JLS - JLS: This 8.2%-Yielding CEF Is Well Aligned For The Current Environment

Summary

- We take a look at JLS - a CEF that allocates primarily to mortgage and securitized assets.

- JLS has a significant allocation to higher-quality floating-rate assets which aligns well with today's environment of inverted yield curve and tight credit spreads.

- JLS trades at an 8.2% yield and a 12.5% discount which provides a nice entry point, particularly in light of the recent large distribution hike.

This article was first released to Systematic Income subscribers and free trials on Feb. 1 .

In this article, we highlight the Nuveen Mortgage and Income Fund ( JLS ) which trades at a 12.5% discount and an 8.2% yield. JLS allocates primarily to mortgage and securitized assets with a significant holding of floating-rate assets. The current environment of an inverted yield curve, relatively tight credit spreads and resilient households favors a position in the fund in our view. Moreover, the fund's outperformance over the past year, a rising level of net income and recent distribution hike as well as attractive valuation support our view. We continue to hold JLS in our Defensive Income Portfolio.

Macro Investment Picture

It's always important to consider how a given security fits into the broader market and macro picture. In this section we look at the case for considering a fund like JLS which 1) has a significant amount of floating-rate assets, 2) holds relatively high-quality assets, 3) takes exposure to primarily mortgage assets such as residential mortgages while also having additional exposure to household-related assets such as Auto and Credit Card receivables.

The chart below shows the 3-month / 5-year Treasury yield curve. The curve is unusually inverted with short-dated yields exceeding their longer-dated counterparts by more than 1%. What this means is that the short-end of the yield curve is unusually attractive from an income standpoint relative to longer-term yields. JLS has half of its portfolio allocated to short-dated yield assets and benefits from this dynamic much more than a typical bond fund.

Systematic Income

Secondly, it can be useful to disaggregate the yield of typical credit assets into a risk-free portion (i.e. the Treasury yield) and the credit spread portion (i.e. the residual yield). Using high-yield corporate bonds as a proxy, what we see is that credit spreads make up a historically low portion of the total high-yield corporate bond yield. This century it was only lower leading up to the GFC (when credit spreads widened out sharply). What this means is that credit spreads are providing comparatively little compensation to investors which, in our view, means it makes sense to also allocate to higher-quality assets or at least avoid very low-quality assets.

Systematic Income

Finally, many income portfolios are already heavily tilted to corporate credit whether through loan or bond funds or BDCs. Having some allocation to funds that allocate to household-related assets such as residential mortgages or securitized assets provides additional portfolio diversification. Moreover, both residential mortgages and household-related assets remain relatively attractive assets given relatively high equity amounts in residential mortgages due to house price appreciation as well as a decent labor market and historically low debt service payments as a percentage of disposable income.

These key factors support a partial allocation to a fund like JLS in our view.

Quick Snapshot

JLS allocates primarily to securitized assets such as mortgage-backed and asset-backed securities. These span the gamut of residential and commercial mortgages, credit card, auto, aircraft ABS and others. Although these assets are not your typical assets like bonds and loans, they are very popular assets in the institutional investment space. JLS is also far from the only CEF that allocates to securitized assets - they make up about half the portfolios of PIMCO taxable CEFs.

The fund has a relatively high-quality credit profile with about a third allocated to investment-grade securities and about half the fund allocated to securities rated BB and higher (BB is the highest non-investment-grade rating bucket). About a quarter of the fund's positions do not carry a rating.

Nuveen

The fund has a modest duration of about 2.4 - less than half of a corporate bond fund and about a quarter of a leveraged Muni fund. It carries leverage of around 30%.

About half the fund is allocated to floating-rate securities, primarily held via residential mortgage assets.

Income Review

The fund has $148m of total assets. With 50% of floating-rate exposure that equates to around $74m of floating-rate assets. This is against $45n of repo which is also floating-rate for a net amount of $29m of net floating-rate assets. This means that the fund's net income should rise alongside the rise of short-term rates over the past year.

If we break down the fund's semi-annual net income figures this is indeed what we find. Over the past two years, net income has risen by 81%. It accelerated over the past 6 months because of the lagged effects of a jump in Libor over the middle of 2022.

