JKS - JinkoSolar: No Slowdown For This Dividend Paying Solar Panel Maker

2023-10-19 14:00:36 ET

Summary

- JinkoSolar has become the largest solar module manufacturer in the world, with a strong market position and focus on innovation.

- The avoidance of U.S. sanctions makes North America a prime target for renewed growth and market share expansion.

- The stock trades at a significant discount to peers with a forward price-to-earnings ratio of 3.2x and price-to-book value of 0.58x.

- The announcement of a 4.75% dividend yield is a great start for shareholder returns in the coming years. A $200 million share buyback program is still running and could buy back 12% of the shares outstanding.

JinkoSolar ( JKS ) got caught up in the solar industry drawdown, even while revenues kept increasing above 50%. Although the stock outperformed its peers, it is trading at a steep discount compared to the others on the list. The recent dividend announcement of almost 5% is a promising start to the increase of shareholder value for the coming golden years. The avoidance of the U.S. tariffs on imports will make JinkoSolar one of the main industry leaders in the North American solar module market.

Business Overview

JinkoSolar is a global leader in the solar photovoltaic (PV) industry. The company is headquartered in the Jiangxi province, China, and has production facilities in China, Malaysia, Vietnam, and the United States. Next to that, it has strategically positioned regional offices, warehouses, and subsidiaries in more than 30 key solar markets worldwide, enabling it to effectively serve its customers.

JinkoSolar operates a vertically integrated business model, encompassing the entire solar value chain (excluding polysilicon). The company designs, manufactures, and sells a range of solar PV modules, as well as other solar energy products and services. Wafers and solar cells that are not used in solar module production are sold to peers in the industry. JinkoSolar's products are used in a wide range of applications, including residential, commercial, and utility-scale solar power projects.

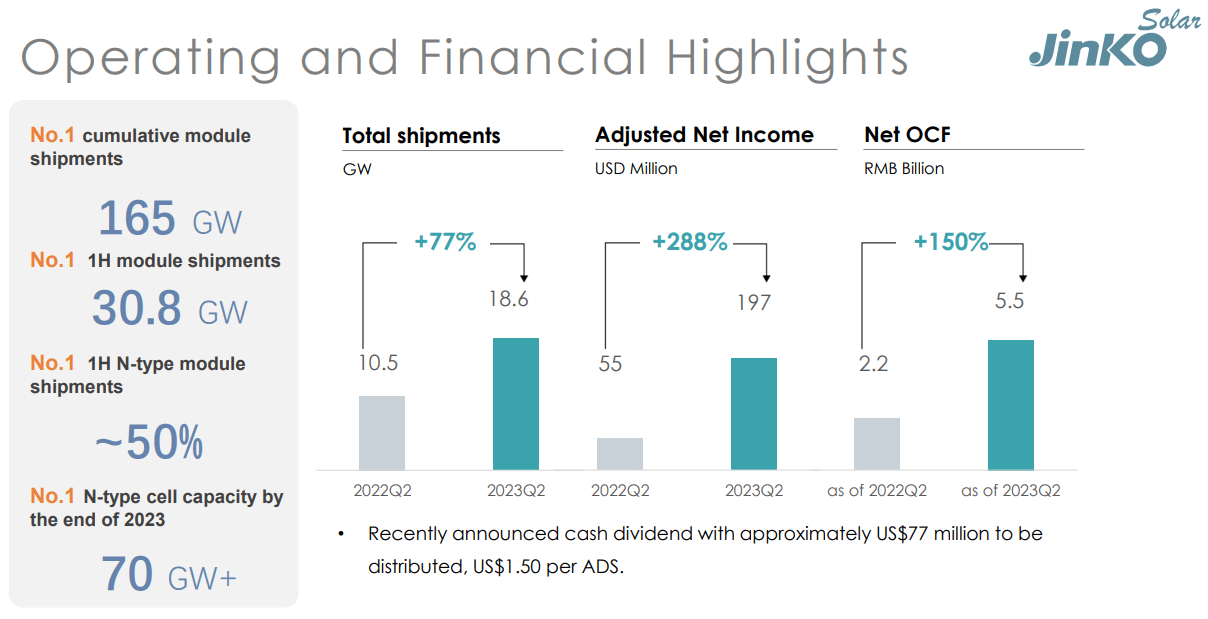

JinkoSolar has become the largest solar module manufacturer in the world, with a total of 30.8 GW of solar panels shipped in the first half of the year. The company's products are highly regarded for their quality and performance, and have been used in some of the world's largest solar power projects.

