JCI - Johnson Controls: Powering The Future Of Infrastructure Spending

2023-11-22 05:28:31 ET

Summary

- JCI’s strong growth is primed to continue on this trajectory, with a business model pivot positioning the company well to benefit from increased services revenue (recurring) and the decarbonization trend.

- Further, the increased demand for “smart building” technologies, alongside the need for infrastructure modernization, should also support consistent revenue growth in the coming years.

- JCI’s margins are noticeably below its peers, although with scope for improvement as JCI focuses on higher-margin segments and as its recurring revenue segment comprises a larger portion of revenue.

- JCI’s quarterly results are strong, with backlog growing well and decarbonization outperforming the wider business. We believe the company’s growth story looks extremely positive.

- JCI valuation, particularly when compared to its historical average, implies value at the current share price. At an FCF yield of ~7%, we consider the stock a buy.

Investment thesis

Our current investment thesis is:

- JCI is a high-quality business with deep expertise and significant scale, positioning it as a leading player in the decarbonization transition and the adoption of smart technologies within buildings. Underpinning this is its growing services segment, creating greater revenue certainty and superior unit economics.

- We expect healthy growth and margin appreciation in the coming years, which will drive shareholder value. At a FCF yield of ~7%, investors can already win today.

Company description

Johnson Controls International (JCI) is a diversified company providing building products, technologies, and solutions. It operates through multiple segments, including Building Solutions North America, Building Solutions EMEA/LA, Building Solutions Asia Pacific, and Global Products.

Share price

JCI's share price performance has been respectable, returning over 90% to shareholders inclusive of distributions. This has lagged behind the market, however, owing to a divergence in recent quarters as the market has been held up by a small handful of tech businesses.

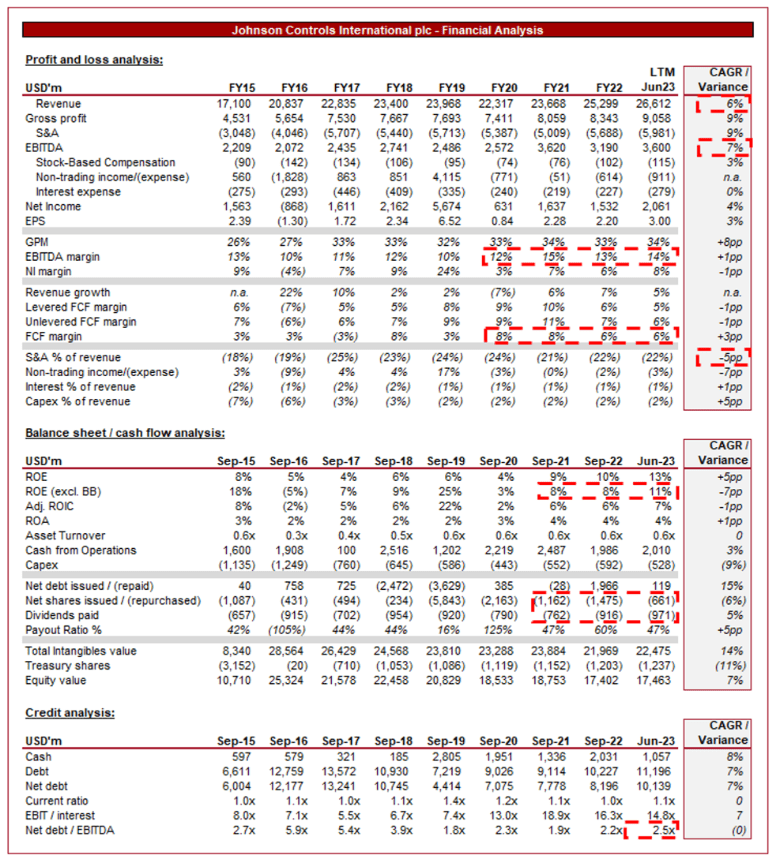

Financial analysis

Johnson Controls International Financials (Capital IQ)

{kind=link}

Presented above are JCI's financial results.

