JHI - JHI: Recession Incoming Avoid

2023-05-14 03:53:02 ET

Summary

- The JHI fund focuses on a portfolio of junk bonds to generate a high yield.

- The JHI fund recently cut its distribution to $0.1925 / quarter or 6.1% annualized. This was predictable and expected.

- With an incoming recession, investors should avoid levered credit funds like JHI, as their holdings can get marked down aggressively when credit spreads spike.

A few months ago, I wrote a cautious article on the John Hancock Investors Trust ( JHI ), commenting that long-term investors are structurally set up to lose due to the fund's 'return of principal' characteristics of paying more than it earns.

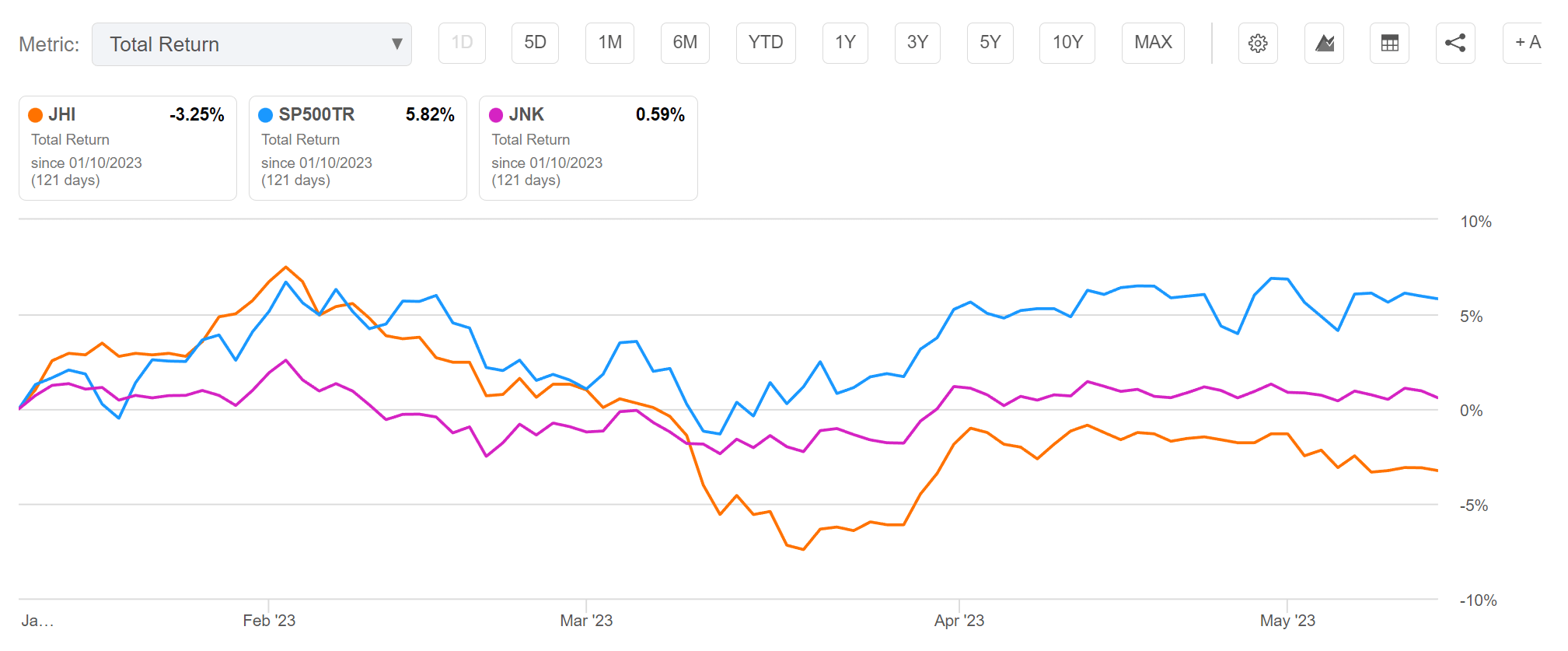

Since my article, the JHI fund has returned -3.3%, underperforming the high yield bond asset class as represented by the SPDR Bloomberg Barclays High Yield Bond ETF ( JNK ) and equity markets as represented by the S&P 500 Total Return index (Figure 1).

Figure 1 - JHI has underperformed high yield bonds and stocks (Seeking Alpha)

{kind=link}

With five months of the year almost done, has my views on the JHI fund changed? Is there anything on the macro front that investors in JHI should watch out for?

