JNK - JNK: Time To Dump Your Junk

2023-06-14 22:33:52 ET

Summary

- SPDR Bloomberg High Yield Bond ETF offers exposure to non-investment grade corporate bonds.

- The junk bond spread over treasury bonds is currently too low to justify the risk.

- I rate JNK a Sell, as the coming recession will likely cause more defaults.

SPDR Bloomberg High Yield Bond ETF ( JNK ) tracks the Bloomberg High Yield Very Liquid Index . JNK holds corporate junk bonds, also known as non-investment grade bonds and high-yield bonds. With AUM of about $8.5B, JNK has a current 30-day SEC yield of about 8.3% . Because of the coming recession, I don't think now is the time to take a risk on junk bonds, especially considering the low-risk-return trade-off. I rate JNK a Sell.

Holdings

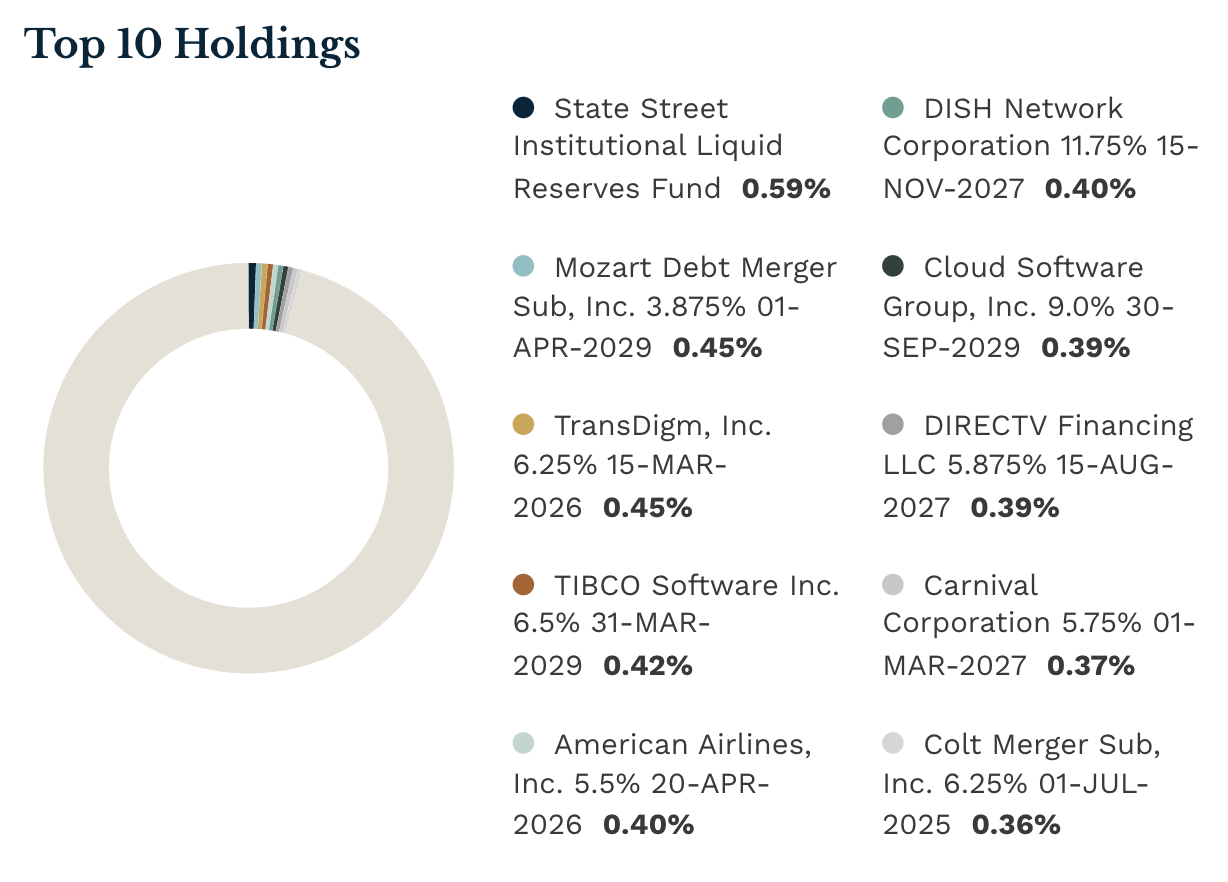

JNK holds 1151 non-investment grade, fixed-rate, taxable bonds that have a maturity between 1-15 years. JNK's top 10 holdings make up only about 4% of the fund, making this ETF very diverse.