Systematic Income

Another key factor in the fund's net income rise is the fact that its borrowings have risen as well. This is in contrast to most leveraged CEFs which were forced to deleverage over 2022. For instance, as we have highlighted a number of times, PIMCO taxable CEFs have had to shed 20-40% of their borrowings to keep their leverage from blowing up as their NAVs came under pressure. Because JLS entered 2022 with a modest level of leverage and because it holds relatively high-quality assets, it was instead able to add assets in an attractive yield environment, rather than having to sell them.

Systematic Income CEF Tool

JLS recently raised its distribution by 40% which reflects its rising level of net income. Because JLS holds relatively high-quality assets which trade at modest credit spreads, the rise in short-term rates has benefited JLS more than other funds as Libor forms a larger percentage of the fund's coupon stream.

JLS has what Nuveen calls a level distribution policy . Nuveen defines this as the following -

The goal of the funds’ level distribution program is to provide shareholders with stable, but not guaranteed, cash flow, independent of the amount or timing of income earned or capital gains realized by the funds. Each fund intends to distribute all or substantially all of its net investment income through its regular monthly distribution and to distribute realized capital gains at least annually. As a result, regular distributions throughout the year are expected to include net investment income and potentially a return of capital or capital gains for tax purposes.

On the face of it this distribution policy is not much different from what other CEFs already do. Some Nuveen CEFs with level distribution policies adjust their distributions several times a year so the policy is level until it's reset to a new, more appropriate level. If anything, this means that investors shouldn't expect monthly changes to distributions of CEFs with this policy. This should provide a measure of comfort for investors who don't like to see frequent distribution changes.

Valuation Review

It's fair to say that JLS has not been in the CEF market limelight. The fund is relatively small and its relatively low beta means it's not going to shoot the lights out in a strong market.

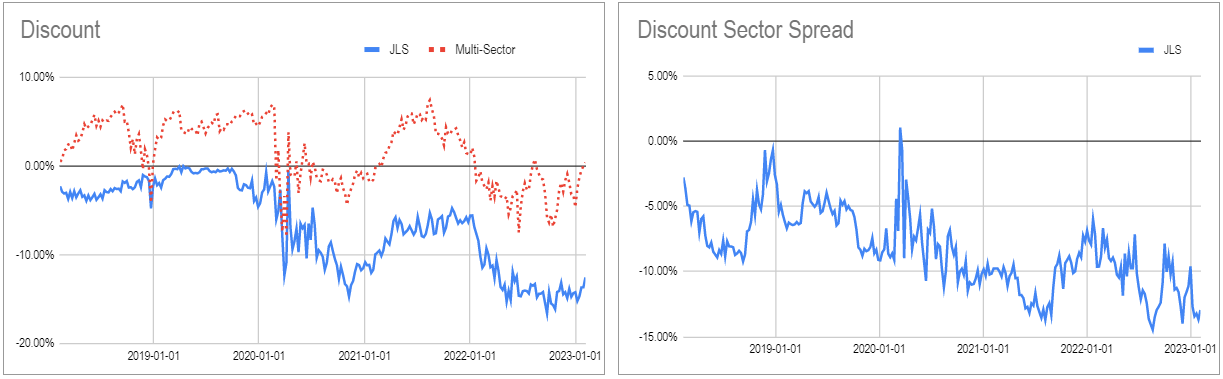

This also explains why the fund's discount remains very wide both on an absolute basis (12.5% vs. 0.5% Multi-sector CEF average - see left-hand chart below) and on a relative basis (12% wider than the sector average - near a historically wide level for the fund - see right-hand chart below).

{kind=link}

However, the recent large distribution hike is likely to make some investors take notice and should push its discount tighter over the medium term, particularly as many leveraged CEFs are busy cutting distributions rather than raising them.

Takeaways

JLS is an attractive fund for today's market environment of high short-term rates, tight credit spreads and resilient households. The recent rally across income assets has left less margin of safety for investors. With JLS allocating to relatively high-quality assets and trading at a double-digit discount, it's an attractive holding at the moment.

For further details see:

JLS: This 8.2%-Yielding CEF Is Well Aligned For The Current Environment