Distribution Cut Was Predictable And Expected

As I warned in my last article:

Given JHI's high distribution rate (9.3% current yield) but mediocre total returns (10Yr average annual returns of 3.6%), I am concerned the JHI fund shows all the hallmarks of a 'return of principal' fund, where it does not earn its distribution.

'Return of principal' funds are characterized by amortizing NAVs and shrinking distributions.

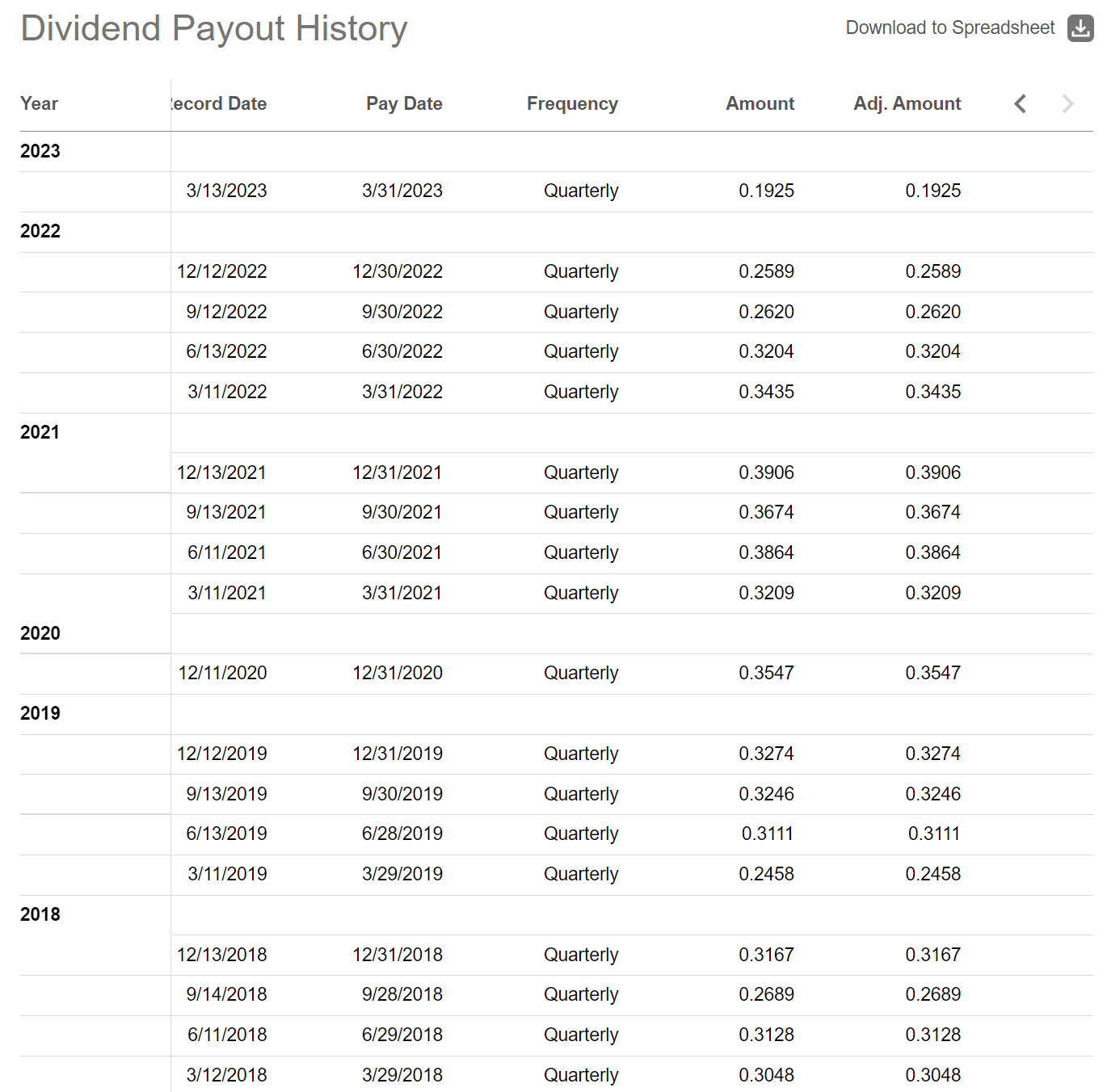

Sure enough, recently, the JHI fund cut its quarterly distribution steeply in the latest March quarter to $0.1925 / share from $0.2589 in Q4/2022, a cut of 26% (Figure 2).