JNK's top 10 holdings (ETF.com)

{kind=link}

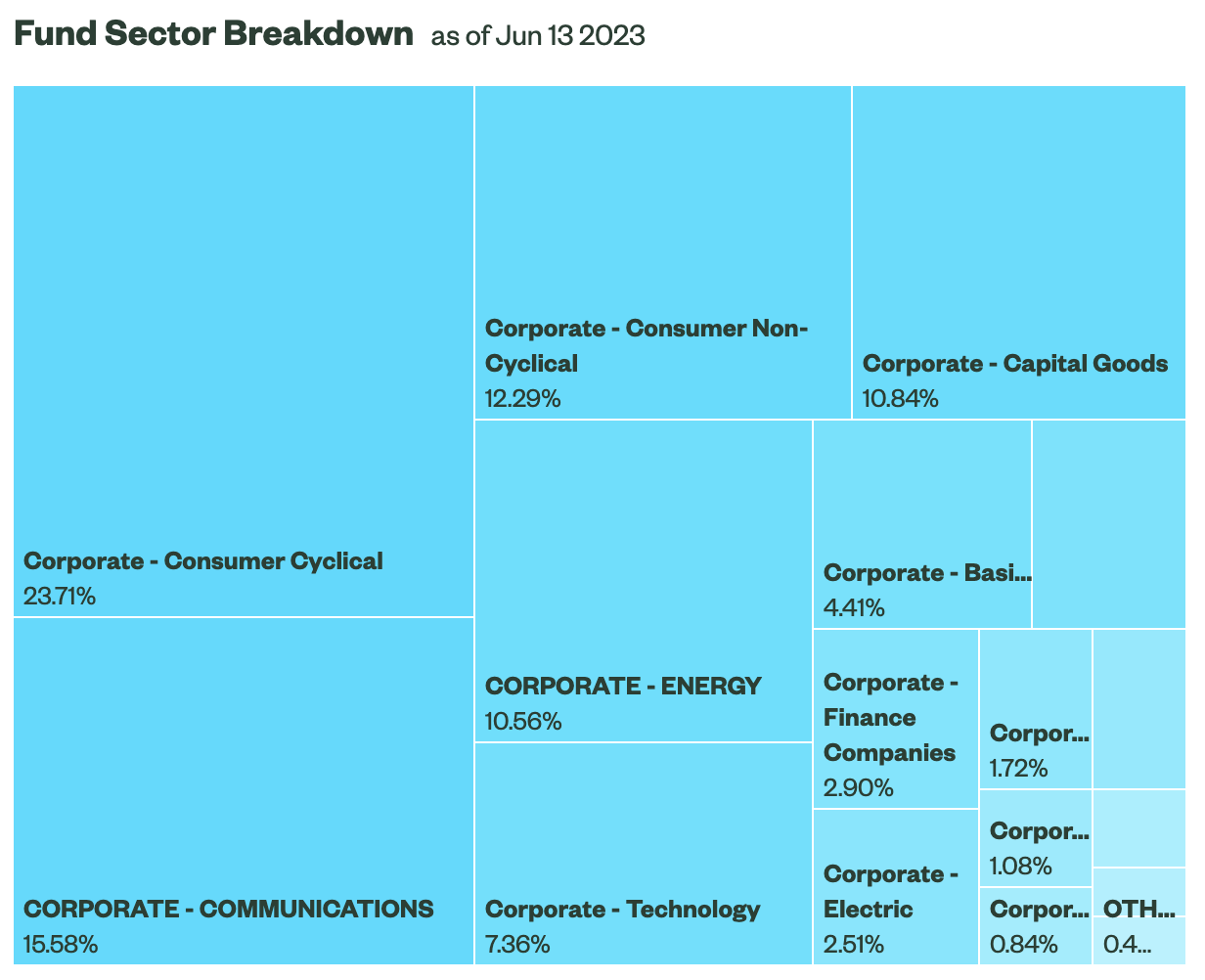

JNK also holds bonds issued by a variety of different sectors, with Consumer Cyclical being the largest category within the fund.

JNK's holdings by sector (ssga.com)

