JNK - JNK: The Fed Supports A Bullish Rating

2023-11-03 10:02:47 ET

Summary

- The article evaluates the SPDR Bloomberg Barclays High Yield Bond ETF as an investment option at its current market price.

- I believe owning higher yielding securities is a good idea as bond performance was expected to improve.

- Issuance has been tight for the sector, which I expect to continue. This supports the underlying prices of the securities in JNK.

Main Thesis & Background

The purpose of this article is to evaluate the SPDR Bloomberg Barclays High Yield Bond ETF ( JNK ) as an investment option at its current market price. This is a high-yield bond fund with a primary objective "to provide investment results that, before fees and expenses, correspond generally to the price and yield performance of the Bloomberg Barclays High Yield Very Liquid Index".

While bonds as a whole have not performed very well in 2023, I saw some merit to owning higher yielding securities as the summer got underway. I felt we were nearing peak rates (from the Fed) and that it was time to re-start buying fixed-income exposure. Looking back, I was a bit early with this call , but JNK proved to be an equity hedge nonetheless:

Fund Performance (Seeking Alpha)

Given the four months that have passed since that article, coupled with the recent Fed meeting this past week, I thought it was time to take another glance at JNK. After review, I continue to see reasons why owning this fund makes sense. This is especially true for investors who want high yield exposure, but are reluctant to take on the added risk that comes with leveraged products (JNK is a passive, non-leveraged fund). I will detail the reasons behind my continued bullishness in detail below.

The Market Loved What The Fed Had To Say

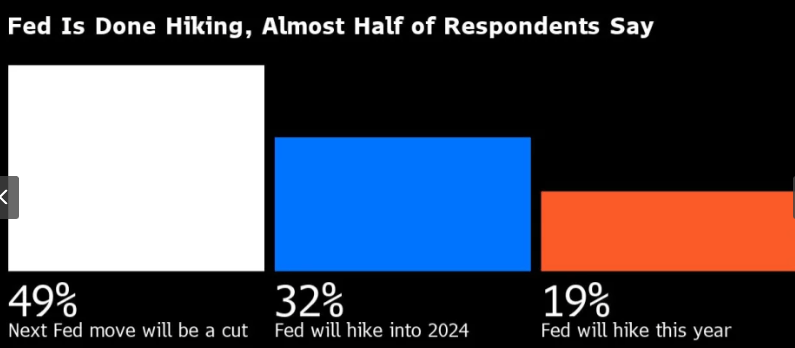

The biggest takeaway from the past week was the Fed's meeting and subsequent statement. Simply, it was a bit dovish compared to what we have heard over the past 18 months. This helped spark a rally in both bonds and equities as investors began to price in a "peak" rate environment. In fact, within a day of this latest statement release investors are now evenly split on whether another rate hike will even be in the cards this cycle:

Investor Expectations (Yahoo (Pulse Survey))

{kind=link}

This was positive for stocks, which had been falling recently, but especially for bonds as bond prices move inversely with yields. If Fed rates - and broader yields - decline, then underlying bond prices should rise. This concept certainly extended to JNK this week, which saw a marked jump immediately after Chairman Powell's remarks:

JNK Price Action (Google Finance)

{kind=link}

Clearly the last couple sessions have been supportive of JNK. But what is more important is where the fund may be going from here. This requires examination of the Fed's statements specific to what actually got investors excited to prompt these upward moves.

Ultimately, the Fed left its benchmark rate unchanged and left the door open for further hikes. But Chairman Powell pleasantly surprised some investors by also suggesting the end of hikes may be a realistic possibility too. This was in stark contrast to prior meeting when it seemed clear the Fed was not "done" for this cycle. This week, the tone shifted:

The question we’re asking is: Should we hike more? Slowing down is giving us, I think, a better sense of how much more we need to do, if we need to do more”

Source: Fed Press Conference (via Youtube )

The market has taken this as a sign that we are either at - or very close to - peak rates and now is the time to get back into both stocks and bonds. That is good news for investors, including those who own JNK. Personally, I think borrowing rates are indeed high enough to stifle some demand (just look at housing numbers and mortgage originations) and the Fed can hold rates where they are and still stifle growth and inflation in-line with their objectives. If I am right, then now is indeed a reasonable time to start building or adding to fixed-income positions - JNK included.

Issuance Has Been Tight, Supporting Prices

Another positive JNK has going for it is that higher yielding bonds are in shorter supply than they have been in past years. This is important because JNK is made up almost exclusively of below IG-rated debt, as shown below:

JNK's Holdings Breakdown (By Rating) (State Street)

Of course, a lot goes in to setting market prices for bonds. Chief among them is interest rates, which we just discussed in the prior paragraph. The other is investor demand - which is fundamentally impacted by rates and investor's outlooks for economic growth. A third is supply. Lack of supply, or too much supply, will send prices up or down, all other things being equal.