Figure 2 - JHI continues to cut its distribution (Seeking Alpha)

{kind=link}

The current distribution rate of $0.1925 / quarter annualizes to 6.1% on market price and 5.6% on NAV, which is much more sustainable in my opinion compared to the prior 9.3% yield.

However, the problem for long suffering JHI unitholders is that we may be on the cusp of a recession, as credit conditions for US businesses and households grow increasingly tighter.

Increasing Signs Of An Impending Recession

As we move deeper into Q2, the economic clouds are certainly darkening. For example, in March, we saw the lagged effects of the Fed's interest rate increases finally starting to have an impact, causing several large regional banks to fail due to unrealized securities losses and deposit flight, both of which are caused directly by higher interest rates (for an explanation of how the Fed's actions have led to the regional banking crisis, please refer to my recent article on the iShares U.S. Regional Banks ETF).

In the face of higher cost of funding (from having to compete with money market funds for deposits), banks are set to further tighten their lending standards for businesses and consumers.

According to the recent Senior Loans Officer Opinion Survey ("SLOOS"), 46 percent of U.S. banks plan to further raise their lending standards on commercial and industrial loans to large firms due to worries about loan losses and deposit flight (Figure 3).

Figure 3 - Banks continue to tighten lending standards (Federal Reserve)

{kind=link}

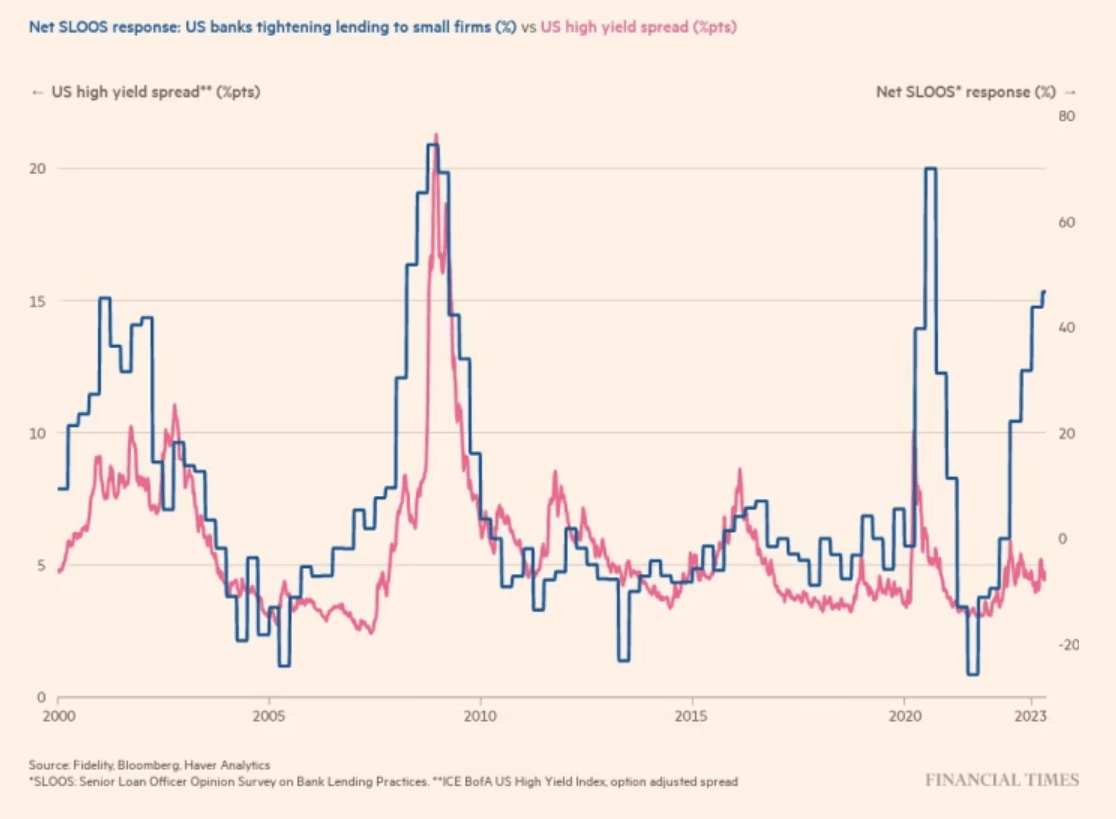

In the past, responses on the SLOOS survey have been a good predictor / coincident indicator for high yield credit spreads, as tighter lending standards raises the cost of funding for risky firms (Figure 4). There is no fundamental reason why this time should be any different.