Revenue & Commercial Factors

JCI's revenue has grown well during the last decade, partially supported by M&A, with a CAGR of +6% into the LTM. In conjunction with this, EBITDA has tracked well, with a CAGR of +7%.

Business Model

JCI is a leader in building technologies and solutions. It provides HVAC systems, building automation, security systems, Fire and Security services, and other solutions to enhance the efficiency and sustainability of buildings. This diversity has helped JCI support differing markets, improving diversification.

In conjunction with its core "installation" services, the company has developed a range of "services" that it sells over time, such as maintenance and inspections. These services are highly important to the long-term success of the company, as margins are higher and it's a recurring revenue stream. This reduces the cyclicality of JCI, as the company is less reliant on infrastructure spending.

JCI has developed a leading market presence through innovation, expertise, and scale, with a strong global presence and operations in numerous countries. This global footprint supports to legitimize the company as a market leader, contributing to a greater scope for growth and brand development.

Sustainability and decarbonization is a key aspect of JCI's business model going forward. The company provides energy-efficient solutions for buildings, leaning heavily into the wider environmental sustainability cause. This is an important growth area in our view, particularly in the coming decades as countries move toward their net-zero targets.

Further, JCI is invested heavily in its smart building capabilities, seeking to develop new solutions and integrate IoT (Internet of Things) devices into its offerings, aligning with the growing trend of smart buildings.

Similarly to other large peers, JCI has engaged in strategic acquisitions to strengthen its portfolio and expand its market reach. This is a core component of its business model and continues to successfully drive value for the business incrementally.

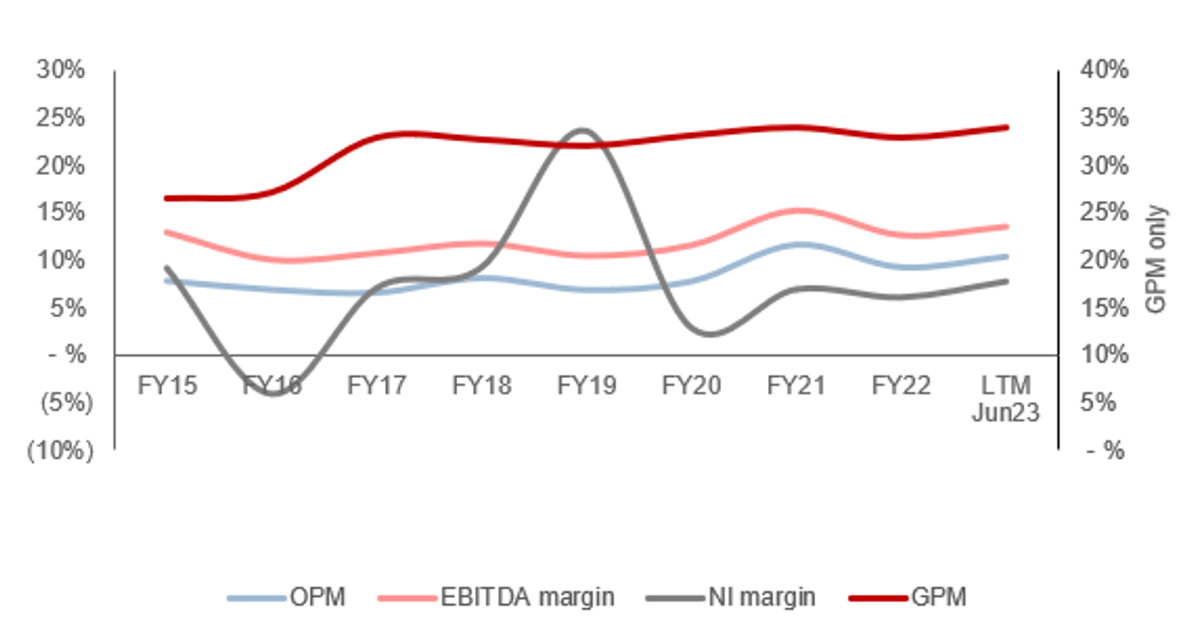

Margins

{kind=link}

JCI's margins have progressed well during the last decade, with EBITDA-M increasing from ~10-13% to consistently in excess of 12%. Margin improvement is a reflection of Management's focus on high-margin services, seeking to streamline the company and remove non-core segments.