{kind=link}

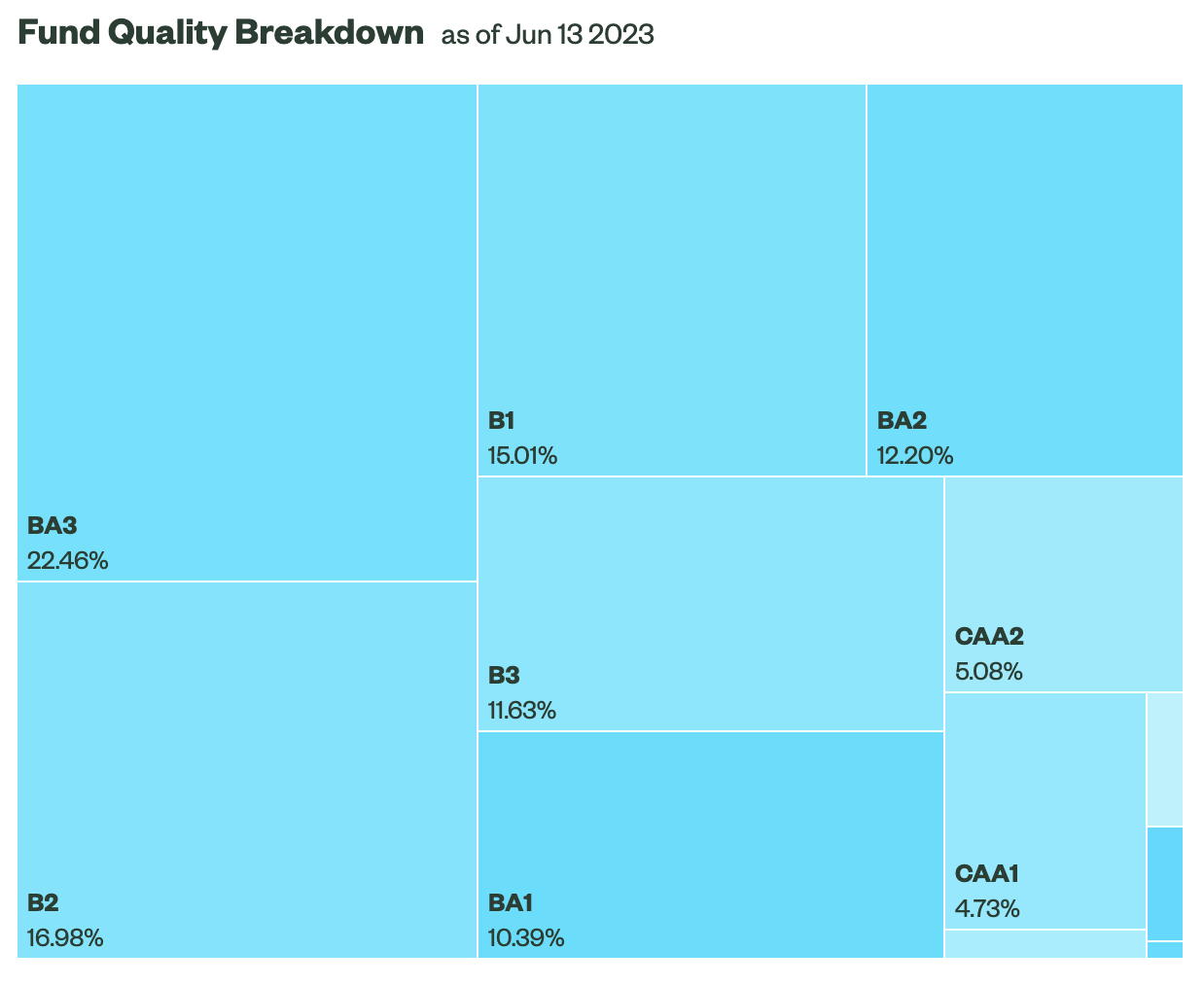

What makes JNK special compared to other corporate bond ETFs is its holding of non-investment grade bonds. Because JNK holds junk bonds ( Ba1/BB+ and below ) there is more risk but also higher yields than investment-grade corporate bonds.

JNK's holding by bond quality (ETF.com)

