DOLE - John B. Sanfilippo & Son Hasn't Fallen Enough To Warrant Another Crack At Things

2023-12-06 10:45:41 ET

Summary

- John B. Sanfilippo & Son, a nut processor and distributor, has seen a decline in stock performance and revenue.

- Sales volume has dropped across various product lines, including branded and private brand products.

- Despite the decline in sales, the company's bottom line figures remain strong, but the future is uncertain, warranting a 'hold' rating.

I have always found myself drawn to companies that have weird or, dare I say, ‘nutty’ business models. And what could be nuttier than a firm like John B. Sanfilippo & Son ( JBSS ) that operates as a processor and distributor of peanuts, pecans, cashews, walnuts, almonds, and other related products? Up until earlier this year, I was right about the potential that the company had. From the time I wrote about the company in July of 2022 until I downgraded it from a ‘buy’ to a ‘hold’ in July of this year, shares had seen upside of 59.3% at a time when the S&P 500 increased a more modest 16.8%.

Since the publication of my last article , however, the stock has underperformed my expectations. A ‘hold’ rating from me is an indication that the stock should perform more or less in line with what the broader market should experience. But since that article was published, shares have dropped 14.5% at a time when the S&P 500 is down only 0.1%. This returned disparity is not because shares were expensive. They looked more or less fairly valued when I downgraded them. Rather, it's likely because of weakness on the top line. Revenue has pulled back slightly as of late, though it's worth noting that bottom line results are actually coming in stronger than they did one year earlier. Normally, this would make me want to buy the stock or at least upgrade it since it seems as though the market is overreacting. But shares are not quite cheap enough for me to upgrade the stock once again.

A nutty time

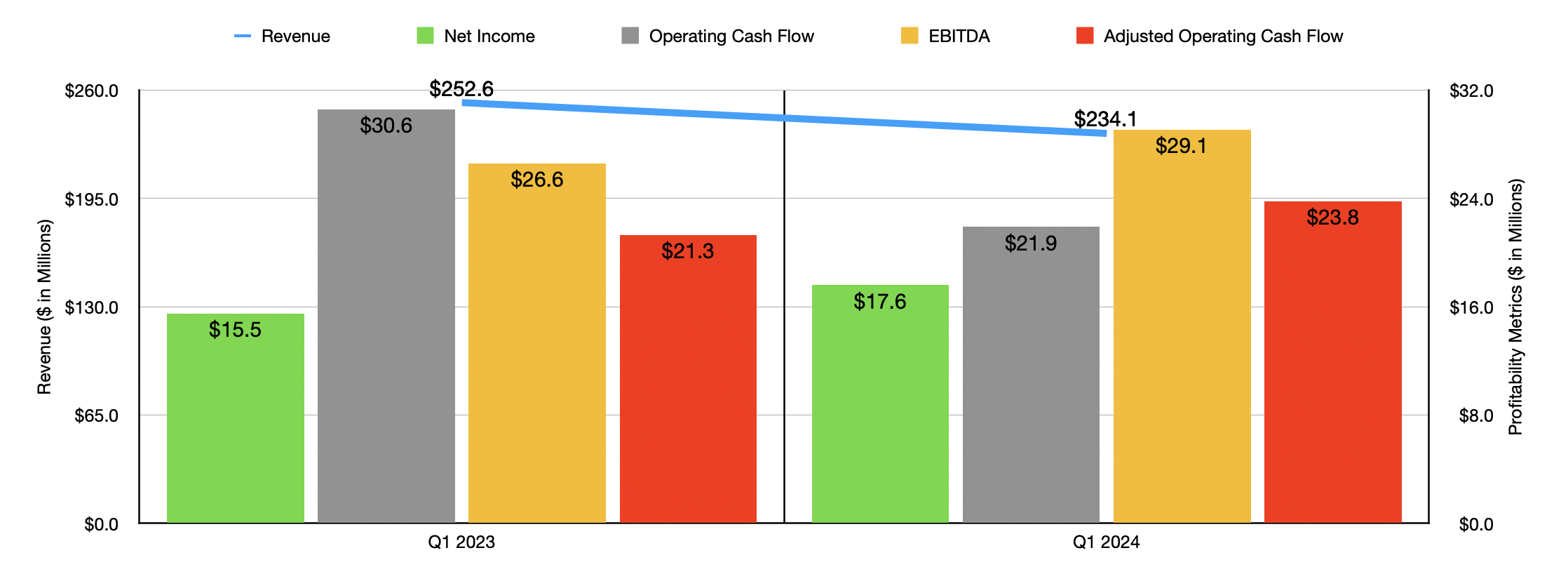

From a sales perspective, things have not been going particularly well for John B. Sanfilippo & Son. As an example, we need only look at data covering the most recent quarter. That would be the first quarter of the 2024 fiscal year. During that time, revenue for the business came in at $234.1 million. That's 7.3% below the $252.6 million generated one year earlier. Management attributed basically all of this decline to a 7.3% drop in sales volume. And honestly, that sales volume declined came from across the board.