Graph made by author

JinkoSolar competes with a number of other solar module manufacturers, including First Solar ( FSLR ), JA Solar, LONGi Solar, Canadian Solar ( CSIQ ) and Trina Solar. The company has some main competitive advantages that include its large production capacity, its global reach, its strong brand recognition, and its constant innovation.

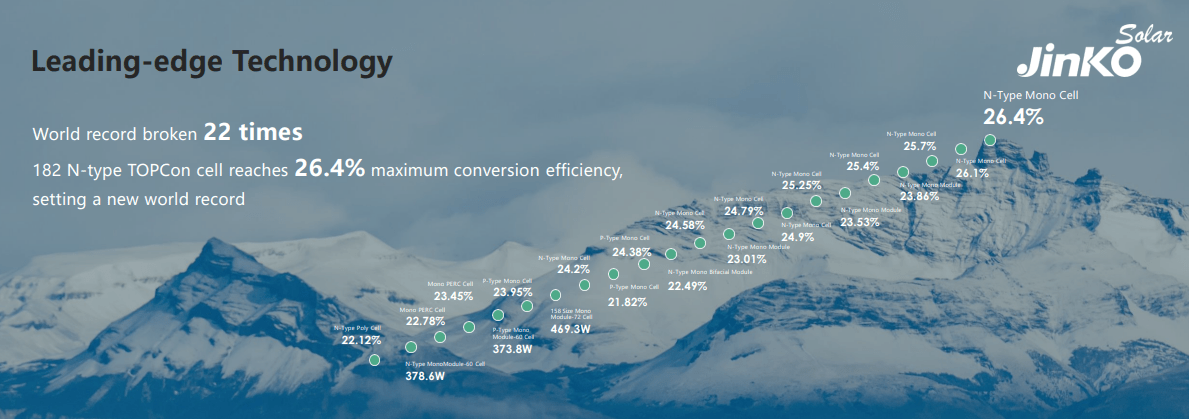

JinkoSolar has achieved several milestones in solar module efficiency, including record-breaking conversion efficiencies for its products. By continuously investing in R&D, the company aims to stay at the forefront of technological advancements, improve energy generation efficiency, and drive down the levelized cost of energy for solar power.

Technological Progress

There are several different solar module technologies available, each with its own advantages and disadvantages. Monocrystalline PERC is currently the most popular type of solar panel, but it has reached its limits in terms of energy efficiency. N-type TopCon technology is rapidly gaining market share and is expected to account for 62% of the overall market by 2026.

N-type TopCon solar panels are more energy-efficient and relatively inexpensive to produce. Two other upcoming technologies, HJT and xBC, are more complex to manufacture and therefore more expensive. HJT has high efficiency and can achieve very high bifacial rates, but it struggles with panel power output.

xBC technology is used by Aiko Energy to produce panels with high efficiency and power output. However, they are new to the market and expensive to build.

JinkoSolar is the industry leader in the manufacturing of N-type TopCon solar modules. The company has broken the world record for panel efficiency 22 times, with the current record standing at 26.4%. The average mass-production cell efficiency is 25.8%.

{kind=link}

In addition to efficiency, JinkoSolar's panels also have the advantage of producing high power output, up to 635W for the Tiger Neo module. The Tiger Neo is a best-in-class panel, outperforming panels from SunPower ( SPWR ), Maxeon ( MAXN ), LONGi, and Trina Solar. Only Aiko's xBC panels match the efficiency of N-type TopCon panels, but JinkoSolar still has the edge in power output.

Canadian Solar's latest TOPBiHiKu7 Bifacial is another high-performing panel that beats Jinko's power output by 45-65W due to its exceptional bifaciality (85% compared to Jinko's 80%) and slightly lower efficiency.

