JNK - JNK: Too Much Risk For Too Little Yield

2023-12-11 23:14:12 ET

Summary

- Investors poured a record amount of money into high-yield bond ETFs in November, but I remain bearish on the junk bond market.

- A looming maturity wall and expected rise in defaults create a negative environment for junk bond ETFs.

- The artificially high prices of junk bonds and low yield spread over treasuries do not justify the risks associated with investing in junk bonds.

The bond market had an exciting November. November 2023 was the best month for bonds since 1985. The Fed funds rate is likely at its peak and investors are expecting over a percent of rate cuts in 2024. I expect broad market bond index ETFs like BND and AGG to have a very successful 2024. But there is one section of the bond market I am extremely bearish on.

Investors dumped a record amount of money into high-yield (also known as junk or speculative grade) bond ETFs in November. A whopping $11.9B was added to junk bond ETF's AUM. In the past, I've covered a couple of junk bond index ETFs. I gave both JNK and HYG a Sell. If you're interested in reading my past coverage, you can find the articles here and here . Investors buying up junk bonds made me want to come back and re-evaluate the current junk bond market. While the market has poured unprecedented optimism into the junk bond market, I remain unconvinced that this is a wise investment. I'll be using SPDR Bloomberg High Yield Bond ETF ( JNK ) as my reference to evaluate the market, but the information in this article will be relevant to most junk bond ETFs.

Past JNK coverage

I covered JNK about 6 months ago. Since I gave it a Sell, JNK has returned 4.6%.

At one point in mid-October, JNK was down 2% and since then it has had a rally of over 6.5%! I gave JNK a sell because I expected an economic slowdown due to high rates causing a rise in defaults.

While in the short-term my Sell thesis hasn't played out, I still believe it will in the long term. Before we get into my reasoning, let's take a look at JNK's holdings.

Holdings

JNK tracks the Bloomberg High Yield Very Liquid Index. Because JNK holds high-risk bonds, the yield is higher than investment-grade bond ETFs. JNK's 30-day SEC yield is 7.95%.

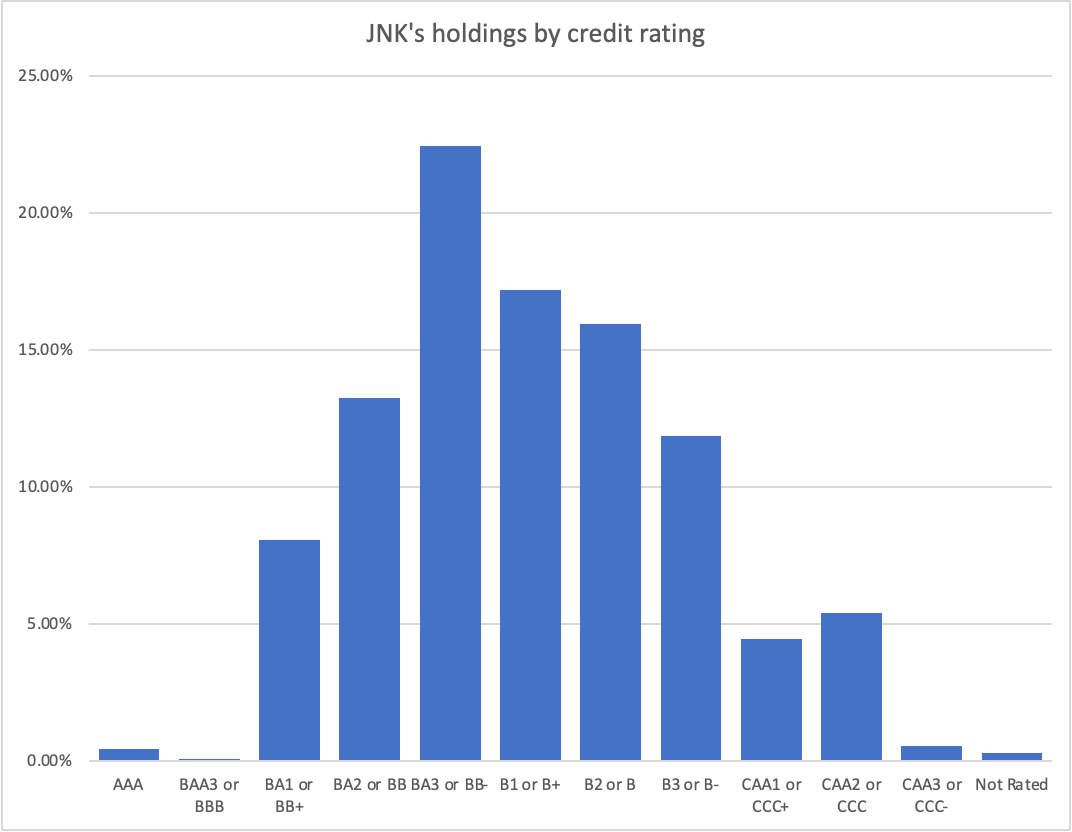

JNK holds almost entirely BA1 (BB+) or lower-rated bonds. Its largest holding is BA3 (BB-) bonds. Almost 56% of this ETF is in bonds rated B+ or below, making this ETF high risk.

