JLS - JLS: This 9%-Yielding CEF Has Hit Its Stride With 2 Recent Distribution Hikes

2023-08-08 12:58:11 ET

Summary

- We take a look at JLS - a CEF that allocates primarily to mortgage and securitized assets.

- JLS has a significant allocation to higher-quality floating-rate assets, which aligns well with today's environment of inverted yield curve and tight credit spreads.

- JLS has outperformed the multi-sector CEF space since 2022 and has made three consecutive distribution hikes.

- JLS trades at a 9.1% yield and a 14.4% discount which provides a nice entry point, particularly in light of the recent distribution hike.

In this article we highlight the Nuveen Mortgage and Income Fund (JLS) which trades at a 14% discount and a 9.1% current yield. JLS allocates primarily to mortgage and securitized assets, with a significant holding of floating-rate assets.

The current environment of an inverted yield curve, relatively tight credit spreads and resilient households favors a position in the fund in our view. Moreover, the fund's outperformance since 2022, a rising level of net income, attractive valuation and three consecutive distribution hikes support our view. We continue to hold JLS in our Defensive Income Portfolio.

Fund Snapshot

JLS allocates primarily to securitized assets such as mortgage-backed and asset-backed securities. These span the gamut of residential and commercial mortgages, credit card, auto, aircraft ABS and others. Although these assets are not your typical assets like bonds and loans, they are very popular assets in the institutional investment space. JLS is also far from the only CEF that allocates to securitized assets - they make up about half the portfolios of PIMCO taxable CEFs.

Nuveen

The fund has a relatively high-quality credit profile, with about 35% allocated to investment-grade securities. 28% of the fund's positions do not carry a rating.

Nuveen

The fund has a modest duration of about 2.0 - about half that of corporate bond funds and about a quarter of leveraged Muni funds. It carries leverage of around 28%.

About half the fund is allocated to floating-rate securities, primarily held via residential mortgage assets.

Macro Investment Picture

It's always important to consider how a given security fits into the broader market and macro picture. In this section we look at the case for considering a fund like JLS which 1) has a significant amount of floating-rate assets, 2) holds relatively high-quality assets, 3) takes exposure to primarily mortgage assets such as residential mortgages while also having additional exposure to household-related assets such as Auto and Credit Card receivables.

The chart below shows the 3-month/5-year Treasury yield curve. The curve is unusually inverted with short-dated yields exceeding their longer-dated counterparts by more than 1%. What this means is that the short-end of the yield curve is unusually attractive from an income standpoint relative to longer-term yields. JLS has half of its portfolio allocated to short-dated yield assets and benefits from this dynamic much more than a typical bond fund.

Systematic Income

Secondly, it can be useful to disaggregate the yield of typical credit assets into a risk-free portion (i.e. the Treasury yield) and the credit spread portion (i.e. the residual yield).

Using high-yield corporate bonds as a proxy, what we see is that credit spreads make up a historically low portion of the total high-yield corporate bond yield. This century it was only lower leading up to the GFC (when credit spreads widened out sharply). What this means is that credit spreads are providing comparatively little compensation to bond investors so it makes sense to also allocate to higher-quality assets or at least avoid very low-quality assets.

Systematic Income CEF Tool

Finally, many income portfolios are already heavily tilted to corporate credit whether through loan or bond funds or BDCs. Having some allocation to funds that allocate to household-related assets such as residential mortgages or securitized assets provides additional portfolio diversification.

Moreover, both residential mortgages and household-related assets remain relatively attractive assets given relatively high equity levels in residential mortgages due to house price appreciation as well as a decent labor market and historically low debt service payments as a percentage of disposable income.

These key factors support a partial allocation to a fund like JLS in our view.