Overall, JinkoSolar has a strong track record of innovation and producing high-quality solar modules.

Growth Opportunities

Although JinkoSolar is already the largest solar panel maker worldwide, it is still growing at the fastest rate compared to competitors. In the second quarter, total shipments grew by an impressive 77%. The company's investments in a global vertical integrated manufacturing complex have increased the efficiency in logistics, transportation and the ability to serve all customers, which are now translating into margin expansion and net income growth.

While polysilicon prices have decreased immensely, JinkoSolar was able to stack up inventory. As a result, margins could remain high in the third quarter of 2023, since most modules are being built with cheap polysilicon. On the other hand, solar module prices have also come down and might cause a counter effect on the profit margin, but a decline in solar module prices will again increase the demand for solar projects.

{kind=link}

One of the large benefits JinkoSolar has compared to the other Chinese solar module manufacturers is the overseas vertical integrated capacity of over 12 GW. Delivering solar panels to the United States has been difficult and under strict rules. However, JinkoSolar was able to bypass tariffs by externally buying polysilicon outside China for the American market and manufacturing the wafers, cells and modules in Vietnam or the United States itself. The other solar panel makers only did the finishing of products outside China and now face the consequences. Considering only 6% of U.S. family homes have solar panels on the roof and solar utility is rare in America, Jinko expects to regain market share and double the sales. In the second quarter earnings call , the CFO mentioned that the shipment target to the U.S. is expected to grow from 4-7 GW to more than 10 GW in 2024.

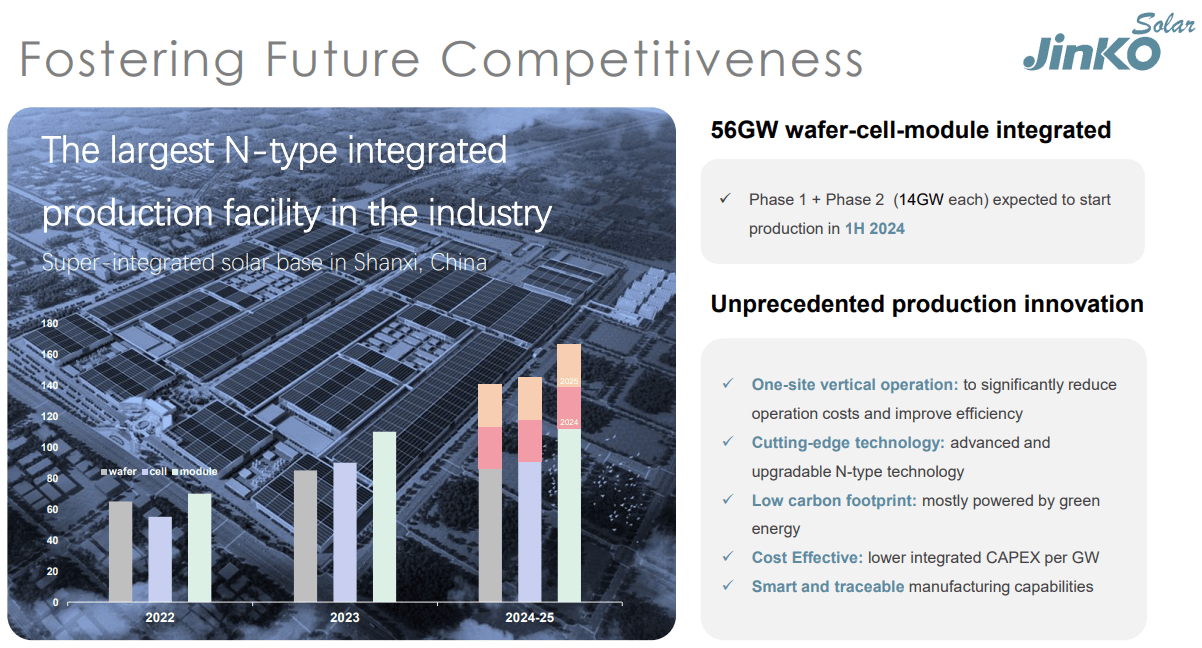

Further, the solar panel manufacturer is expanding their N-type production capacity by 56 GW with a new integrated production facility in Shanxi, China. The one-site super facility will drive down operational costs, scale up efficiencies and be able to support the latest technology of solar panels. First production is expected to start as soon as 2024. This large investment will be partly funded by the issue of ordinary shares or dilution of the STAR listing Jinko Solar (688223.SS) for no more than RMB9.7 billion or $1.3 billion. The CFO expects a slight dilution of JinkoSolar shareholders of the subsidiary from 58% to 53%.

