JKS - JinkoSolar: A Very Strong Quarter In A Very Difficult Environment

2023-11-15 05:05:04 ET

Summary

- JinkoSolar's share price declined during the year due to falling ASPs, but Q3 results were phenomenal, leading to a little share price recovery that we believe has legs.

- The company's Q3 results showed higher margin N-type cells and Tiger Neo modules will make up 85% of sales next year.

- Despite declining ASPs and currency headwinds, JinkoSolar performed well and expects a good 2024 in terms of EPS.

JinkoSolar ( JKS ) is the leading Chinese solar manufacturer that experienced a major decline in its share price during the year on the back of falling ASPs:

FinViz

However, despite that challenge, the third quarter results were simply phenomenal, and a share price recovery has started on the back of these results.

Management argues that ASPs will stabilize and analysts still expect a bumper 2024 in terms of EPS. We think they are onto something.

Positive

There are lots of positives to take away from the Q3 results.

- Higher margin N-type cells, Tiger Neo modules will be 85% of sales next year

- Falling ASPs compensated by a shift towards Tiger Neo, lower polysilicon prices, and an improving US market

- Financial metrics up significantly

- Gross margin expansion

- Operating leverage

- Debt reduction

- Dividend

- Increased guidance

- Shares are cheap

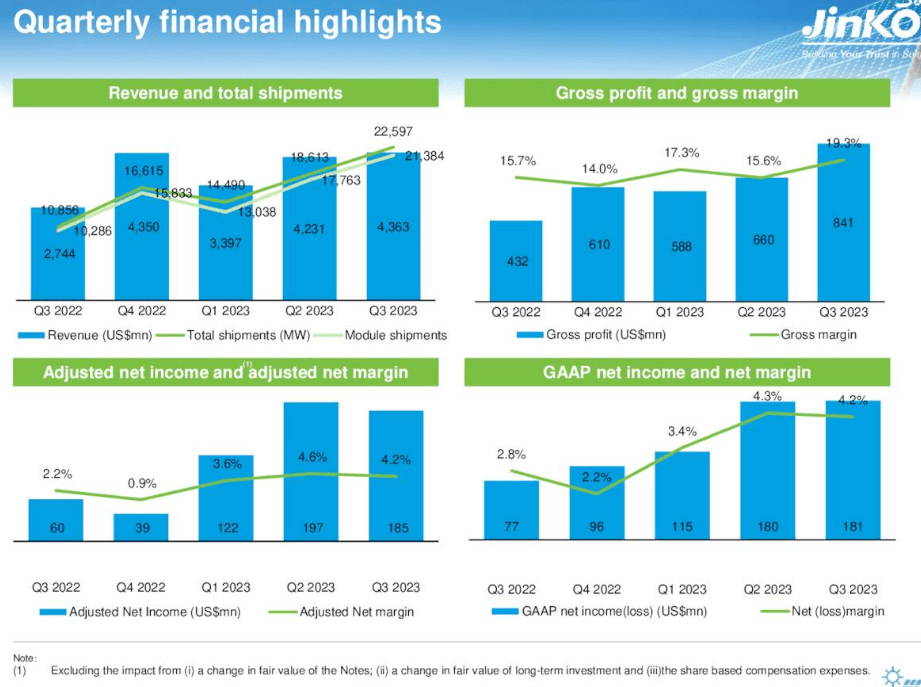

The company posted very good Q3 results with all metrics making significant gains over last year:

{kind=link}

Shipments were up 108.2%, revenue was up 63.1%, net income was up 140.7%, adjusted net income was up 215.1%, gross margin was up 360bp (to 19.3%), OpEx was up just 4.5% and diluted EPS was up 188.7% to $0.63.

Basically a good news show, although one can tease out two problems:

- Revenue growth was considerably slower than shipment growth, pointing to declining ASPs

- There was a considerable degree of currency headwind: RMB300M versus a RMB500M currency tailwind in Q3/22.

It's remarkable that the company performed so well in what is generally considered tough industry circumstances, with rising interest rates biting green energy projects and customers hesitating in the face of rapidly falling ASPs and many peers suffering declining profits.

What helped was that the company generated 40% from their home market where interest rates aren't a problem and installations were up 50%, although margins are slightly lower in China.

The company gets an increasing amount of revenue from its premium N-type technology (and Tiger Neo modules), which have higher conversion efficiency and sell at a premium:

JKS earnings deck

So far these were good for 57% of revenue this year but management expects this to rise to 85% of revenue next year. The company has seen a 360bp rise in gross margin on:

- Polysilicon cost falling faster than ASPs

- A shift towards higher margin Tiger Neo modules (with N-type cells)

- Improving US market

The latter warrants some explanation. As a Chinese company, Jinko had to be able to show the origin of its polysilicon due to the Uyghur Forced Labor Prevention Act (UFLPA).