{kind=link}

Under the Consumer Distribution Channel of the company, for instance, Private Brand Products reported a 5% drop in sales volume because of a reduction in promotional programs and lower seasonal sales volume for snacks and trail mixes at two mass merchandising retailers. Lower peanut sales volume at those same two retailers also helped to push demand lower. But that was nothing compared to the 17% drop seen across the company’s Branded line of products. The biggest pain there involved a 30.9% decline in sales volume associated with Fisher snack nuts that management attributed to more competitive pricing pressures from other players in the market, the discontinuance of a product line at a single mass merchandising retailer, and a change in the timing of holiday sales orders for a customer that operates outside of the food sector. Sales volume for another brand, known as Southern Style Nuts, dropped 36.6% year over year because of a reduction in distribution and promotional programs at one of the company’s club store customers.

Outside of the Consumer Distribution Channel, the company also experienced weakness. For instance, the Commercial Ingredients Distribution Channel reported a 5.5% decline in sales volume thanks to a 50.3% drop in sales volume of peanut crushing stock to peanut oil processors that management ultimately attributed to lower peanut shelling. The Contract Packaging Distribution Channel, meanwhile, reported a 19.4% decline in sales volume thanks largely to a reduction in peanut distribution and the timing of holiday sales orders for one of the company's largest customers.

To be honest with you, I find it surprising that nut sales would be down like this. So I did some additional digging outside of what management reported. According to the National Peanut Board (yes, I’m every bit as surprised as you are that such an organization exists), or NPB as it calls itself, cited a report by J. M. Smucker ( SJM ) that found that the pandemic accelerated the growth of peanut sales by 7.1% for the 12 months ending on November 1st of 2020. The NPB saw a 55% increase in peanut butter recipe mentions on social media during the pandemic. In 2020 alone, peanut butter retail sales were up 8.8% year over year. The peanut was not the only nut (I know it’s technically a legume) to report strong demand in the nut space during the pandemic. In fact, the snack nut category as a whole reported a 7.2% rise in demand in the course of a single year during the pandemic.

With the pandemic basically over, I wouldn't find it surprising to see a reduction in snack food consumption and a drop, in turn, in nut consumption as a whole. In fact, according to Southern Ag Today, peanut production dropped in 2022, with the number of acres of peanuts planted down 8% and yields dropping 2.7%. Even outside of that, there have been some issues. For instance, Texas, which has been hit by droughts, reported a 21.6% drop in the yield per acre and the drought led to roughly 25 per cent of planted acreage within Texas going unharvested. That all caused a 12% decline in peanut tonnage year over year. This all coincided with a 4% drop in peanut demand here at home, that was driven largely by a 7% forecasted decline in exports.

You would expect a drop in sales to bring with it a decline in profits. But that is not what we saw. Net income actually inched up from $15.5 million to $17.6 million. Improved manufacturing efficiencies, a reduction in volumes shipped, and lower acquisition costs for major tree nuts, all were responsible for attractive margin expansion. Other profitability metrics followed suit. While operating cash flow dropped from $30.6 million to $21.9 million, the adjusted figure for it grew from $21.3 million to $23.8 million. Over the same window of time, EBITDA for the company expanded from $26.6 million to $29.1 million.