Further, the company has benefited from positive pricing action and operational improvements driving cost leverage. We suspect the benefits of this will soften in the coming quarters, although with inflation declining, JCI is positioned well to retain its gains.

Quarterly results

JCI's recent performance has been strong, with top-line revenue growth of +5.2%, +3.5%, +9.6%, and +7.8% in its last four quarters (10 successive quarters of >2.5% growth). In conjunction with this, margin growth has softened, slightly impacted by negative product mix.

The company's strong growth is a reflection of broader spending momentum, with growth across various segments of the company. Building solutions backlog grew 8% in its last quarter, as long-term planning and required capital expenditure offset the impact of near-term macroeconomic headwinds. There is a strong push across the West to invest in the improvement and enhancement of infrastructure, front-run by the IIJA.

Further, JCI's focus on developing its services segment, which is positioned to be incredibly valuable to its wider business model through less volatile revenue generation, has continued to outperform, growing by +12% in its last quarter.

Additionally, as discussed above, the company is seeing its decarbonization efforts materialize into strong revenue contribution, with LTM orders up +20% and strong momentum. With Management expecting this to be a ~$240b opportunity, the runway for a continuation of this momentum is high.

Finally, JCI continues to see positive price/volume mix gains, with price contributing +8% and volume offsetting at (2)%. These factors have allowed the business to primarily drive its growth organically, an impressive achievement in a mature industry at a substantial scale.

The company has seen offsetting softness in its residential segment, as consumers have experienced negative pressure on their living costs due to inflation and interest rates. This is dissuading large ticket purchases, not only in the capital expenditure segment but also in the acquisition of new homes. This will likely continue into FY24 as rates remain elevated in the coming quarters. For this reason, we expect JCI's quarterly results to be slightly weighed down, although its impressive momentum suggests it can maintain MSD growth.

JCI recently announced that it had delayed its Q4 earnings to the 14th December due to a cyberattack, which has caused " disruptions to portions of the company's systems that support or provide data used in financial reporting ". It is unclear if any client-related data was taken, although Management has not indicated this to be the case. This represents a small risk, although we are not in a position to speculate.