In H1/23, there were still a considerable amount of Jinko panels in US customs, which adds costs as well as foregoes revenues, but this was already less the case in Q3 and will be even less in Q4. Next year the situation will normalize and the US will contribute to gross margins next year.

Management expects to ship more than 10GW to the US next year. We might keep in mind that they actually have a plant in the US in Jacksonville the capacity of which is being expanded from 400MW to 1GW and might even benefit from the IRA, but that's not a given.

The company experienced a great deal of operating leverage with operating expenses flat for a couple of quarters, OpEx rose just 4.5% y/y to $430.8M:

Negatives

- Rapidly declining ASPs

- RMB300M currency headwinds

- High-interest rates

ASP declines have been considerable this year :

LinkedIn

Management expects ASPs to continue to decline in Q4 but stabilize next year. Luckily, the fall in polysilicon prices has been even steeper ( PV tech ):

PV Tech

Given that most solar stocks, very much including Jinko, have been under considerable pressure the expectations seem to be that things will get worse. That is, panel ASPs falling faster than polysilicon prices.

That could lead to margin contraction and indeed management guides Q4 gross margin a tad lower than the stellar 19.3% in Q3.

Meanwhile, the company is booming and generating enough cash to pay back debt as well as surprise shareholders with a dividend of $1.50 per ADS , which produces a 5% yield at a $30 share price. It's interest bearing debt was $4.23B at the end of Q3, down from $4.73B at the end of the last quarter.

Higher interest rates are negative as:

- They make financing green energy projects more expensive

- They increase Jinko's interest costs

Net interest costs increased 15.1% to $20.3M despite the decline in interest-bearing debt. Interest-bearing debt $4.23B up from $4.16B at the end of Q2/22 but down from $4.73B at the end of Q2/23.

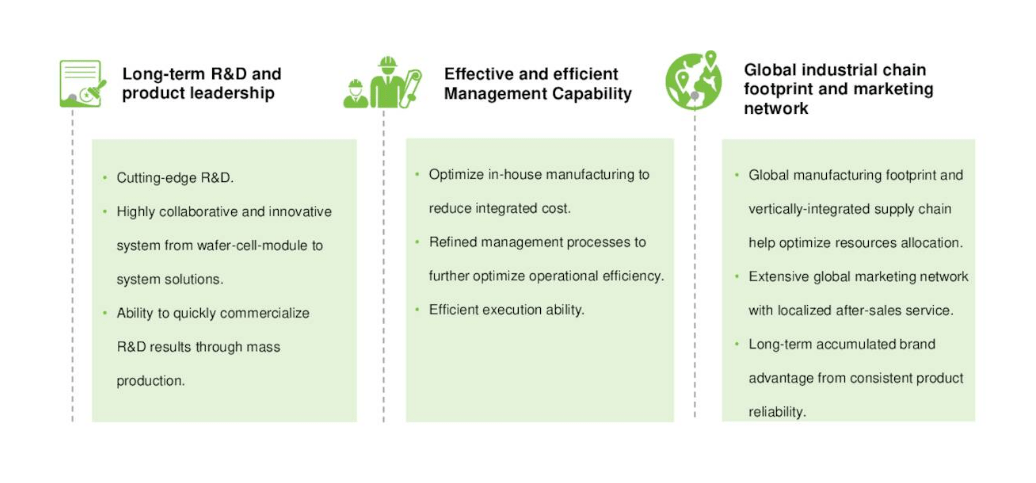

Top Tier-1 integrated producer

{kind=link}

With a possible further downturn in the ASPs, which seems what the market is expecting, the company will be affected but less so than others, due to its competitive strength which consists of the following elements:

- Top N-type cell producer setting efficiency records

- Integrated producer (wafers, cells, modules, panels)

- Worldwide sales and production network

- One of the most bankable solar companies, AAA rating

- Overall Highest Achiever for the fourth consecutive year in Renewable Energy Testing Center's ("RETC") PV Module Index Report ("PVMI")

What normally happens in a downturn is that the Tier-1 producers are less affected compared to lower-tier producers, given their superior cost structure and bankability.