{kind=link}

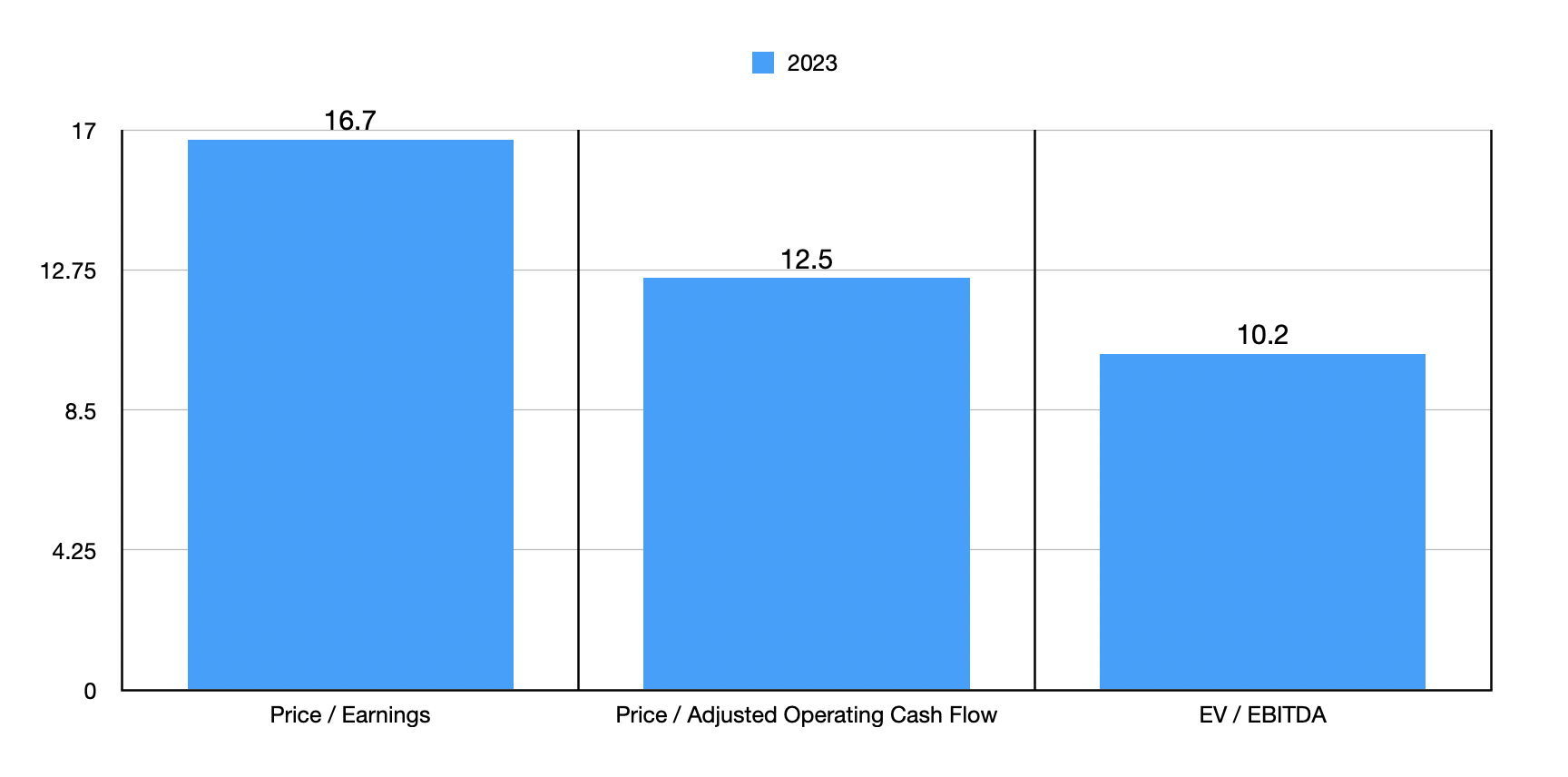

Given this performance, it would be tempting to value the company based on forward estimates for 2024. But it would be more prudent to use the recently announced (as in earlier this year) 2023 figures. Using the data from that year, I was able to create the chart above. In it, you can see how shares are priced. I then, in the table below, compared with the company to five similar firms. On a price to earnings basis, only one of the five companies was cheaper than John B. Sanfilippo & Son. Using the price to operating cash flow approach, this number increases to three before dropping to two if we use the EV to EBITDA approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| John B. Sanfilippo & Son |

| 16.7 |

| 12.5 |

| 10.2 |

| TreeHouse Foods ( THS ) |

| 104.0 |

| 17.6 |

| 11.3 |

| Mission Produce ( AVO ) |

| N/A |

| 20.3 |

| 208.7 |

| The Hain Celestial Group ( HAIN ) |

| 33.2 |

| 11.2 |

| 16.1 |

| Dole ( DOLE ) |

| 10.1 |

| 5.1 |

| 6.3 |

| Post Holdings ( POST ) |

| 18.1 |

| 7.8 |

| 10.1 |

Takeaway

Based on the data provided, it seems to me as though John B. Sanfilippo & Son remains in something of a rough patch. While this is regretful, the company's bottom line figures are robust and shares look decently priced. The stock has gotten cheaper, but with the drop in revenue and uncertainty about the future, I would say that a ‘hold’ rating still makes the most sense at this point in time.

For further details see:

John B. Sanfilippo & Son Hasn't Fallen Enough To Warrant Another Crack At Things