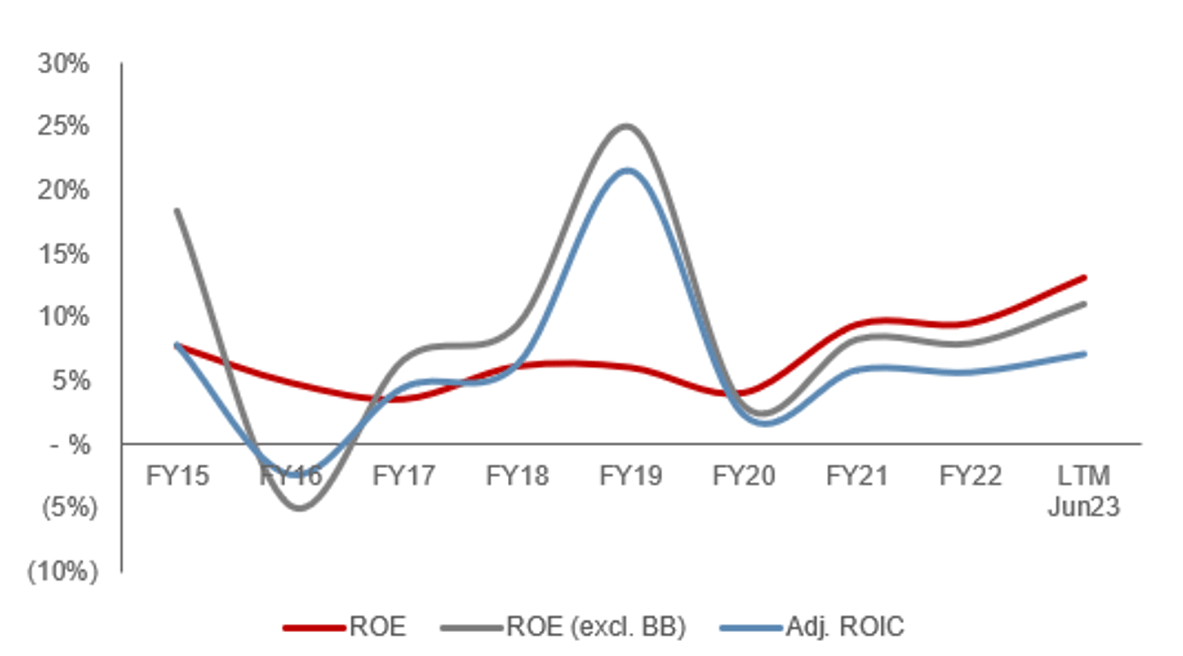

Balance sheet & cash flows

JCI is moderately financed, with a ND/EBITDA ratio of 2.5x. Management's capital allocation policy is well balanced, with strong shareholder distributions alongside consistent M&A activity. This allows the business to protect its long-term growth story alongside rewarding shareholders with its impressive FCFs.

{kind=link}

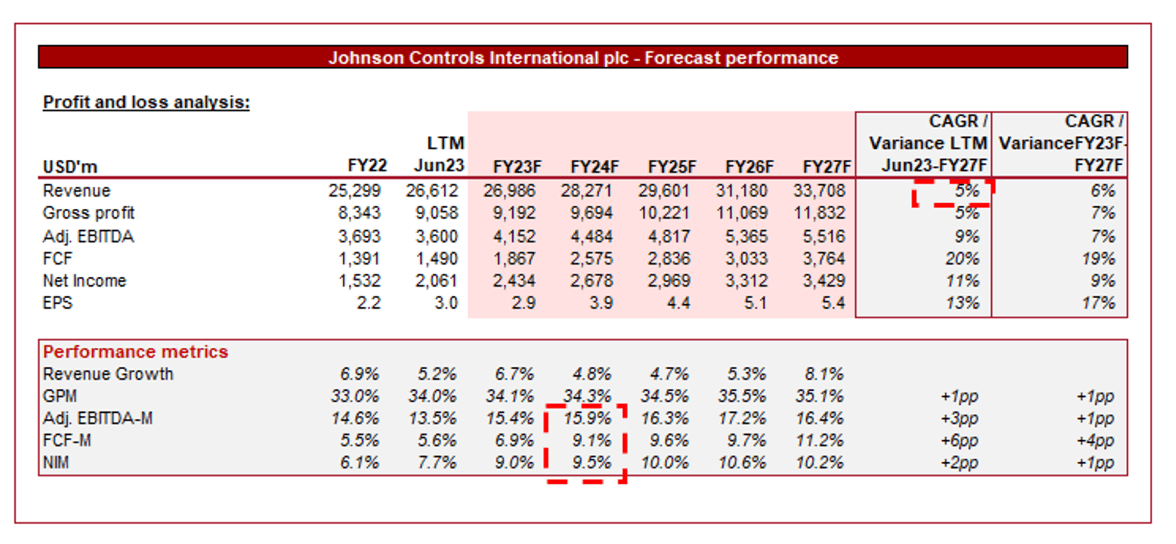

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its current growth trajectory, with a CAGR of +5% into FY27F. Alongside this, margins are expected to sequentially improve.

We broadly concur with this assessment. With multiple growth levers, namely decarbonization and infrastructure spending, alongside its non-cyclical nature and economic growth, the business is positioned well to deliver this. Further, its focus on high-margin segments and growing its services should allow for margins to increase.