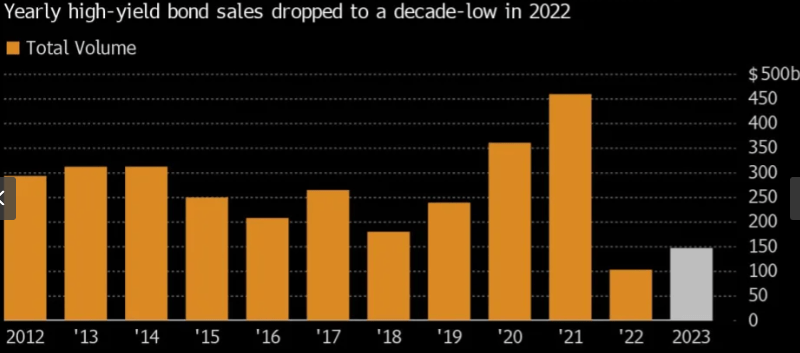

Why is this relevant now? Because supply has been fairly muted in 2023, coming off a weak year of issuance in 2022 as well:

Bond Sale Volume (By Year, Non-IG rated) (Bloomberg)

{kind=link}

This isn't necessarily "good" news is below-IG rated companies are not as liquid as they could be. But it is good in the sense that it keeps the amount of available bonds for share on the open market low. This can drive up prices if demand is stable (or growing). While demand for bonds has been generally weak year-to-date, the sudden uptick in interest for risk-on assets this past week could change things for the rest of Q4. If so, the low levels of issuance in the junk bond market will help support prices going forward. This is a strong sign for funds like JNK that own these bonds.

High Yield Is Offering Attractive Income

Another reason to consider the high yield bond sector at the moment has to do with the income stream. The reality is that as rates have risen and bonds have gotten punished, this has repeatedly made new positions more and more attractive. At this juncture, it is difficult to ignore yields in excess of 9% for the sector. This is near the top end of the range over the past two years and well above the average for that time period:

Current Yield (Junk rated) (Bloomberg)

{kind=link}

JNK, as a passive ETF tracking this sector, similarly is offering a current yield in this range as a result:

JNK's SEC Yield (State Street)

Now, this is not a sure thing by any means. A 9% yield is certainly not a ceiling. It doesn't represent the end of a cycle and automatic gains. While it is an attractive income stream historically, we don't have to look much further than the past ten months to know that high yields can go higher. If they do, then bond prices will keep falling and investors in JNK could see a negative total return. This is definitely a risk - and one that readers should evaluate carefully.

But I see the Fed's recent inaction and the understanding that a 9% yield is not the norm for JNK as reasons to buy. Is there risk? Of course. But I think it is a risk that is worth taking.

Defaults Ticking Up, But Rate Is Manageable

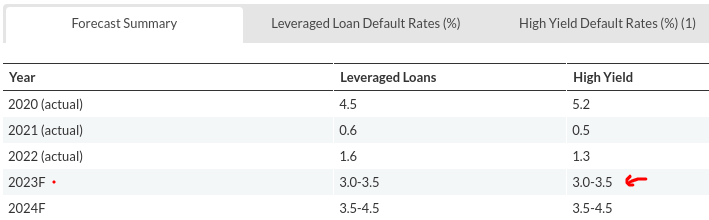

I talked about there being risks, so let's examine what some of those risks are. Chief among them is default risk. Unlike IG-rated corporates, munis, or treasuries, the chance of a high yield bond defaulting is not unfathomable. This risk is always present and high yield bonds do default every year. Defaults spiked in 2020, only to come down dramatically in the years that followed as cheap money became the norm. Now, with rates rising and the economic picture challenging - both here and abroad - the default rate for 2023 is likely to finish in the 3 - 3.5% range:

{kind=link}

Seeing defaults go up is never a good thing. I am not suggesting that in any way. But we have to take this metric in stride. JNK is offering a 9% distribution rate and has already baked in an uptick in defaults based on its performance this year. The takeaway for me is that a 3% default rate is not a calamity, and the fund can absorb that and still offer investors a positive return if other factors (such as limited supply) continue. This is central to why I am not letting the uptick in defaults deter me from this sector. It is something high yield investors always have to contend with and I believe the risk-reward proposition is attractive enough with all factors considered.

Bottom-line

JNK has squeezed out a minuscule gain in the last four months, but I see brighter days ahead. It remains a reasonable equity hedge, it will continue to see a short-term boost from a more dovish Fed, and the American economy's resilience is rewarding risk-on plays for now. Due to this, I believe a "buy" rating on JNK continues to be justified and I suggest that readers give this idea some thought going forward.

For further details see:

JNK: The Fed Supports A Bullish Rating