{kind=link}

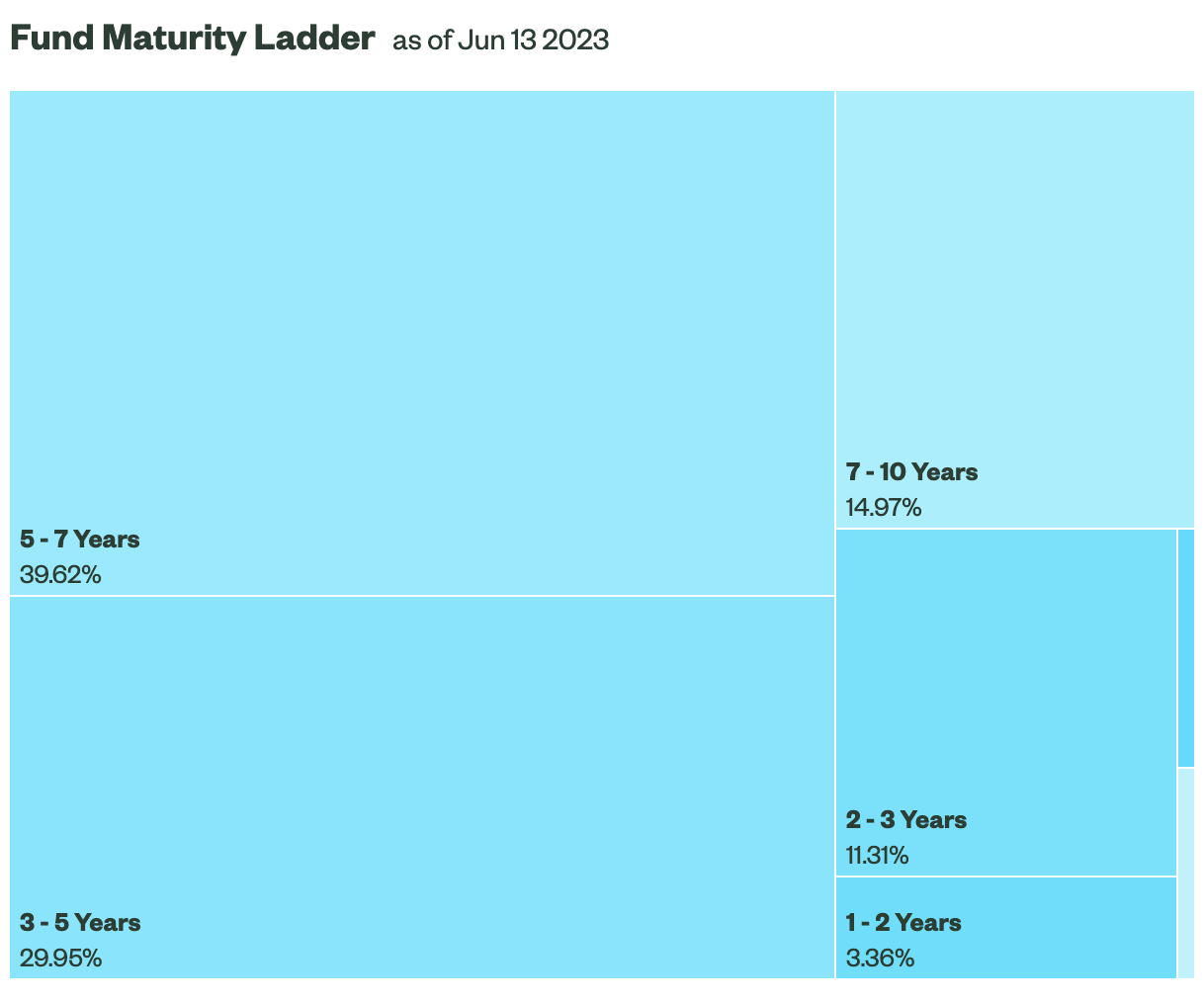

Finally, JNK offers non-investment grade bonds with a wide range of maturities. About 70% of these bonds have maturities between 3 and 7 years.

JNK's holdings by maturity length (ssga.com)

{kind=link}

The coming recession

After the announcement by Fed Chairman Powell that there will likely be another 2 rate hikes this year, I think a recession is extremely likely. The economy has shown some signs of slowing, but that's obviously not enough for the Fed. The day before Powell announced a June pause in rate hikes and to expect 2 more hikes , Bloomberg had an article saying that because the last inflation report showed signs of a slowing economy, there will be no more rate hikes in 2023. I think this is a great testament to the fact that the Fed isn't taking any chances with inflation. Although we had good CPI news, the Fed is still making sure it will be brought under control, with the likely result being that the economy is pushed into a recession.