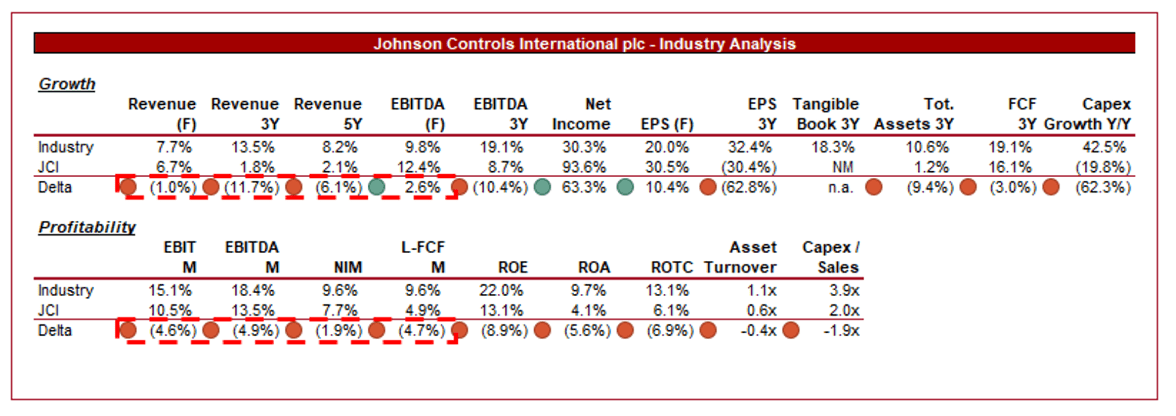

Industry analysis

Building Products Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of JCI's growth and profitability to the average of its industry, as defined by Seeking Alpha (37 companies).

JCI's financial performance relative to its peers is fairly underwhelming. The company is lacking in both growth and margins when compared, contributing to a noticeably lower ROTC/ROE.

This is a reflection of differences in solutions provided and the scope for value development through such factors as innovation, limiting JCI's ability to earn higher unit economics. This said, there is inherently an underperformance baked in here, as a business of its size and capabilities should be more profitable.

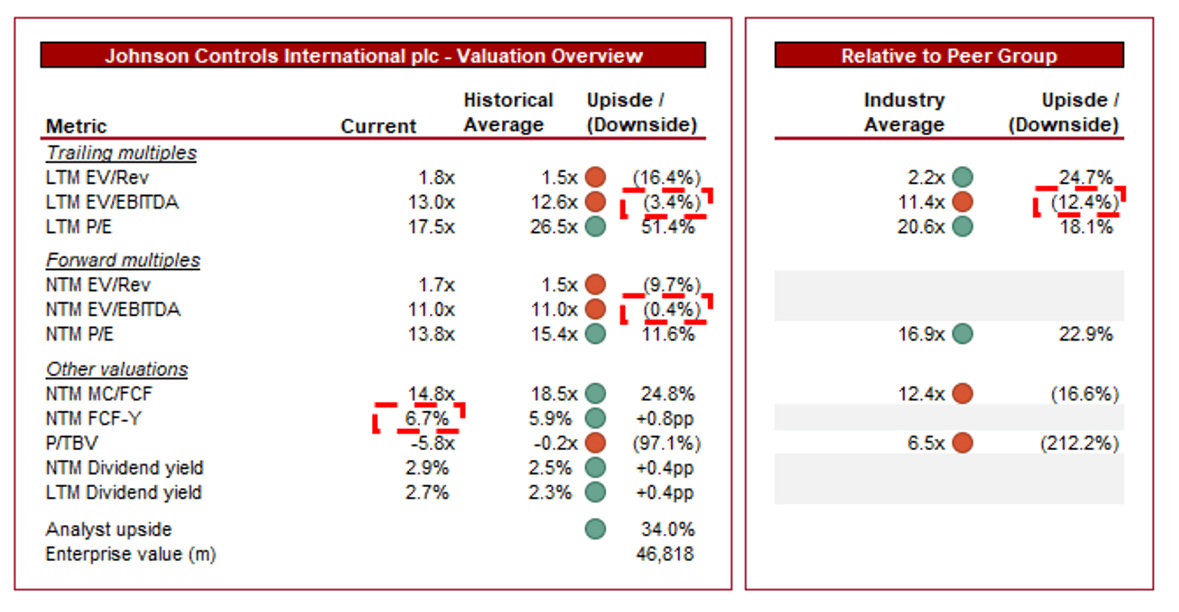

Valuation

{kind=link}

JCI is currently trading at 13x LTM EBITDA and 11x NTM EBITDA. This is broadly in line with its historical average.

