in the fund. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase floating-rate securities and similar assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are significantly lower than retail rates. As such, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As a result of this concept, we want to ensure that the fund is not using too much debt because that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Nuveen Floating Rate Income Fund has leveraged assets comprising 38.43% of its total assets. This is certainly higher than the one-third level that we want to see. However, it is slightly better than the 38.97% ratio that we saw the last time that we discussed this fund and overall, it is probably acceptable. After all, as we have already seen, floating-rate securities are not especially volatile in terms of price.

As such, the risk that the value of this fund’s assets will rapidly decline is negligible. That is the biggest risk involved in the use of leverage, so realistically this fund can carry a lot more leverage than funds focused on more volatile assets can handle. As such, the leverage here is probably okay, and we should not need to worry too much about it. However, we should still keep an eye on it because we do not want the fund’s leverage to get too far out of control.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Nuveen Floating Rate Income Fund is to provide its investors with a high level of current income. In order to accomplish this objective, the fund invests in a portfolio of floating-rate debt securities and similar fixed-income instruments. These securities tend to have fairly high yields due to the fact that most of them are speculative-grade securities. For example, 4% above LIBOR is not an uncommon rate, and LIBOR is currently at 5.88272% so a spread of 600-basis-points would put the yield of such a security at just shy of 10%. The fund purchases securities such as these and then applies a layer of leverage to artificially increase the effective yield that it receives from the securities in the portfolio. It collects all the payments that it receives from the securities in the portfolio and then pays them out to its shareholders, net of the fund’s own expenses. As such, we can expect that the fund will have a fairly high yield itself.

This is certainly the case as the Nuveen Floating Rate Income Fund pays a monthly distribution of $0.0850 per share ($1.02 per share annually), which gives the fund a 12.72% yield at the current price. That is certainly an attractive yield, but unfortunately, the fund has not been particularly consistent with respect to its payout over the years:

{kind=link}

As we can clearly see, the fund has varied its payout considerably over its lifetime, which may immediately be a bit of a turn-off for those investors who are seeking a safe and consistent source of income to use to pay their bills or finance their lifestyles. However, as mentioned earlier, this is one of the few closed-end funds that has actually managed to increase its distribution over the past year. In fact, the fund has increased its payout twice over the past twelve months. This is because the fund’s distribution varies directly with interest rates. After all, the securities in the portfolio pay more money to the fund when interest rates rise. This is yet another reason why investors seeking reasonably consistent income may want to pair this with an ordinary bond fund that can better exploit interest rate declines. After all, such a position will provide the best of both worlds.

Naturally, we want to ensure that the fund can actually afford the distribution that it pays out. After all, we do not want to be the victims of a distribution cut, as that would reduce our incomes and almost certainly cause the fund’s share price to decline.

Fortunately, we do have an incredibly recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on July 31, 2023. As such, this is a much newer report than the one that we had available to us the last time that we discussed this fund. That is certainly nice to see as the first half of this year was dominated by a rather optimistic market that expected the Federal Reserve to rapidly pivot its monetary policy and begin cutting rates. As such, it was buying up bonds and driving prices up and down. However, this did not have the same effect on LIBOR, which generally increased during every month year-to-date:

{kind=link}

That is important since it is generally LIBOR that determines the fund’s income. However, the fund does have a 13% allocation to traditional corporate bonds, so the generally positive environment for them may have given it the potential to earn some capital gains. This financial report will give us a good idea of how well the fund performed in that situation.

During the full-year period, the Nuveen Floating Rate Income Fund received $72,519,480 in interest and $3,118,014 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund brought in $76,471,079 during the period. It paid its expenses out of this amount, which left it with $51,585,735 available for shareholders. This was, fortunately, more than enough to cover the $49,433,689 that the fund paid out in shareholder distributions. This is rather encouraging, as generally speaking we like it when a fixed-income fund simply funds its entire distribution out of net investment income.

Unfortunately, the fund failed to fully cover its distribution during the prior-year period, as its net investment income of $31,747,379 was insufficient to cover the $40,070,601 that it paid out in shareholder distributions. However, it is important to keep in mind that quite a bit of the prior-year quarter was the second half of 2021 when real interest rates were negative, and money was basically free. That would obviously be a very challenging time for any floating-rate bond fund.

For the most part, the fund can probably sustain the current payout as long as interest rates remain at their current level or increase. However, it may be forced to cut if and when interest rates begin to decline to more normal levels.

Valuation

As of October 6, 2023 (the most recent date for which data is available as of the time of writing), the Nuveen Floating Rate Income Fund has a net asset value of $9.11 per share but the shares currently trade for $8.04 each. This gives the fund’s shares an 11.75% discount on the net asset value at the current price. This is a very reasonable discount, and it is quite a bit better than the 10.57% discount that the shares have had on average over the past month. As such, the current price appears to be a very reasonable entry price.

Conclusion

In conclusion, the Nuveen Floating Rate Income Fund looks like a reasonably solid play during a period of monetary tightening. The securities that comprise the bulk of this fund actually benefit from rising interest rates, which is in stark contrast to the performance of traditional fixed-rate bonds. However, due to the uncertainty with respect to the forward trajectory of interest rates right now, risk-averse investors may want to pair this fund with one that invests in more traditional debt instruments. This trade should allow investors to profit regardless of the direction of interest rates.

The whopping 12.72% yield possessed by Nuveen Floating Rate Income Fund certainly seems sustainable as long as interest rates remain at their present level, and the shares are trading at a discount to their intrinsic value. Thus, the current price does look like a fairly good place to get in.

For further details see:

JFR: A Good Fund For High Rates Or A Pair Trade