Junk bonds during recessions

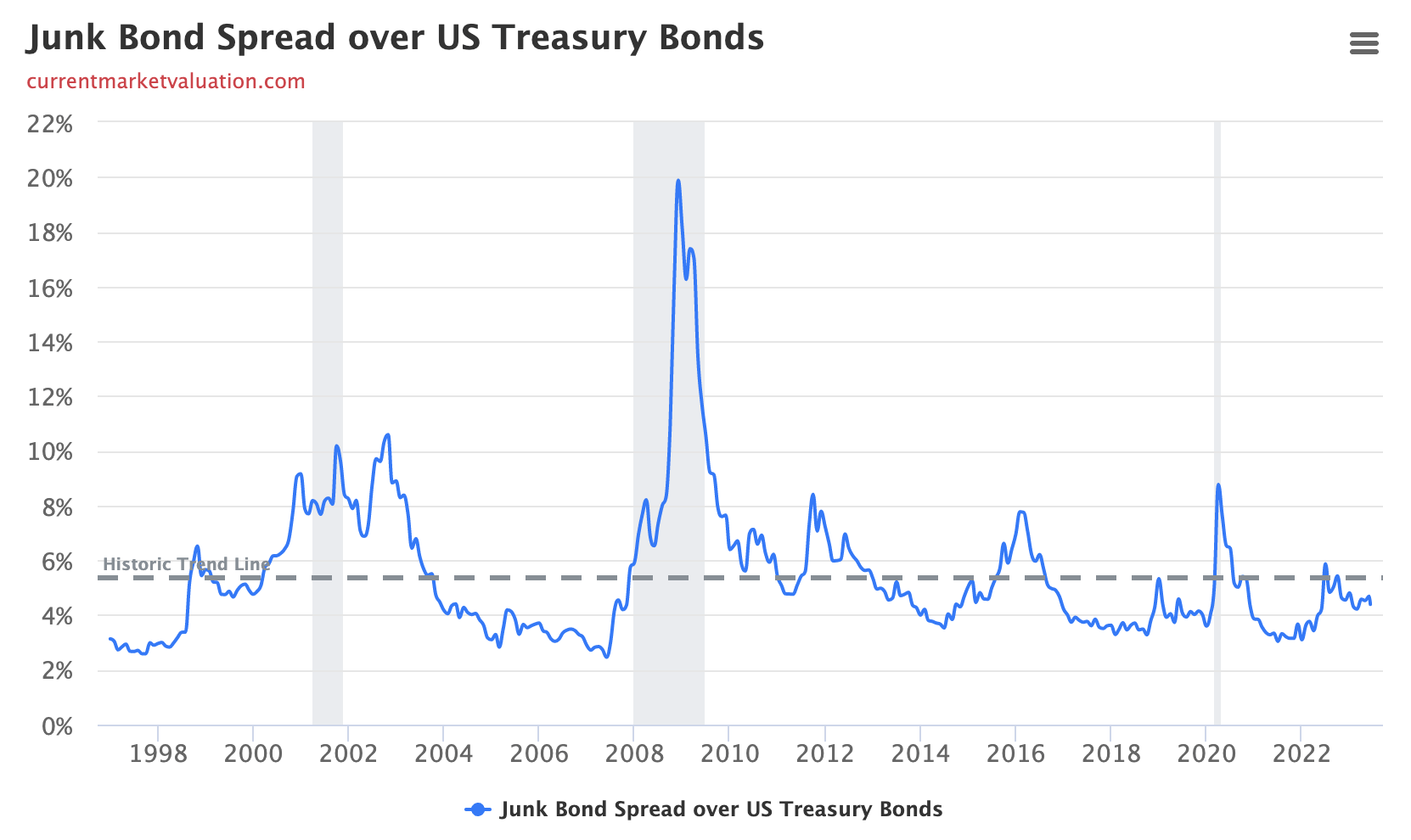

During a recession, it's no surprise that the number of bond defaults increases . Although investment-grade bonds also have increased defaults during a recession, junk bonds are especially at risk, considering that they have low credit ratings. Treasury bonds are usually considered the safest and junk bonds the most dangerous. With this being said, the spread between junk bonds and treasury bonds should be large enough to account for the added risk. The chart below shows the junk bond spread over treasury bonds, with a historic trend line of a little over 5%.

Treasury bond and corporate junk bond spread (currentmarketvaluation.com)