Figure 4 - SLOOS survey tends to lead credit spreads (Financial Times)

{kind=link}

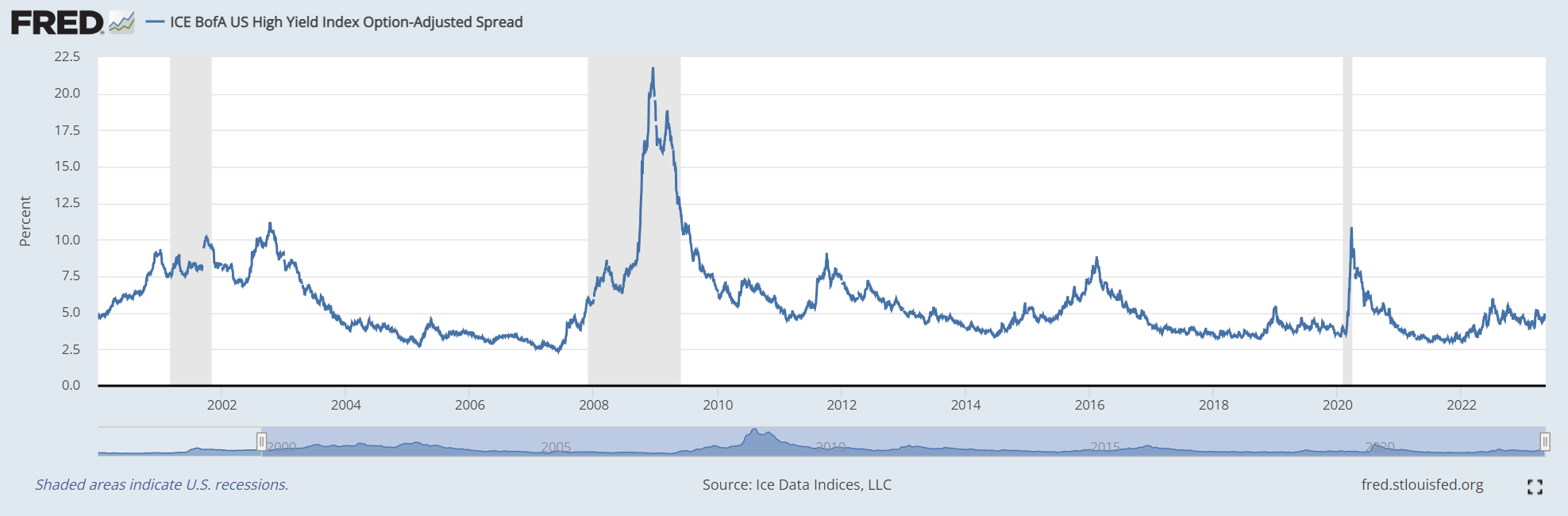

Furthermore, spikes in credit spreads have historically preceded and/or coincided with recessions (Figure 5).

Figure 5 - Credit spread spikes coincide with recessions (St. Louis Fed)