Fund Overview

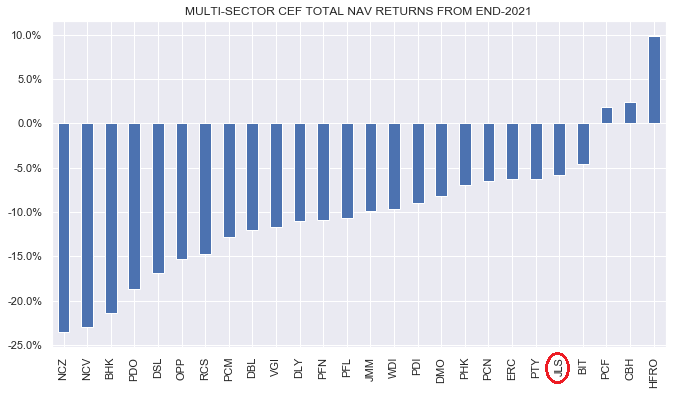

As highlighted above, within the broader Multi-sector credit space JLS has two relatively distinct features - its credit allocation is up-in-quality with a majority investment-grade profile and its duration is quite short at just 2.0. This combination means the fund has been relatively resilient since the end of 2022 as the following chart shows.

{kind=link}

The fund recently hiked its distribution once again - the third consecutive time. It stands at the highest level in over six years.

Systematic Income CEF Tool

The fund has $145m of total assets. With around half in floating-rate exposure that equates to around $73m of floating-rate assets. This is against $41m of repo which is also floating-rate for a net amount of $32m of net floating-rate assets or about a third of its NAV. This explains why the fund's net income has risen alongside the rise of short-term rates over the past year.

If we break down the fund's semi-annual net income figures this is indeed what we find. Over the past two years, net income has risen by 67%. It accelerated in late 2022 because of the lagged effects of a jump in Libor over the middle of 2022.

Systematic Income CEF Tool

Net income should continue to rise over the medium term though not at the same pace as over 2022. Distribution coverage as of the first six months of the year is 91%, however, that's understated given the upward continued momentum in short-term rates. We wouldn't rule out another distribution hike down the line.

The fund's borrowings have remained fairly steady, in contrast to many other funds, most notably PIMCO CEFs, which have shed borrowings. JLS borrowings have been relatively stable for three main reasons: its relatively low NAV beta (which lessens the risk of a forced deleveraging), its relatively low starting leverage (leaving room for leverage to rise in case of NAV drop) and its rising net income (so that maintaining leverage actually makes sense).

Systematic Income CEF Tool

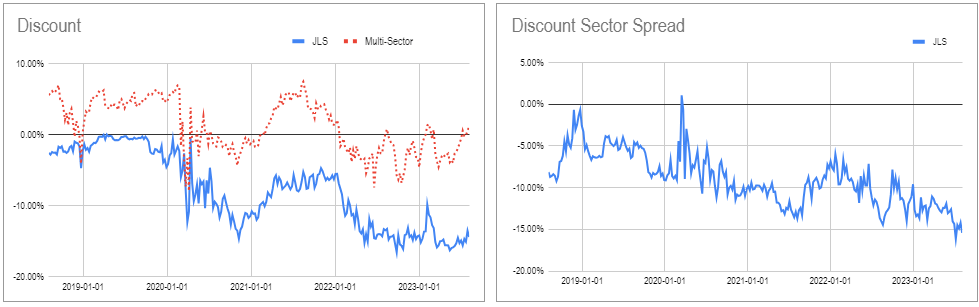

The fund's valuation remains attractive in both absolute terms as well as relative to the other Multi-sector CEFs as the charts below demonstrate. Despite its outperformance and partial yield convergence, its valuation has cheapened even more relative to the sector.

{kind=link}

JLS remains an attractive option for more defensively-positioned investors, whether from a credit risk or duration standpoint. Investors who want to avoid any CMBS exposure or those who believe that the Fed will sharply cut interest rates in the medium term may want to consider other options.

For further details see:

JLS: This 9%-Yielding CEF Has Hit Its Stride With 2 Recent Distribution Hikes