{kind=link}

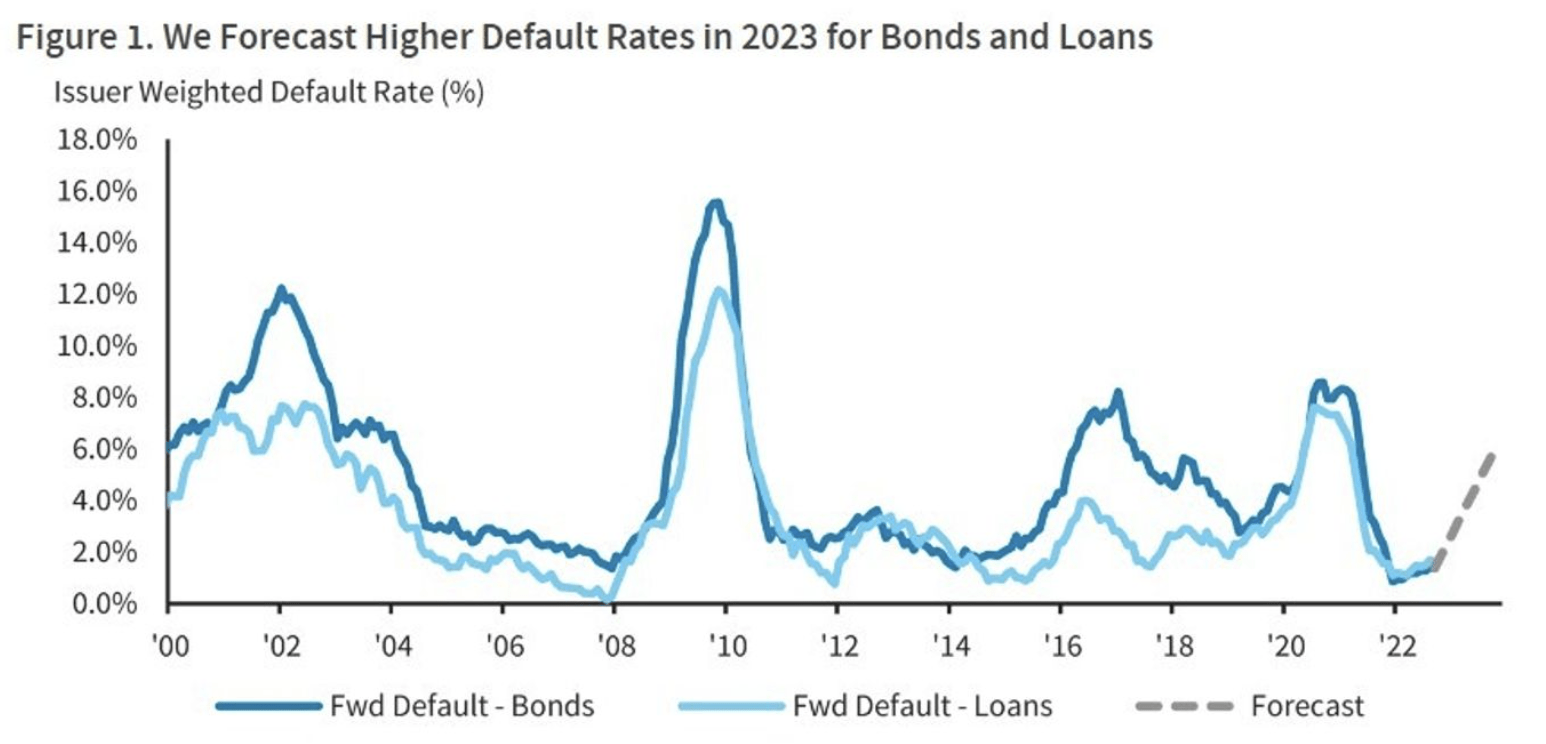

With the added risk of a coming recession, I see no reason for the current spread to be below the trend line. The spread is suggesting that we are in normal economic times. Until this spread increases, the risk-reward trade-off is not worth it, especially when you consider default forecasts of junk bonds. The chart below shows junk bond default rates since 2000 and Barclays credit analysts forecast for junk bond defaults for 2023.

Junk bond default forecast (marketwatch.com)

{kind=link}

The forecast shows defaults shooting up to about 6%. If this is the case and the risk for junk bonds is increasing, there is no reason to take on the added risk when the junk bond spread over treasury bonds is still below the historic average.