{kind=link}

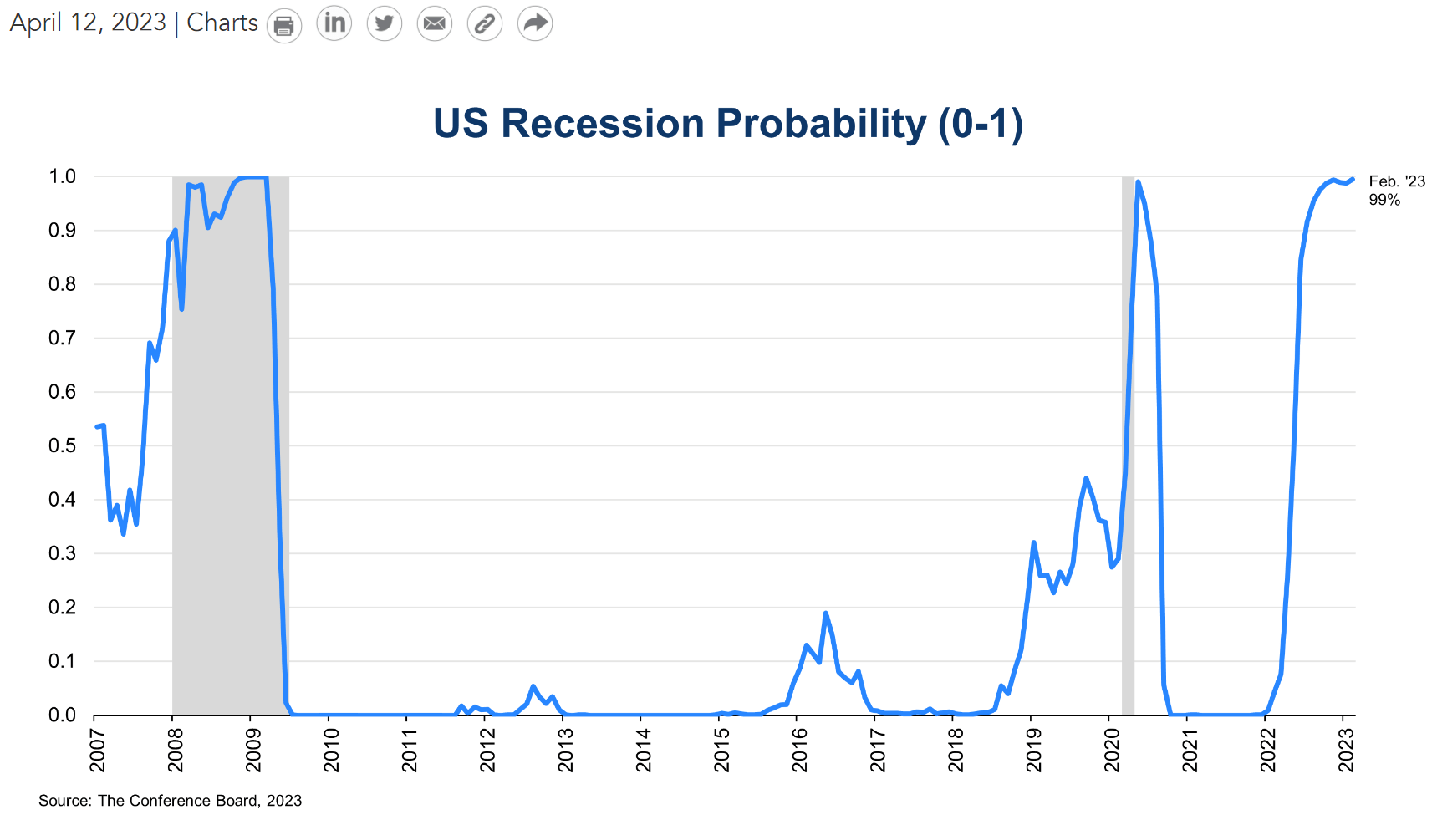

While high yield credit spreads are currently still benign at only 4.81%, figure 4 above suggest high yield credit spreads are set to widen significantly in the near future, which may coincide with an impending recession as predicted by many economists (Figure 6).

Figure 6 - U.S. recession probability at 99% (Conference Board)