A premium to its historical average is warranted in our view, owing to the streamlining of the company and the development of new technologies, positioning the company well for healthy growth in the coming years alongside margin appreciation. From a downside perspective, the business has limited weaknesses compared to its average position during the last decade, at least implying it is within range of its fair value.

Further, JCI is trading at a discount to its peers on a P/E basis, both LTM and NTM, although this is not the case on a LTM EBITDA or NTM FCF basis. A discount to its peers is warranted in our view, principally due to the financial weakness experienced, although its relative performance over the coming 5 years may exceed the average.

Overall, we believe the stock is undervalued. Confirming this for us is its FCF yield, which is an impressive ~7% and above its historical average. Given the distribution track record of the business, this directly translates to shareholder value.

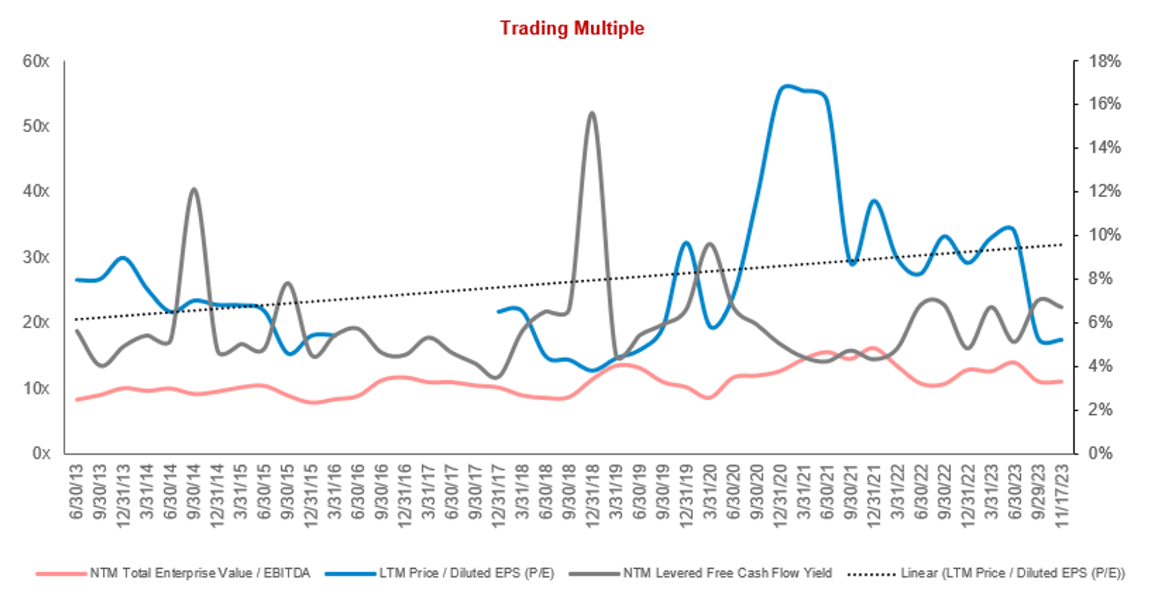

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Extended economic difficulties affecting the construction industry.

- Intense competition limiting margin improvement.

- Value destructive M&A.

Final thoughts

JCI is a high-quality business in our view, owing to its strong market position and industry tailwinds supporting the sustainability of revenue growth. With increased infrastructure spending, decarbonization, and smart technology demand in particular, we see MSD/HSD growth in the coming decade with limited volatility. When partnered with sequential margin improvement, we see strong value in the coming years.

For further details see:

Johnson Controls: Powering The Future Of Infrastructure Spending