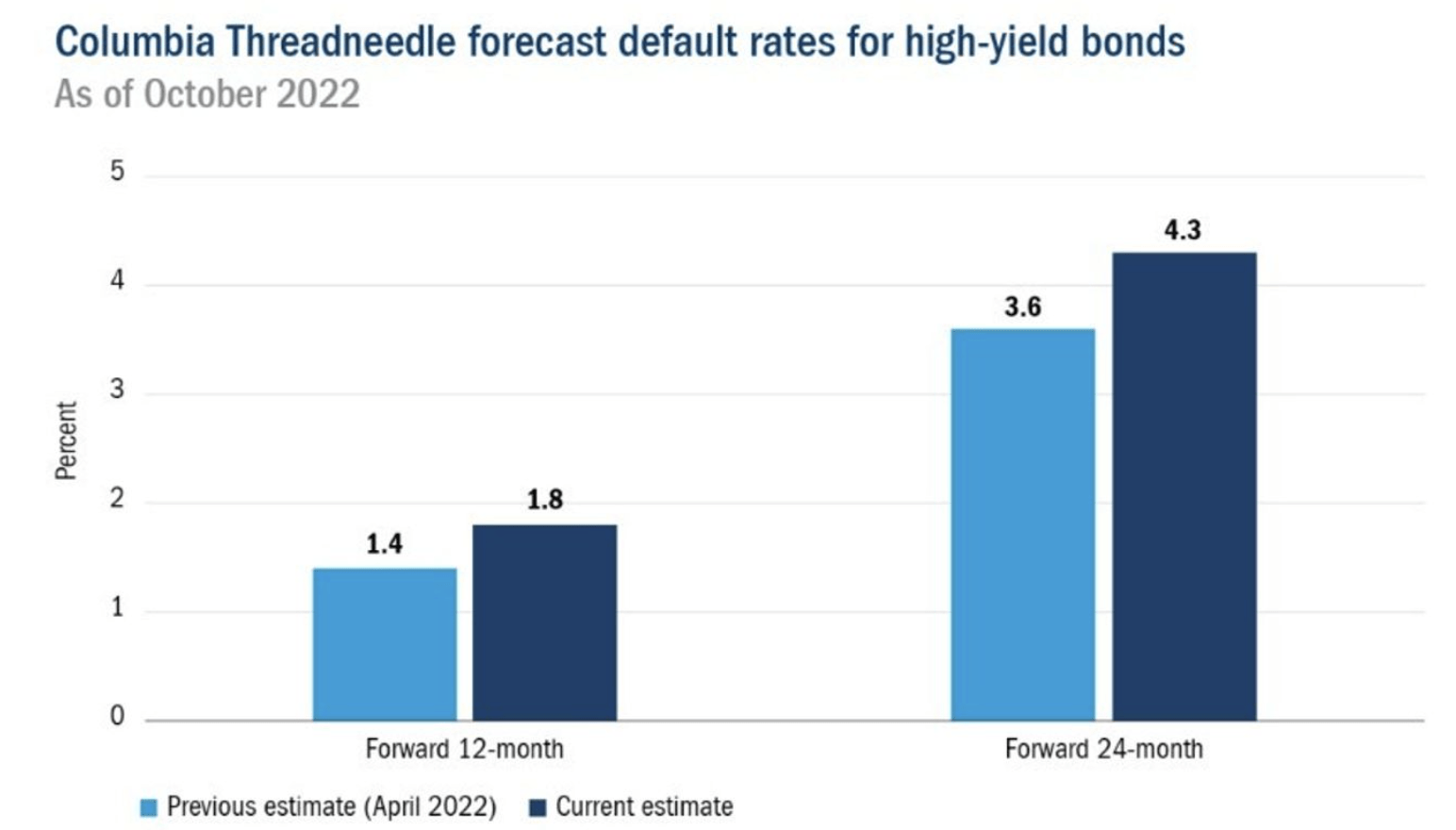

As more economic data comes in regarding inflation and interest rate hikes, junk bond default rate forecasts continue to rise. Both the 12-month and 24-month predictions have increased, and the coming additional rate hikes will likely increase those forecasted default rates even more.

Forecast default rates for junk bonds (marketwatch.com)

{kind=link}

Why investment grade is better right now

With a coming recession, I don't think taking on all the default risk that JNK has is worth it, especially while it has a lower-than-average spread compared to treasuries. In every recession since 1950, investment-grade bonds have outperformed stocks and cash . This is because after the economy goes into a recession, interest rates begin to fall, causing investment-grade bonds to go up in price. This doesn't happen to junk bonds to the same effect. Two things play into bond rates; default risk and interest rates. Because investment-grade corporate bonds have lower default risk, they are more dependent on interest rates, and because junk bonds have high default risk, they are more dependent on economic conditions. Junk bonds don't get the same level of capital appreciation as investment-grade corporate bonds when rates fall in a bad economy, because of the impact of default risk.

Conclusion

JNK tracks high-yield junk bonds. The bonds JNK offers give a higher yield but also have a much higher risk of default. This default risk is elevated even more during a recession, which I think is on the way. Not only will JNK suffer from defaults during a recession, but it also doesn't offer the same benefits as investment-grade corporate bonds as rates are cut. Because of this, I rate JNK a Sell.

For further details see:

JNK: Time To Dump Your Junk