{kind=link}

Valuation

Historically, JinkoSolar only traded once below the current price-to-sales ratio when the company saw its revenue stagnate for a few quarters back in 2017-2018 and the stock price dropped from $30 to below $8. The stock price saw a similar drawback this time around, but all the while the fundamentals are getting better for the company. The same can be said about the price-to-book value, that is trading at 0.58x and is closing in on the 2019 low.

In addition, when we compare JinkoSolar with competitors that trade on the public market, it is visible that the business is highly undervalued. Next to JinkoSolar, Canadian Solar is the only stock that trades at a similar valuation.

Based on EV-to-EBITDA, Canadian Solar is the cheapest stock with JinkoSolar in second place. Nevertheless, JinkoSolar is increasing its EBITDA at a higher pace each quarter, which is illustrated in the graph below.

Despite multiple solar panel makers seeing a slowdown in revenue growth, JinkoSolar was able to grow (not 53%) but 63%. This might have to do with capital expansion delays for some of the other companies. Yet, JinkoSolar is quietly increasing its market share and dominance globally, showcasing its know-how in the business. Technically, the company is a fast-growing business, still it is priced as a dying and bankrupt business.

Balance Sheet, Dividend and Share Buyback

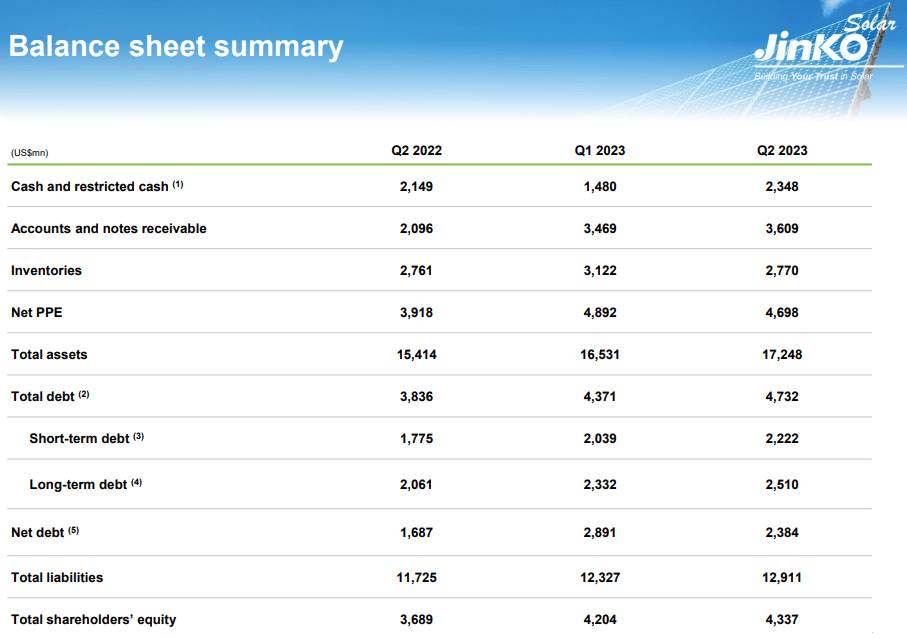

Finally, it is time to have a look at the balance sheet to see if the company has financing problems or could go bankrupt. Their balance sheet is not the best I have ever seen, but there are no short-term problems to pay the bills. The solar module business is capital-heavy and the expansion strategy of management secured the market position they have right now. The current ratio is 1.11x, which indicates that the current assets are higher than the current liabilities. Overall, I expect the cash-in to increase in the following quarters and towards next year, resulting in more flexibility in the cash allocation.

