JKS - JinkoSolar Holding In The Grip Of China And Solar Fears

2023-08-21 21:37:32 ET

Summary

- JinkoSolar's shares have recently performed poorly despite strong Q2 results and improving access to the US market.

- The company is executing capacity increases and has a positive outlook for Q4 in China.

- Concerns about overproduction in the Chinese market and declining ASPs may be impacting investor sentiment.

It's not immediately obvious why the shares of JinkoSolar ( JKS ) has done so badly recently:

FinViz

- The company produced stellar Q2 results.

- The results would have been even better if not for a one-time inventory write-off on polysilicon inventory, the price of which started to plummet in June.

- Access to the US markets is improving and the hold up (and significant costs) at the border for their modules is decreasing. The company is also building a plant in the US.

- The company is executing big capacity increases, much of which are financed out of cash flow and the remainder from a recent offering in China.

- Not even a Chinese economic slowdown seems to be a factor as management expects a bumper Q4 in China.

- Sentiment on the CC which was less than a week ago was excellent.

Q2 Results

Very solid results, especially the rise in net income:

{kind=link}

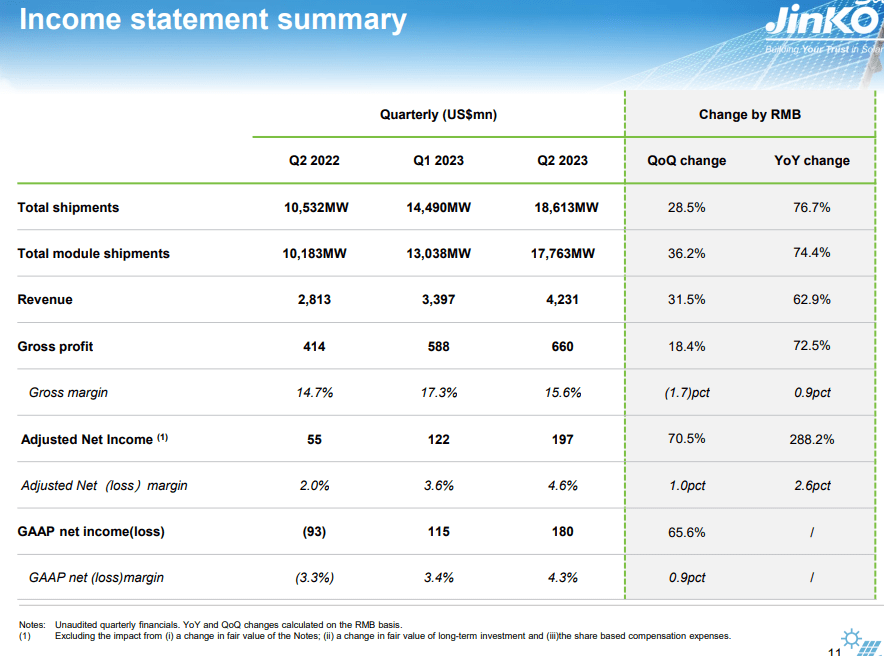

So module shipments increased 36.2% sequentially and 74.4% y/y and revenues were up 31.5% sequentially and 62.9% y/y, that's quite a bumper quarter. A three-year perspective shows impressive growth as well:

Ok, it's no longer the 100%+ growth rate of a year ago but we would argue that 53% is still pretty hefty. Keep in mind this is in US$, not GW so it included ASP declines. Now, revenue growth is one thing, margins are another. However:

Here too the company is doing very well, and management conceded that the gross margin would have been 20% but for a whopping RMB400M Inventory write-off in Q2.

Then there were the RMB200M US port charges (down from RMB400M in Q1) as their modules get held up for inspection of the origin (Xinjiang) of content. This is going to almost disappear in Q3.

The company is also increasing the percentage of higher-efficiency N-type modules, which have better ASPs and margins. They were 50% of sales in H2 but that will be 60% for FY23.

{kind=link}

There is quite an impressive OpEx decline as well, from 16% of revenue in Q2/22 to 12% in Q1/23 to 11% in Q2/23, there is quite a bit of operating leverage kicking in, which is visible in the graph above.

CapEx

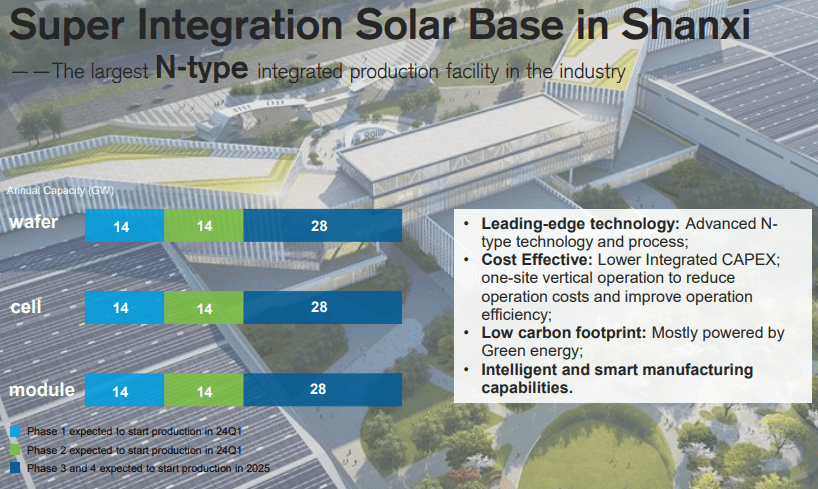

Should we be worried about the big plant the company is building in Shanxi?