{kind=link}

JHI Is Full Of High Yield Bonds

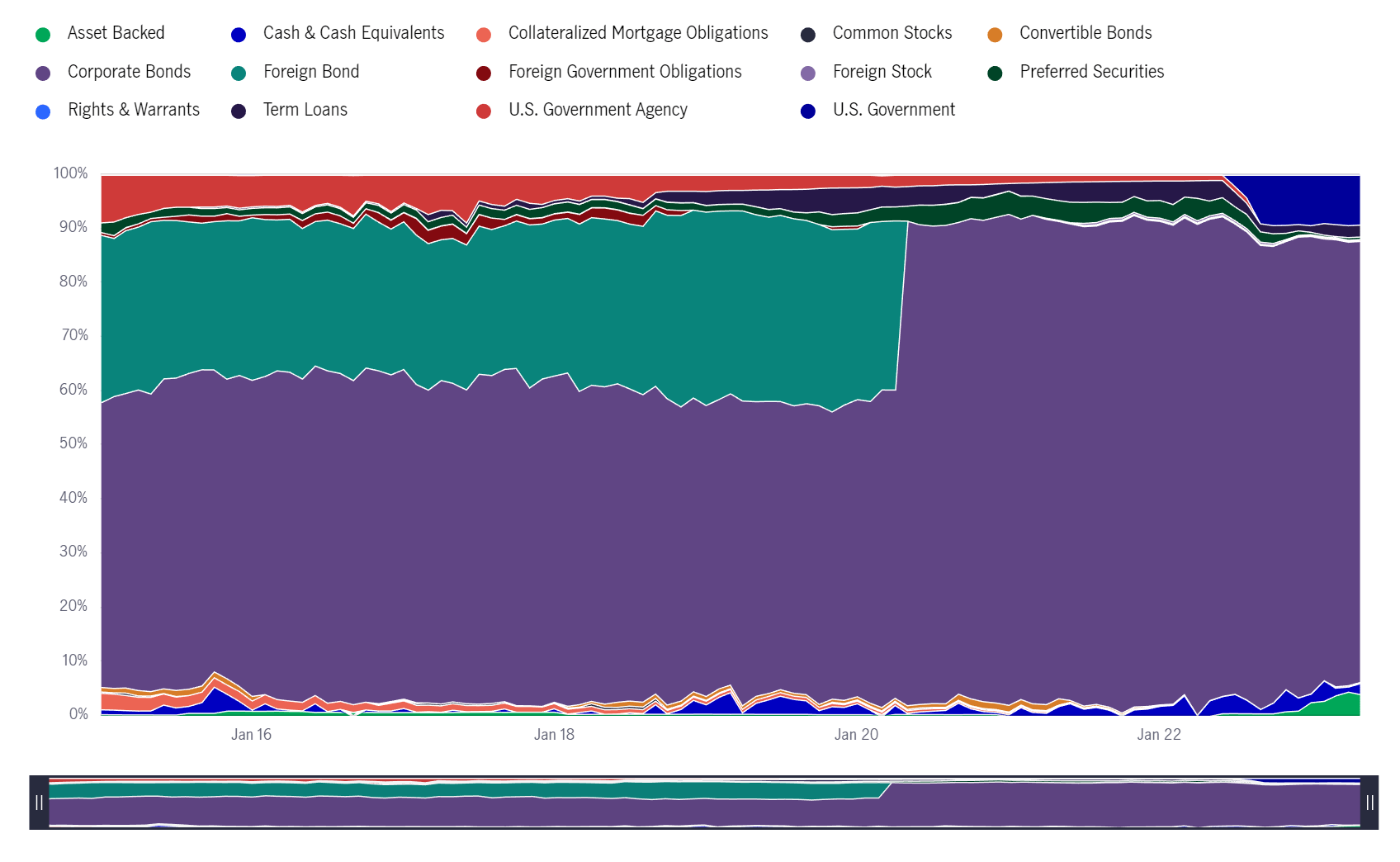

For levered credit funds like the JHI, a recession / credit spread widening event is very negative for the fund, as 81.5% of the fund's assets are corporate bonds (Figure 7).