{kind=link}

The management agrees with me that the best days of profitability are ahead, by announcing a cash dividend . A $1.5 per ADS dividend will be paid out to shareholders as of November 24, 2023. This accounts for a solid dividend yield of 4.75%. The advantage of being massively undervalued is that the dividend will cost only $77 million, or 3% of the cash position. Another benefit is that the dividend yield can lead to an indirect share buyback. The shareholders will have the choice to buyback cheap JinkoSolar shares or invest somewhere else with the money.

Furthermore, JinkoSolar has an open share buyback program of $200 million, that could buy back around 12% of the shares outstanding. I did not find any news that management had already spent any money on repurchases, but at the current valuation repurchasing shares would be optimal. A secondary benefit would be the counter of dilution on the Chinese subsidiary stake JinkoSolar has. Since the Chinese listed subsidiary shares trade at a much higher multiple of 16.8x earnings compared to JinkoSolar's multiple of 3.3x earnings, it is very easy to use arbitrage and increase their stake in Jinko Solar (STAR) again by retiring cheap ADS shares. For those that do not know, JinkoSolar's subsidiary is worth $12.4 billion, of which JinkoSolar owns 53% or $6.57 billion. As a result, the subsidiary stake is worth 4 times more than JinkoSolar itself. This indicates that Chinese shareholders value the subsidiary much more than investors in the American-listed company do.

Risks

Nonetheless, investors need to keep in mind that JinkoSolar has been identified by the SEC under the Holding Foreign Companies Accountable Act .

This means the company will be delisted by 2024, if they do not show the right auditing under the rules of the United States. The company is confident that the latest annual report followed the rules and that they should not be delisted. In case of a delisting, you get the chance to sell your shares, but the stock price could have already fallen substantially. For now, I personally do not think the U.S. will delist all the Chinese listed companies as most of the money is American and they would shoot themselves in the leg with a move like that. Yet, I suggest shareholders in Chinese companies to keep track of the auditing progress.

A few other fears investors have, are falling profitability and oversupply. Falling profitability can be caused by the decrease in module prices. So far, this is not a large worry since polysilicon prices have dropped even more and module prices are still catching up to that correction. Overall, lower module prices are a good thing as it will re-boost solar panel projects. Interest rates have a temporary effect on the demand for solar projects because it's not a small investment and borrowing money is getting more expensive. However, lower module prices and higher energy prices could make homeowners rethink that quickly.

Additionally, any oversupply concerns forget the long-term picture. Solar is growing incredibly fast year-over-year supported by international policies like USA's Inflation Reduction Act and Europe's REPowerEU. Solar is the most cost-efficient power-generating technology, improvements in panel efficiency, the cost decrease of panels, and the advancement in manufacturing efficiency will likely have a positive impact on the profitability of players like JinkoSolar.

Lastly, JinkoSolar's subsidiary is already giving positive signs for the next quarter. Jiangxi Jinko or Jinko Solar announced it shipped 52 GW in solar panels for the first nine months of the year. That would mean the subsidiary alone shipped more panels than the previous two quarters based on the total shipments of JinkoSolar. They also shared preliminary results with net income expectations for the first nine months of the year between RMB6.14 and RMB6.54 billion, increasing by 266% to 290% year-over-year. Both debunk the profitability and oversupply issues.

Takeaway

JinkoSolar has now been outperforming all solar module peers in terms of technology and operating performance for many years. The avoidance of the U.S. tariffs shows the excellent capabilities of the management team. New commitments to lower leverage on the balance sheet, improvements of cash and the increase of shareholder returns through dividends and buybacks are promising prospects.

The IEA (International Energy Agency) calls out that annual solar PV capacity additions will increase every year for the next five years. JinkoSolar is one of the only solar module manufacturers that has built out a global manufacturing base. They will be the main beneficiary of the tailwind in the industry and have the highest margins going forward, because of the vertically integrated manufacturing facilities in the best spots of the world.

I rate JinkoSolar a 'Strong Buy' and have built a position in my own portfolio in the last months. Despite the risk of China, JinkoSolar has been very compliant with the U.S. government, and I see enormous value in the shares of JinkoSolar today.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

JinkoSolar: No Slowdown For This Dividend Paying Solar Panel Maker