{kind=link}

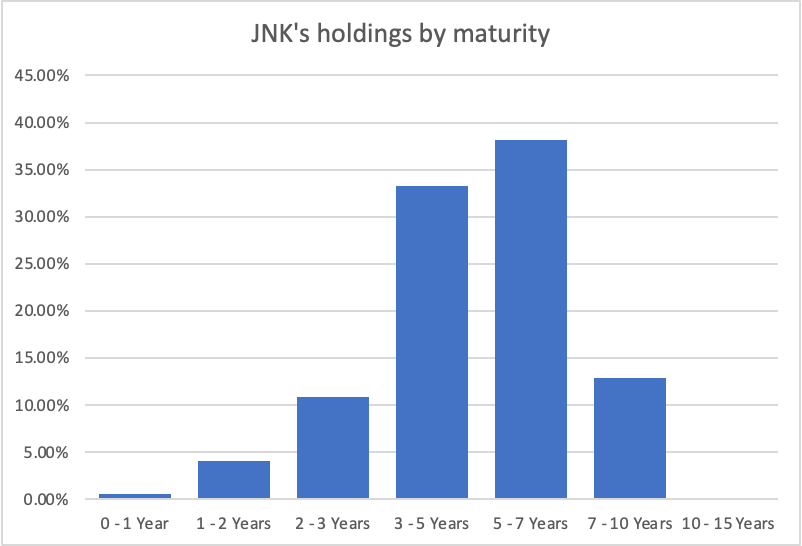

JNK's average maturity is 4.94 years. This is pretty short-term for a bond index ETF. 49% of this JNK's AUM is in junk bonds with a maturity of less than 5 years.

{kind=link}

You may be thinking that shorter-term bonds carry less risk so this is a good thing. Well, let's take a look at that.

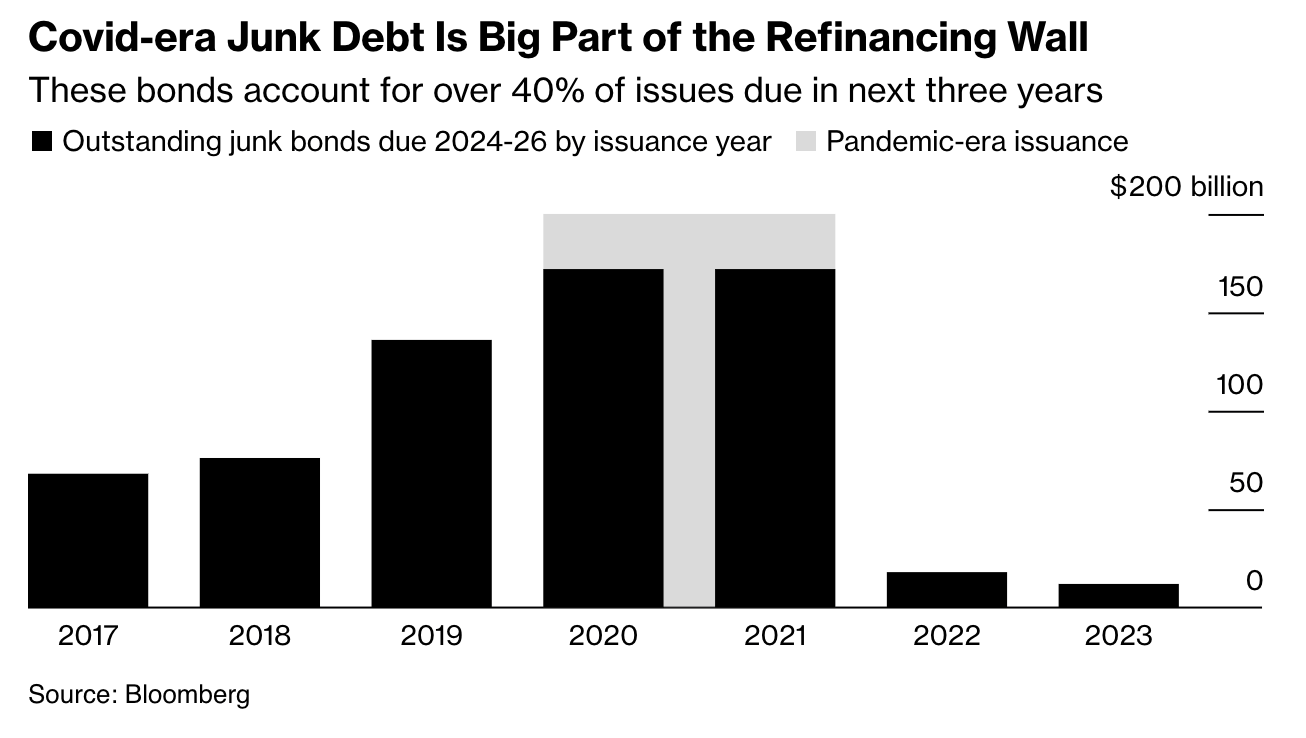

Looming Maturity wall

There is a $785 billion junk-bond maturity wall approaching. Because only about half of JNK is in shorter-term junk bonds, I'll give a quick analysis of the maturity wall, but if you want a more in-depth look, I go into more detail here . During the era of cheap borrowing, we had massive amounts of junk debt being issued, particularly during the COVID-19 pandemic. The image below shows the amount of outstanding junk bonds due between 2024 and 2026.