Guidance

{kind=link}

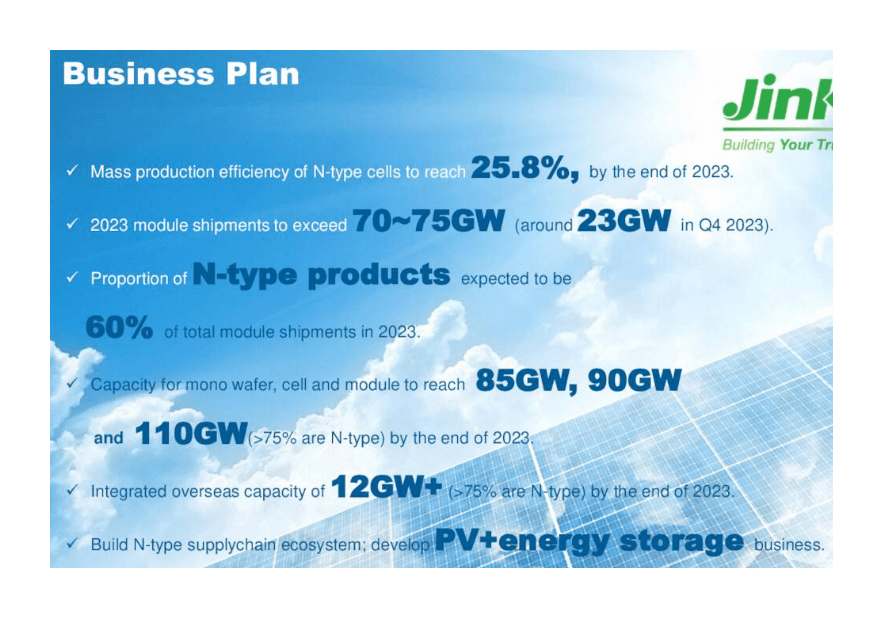

FY23 shipments are going to exceed the guided 70-75GW range (they were 52GW in the first nine months of the year). Q4 shipments are guided at 23GW. Management sees market demand rise another 20-25% next year.

Valuation

There is something odd:

Gross margin and EPS are at a three-year high while the stock price just came off of a three-year low, clearly the market doesn't believe that the margins will maintain at these levels, but even so, it's quite remarkable.

The company recently paid a dividend of $1.5 per share (5% yield) and is paying off debt as well with the US market normalizing for them so it's curious to know what they'll have to do to get some interest from investors.

Conclusion

Earnings, and gross margin at three-year highs, the company started to pay a dividend with a pretty good yield (5%) and is paying off debt. Its revenue growth is hefty, there is a good deal of operating leverage, production shifts almost entirely towards higher margin N-type cells next year (the target is 85%), and the US market is normalizing and will contribute to margins next year. Earnings valuation is on ridiculous multiples (the shares trade on less than 3x this year's and next year's earnings).

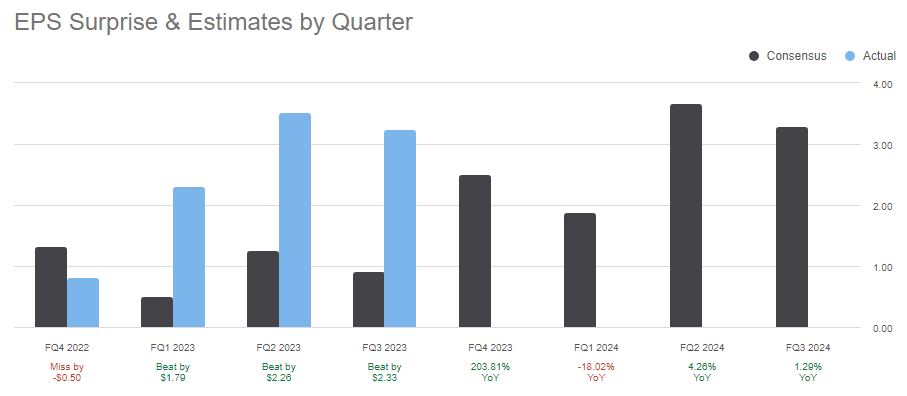

Basically, it's a good news show. The stock price just recovered from a three-year low and analyst expectations remain firm ( from SA ):

{kind=link}

Note also the huge beats in the last three quarters which did nothing for the share price, but we think this time will be different and see further upside for the shares.

The upshot : We are somewhat baffled, by all metrics, the company is doing extremely well but until very recently, none of this is reflected in the share price, which kept declining precipitously, despite analyst expectations remaining solid for next year.

It's either the China discount and/or investor fear of high-interest rates eating into the energy transition and/or ASPs falling much further (but somehow without affecting ESP expectations).

The shares seemed to trade on fear for most of the year, and that fear looks overdone to us, given the stellar results in a difficult environment. Of course, the risk is that the environment will worsen, but the shares have gotten so cheap that we think they should be able to bear that, bar any major catastrophe.

For further details see:

JinkoSolar: A Very Strong Quarter In A Very Difficult Environment