{kind=link}

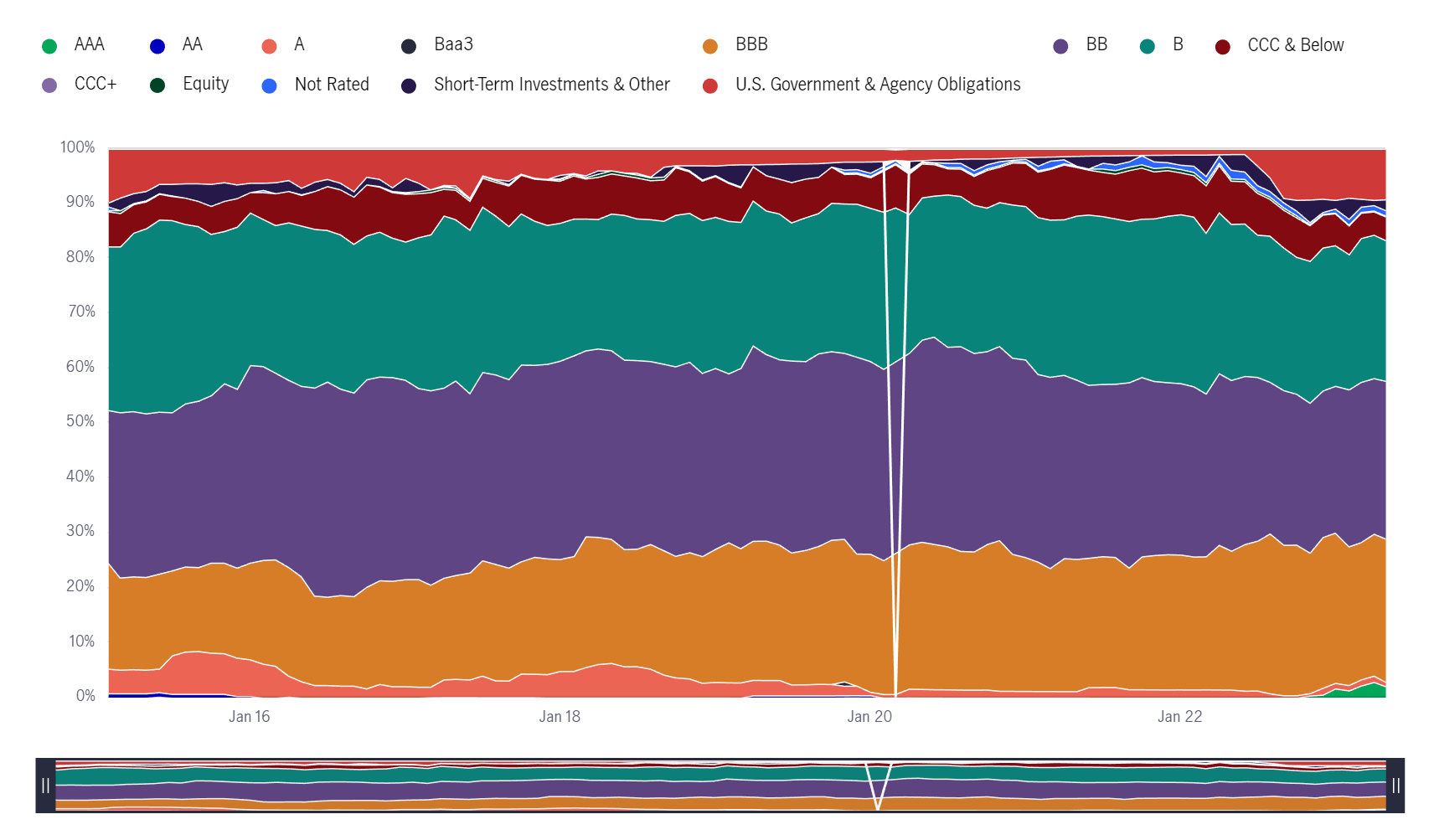

Furthermore, the credit quality allocation of the fund is predominantly non-investment grade securities, with 28.8% of the portfolio rated-BB and 25.6% of the portfolio rated-B, and approximately 5% rated-CCC and below or unrated (Figure 8).

Figure 8 - JHI credit quality allocation (jhinvestments.com)

{kind=link}

High yield bonds tend to suffer large mark-to-market ("MTM") price declines during recessions as credit spreads spike higher in anticipation of credit defaults. Historically, we can see that JHI's NAV tends to tumble whenever credit spreads widen significantly (Figure 9).

Figure 9 - JHI's NAV trades inversely to high yield credit spreads (Author created with price chart from stockcharts.com)

{kind=link}

During recessions, high yield credit spreads can easily widen to 8-10%. With effective duration of 2.6 years , every 1% increase in credit spreads could lead to a 2.6% decline in the portfolio, using a first order approximation.

A Recession Could Be A Buying Opportunity

On the bright side, a recession could be a buying opportunity for patient investors looking to play a credit recovery.

Due to the mean reverting nature of credit spreads, eventually, credit spreads will normalize and investors who have the courage to buy in the depths of recessions will likely earn above average forward returns even if a few of the fund's portfolio investments go into default. The difficulty is having the patience to wait for a good reward/risk entry.

Conclusion

Although the JHI fund's recent distribution cut addressed some of my concerns regarding the fund's 'return of principal' structure, I believe now is not the time to buy the JHI fund as we are on the cusp of a recession. Recessions are normally accompanied by spikes in credit spreads, which negatively hurt levered credit funds like JHI through their high yield bond holdings.

However, not all is gloom and doom. Recessions are also terrific opportunities for patient investors to buy levered credit funds from panicked investors. This is because credit spreads will eventually normalize, and investors who have the courage to buy during recessions may enjoy above average forward returns.

For further details see:

JHI: Recession Incoming, Avoid