{kind=link}

The company's FY23 CapEx will be RMB15B, but the company also expects RMB10B+ in operating cash flow this year (it also has $2.35B in cash). Apart from that, their majority-owned subsidiary Jiangxi Jinko embarked on a RMB9.7B share offering in Shanghai.

That could be the reason for some headwinds in the US ADS as management argued it would lead to a 7-9% dilution for ADS holders, but that's it, they're covered for next year as well (Q2CC):

So we don't foresee any additional cash needs next year for the 12 gigawatts integrated capacities.

1GW US capacity coming online in September (which will bring IRA advantages but management isn't budgeting for these), 12GW capacity overseas by yearend, 75% of which will be N-type capacity.

Outlook

The polysilicon crash that started in June has created some hesitations from buyers, waiting for more favorable prices (as well as causing the above-mentioned one-off inventory write-down) but the resulting ASP decline has led management to increase FY23 shipment guidance to 70-75GW ( up from 60-70GW ), with N-type approximately 60% of that.

Management has 80% order book visibility for 2023 already, so they can have considerable confidence in that guidance. The outlook for the Chinese market is brightening ( Bloomberg ):

The country installed almost three times the volume of solar capacity between January and the end of April than in the same period in 2022, and is on track to add more panels this year than the entire total in the US...

The nation might set up 154 gigawatts of solar capacity this year, BloombergNEF claimed on Monday, elevating its China forecast from a previous total of 129 gigawatts. The US had a cumulative total amount of 144 gigawatts installed at the start of 2022, according to BNEF data.

Installing 154GW is an extraordinary figure but 2024 might be even much better:

Installments in China might rise to 200 to 300 gigawatts next year, Liu Hanyuan, chairman of top polysilicon manufacturer Tongwei Co., said in a meeting on the sidelines of the SNEC PV Power Expo, the industry's largest China seminar that opened up Tuesday in Shanghai.

And the outlook for subsequent years also increased according to BloombergNEF:

Bloomberg NEF

It might seem strange that despite this booming demand there are actually fears of overcapacity in China although this is mostly related to polysilicon capacity and not everybody is convinced ( Bloomberg ):

Others pushed back against overcapacity concerns. Companies that are expanding are doing so because their customers need it, said Li Junfeng, executive council member of the China Energy Research Society. “These are the industry leaders, they’re on the front lines, they know the market characteristics the best,” Li said on a panel Tuesday.

If there is any worry it's about declining ASPs, but there are offsetting forces in H2:

- Lower ASPs boost demand, hence the increase in FY shipment guidance.

- Shipments to the US will accelerate in Q3 (but this is included in the guidance).

- Lower ASPs are a direct result of the polysilicon price decline so costs also decline, management isn't guiding for lower gross margins.

- The disappearance of the inventory write-down and US port charges.

- The increasing percentage of N-type modules in sales.

- Yuan depreciation making solar panels cheaper abroad.

- Operating leverage.

- Next year their energy storage business will also start to gain traction.

And of the wider fear of overproduction and a price plunge in China, management argued (Q2CC, our emphasis):

The second half year is, for sure, in a downward trend but it has been stabilized. And we believe, thanks to the very, very strong China installations, particularly in Q4 this year, the ASP will may turn and maybe possible relatively in upward trends ...And for this year, we believe the momentum will continue and year-over-year. It's a very good year for Jinko in terms of the profitability, even in the second half year.

So while Jinko's management doesn't see any imminent crunch, but we still think this is the most likely reason for the declining stock price and this is reflected in the wider sector:

FinViz

So despite Jinko's stellar results and optimism, it looks like they are being thrown out with the bathwater by investors. The solar ETF TAN is at a three-year low:

FinViz

With $9.54 in EPS expected for FY23 the shares can be considered cheap although p/e ratios are of lesser value for cyclical companies.

Conclusion

Despite stellar results, a cheap valuation and a booming market, the shares of JinkoSolar have plunged recently and the one reason we can find is fears of overproduction in the Chinese market.

Given the magnitude of the Chinese solar boom, these fears seem curious as demand is rip-roaring higher. Jinko's management doesn't seem to see any imminent crunch and even entertains the possibility of a reversal of the ASP declines in Q4 in China.

One should also keep in mind that most of the ASP declines are produced by a polysilicon glut and so the financial impact is damped by both rising demand as well as falling cost. Jinko also has a few other countervailing forces like renewed access to the US market and some one-off costs disappearing.

The Q2CC was just August 14 and there was very little negative sentiment from analysts or management, quite the contrary.

But in the end, it's fears of overproduction and falling ASPs and the increasing gloom if not outright alarm that is rapidly engulfing the Chinese economy that is spoiling sentiment for Jinko, despite the company set for a record year.

While the shares look oversold to us and might very well have a short-term bounce, we're a little concerned by what seems a rapidly worsening sentiment so we're staying clear for the moment.

For further details see:

JinkoSolar Holding In The Grip Of China And Solar Fears