Covid-era junk debt issuance (Bloomberg)

{kind=link}

So why is this a big deal? In the past, this wouldn't have been a big issue. Companies would just issue new debt to pay off the old. But interest rates are no longer extremely low. This has already caused some economic slowdown and can hurt these junk-rated companies. But it also means that they will have to refinance at a much higher rate, putting the company under even more strain because it has to pay even more interest on the newer debt, potentially leading to more defaults.

The Fed funds rate is expected to be cut by 1.15% in 2024, but bond rates will still be much higher than these companies were used to paying over the past decade. The only way junk-rated companies could refinance at a rate close to COVID-era rates would be a severe recession. This would prompt the Fed to cut rates to stimulate the economy. However, a recession would severely hurt the junk-rated companies and would cause their default rates to shoot up. So there are 2 likely scenarios; rates fall slightly and junk-rated companies are forced to refinance at a higher interest rate that may not be sustainable, or rates are heavily cut because of a recession, and junk companies are unable to pay back debt even at a lower interest rate.

With only about 50% of JNK in shorter-term bonds, this issue is more relevant for short-term junk bond ETFs like SJNK and SHYG , but it is still a major concern for JNK investors.

Yield

The reason investors are willing to take the added risk of junk bonds is because they get more in yield. One of the ways many investors gauge how good junk bond yields are is by looking at the spread between junk bond yields and treasury yields. Right now, the spread is approximately 3.8%. Since 1979, the average spread has been 5.4%. This would seem to suggest that the market considers junk bonds to be relatively safe right now, but this isn't the case.

Artificially high junk bond prices

Junk bond prices are artificially high for multiple reasons. One of the reasons is that investors now realize the very short-lived era of 5% on 10-year treasuries is over. Investors are getting 'FOMO' and looking for other high-yielding assets to buy. I am worried that at the first sign of economic slowdown due to higher interest rates, investors will dump their high-yield bonds because they realize they took on too much risk.

Another reason for the artificially high prices of junk bonds is that there has been an extreme decline in junk bond issuance. As supply shrinks, prices rise. Companies don't want to issue unnecessary debt because interest rates are so high. This especially affects the lower-rated companies. Because these companies' bonds are riskier, they have to raise the yield to become attractive. For very low-rated issuers like CCC and below, this is even more of a concern. They are having trouble finding investors willing to take on the risk of their debt. To overcome this, they go to private lenders, further shrinking the supply of tradable junk bonds and further propping up their prices.

JNK has to continue to buy junk bonds to accurately reflect the market index regardless of the shrinking supply. This leads to them being forced to buy overpriced bonds that they otherwise wouldn't have. As I said before, if investors realize these bonds are overpriced and are paying a historically low yield compared to treasuries, the floor could fall out and these artificially high prices will return to being fairly priced.

Defaults

On top of the looming maturity wall, a historically low yield compared to very safe bonds, and the shrinking junk bond supply, defaults are expected to rise in 2024. Junk bond defaults are currently at about 3%. S&P Global expects them to rise to 4.5% in 2024 and says that in the case of a recession, it's likely to increase to 6.5%. Moody expects default rates to peak at 5.6% in 2024.

Putting everything together

A looming maturity wall, a low yield spread over treasuries, a shrinking junk bond supply, and an expected rise in defaults do not provide a positive environment for junk bond ETFs. It all comes down to this. There is a massive amount of risk the junk bond market is facing and the market isn't currently willing to pay enough for me to be willing to undertake it. When investing in a market like junk bonds, there are always going to be many risks. The market prices in these risks. That's why junk bond yields are higher than treasuries. But for all the risks the junk bond market is facing right now, it's only paying about 3.8% more than treasuries. That is not enough. Ultra-low-risk assets like SGOV are paying 5.3%. That's only 2.65% less than junk bonds. The only risk SGOV has is reinvestment risk. JNK's yield is just not enough to justify the risks associated with it.

Takeaways

JNK is a very risky ETF right now. The junk market is artificially overpriced and facing a huge maturity wall. Despite all this added risk, the spread between junk bonds and treasuries is far below the historic average. If rates stay high, junk bond issues are going to have trouble refinancing. The only likely reason for rates to fall drastically would be a recession which would seriously hurt these already struggling junk bond issuers. I rate JNK a Strong Sell.

For further details see:

JNK: Too Much Risk For Too Little Yield